- Plastics, Polymers & Resins

- Powder Polyester Resins Market

Powder Polyester Resins Market Size, Share, and Growth Forecast 2026 - 2033

Powder Polyester Resins Market by Resin Type (Unsaturated, Saturated, Other), Technology (TGIC, TGIC-Free), Application (Decorative Coatings, Protective Coatings, Automotive Coatings, Electronics & Electrical Coatings, Other), and Regional Analysis for 2026-2033

Powder Polyester Resins Market Size and Trend Analysis

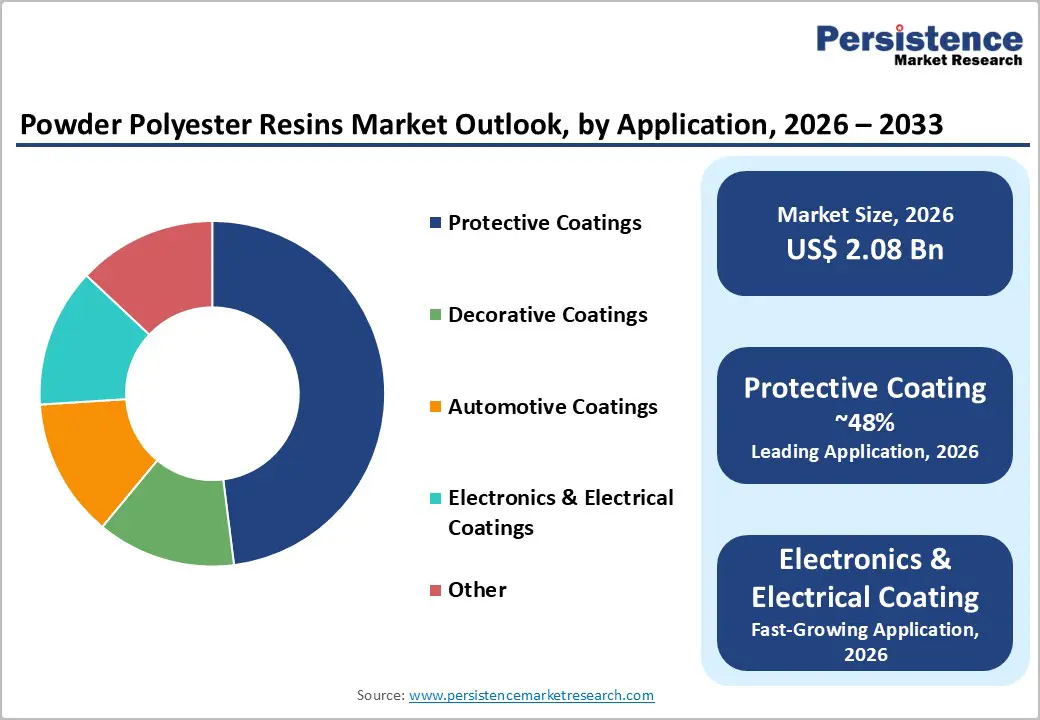

The global powder polyester resins market size is supposed to be valued at US$ 2.1 billion in 2026 and is projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. The powder polyester resins market is experiencing robust expansion driven by escalating demand for sustainable, low-VOC (volatile organic compound) coating solutions across automotive, construction, and electronics sectors.

Environmental regulations such as EU REACH regulations limiting VOC emissions to ≤35g/m³ for industrial coatings and China GB 37824 standards enforcing ≤50g/m³ for automotive coatings as of January 2024 are compelling manufacturers to transition from liquid to powder formulations. Additionally, the global automotive industry's shift toward electric vehicles (EVs) necessitates specialized coatings for battery casings and electrical components, creating substantial demand for high-performance powder polyester resins that offer superior durability, chemical resistance, and thermal stability without compromising environmental standards.

Key Industry Highlights:

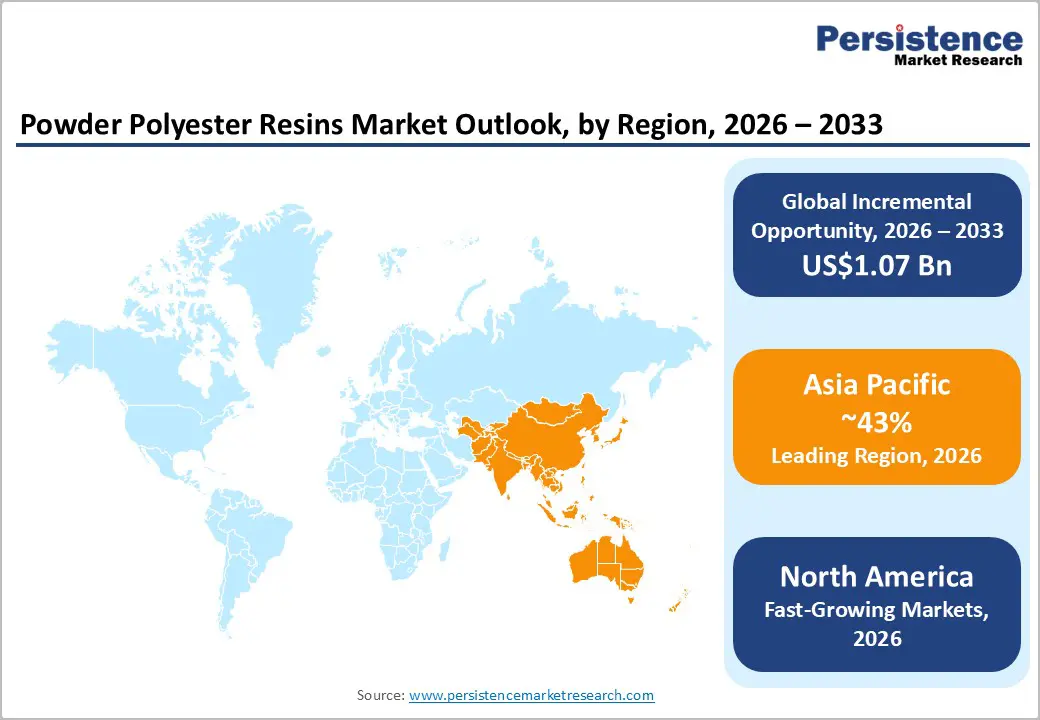

- Regional Leadership: Asia Pacific dominates the powder polyester resins market globally, accounting for approximately 43% of incremental market growth and emerging as the highest-demand region through 2033.

- Fastest Growing Region: North America represents the fastest-growing regional market for powder polyester resins, supported by stringent VOC regulations, strong automotive innovation, and the rapid electrification of the vehicle fleet.

- Leading Segment: Protective coatings dominate the application landscape with approximately 48% market share, delivering superior corrosion protection and durability enhancement across industrial equipment, infrastructure, and metal component finishing applications.

- Fastest Growing Segment: Electronics & electrical coatings represent the fastest-growing application segment, expanding at 7.2% CAGR through 2033, driven by advanced driver assistance systems, sophisticated infotainment electronics, and high-voltage component protection requirements.

- Key Market Opportunity: Sustainable bio-based resin technology development presents exceptional market opportunity potential, supported by regulatory mandates and corporate sustainability commitments, enabling premium market positioning for manufacturers implementing innovative renewable feedstock formulations.

| Key Insights | Details |

|---|---|

| Powder Polyester Resins Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 3.1 Bn |

| Projected Growth CAGR (2026-2033) | 6.1% |

| Historical Market Growth (2020-2025) | 5.2% |

Market Dynamics

Drivers - Environmental Regulatory Compliance and VOC Reduction Initiatives

Regulatory frameworks, including the European Union’s REACH and Industrial Emissions Directive, along with national sustainability mandates, are increasingly requiring manufacturers to eliminate volatile organic compound (VOC) emissions from coating processes. Powder polyester resins, which release nearly zero VOCs during application and curing, provide a compliant and efficient alternative that enables manufacturers to maintain performance standards while avoiding regulatory penalties.

In North America, varying state regulations, such as California’s stringent 50 g/L VOC limit compared with Texas’s 380 g/L allowance, create fragmentation that reinforces the appeal of powder coatings as a universally compliant option. Adoption is further accelerated by the EU’s focus on circular economy principles, exemplified by Arkema’s 2024 initiative incorporating up to 40% recycled PET to achieve a 20% carbon-footprint reduction. Additionally, these regulations enhance worker safety by eliminating hazardous air pollutants associated with solvent-based systems.

Automotive Industry Electrification Driving Specialized Coating Demand

The global shift toward electric vehicle (EV) production is driving significant demand for specialized powder polyester resin coatings designed to meet the distinct protection requirements of EV components. Battery systems in particular require coatings that provide electrical insulation, effective thermal management, and resistance to electrolyte exposure, areas in which powder polyester resins outperform conventional liquid coatings. Europe’s strong position in EV manufacturing, supported by expanding production facilities in Germany, France, and Italy to meet the 2035 internal combustion engine phase-out mandate, is contributing to rising powder coating consumption.

In the United States, automotive output reached 10.06 million units in 2022, a 10% increase from 2021, with continued growth projected by the National Automobile Dealers Association. This trend supports increasing demand for powder polyester resins in both conventional automotive finishing and EV-specific applications. Their superior durability, chip resistance, and corrosion protection make powder coatings ideal for underbody structures, chassis components, and exterior trim, which require long-lasting performance and visual appeal throughout the vehicle lifecycle.

Restraints - Film Thickness Limitations Restricting Application Scope

Powder polyester resin coatings are constrained by inherent technical limitations related to achievable film thickness, particularly in TGIC-free formulations. These systems release water vapor during curing, which can create pinhole defects when film thickness exceeds approximately 4.0–5.0 mils. While TGIC-based coatings can achieve film thicknesses ranging from 1.5 to 10 mils, the industry’s transition toward TGIC-free alternatives, driven by toxicity concerns, reduces suitability for applications requiring thick protective layers, such as heavy industrial and marine environments. This limitation places powder coatings at a disadvantage compared with advanced water-based liquid coatings, which can be uniformly applied to complex geometries and thin substrates without similar restrictions. Consequently, applications demanding ultra-thin films, multi-layer finishes, or coating of intricate assembled components remain challenging, limiting powder coating adoption in sectors like consumer electronics, precision instruments, and decorative architectural elements.

Higher Curing Temperature Requirements Increasing Energy Costs

Powder polyester resins, particularly TGIC-free formulations based on β-hydroxyalkyl-amide (HAA) crosslinkers, require minimum curing temperatures around 335°F (168°C) compared to TGIC variants that cure at 275°F (135°C). These elevated temperature thresholds translate to increased energy consumption, longer curing cycles, and substrate compatibility limitations that exclude heat-sensitive materials such as certain plastics, wood composites, and pre-assembled components containing temperature-sensitive elements.

Rising energy costs globally, compounded by industrial decarbonization pressures to reduce fossil fuel consumption, intensify the economic burden of powder coating operations. The 20°F higher curing temperature typical for HAA-based systems compared to alternatives constrains adoption in cost-sensitive markets and applications where substrate heat tolerance represents a critical limitation, creating market segmentation favoring liquid low-bake or ambient-cure coating technologies.

Opportunities - Infrastructure Development Programs Expanding Architectural Coating Applications

Government-led infrastructure development programs across emerging economies, particularly India’s rapid expansion of residential, commercial, and industrial construction supported by new industrial parks and logistics hubs, are creating significant growth opportunities for powder polyester resins in architectural applications. The Polyester Polyols Market, which supplies key raw materials for polyester-based systems, including powder coating resins, highlights strong value-chain integration as construction activity accelerates.

Powder coatings offer substantial advantages such as high durability, resistance to UV exposure and weathering, and superior aesthetic flexibility compared with traditional liquid coatings, while also supporting compliance with sustainability certification standards. Buildings incorporating powder-coated components can earn LEED and other green-building credits, making them attractive to environmentally focused developers. The long service life and minimal maintenance requirements of powder-coated architectural elements reduce total ownership costs, especially for large-scale infrastructure projects where maintenance access is challenging.

Technology Innovation in TGIC-Free Formulations Expanding Market Accessibility

Continuous advancements in TGIC-free powder polyester resin chemistry are effectively addressing historical performance limitations while eliminating the toxicity concerns associated with traditional triglycidyl isocyanurate crosslinkers. Recent formulation innovations have enhanced electrostatic charging behavior, improved transfer efficiency, reduced material waste by 15–20%, and strengthened penetration into Faraday cage regions that previously posed application challenges. The Silicone Modified Polyester Resin market further extends applicability by offering superior weatherability and flexibility for demanding exterior conditions and flexible substrates.

In parallel, technology providers are developing lower-temperature-curable powder coating systems, with some HAA-based formulations achieving full cure at 392°F (200°C) within five minutes, thereby reducing energy consumption and enabling application on moderately heat-sensitive substrates. Innovations in the Polyester Resin Dispersion market also contribute to competitive pressure, driving improved smoothness, gloss control, and batch-to-batch consistency, further reinforcing the competitiveness of powder coating technologies over liquid alternatives.

Category-wise Analysis

Resin Type Insights

Saturated polyester resins dominate the powder coating market, commanding approximately 55% market share within the polyester resin category due to their superior weatherability, flexibility, and chemical resistance characteristics. Saturated polyester formulations exhibit exceptional outdoor durability, making them indispensable for architectural applications, including pre-coated metal, window frames, and building facades exposed to harsh environmental conditions.

The technical advantages of saturated resins, including superior adhesion properties, reduced susceptibility to color fading, and enhanced cross-link density following thermal curing, position them as the preferred choice for long-service-life applications where coating durability directly impacts product lifecycle costs and customer satisfaction. Unsaturated polyester resins, while representing approximately 40% of market share, find greater application in indoor decorative coatings and electronics where outdoor weathering is not a primary requirement, though their lower cost and faster curing characteristics maintain steady demand across cost-sensitive applications.

Technology Insights

TGIC-based polyester technology maintains market dominance with approximately 62% market share, despite ongoing regulatory scrutiny and health concerns surrounding isocyanurate cross-linkers. TGIC's superior reactivity, excellent mechanical properties, and proven performance across diverse applications have established this technology as the industry standard for decorative and protective coatings requiring high durability specifications. However, the competitive landscape is shifting toward TGIC-free alternatives, which currently capture approximately 38% market share and are experiencing accelerated adoption in response to occupational health regulations, particularly in Europe, where worker exposure limits are increasingly stringent.

TGIC-free polyester resins, formulated with alternative cross-linkers such as polyisocyanates and cycloaliphatic amines, are gaining market acceptance as manufacturers invest in research and development to achieve performance parity with conventional TGIC systems. This technology transition is expected to reshape competitive dynamics, with companies achieving rapid commercialization of robust TGIC-free formulations positioned to capture market share from traditional providers.

Application Insights

Protective coatings constitute the largest application segment, accounting for approximately 48% of the market, driven by strong industrial demand for corrosion resistance and enhanced durability in metal infrastructure. Powder polyester resin–based protective coatings deliver high resistance to environmental degradation, moisture penetration, and chemical exposure, thereby extending asset lifecycles and reducing maintenance requirements. This segment includes infrastructure protection, industrial equipment coatings, marine applications, and utility sector needs.

Automotive coatings represent the second-largest segment at around 32%, covering OEM finishing, primer surfacers, and clear topcoats for various vehicle components. Demand in this segment continues to rise with the expansion of electric vehicles, which require specialized coatings for battery enclosures and high-voltage components. Electronics and electrical coatings form the fastest-growing subsegment, with a projected 7.2% CAGR through 2033, driven by requirements for ADAS technologies, infotainment systems, and centralized control units.

Regional Insights

North America Powder Polyester Resins Market Trends

North America represents the fastest-growing regional market for powder polyester resins, supported by stringent VOC regulations, strong automotive innovation, and the rapid electrification of the vehicle fleet. Regulatory measures, including EPA emissions standards and NFPA coating booth safety guidelines, have driven widespread adoption of low-VOC coating technologies, thereby strengthening market penetration for powder polyester resins. The U.S. leads regional demand, accounting for an estimated 64.6% share of powder coating equipment consumption in 2024, reflecting robust infrastructure development and industrial coating use. In February 2025, PPG Industries Inc. announced major investments in its powder coatings portfolio, reinforcing its strategic focus on sustainable growth.

The region’s commitment to eco-friendly technologies and advancements in powder resin applications, particularly for electric vehicles and lightweight construction materials, continues to support strong market expansion. Canada also demonstrates solid growth, with a market valuation of US$133.2 million in 2024 and a projected 6.2% CAGR through 2034, driven by increasing environmental awareness and demand across the automotive, furniture, and construction sectors.

Europe Powder Polyester Resins Market Trends

Europe represents the most mature market for powder polyester resins, distinguished by stringent regulatory frameworks and advanced technological adoption. The European Union’s REACH and environmental directives have positioned the region as the global leader in the transition toward TGIC-free technologies, prompting widespread use of HAA-based formulations for compliance. Germany, the United Kingdom, France, and Spain exhibit strong industrial coating demand, driven by advanced automotive production, aerospace applications, and architectural finishing needs.

Recent regulatory harmonization across the EU has established uniform emission and product safety standards, supporting market consolidation and technological standardization. European manufacturers continue to pioneer sustainable resin innovations, including PFAS-free texture agents and bio-based formulations, reinforcing the region’s role as the innovation hub for powder polyester resins through 2033.

Asia Pacific Powder Polyester Resins Market Trends

Asia Pacific dominates the powder polyester resins market globally, accounting for approximately 43% of incremental market growth and emerging as the highest-demand region through 2033. China maintains a dominant regional market share supported by the world's largest automotive production capacity, extensive appliance manufacturing, and aggressive construction activity that consume powder coatings at an unprecedented scale.

India represents the fastest-growing market, propelled by strong construction and automotive sectors, government-led modernization initiatives, and rising middle-class incomes. Japan and South Korea continue to advance resin formulation technologies, while ASEAN economies such as Indonesia and Thailand experience accelerating industrialization and construction activity. Collectively, the region’s cost-efficient manufacturing environment and expanding consumer base position Asia Pacific as the primary global growth engine for powder polyester resins.

Competitive Landscape

The powder polyester resins market exhibits a fragmented competitive structure, led by major multinational chemical companies supported by specialized regional manufacturers. Global players such as DIC Corporation, Arkema SA, DSM-Firmenich, BASF SE, PPG Industries, Inc., and The Sherwin-Williams Company maintain significant market share through extensive production capabilities, advanced R&D infrastructure, and established distribution networks. Market concentration is reinforced by high entry barriers, including substantial capital investment, specialized expertise in resin chemistry, and stringent regulatory compliance requirements. Competitive strategies increasingly focus on developing sustainable, low-VOC formulations, expanding into high-growth emerging markets, forming strategic collaborations with equipment manufacturers, and differentiating through advanced curing technologies. Key competitive advantages include proprietary resin chemistries, transfer-efficiency performance, environmental certifications, and strong technical support. Rising investments in bio-based resin technologies and strategic acquisitions are expected to accelerate market consolidation through 2033.

Key Developments:

- September 2024: Akzo Nobel commenced commercial production at its newly established powder coatings facility in Gwalior, India, enhancing supply capabilities in the region and demonstrating major manufacturer commitment to Asia Pacific capacity expansion.

- February 2025: PPG Industries Inc. announced significant portfolio investments in powder coatings technology, positioning it as a core strategic component of sustainability-focused sales growth initiatives and innovation in specialized applications.

- April 2024: BASF coatings division launched a new generation of clear coats and undercoats specifically formulated for the Asia Pacific refinish market, delivering higher quality, increased productivity, and significant CO2 emission reductions through advanced formulation chemistry.

Top Companies in the Powder Polyester Resins Market

BASF SE (Ludwigshafen, Germany) represents a global chemical industry leader with extensive polyester resin portfolios serving diverse industrial coatings applications across automotive, electronics, and protective coating segments. The company demonstrates technological excellence in sustainable resin formulations and maintains significant production capacity across North America, Europe, and the Asia Pacific regions.

PPG Industries, Inc. (Pittsburgh, U.S.) operates as a premier coatings and specialty materials manufacturer with comprehensive powder polyester resin capabilities and advanced application technologies for automotive, industrial, and architectural coating solutions. The company exhibits strong market presence through integrated coating systems solutions and continuous product innovation investments.

Arkema SA (Colombes, France) specializes in high-performance coating resins with particular expertise in sustainable polyester formulations and advanced TGIC-free systems for environmentally conscious applications. The company maintains strong regional presence in Europe and Asia with significant investments in bio-based resin technology development.

Companies Covered in Powder Polyester Resins Market

- DIC Corporation

- Arkema SA

- DSM-firmenich

- BASF SE

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Evonik Industries AG

- Stepan Company

- Karna Paints Pvt. Ltd.

- Akzo Nobel N.V.

- Jotun A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

Frequently Asked Questions

The global powder polyester resins market is projected to reach US$ 3.1 Bn by 2033, expanding from US$ 2.1 Bn in 2026 at a 6.1% CAGR, driven by increasing demand for sustainable, low-VOC coating solutions across automotive, protective, and industrial applications.

Primary demand drivers include stringent environmental regulations promoting low-VOC formulations, rapid expansion of automotive and electronics manufacturing sectors, global shift toward sustainable manufacturing practices, infrastructure development in emerging markets, particularly China and India, and accelerating adoption of electric vehicle technologies requiring advanced protective coatings for battery systems and electronic components.

Protective coating represents the leading application segment with approximately 48% market share, encompassing industrial equipment, infrastructure protection, and corrosion prevention applications.

Asia Pacific dominates the market with the highest demand generation and fastest growth, accounting for approximately 43% of incremental market growth through 2033, driven by rapid industrialization, infrastructure expansion in China and India, manufacturing capacity development, and government sustainability initiatives.

Infrastructure development programs, particularly India's construction investments in residential, commercial, and industrial projects, create substantial opportunities for architectural powder coating applications that meet green building certification requirements while delivering superior durability and lifecycle cost advantages.

Leading market players include BASF SE, PPG Industries, Inc., The Sherwin-Williams Company, Arkema SA, DSM-Firmenich, DIC Corporation, Axalta Coating Systems Ltd., Evonik Industries AG, AkzoNobel NV, and Stepan Company, demonstrating technological leadership through advanced resin formulations, sustainable solutions development, and geographic market expansion strategies.