- Processed Food

- Organic Poultry Market

Organic Poultry Market Size, Share, and Growth Forecast, 2026-2033

Organic Poultry Market by Product Type (Eggs, Meat), Processing Type (Fresh, Frozen, Processed), Distribution Channel (Supermarkets, Specialty Stores, Online Sales, Others), and Regional Analysis for 2026-2033

Organic Poultry Market Share and Trends Analysis

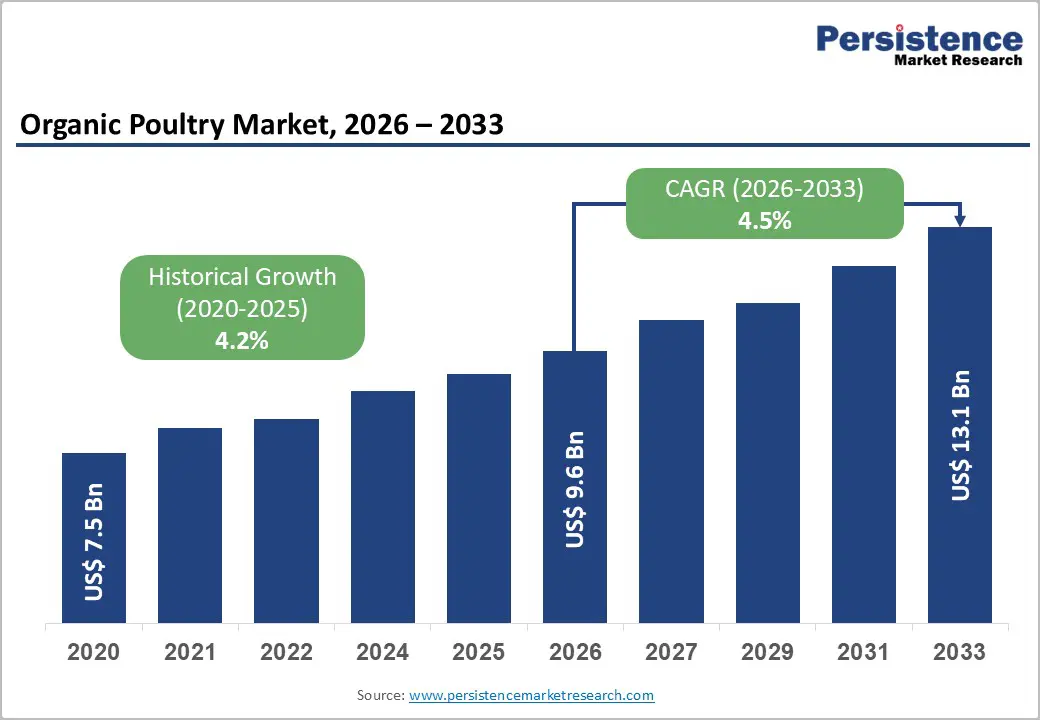

The global organic poultry market size is likely to be valued at US$ 9.6 billion in 2026, and is projected to reach US$ 13.1 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026-2033. Consumers are increasingly demanding organic poultry products that offer clean-label proteins. This shift has driven the global organic poultry market toward steady expansion in recent years.

Health awareness continues to rise, prompting more people to choose antibiotic-free meat and eggs. Regulatory bodies have emphasized these standards, which reshape consumption habits worldwide. Poultry farmers have adopted organic practices more widely, supported by investments in supply chain traceability and processing innovations. Distribution channels, such as supermarkets, specialty stores, and online retail platforms, have expanded to meet this demand, underpinning further market growth by ensuring sustainable access to premium proteins.

Key Industry Highlights

- Dominant Product Type: Organic meat is set to command around 58% of the revenue share in 2026, while organic eggs are likely to grow the fastest at 5.2% CAGR through 2033, driven by rising consumer demand for cage-free variants.

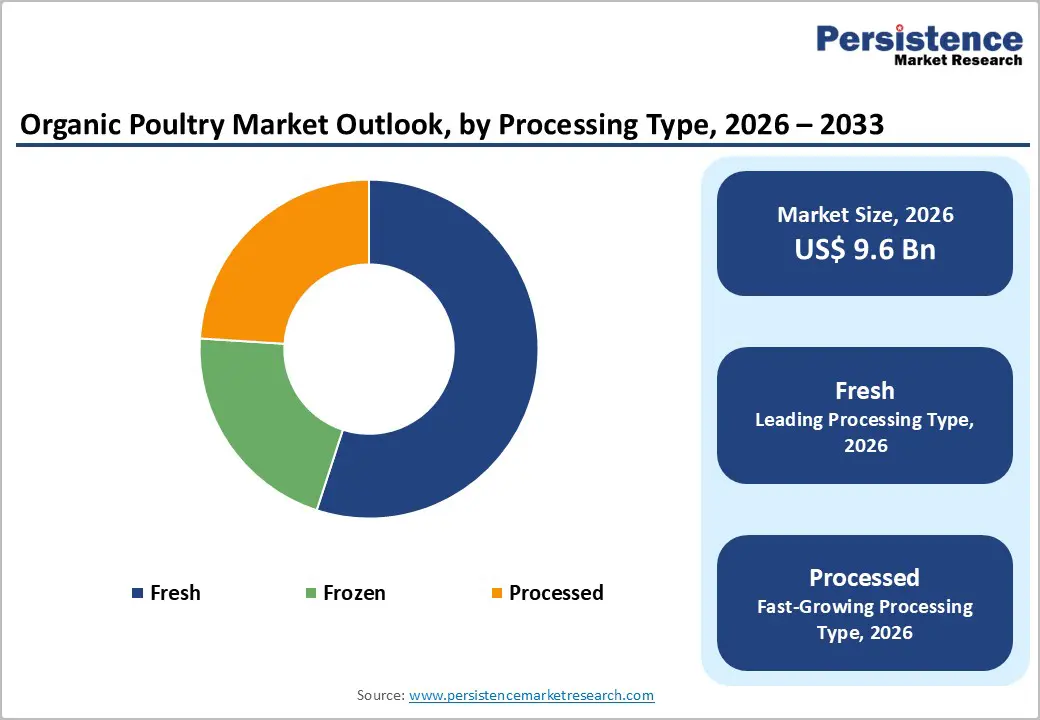

- Leading Processing Type: Fresh organic poultry is expected to lead with an estimated 55% market share in 2026, while processed products are projected to grow fastest at 6.1% CAGR through 2033, reflecting high demand for convenient ready-to-cook options.

- Dominant Distribution Channel: Supermarkets are expected to hold about 62% of the revenues in 2026, while online sales are projected to grow the fastest at roughly 9.3% CAGR from 2026 to 2033, owing to e-commerce expansion.

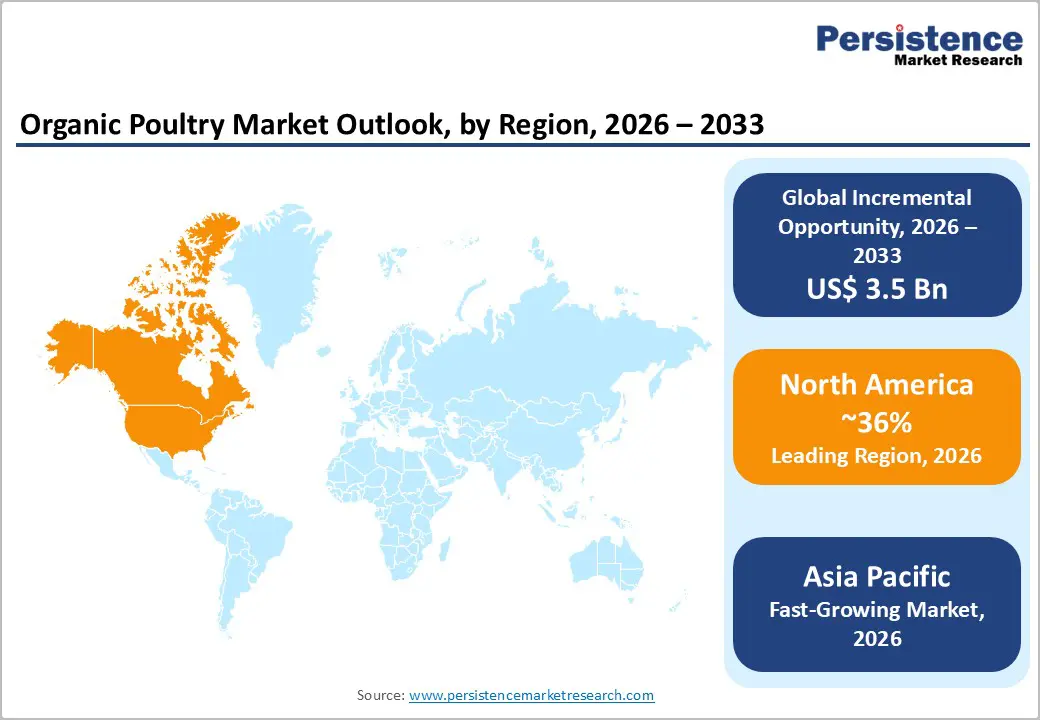

- Regional Leadership: North America is poised to dominate with about 36% in 2026, while the Asia Pacific market is anticipated to register the fastest growth at 6.5% CAGR through 2033, led by improving cold-chain logistics.

- Competitive Environment: Competitive dynamics are being shaped by strategic ecommerce expansions, investments in cold-chain infrastructure, product innovation, and geographic diversification to capture high-growth markets.

- November 2025: The United States Department of Agriculture (USDA)’s National Institute of Food and Agriculture (NIFA) invested US$ 6.4 million across seven Organic Transitions Program projects to support farmers transitioning to organic practices.

| Key Insights | Details |

|---|---|

| Organic Poultry Market Size (2026E) | US$ 9.6 Bn |

| Market Value Forecast (2033F) | US$ 13.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Demand and Supportive Infrastructure for Organic Poultry

The increasing global health consciousness has significantly driven the demand for organic poultry products, particularly organic meat and eggs, as consumers prioritize chemical-free and antibiotic-free foods. Buyers are shifting toward organic options due to concerns over conventional poultry practices that rely on antibiotics and growth promotants. This trend aligns with broader organic food consumption patterns, with over 60% of consumers preferring organic poultry for its transparency and safety. Rising disposable incomes and urbanization in emerging economies further supports premiumization trends and willingness to pay for high-quality, organic protein sources, driving the organic poultry market growth.

The expansion of modern retail and e-commerce channels has enhanced access and convenience, acting as a key growth enabler. Supermarkets and hypermarkets dominate distribution by offering wide product ranges and on-site quality comparison, while online platforms grow rapidly due to advanced cold-chain logistics and home delivery services. Agencies such as the USDA National Organic Program (NOP) and the European Union (EU)’s organic certification guidelines provide rigorous standards covering feed, housing, antibiotic use, and animal welfare, which directly influence market credibility. Investments in digital marketing, subscription models, and traceable supply networks ensure consumers, especially millennials and Gen Z, have easy access to fresh and processed organic poultry, reinforcing confidence, adoption, and sustained revenue growth.

High Production Costs, Supply Chain Challenges, and Disease Risks

The rising operational expenses and consumer price sensitivity remain key challenges for the organic poultry market. Costs associated with organic feed, certification compliance, and animal welfare practices translate into higher retail prices, with approximately 30% of consumers citing cost as a purchase barrier. This limits adoption among price-sensitive segments, especially in emerging markets where disposable incomes are lower. Conventional poultry continues to dominate overall protein consumption, restricting organic market share. Producers and retailers must adopt efficient supply chain and packaging strategies to maintain affordability without compromising organic standards or product integrity.

Structural supply chain constraints and health risks further restrain market growth. Less than 15% of poultry farms are certified organic, limiting production scalability, while inconsistent standards across regions create compliance hurdles. Cold-chain limitations affect the distribution of fresh products, particularly in rural areas. Moreover, avian influenza (bird flu) outbreaks have led to temporary flock culling, higher biosecurity costs, and production delays. For example, following the outbreak of bird flu (H5N1) in Kerala in December 2025, Tamil Nadu's poultry industry has intensified biosecurity measures with disinfection, vaccinations, and vehicle checks. These disruptions, combined with potential short-term consumer hesitancy, create significant obstacles despite the market’s strong underlying demand for organic poultry.

Emerging Market Expansion, Product Innovation, and Digital Engagement

Underpenetrated markets of Asia Pacific, Latin America, and the Middle East and Africa present significant growth opportunities for organic poultry products. Rising disposable incomes and urbanization have fueled the demand for cleaner protein sources, while health awareness continues to shape consumer preferences. Indian producers, including Country Chicken Co. and Shachi Organic Farms, have scaled free-range poultry production, while Fresh Farm Goodness has broadened its certified organic egg offerings. These efforts highlight potential for retail network growth, local certification uptake, and first-mover benefits, bolstered by investments in cold-chain logistics and consumer education. Consider prioritizing such strategies to secure early regional dominance.

Product innovation and digital engagement are opening even more novel avenues for expansion. Producers have diversified into pre-marinated organic meat, ready-to-cook meals, and meal-kit solutions to address urban convenience demands without compromising organic standards. For instance, in February 2025, Tanmiah Food Company's 'Taste Secrets' marinated fresh chicken range was shortlisted for the 2025 Gulfood Innovation Awards in the Best Meat and Poultry Product category. This line of offerings features tender, locally sourced chicken breasts in flavors such as Shish Tawouk, Spicy, and Tandoori, promoting convenience, sustainability, and reduced food waste through pre-portioned trays. Digital traceability tools, such as QR-code certifications and blockchain tracking, have built transparency and consumer trust. E-commerce platforms and loyalty programs are converting initial buyers into loyal patrons. Direct-to-consumer (D2C) models and omnichannel approaches will position leaders to outpace traditional retail, fostering sustained growth across emerging and mature markets.

Category-wise Analysis

Product Type Insights

Organic poultry meat, particularly organic chicken, is expected to command the largest share at 58% in 2026, driven by strong consumer preference for lean protein, versatility across cuisines, and consistent availability in major retail chains. Demand for antibiotic-free meat is particularly high in the U.S. and Germany, supported by national nutrition guidelines, while labeling programs in Japan enhance trust and justify premium pricing. The segment’s appeal is reinforced through foodservice partnerships, including Whole Foods Market and farm-to-table restaurants, boosting visibility and perceived nutritional value. Investments in free-range and pasture-raised systems further strengthen supply, supporting both volume growth and sustained revenue leadership.

Organic eggs are projected to grow at approximately 5.2% CAGR from 2026 to 2033, boosted by the rising demand for ethical, free-range, and cage-free variants. Consumers increasingly favor animal welfare–certified eggs, prompting producers to adopt free-range systems and certifications such as Certified Humane and Global Animal Partnership. Price accessibility further supports adoption, as eggs often retail at smaller premiums than organic meat. Examples include Pete and Gerry’s Organic Eggs expanding into major grocery chains in the U.S. and premium organic eggs launching on online platforms in South Korea. Initiatives such as the Soil Association Organic Standards in the UK ensure traceability and welfare compliance, accelerating growth and reinforcing eggs as a rapidly expanding segment.

Processing Insights

Fresh organic poultry is likely to remain the largest segment, capturing 55% of the market revenues in 2026, driven by consumer preference for minimally processed products perceived as more natural and nutritious. Fresh cuts and whole birds are widely stocked in supermarkets and specialty stores across North America and Europe, aligning with shopper expectations for quality and transparency. Regulations such as Canada’s Safe Food for Canadians support consistent handling, bolstering confidence. Retailer initiatives, such as Sainsbury’s Organic Range in the U.K., have enhanced visibility and encouraged repeat purchases, while ongoing cold-chain investments sustain accessibility and freshness.

Processed organic poultry is anticipated to grow the fastest at roughly 6.1% CAGR between 2026 and 2033, fueled by a massive demand for convenient, ready-to-cook, and pre-seasoned options. Urban lifestyles and time-constrained consumers are driving adoption, with companies such as Macro Organic offering marinated and heat-and-serve products in major grocery chains. Online platforms such as Deliciously Organic Meal Kits expand reach and convenience. These innovations tap evolving consumption patterns, offering premium, time-saving solutions while maintaining organic integrity.

Distribution Channel Insights

Supermarkets and hypermarkets are likely to be the largest distribution channel, capturing 62% of the organic poultry market revenue share in 2026, supported by high foot traffic, established cold-chain infrastructure, and broad product assortments. Major retailers such as Loblaws and Aldi feature dedicated chilled organic poultry aisles, making certified products easily accessible. Government programs such as India’s National Programme on Organic Production (NPOP) enhance transparency and consumer trust. Strategic marketing campaigns emphasizing organic certification and welfare standards further drive repeat purchases, reinforcing supermarkets’ leadership in distribution.

Online sales are projected to grow fastest at 9.3% CAGR through 2033, fueled by expanding ecommerce infrastructure, improved cold-chain logistics, and consumer preference for doorstep convenience. Platforms such as FreshDirect and BigBasket enable direct delivery of fresh and processed organic poultry. Features such as digital traceability, subscription services, and curated meal bundles enhance consumer trust and repeat purchases. Markets such as Japan and South Korea show rapid adoption of online grocery channels, making ecommerce a key growth driver alongside traditional retail.

Regional Insights

North America Organic Poultry Market Trends

North America, led by the United States, is expected to remain the largest regional market for organic poultry, contributing an estimated 36% share in 2026. This leadership is supported by well-established regulatory frameworks such as the USDA’s organic standards and strong consumer consciousness around health, sustainability, and antibiotic-free foods. Widespread supermarket penetration, advanced cold-chain logistics, and deep retail infrastructure drive broad market access across urban and suburban demographics. Consumer trust is further reinforced by regular compliance audits and government-mandated labeling transparency.

High disposable incomes and mature certification systems enhance consumer confidence and enable premium pricing for organic products. Major retail chains such as Kroger and Costco have expanded organic poultry assortments, while regional foodservice operators such as The Organic Butcher of McLean, VA emphasize traceability and welfare-driven sourcing. North America’s competitive landscape features both established integrators and innovative small to mid-sized organic producers, reinforcing sustained demand despite occasional price sensitivity in select consumer segments. Investment in omnichannel retail and digital marketing also continues to expand reach and visibility.

Europe Organic Poultry Market Trends

Europe is foreseen to capture the second-largest slice of the organic poultry market share, supported by stringent EU organic standards and widespread sustainability awareness. The key markets such as Germany, the U.K., France, and Spain consistently show strong demand for free-range and certified organic poultry across fresh and packaged categories. Harmonized regulatory frameworks, including the EU Organic Regulation, simplify cross-border trade and strengthen consumer trust in certified products. Consumers increasingly prioritize products with transparent sourcing and animal welfare guarantees, driving steady adoption of organic poultry.

Public policies promoting organic farming, animal welfare, and environmentally sustainable food systems reinforce long-term market growth. Retail leaders such as Carrefour and REWE Group feature dedicated organic poultry sections and sustainability campaigns, while Ocado expands accessibility via online grocery delivery. Growing consumer preference for traceable, ethical products has accelerated specialty and organic channels, while improvements in cold-chain logistics further support consistent supply and product quality. Europe continues to maintain a strong and stable organic poultry market.

Asia Pacific Organic Poultry Market Trends

Asia Pacific is projected to be the fastest-growing regional market for organic poultry, forecasted to register a CAGR of approximately 6.5% between 2026 and 2033, reflecting rising disposable incomes, urbanization, and expanding modern retail penetration. Nations such as China, Japan, and India are witnessing rapid shifts in consumer diets, with organic foods gaining traction among middle and upper income segments. The growth is further supported by expanding supermarket networks, modern trade formats, and e-commerce platforms that improve accessibility for both fresh and processed organic poultry. Awareness campaigns and educational initiatives have also increased consumer trust in organic certification.

While organic certification infrastructure and cold-chain networks are still developing, targeted government initiatives are accelerating progress. For example, Japan’s Agriculture Standard (JAS) organic certification enhances product credibility, while India’s PM-KSAM (Prime Minister’s Kisan Sampada Yojana) incentivizes cold-chain expansion and food safety compliance. Domestic players such as Zenith Agro and Shanghai Organic Farmer’s Cooperative are scaling production of certified poultry and eggs, responding to rising health awareness. As infrastructure, traceability, and retail penetration improve, Asia Pacific is positioned for sustained long-term growth, attracting both local and foreign investment.

Competitive Landscape

The global organic poultry market structure is moderately consolidated, with leading players such as Tyson Foods, Perdue Farms, Cargill, and PHW Group accounting for a substantial portion of overall revenues. These companies benefit from vertically integrated supply chains, long-standing relationships with large retailers, and strong investments in certified organic and antibiotic-free production systems. Advanced automation, farm-level traceability, and cold-chain infrastructure enable consistent quality, food safety, and scale efficiencies. Their broad geographic reach and brand recognition support premium pricing strategies while ensuring steady product availability across retail and foodservice channels.

Alongside global leaders, regional and niche players including Zenith Agro, Shanghai Organic Farmer’s Cooperative, and Organic Valley focus on specialty offerings, local sourcing, and cooperative-based models. Entry barriers remain high due to stringent organic certification requirements, animal welfare standards, and elevated production costs. However, digital traceability tools, direct-to-consumer platforms, and partnerships with e-commerce retailers are improving market access for smaller producers. The gradual consolidation is expected as major players pursue acquisitions, farm modernization, and technology-driven efficiency improvements.

Key Industry Developments

- In December 2025, ORGE CO Ltd launched new organic chicken drumsticks and whole legs, entering Hong Kong SAR and Japan to capture growing premium organic demand. The company leveraged localized marketing, influencer collaborations, and existing certifications to build trust and strengthen retail and e-commerce presence. This expansion positions ORGE CO Ltd as a leading Asian supplier and highlights strategic product development tailored to regional preferences.

- In August 2025, Farmer Focus rolled out the “Chicken for Good” campaign, emphasizing traceability via QR codes, ethical practices, and USDA organic certification. Consumers can scan Farm ID codes to see photos and information about independent family farms, reinforcing transparency, ethical production, and trust in organic poultry.

- In May 2025, Herbruck’s Poultry Ranch launched pasture-raised organic eggs under the Love Your Eggs brand.Hens receive daily outdoor access, fresh air, and natural foraging space, yielding certified organic, high-quality eggs with deep yolks.Products appear at retailers such as Forest Hills Foods and Family Fare in Michigan and nearby states.

Companies Covered in Organic Poultry Market

- Tyson Foods, Inc.

- Perdue Farms, Inc.

- Sanderson Farms

- Pilgrim’s Pride Corp.

- Bell & Evans

- Shenandoah Valley Organic

- Yorkshire Valley Farms

- Petaluma Poultry

- Riverford Organic Farmers Ltd.

- Hain Celestial Group

- Tecumseh Poultry LLC

- Bostock’s Organics

- Cargill, Inc.

- Plukon Food Group

Frequently Asked Questions

The global organic poultry market is projected to reach US$ 9.6 billion in 2026.

Surging demand for chemical- and antibiotic-free protein, growth of modern retail and e-commerce, and supportive organic certification frameworks drive market growth.

The market is poised to witness a CAGR of 4.5% between 2026 and 2033.

Major opportunities are being generated in emerging markets owing to improving health awareness, expansion of processed and value-added products, and digital traceability and ecommerce platforms to engage consumers.

Tyson Foods, Perdue Farms, Cargill, PHW Group, Zenith Agro, and Shanghai Organic Farmer’s Cooperative are some of the key players in the market.