- Processed Food

- Organic Fish Market

Organic Fish Market Size, Share, and Growth Forecast, 2026 - 2033

Organic Fish Market by Product Type (Salmon, Tuna, Trout, Others), Form (Fresh, Frozen, Processed), Distribution Channel (Off-Trade, On-Trade), and Regional Analysis for 2026 – 2033

Organic Fish Market Size and Trends Analysis

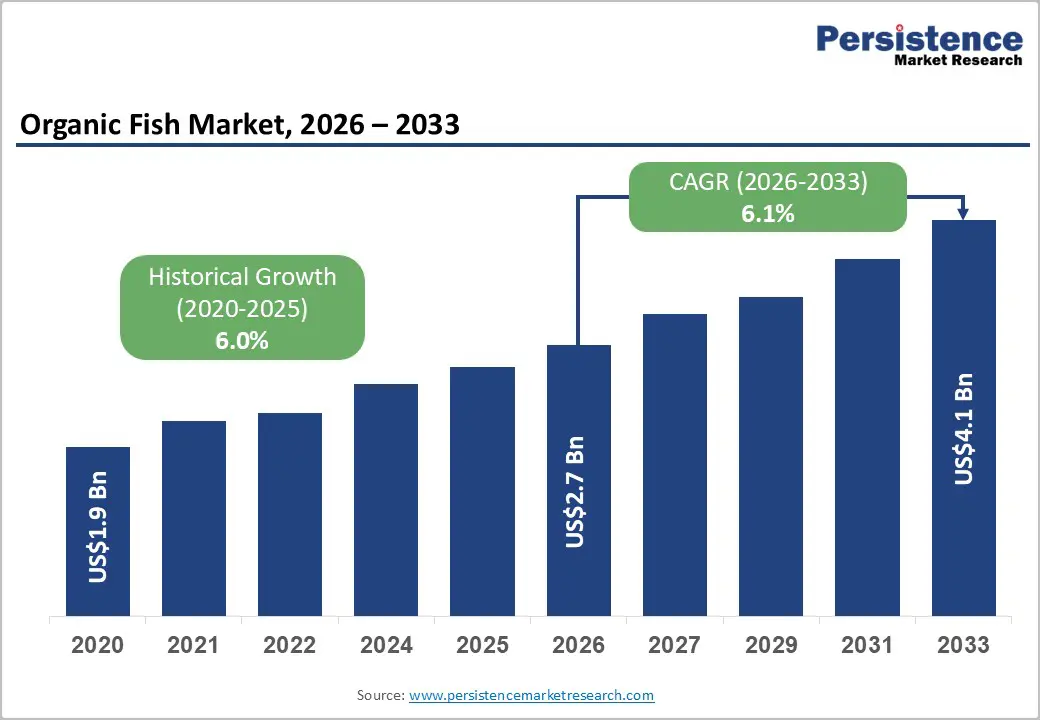

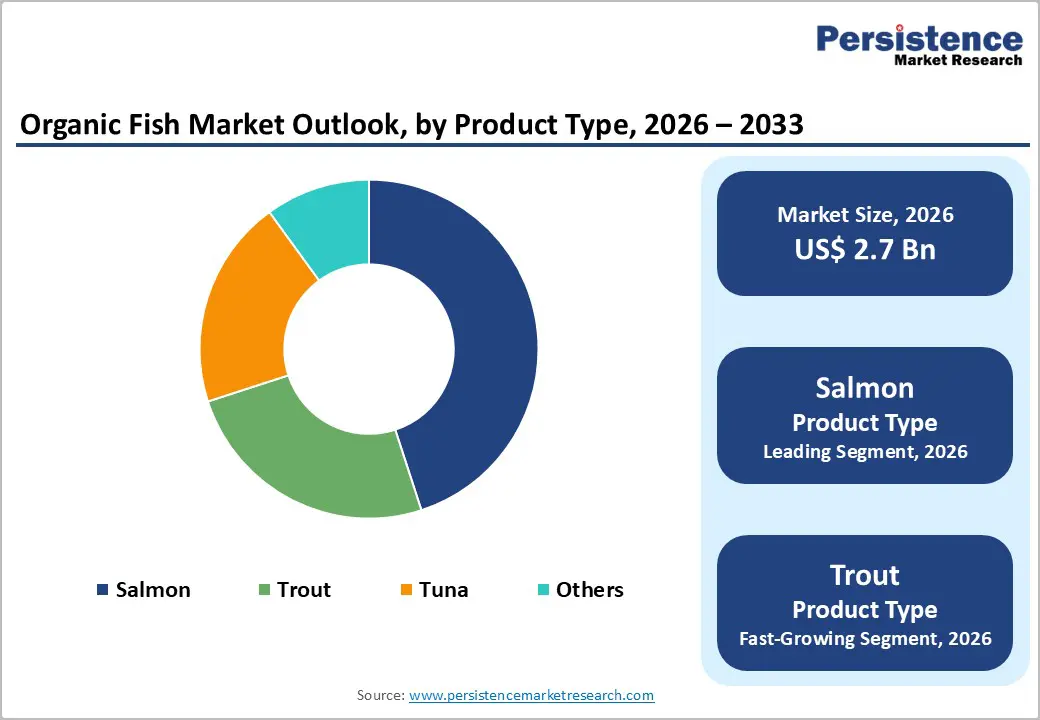

The global organic fish market size is likely to be valued at US$2.7 billion in 2026, and is expected to reach US$4.1 billion by 2033, growing at a CAGR of 6.1% during the forecast period from 2026 to 2033, driven by the increasing prevalence of health-conscious consumers, rising demand for antibiotic-free and sustainable seafood, and growing retail availability of certified organic fish products.

Growing demand for organic salmon and fresh/frozen formats, especially in North America and Europe, is accelerating adoption across off-trade and on-trade channels. Advances in certified organic aquaculture practices, traceability systems, and eco-friendly feed formulations are further boosting uptake by offering better nutritional profiles and environmental credentials. Increasing recognition of organic fish as critical for clean-label protein, reduced chemical exposure, and ethical consumption in premium and wellness-focused markets remains a major driver of market growth.

Key Industry Highlights:

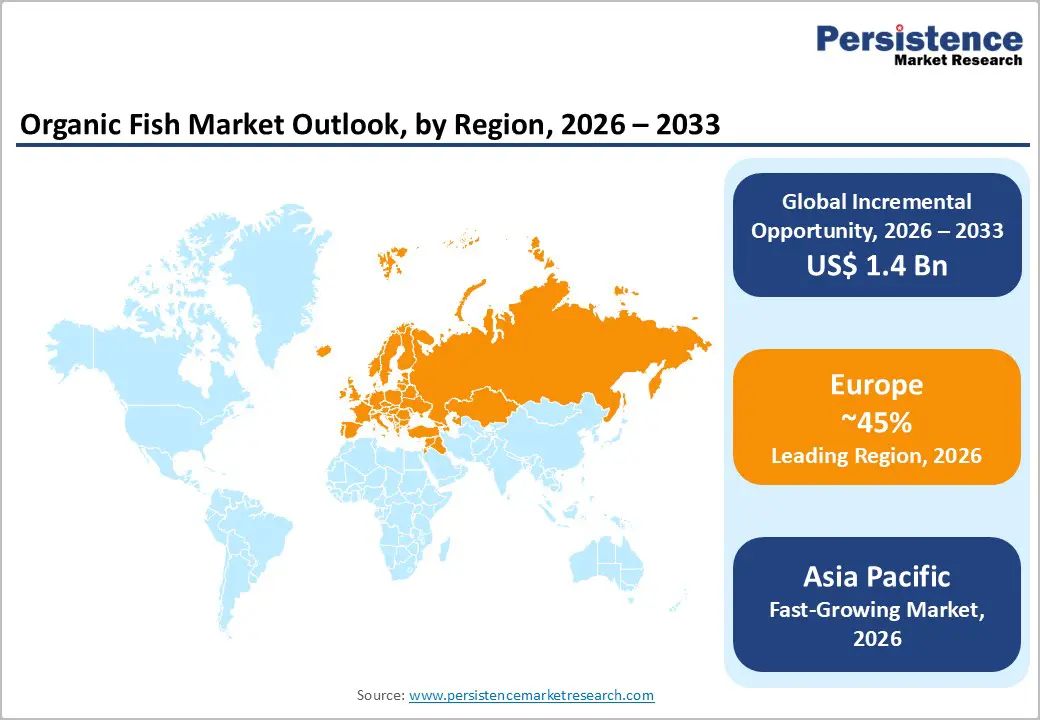

- Leading Region: Europe, anticipated to account for a 45% market share in 2026, driven by strong organic certification standards, high per-capita consumption, and premium demand in Norway, Scotland, and Ireland.

- Fastest-growing Region: Asia Pacific, fueled by rising middle-class health awareness, expanding cold-chain infrastructure, and increasing organic aquaculture investments in China and Vietnam.

- Dominant Product Type: Salmon, to hold approximately 62% of the market share, as it remains the flagship species in certified organic aquaculture.

- Leading Form: Fresh, to contribute nearly 48% of the market revenue, owing to the highest consumer preference for premium quality.

- Rapid Expansion of Organic Aquaculture Volume: Global organic aquaculture production exceeded 510,000?metric?tons in 2023, with Asia representing about 61?% and Europe about 35?% of total volume, highlighting strong regional engagement in organic fish farming.

| Key Insights | Details |

|---|---|

| Organic Fish Market Size (2026E) | US$2.7 Bn |

| Market Value Forecast (2033F) | US$4.1 Bn |

| Projected Growth CAGR (2026-2033) | 6.1% |

| Historical Market Growth (2020-2025) | 6.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Health Consciousness and Premium Protein Demand

Increasing health consciousness and demand for premium protein are key drivers of the organic fish market, with consumers prioritizing nutrient-dense and wholesome foods within balanced diets. Fish is recognized globally as a high-quality source of animal protein that provides all essential amino acids, supporting muscle repair, immune function, and overall health. Government data shows that fish provides about 15% of the global population’s intake of animal protein and about 5% of all protein consumed, underscoring its role in meeting core nutritional needs at scale. Fish also contributes unique micronutrients and healthy fats, adding tangible health value that appeals to health-oriented consumers.

This nutrition positioning has elevated consumer interest in organic and sustainably sourced fish, as buyers seek products perceived as safer and purer alternatives to conventionally farmed options. Organic fish is often associated with reduced chemical exposure and enhanced environmental stewardship, aligning with broader wellness trends. Rising awareness of diet-linked chronic disease prevention and weight management continues to push demand toward lean, premium protein sources such as organic fish. More than 3.1 billion people depend on fish for at least 20% of their animal protein intake, indicating broad recognition of its dietary importance.

Retail Availability and Certification Awareness

Retail availability and certification awareness have significantly expanded the organic fish market by improving consumer trust and broadening access points for purchase. According to the USDA, conventional grocery retailers, including supermarkets, club stores, and supercenters, accounted for 56% of organic food sales by 2020, indicating that certified organic products have moved well beyond niche stores into mainstream retail channels where consumers regularly shop. This widespread presence increases visibility for organic certified items, making it easier for buyers to discover, compare, and choose organic alternatives during routine grocery trips.

Consumer confidence in certification labels further supports market growth as awareness grows around what constitutes authentic organic production and handling. Certified organic logos signal compliance with defined standards, assuring buyers that products meet regulated criteria for organic aquaculture and handling. As more retailers adopt clear labeling practices and educate shoppers about the meaning, purchase decisions are increasingly driven by informed choice rather than assumption. The resulting synergy between broader retail availability and stronger certification awareness enhances demand for organic fish, reinforcing its value proposition in health- and sustainability-oriented consumer segments.

Barrier Analysis – High Production Costs and Limited Supply

Producing certified organic fish requires adherence to stringent standards for feed, water quality, stocking density, and disease management, all of which elevate operational expenses relative to conventional aquaculture. These requirements often lead to slower growth rates, higher feed costs, and reduced yields, making organic fish products more expensive for both producers and end consumers. Limited numbers of certified organic farms and processing facilities restrict overall output, leading to supply shortages that struggle to meet rising demand.

Global fisheries data reported that aquaculture contributed around 50% of the total fish supply for human consumption in recent years, indicating that half of the market still depends on conventional farmed production, with organic segments representing only a small subset of this share. In the U.S., only about 1% of the total aquaculture value was attributed to certified organic products, highlighting how certification costs and limited production scale constrain availability. These cost and supply limitations narrow market accessibility and slow broader adoption of organic fish offerings.

Certification Complexity and Consumer Confusion

Certification complexity and consumer confusion act as significant restraints on the organic fish market by creating barriers to both supply chain participation and informed purchasing. Organic certification for fish involves detailed standards that cover feed sources, water quality, animal welfare, stocking densities, and record-keeping protocols. These standards are enforced by regulatory bodies and third-party certifiers to ensure that products genuinely meet organic criteria from farm to fork. The complexity of these requirements increases administrative costs for producers, who must invest in documentation, audits, and compliance management on top of routine operational expenses. For smaller farms and processors, these burdens can be prohibitive, limiting the number of certified organic fish products available in the market and concentrating supply among larger operators with sufficient resources.

Overlapping labels such as “organic,” “wild-caught,” “sustainably sourced,” and “natural” can create confusion at the point of purchase. Many consumers are uncertain about what each certification signifies, leading to hesitancy or misinformed choices that may undervalue certified organic fish products. Retailers and certification bodies are challenged to communicate distinctions effectively so that shoppers understand the rigorous criteria behind organic designation and its implications for food quality and environmental stewardship.

Opportunity Analysis – Organic Salmon and Traceable Fresh/Frozen Formats

Growing demand for organic salmon and traceable fresh/frozen fish formats presents a clear opportunity in the organic fish market by aligning premium product attributes with enhanced supply chain transparency and food safety assurances. Certified organic salmon carries strong consumer appeal due to perceived quality, sustainable practices, and nutrient density, supporting premium pricing and differentiated retail positioning. Traceability systems that track product origin, handling, and processing from farm or harvest site to point of sale build consumer confidence and reinforce brand integrity for organic and high-value fish products. Government data shows that aquaculture, which includes salmon and other farmed fish, supplies more than 50% of all seafood produced for human consumption, indicating a large and growing base for traceable aquaculture formats to capture consumer interest.

In the U.S., total sales of aquaculture products reached approximately USD1.9 billion in 2023, reflecting expanding production and market scale that organic and traceable fresh/frozen segments can tap into. Traceable fresh/frozen formats allow producers and retailers to document harvesting and processing steps, which supports compliance with safety standards and helps differentiate organic offerings in competitive retail environments. Consumer interest in knowing where and how their food was produced drives preference for products that transparently communicate quality attributes, encouraging retailers to expand shelf space and invest in traceable supply chains for organic fish products.

Expansion in Asia Pacific and Processed Organic Seafood

Rapid economic growth and rising consumer incomes across Asia Pacific are expanding demand for higher-quality and convenient food choices, creating opportunities for processed organic seafood products. Aspiring middle-class consumers in countries such as China, India, and Southeast Asian markets are increasingly prioritizing food safety, nutritional value, and sustainable production methods. These preferences support broader acceptance of organic certified seafood, which is perceived as a premium option that aligns with health and environmental values. As retail infrastructure modernizes with greater penetration of supermarkets, hypermarkets, and e-commerce grocery platforms, processed, ready-to-cook organic seafood formats become more accessible to consumers who seek trustworthy quality and convenience.

Processors in the region are responding by introducing a wider array of organic seafood products, including frozen fillets, pre-seasoned portions, and value-added preparations that reduce meal-time effort while preserving nutritional integrity. Government efforts in some Asia Pacific countries to improve aquaculture practices and enhance food safety oversight further support producers in meeting organic standards and building consumer confidence. Expanding cold-chain logistics and certification frameworks also enable processors to maintain quality from harvest through distribution, encouraging exports and regional trade.

Category-wise Analysis

Product Type Insights

Salmon is anticipated to dominate the market, accounting for approximately 62% of the market share in 2026, driven by its strong global demand, premium positioning, and established aquaculture infrastructure. It is widely recognized for high omega-3 fatty acid content, quality protein, and consistent taste, making it a preferred choice among health-conscious consumers. Well-developed farming systems in Norway, Scotland, Canada, and Chile enable scalable organic salmon production compared to other species. Salmon also adapts effectively to fresh, frozen, and smoked value-added formats, supporting retail and foodservice penetration. Cooke Aquaculture Chile’s “Shima” organic salmon brand, where the company successfully produced and exported 100% certified organic Atlantic salmon that met the European Union’s organic production standards, a first for the Chilean industry. This organic salmon was harvested under strict organic farming practices, including adjusted stocking densities and certified organic feed sourced from affiliated facilities, enabling Cooke to supply premium salmon into the EU and UK markets under recognized organic credentials.

Trout represents the fastest-growing product type, owing to the expanding consumer interest in diverse, healthy seafood alternatives and improved aquaculture practices that support sustainable trout production. Its mild flavor, firm texture, and nutritional profile rich in protein and omega 3 fatty acids make it appealing in both fresh and value?added formats, such as fillets and ready?to?cook portions. Trout farming systems are adaptable to certified organic standards, enabling producers to scale organically with managed water quality and feed inputs. Hima Seafood, a Norwegian company that launched what is described as the world’s largest land?based trout farm in Rjukan, Norway. Their facility welcomed a significant batch of 420,000 trout roe to begin large scale sustainable trout production with advanced water recirculation technology, supporting high?quality trout growth and consistent supply for restaurants, hotels, and retailers.

Form Insights

The fresh segment is expected to dominate, contributing nearly 48% of the revenue in 2026, owing to the strong consumer preference for minimally-processed, nutrient-rich products. Fresh formats preserve natural taste, texture, and nutritional content, including high-quality protein and omega-3 fatty acids, appealing to health-conscious buyers. Improved cold-chain logistics and retail refrigeration infrastructure enable wider distribution of fresh organic fish, ensuring safety and quality from farm to consumer. Pescafresh is an India?based seafood retailer that has built a strong presence in fresh fish delivery across major cities, including Mumbai, Delhi, and Bangalore. Pescafresh has delivered fresh catches such as Norwegian pink salmon and Himalayan trout directly to consumers and partnered with supermarket counters such as Star Bazaar’s gourmet seafood section to offer fresh, high quality seafood in retail settings.

Frozen represents the fastest-growing form, with its extended shelf life, ease of storage, and ability to preserve nutritional quality and freshness during distribution. Freezing enables year-round availability of seasonal fish, supporting consistent supply to retailers, foodservice providers, and e-commerce platforms. Advanced freezing techniques, such as flash-freezing and vacuum-sealed packaging, maintain protein integrity, omega-3 content, and taste, appealing to health-conscious consumers. Thai Union Group PCL is a major global seafood producer known for its wide range of frozen fish and seafood products sold under brands such as Chicken of the Sea and John West. The company supplies frozen tuna, salmon, and other seafood to retail and foodservice channels worldwide, supporting convenience and long shelf life offerings.

Regional Insights

North America Organic Fish Market Trends

Market growth in North America is fueled by the region’s high health & wellness awareness, strong retail infrastructure, and high public demand for clean-label seafood. Distribution systems in the U.S. and Canada provide extensive support for organic fish programs, ensuring wide accessibility across salmon, fresh, and off-trade populations. Increasing demand for certified, convenient, and easy-to-prepare forms is further accelerating adoption, as these formats improve nutritional value and reduce barriers associated with conventional seafood.

Innovation in the organic fish supply chain, including stable traceability, improved frozen delivery, and targeted premium enhancement, is attracting significant investment from both public and private sectors. Government initiatives and USDA campaigns continue to promote use against chemical risks, sustainability concerns, and emerging clean-label threats, creating sustained market demand. The growing focus on frozen grades and specialty uses, particularly for salmon and others, is expanding the target applications for organic fish.

Europe Organic Fish Market Trends

Europe is projected to lead with a market share of 45% in 2026, driven by increasing awareness of organic certification benefits, strong regulatory systems, and government-led sustainable aquaculture programs. Countries such as Norway, the U.K., Ireland, and Scotland have well-established organic fish production frameworks that support routine market growth and encourage adoption of innovative supply methods, including salmon and fresh formats. These high-quality formulations are particularly appealing for fresh populations, regulation-conscious retailers, and food-service users, improving nutritional value and coverage rates.

Technological advancements in organic fish development, such as enhanced land-based systems, application-targeted delivery, and improved frozen grades, are further boosting market potential. European authorities are increasingly supporting research and trials for organic aquaculture against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, ethical options is aligned with the region’s focus on preventive chemical reduction and animal welfare. Public awareness campaigns and promotion drives are expanding reach in both retail and food-service segments, while producers are investing in certification and novel variants to increase efficacy.

Asia Pacific Organic Fish Market Trends

Asia Pacific is likely to be the fastest-growing market for organic fish in 2026, driven by rising health & wellness awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Vietnam, and Japan are actively promoting organic fish campaigns to address protein demand and emerging premium needs. Organic fish is particularly attractive in these regions due to its scalable administration, ease of adoption, and suitability for large-scale retail and food-service drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-distribute organic fish, which can withstand challenging supply-chain conditions and minimize certification dependence. These innovations are critical for reaching domestic retailers and improving overall product coverage. Growing demand for salmon, fresh, and off-trade applications is contributing to market expansion. Public-private partnerships, increased premium protein expenditure, and rising investment in organic aquaculture research and production capacity are further accelerating growth. The convenience of organic fish delivery, combined with improved quality and reduced risk of contaminants, positions it as a preferred choice.

Competitive Landscape

The global organic fish market is characterized by competition between established aquaculture leaders and emerging certified producers who focus on sustainability, quality, and traceability. In Europe and North America, companies such as Mowi ASA and Loch Duart Ltd. maintain leading positions through rigorous organic certification, extensive distribution networks, and strong brand recognition. Their investments in innovative salmon programs and fresh product offerings enhance nutritional value, reduce chemical exposure, and support high-quality consumer experiences.

In the Asia Pacific region, regional players are gaining traction by offering cost-efficient solutions that improve accessibility and address growing demand for organic fish among urban and health-conscious consumers. Salmon products, whether fresh or value-added, support widespread integration across retail and foodservice channels, reinforcing market penetration. Strategic partnerships, joint ventures, and acquisitions are accelerating innovation, expanding product portfolios, and enabling faster commercialization of certified organic fish. Advanced frozen formulations address logistical challenges, maintaining product quality over long distances and supporting export growth.

Key Industry Developments:

- In May 2025, Salmofood, a brand of Vitapro, and Cooke Aquaculture launched RAW, a new organic feed for salmon farming in Chile. The feed was produced at Salmofood’s Castro plant, the first facility in Chile certified for organic salmon feed production and compliant with European Union regulations. The partnership was established to supply Cooke Aquaculture’s organic operations with a locally sourced, high-quality feed. RAW was formulated from organic plant-based ingredients, sustainably sourced marine materials, and natural additives, aiming to enhance sustainability and productivity in organic salmon farming.

Companies Covered in Organic Fish Market

- Mowi ASA

- Loch Duart Ltd.

- Leroy Seafood Group ASA

- SalMar ASA

- Glenarm Organic Salmon Ltd.

- Valhalla Salmon

- The Irish Organic Salmon Company Ltd.

- Dom International Ltd.

- Coombe Farm Organic

- Blue Circle Foods

- Loch Fyne Oysters Ltd.

- Scottish Salmon Company (Bakkafrost)

- Organic Sea Harvest Ltd.

- North Coast Seafoods

- Fish4Ever

- Isle of Skye Smokehouse

- Cooke Aquaculture Inc.

- Solex Catsmo

- Anova Seafood B.V.

Frequently Asked Questions

The global organic fish market is projected to reach US$2.7 billion in 2026.

Increasing consumer focus on nutritious, high-protein diets is driving demand for organic fish, particularly salmon and trout, which are rich in omega-3 fatty acids and essential nutrients.

The organic fish market is poised to witness a CAGR of 6.1% from 2026 to 2033.

Growing consumer demand for premium, traceable seafood supports investment in certified organic salmon and convenient fresh or frozen products, enabling wider market reach and brand differentiation.

Mowi ASA, Loch Duart Ltd., SalMar ASA, Leroy Seafood Group ASA, and Glenarm Organic Salmon Ltd. are the key players.