- Processed Food

- Organic Chicken Market

Organic Chicken Market Size, Share, and Growth Forecast, 2026 – 2033

Organic Chicken Market by Product Type (Fresh, Frozen, Processed), Distribution Channel (Retail Stores, Online, Food Service Centers, B2B), End-User (Household, Food Service & Institutional), and Regional Analysis for 2026-2033

Organic Chicken Market Share and Trends Analysis

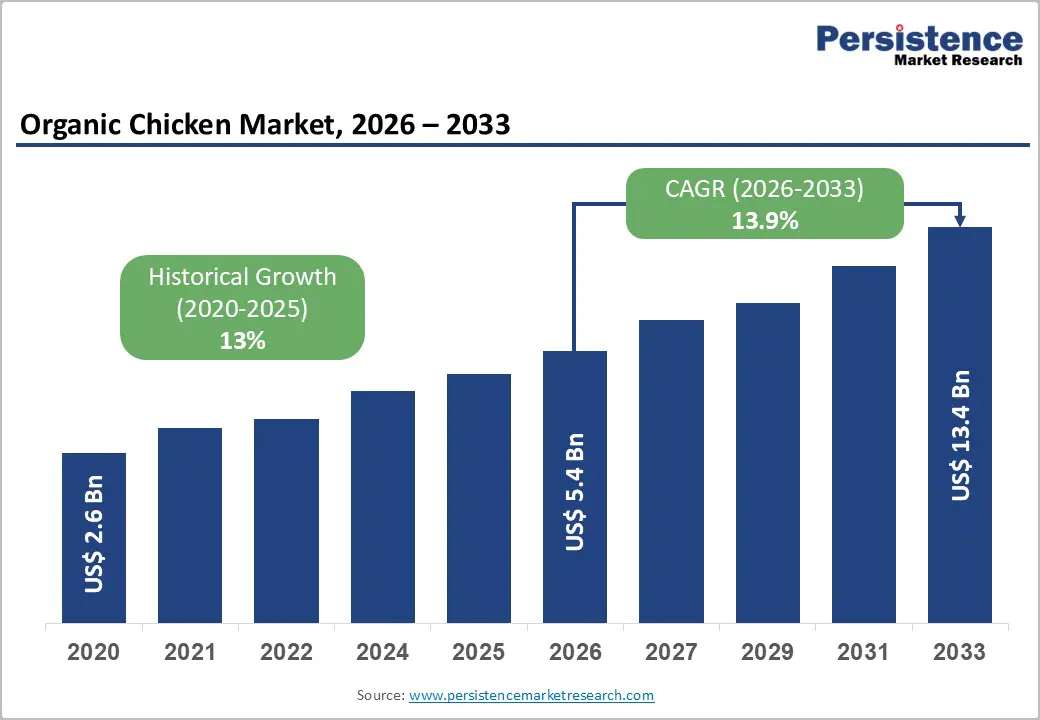

The global organic chicken market size is likely to be valued at US$ 5.4 billion in 2026, and is projected to reach US$ 13.4 billion by 2033, growing at a CAGR of 13.9% during the forecast period 2026−2033. This rapid expansion is driven by rising consumer awareness of the adverse effects of synthetic additives, antibiotics, and hormones in conventional poultry production, which is increasing demand for organic alternatives perceived as safer and more nutritious. Retail penetration and online distribution channels have broadened access to organic chicken worldwide, making it easy for consumers to choose certified products. Certification regimes such as the United States Department of Agriculture Organic (USDA Organic) and similar regional standards have reinforced consumer trust and brand transparency, further supporting market growth.

Key Industry Highlights

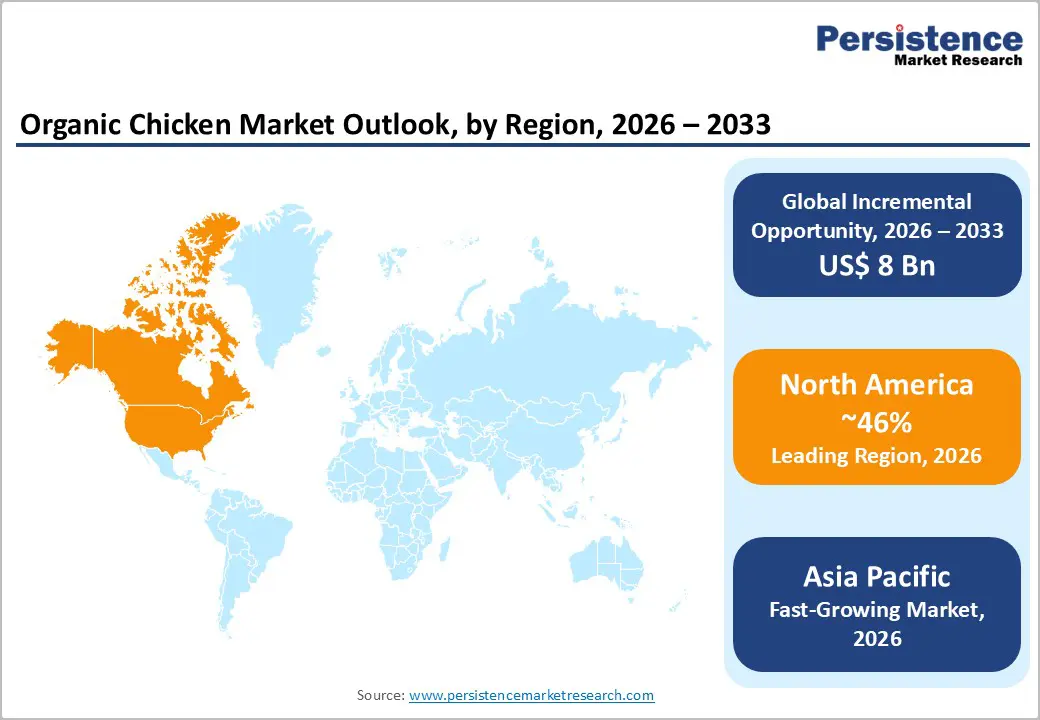

- Dominant Region: North America is projected to capture around 46% market share by 2026, fueled by a mature organic food ecosystem and early adoption of organic poultry.

- Fastest-growing Market: Asia Pacific is positioned to be the fastest-growing market through 2033, supported by a growing demand for natural and antibiotic-free protein and expanding access through modern retail and online channels.

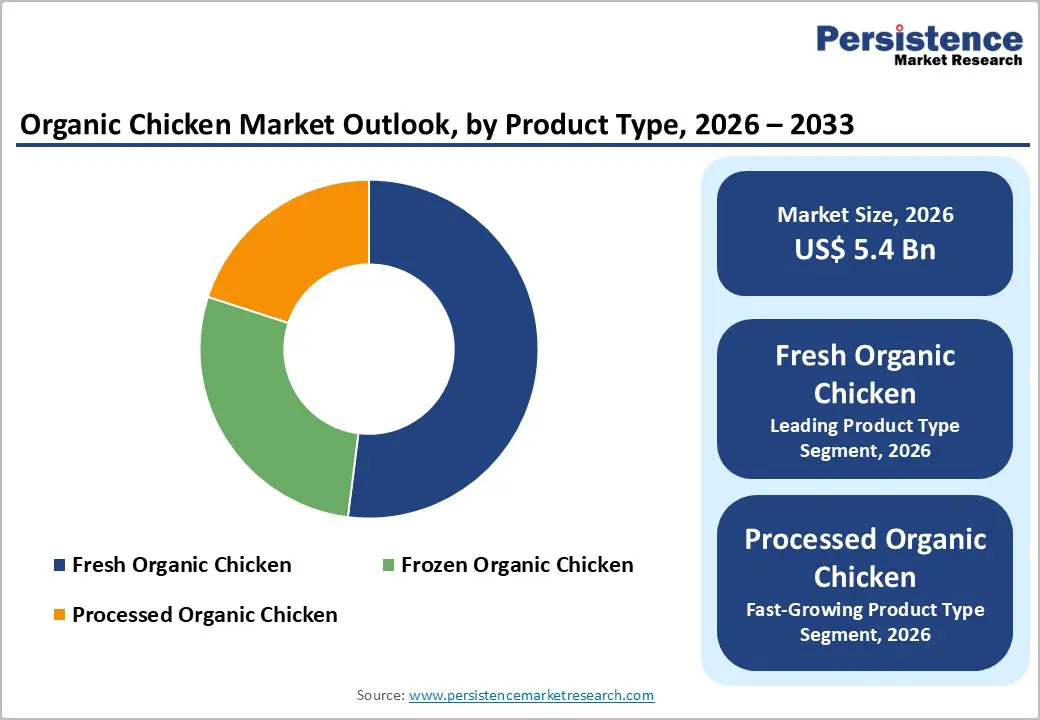

- Leading Product Type: Fresh organic chicken is likely to account for around 52% of revenue share by 2026, driven by strong consumer preference for minimally processed, high-quality protein.

- Fastest-growing Product Type: Processed organic chicken is expected to grow the fastest through 2033, driven by a rising demand for convenient, ready-to-cook, and ready-to-eat protein solutions.

- April 2025: Applegate Farms introduced gluten-free APPLEGATE NATURALS Lightly Breaded Chicken Tenders and Popcorn Chicken, made from humanely raised, antibiotic-free white meat chicken.

| Key Insights | Details |

|---|---|

| Organic Chicken Market Size (2026E) | US$ 5.4 Bn |

| Market Value Forecast (2033F) | US$ 13.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 13% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Improving Health Consciousness and Demand for Antibiotic-Free Products

With health consciousness rising among modern-day consumers, the demand for antibiotic-free products is steadily driving growth in the organic chicken market, shaped by heightened scrutiny of food safety, nutritional quality, and long-term wellness outcomes. Consumers increasingly associate routine antibiotic use in poultry with antimicrobial resistance, immune disruption, and reduced nutritional integrity, creating a strong preference for cleaner protein sources. Organic production practices align with evolving dietary priorities focused on transparency, traceability, and minimal chemical exposure. Premium protein categories gain traction as households reallocate spending toward products perceived as safer, ethically produced, and aligned with modern nutrition standards. Purchasing decisions increasingly reflect risk mitigation behavior tied to health preservation.

Regulatory oversight, medical guidance, and public health discourse have reinforced awareness around antibiotic stewardship, accelerating the adoption of certified antibiotic-free poultry. Healthcare professionals, nutritionists, and wellness platforms actively promote reduced antibiotic intake through food, influencing mainstream consumption patterns. Foodservice operators and retailers respond by prioritizing clean-label offerings to maintain credibility and meet evolving procurement standards. Supply chains adjust to support consistent availability, while certification frameworks validate production claims and reduce information asymmetry.

Supply Chain Constraints and Limited Scalability

Supply chain constraints and limited scalability emerge as key restraints due to the structurally complex production ecosystem required for certified organic poultry. Organic feed sourcing remains a primary bottleneck, as grains must be cultivated without synthetic fertilizers or pesticides, resulting in lower yields and higher price volatility. Dependence on a narrow base of certified feed suppliers increases exposure to climatic risks, regional crop failures, and logistics disruptions. Breeding cycles follow stricter animal welfare norms, including longer growth periods and lower stocking densities, which reduce throughput per facility.

Limited scalability is further reinforced by regulatory complexity and high compliance costs across farming, processing, and distribution stages. Certification audits, traceability documentation, and periodic inspections require sustained administrative investment, discouraging rapid capacity expansion. Smaller producers face financial strain when attempting to scale operations, while larger players struggle to maintain consistent standards across geographically dispersed facilities. Labor requirements remain elevated due to manual handling, welfare monitoring, and biosecurity protocols. Land availability for organic farming remains constrained, given multi-year soil conversion requirements before certification approval.

Product Innovation and Value-Added Offerings

Product innovation and value-added offerings represent a key opportunity as purchasing decisions increasingly reflect lifestyle alignment rather than basic protein demand. For example, small farms in South Dakota, such as Bear Butte Gardens and Odessa Farms, are thriving amid the farm-to-table movement by diversifying revenue through produce sales, farm tours, workshops, events, and local restaurant supplies despite certification challenges. Consumers are actively seeking differentiated attributes such as antibiotic-free processing, hormone-free rearing, enhanced animal welfare, and clean-label positioning that go beyond standard organic certification. Innovations in cuts, portion-controlled packs, marinated variants, and ready-to-cook formats address time-constrained households and elevate perceived convenience. Functional positioning through claims linked to higher protein density, improved fatty acid profiles, or enhanced traceability strengthens premium perception and supports price realization.

Value-added offerings create a pathway to margin expansion and customer retention by shifting competition away from price-led commoditization toward experience-led differentiation. Product lines aligned with specific dietary preferences, such as high-protein nutrition, fitness-focused consumption, or family-friendly meal solutions, enable targeted engagement across income segments. Co-branding with health, wellness, or sustainability narratives strengthens brand credibility and fosters long-term loyalty. Innovation across processing techniques, flavor profiles, and convenience formats supports faster inventory turnover and improves channel adaptability.

Category-wise Analysis

Product Type Insights

Fresh organic chicken is expected to lead the market, capturing approximately 52% of the market revenue in 2026, driven by strong consumer preference for minimally processed protein that offers freshness, quality assurance, and nutritional integrity. Shoppers increasingly favor visible, natural formats that meet clean-label expectations and reflect trust in sourcing practices. Retailers reinforce this trend through prominent product placement, rapid inventory turnover, and premium pricing, while robust cold-chain infrastructure and reliable supply chains ensure consistent availability across organized retail and specialty outlets.

Processed organic chicken is projected to be the fastest-growing segment from 2026 to 2033, as demand rises for convenient protein solutions suited to time-constrained lifestyles. Ready-to-cook and ready-to-eat formats are gaining traction among urban households and foodservice operators, supported by innovation in portion control, flavor profiles, and packaging that enhance usability and brand differentiation. Expanding quick-service restaurants and institutional catering further accelerate market penetration, positioning value-added organic chicken as a key growth driver in the category.

Distribution Channel Insights

Retail stores are forecasted to dominate in 2026, capturing approximately 58% of the organic chicken market revenue share, as consumers rely on physical verification of product quality, visible organic certification, and immediate availability. Supermarkets, hypermarkets, and specialty outlets ensure controlled cold-chain handling, in-store quality assurance, and established trust in food safety. Promotional depth, private-label offerings, and loyalty programs encourage repeat purchases, while well-developed logistics networks and supplier integration maintain consistent supply, reinforcing retail stores as the primary channel for organic protein purchases.

Online platforms are expected to be the fastest-growing segment from 2026 to 2033, driven by convenience-oriented purchasing behavior and the expansion of digital grocery ecosystems. Home delivery, flexible ordering, and broader product assortments attract urban consumers, while enhanced transparency through detailed product information and customer reviews builds confidence in organic selections. Advancements in cold-chain last-mile delivery and data-driven promotions accelerate channel scalability, positioning online platforms as a key growth driver in distribution strategies.

End-User Insights

Household consumers are projected to capture around 64% of the end-user revenue share in 2026, reflecting a sustained focus on health-conscious eating, clean-label preferences, and daily meal consumption patterns. Households prioritize proteins perceived as safer, naturally produced, and nutritionally reliable, with regular home cooking and family-oriented meal planning driving consistent purchase frequency. Expanding availability through organized retail and private-label offerings enhances accessibility, while a willingness to pay for quality reinforces dominance across both mature and emerging markets.

Food service and institutional buyers are expected to register the highest CAGR between 2026 and 2033, owing to menu premiumization and rising demand for transparency in ingredient sourcing. Restaurants, hotels, and catering operators are increasingly adopting organic poultry to align with wellness positioning and sustainability commitments. Fast-casual and premium dining formats use quality differentiation to attract discerning consumers, while institutional cafeterias in corporate, healthcare, and education settings further support volume expansion through standardized procurement and long-term supply agreements.

Regional Insights

North America Organic Chicken Market Trends

North America is expected to account for about 46% of the organic chicken market share in 2026, supported by an established organic food ecosystem, early-scale commercialization of certified poultry, and mature supply chains that are delivering stable volumes, consistent quality, and more predictable pricing. Producer–retailer coordination is improving speed-to-shelf execution and enabling faster product development, while strict enforcement of certification rules, such as the organic requirements established by the USDA, is strengthening label credibility and reducing shopper hesitation. Premium retail penetration and expanding private-label portfolios have been widening household access and stabilizing baseline offtake across mainstream channels.

Buyer behavior is becoming more sophisticated as consumers in the region have been planning meals, customizing diets, and aligning purchases with wellness-led lifestyles, which is sustaining repeat buying and trading up. Food service operators are incorporating certified poultry to support menu transparency and premium positioning, and this shift is expanding institutional throughput in formats such as fast-casual restaurants and corporate catering. To protect margins, operators are scaling cold-chain capabilities, automating processing, and applying data-driven inventory controls that are reducing spoilage and improving service levels. By 2026, leading brands will have reinforced loyalty by investing in measurable sustainability practices and animal welfare standards that meet rising environmental expectations from both consumers and commercial buyers.

Europe Organic Chicken Market Trends

The Europe organic chicken market is well-position to witness steady expansion through 2033, on the back of a consistent demand for high-quality, sustainable protein and regulatory frameworks that uphold certification credibility. Mature retail networks, such as supermarkets and premium grocers, ensure broad access to certified poultry, while stable purchasing behavior is driven by health awareness, environmental concerns, and a preference for clean-label products. Established cold-chain logistics and processing infrastructure maintain product quality and shelf-life consistency, preventing significant demand volatility.

Market stability is reinforced by the alignment of production capacity with consumption trends, where small-scale producers coexist with industrial operations to enable regional sourcing and traceability. Ready-to-cook and portion-controlled formats remain relevant for urban households, while value-added offerings generate incremental revenue. Food service operators, including casual dining and institutional catering, are integrating organic chicken to meet consumer expectations for transparency and quality, ensuring steady adoption across commercial channels.

Asia Pacific Organic Chicken Market Trends

Asia Pacific is poised to be the fastest-growing regional market for organic chicken between 2026 and 2033, aided by rapid urbanization, rising disposable incomes, and a stronger focus on food safety and preventive health. Expanding middle-class populations have been shifting their consumption toward protein that is perceived as natural, antibiotic-free, and hormone-free, creating a more favorable demand base for certified products. Awareness of nutritional quality and wellness trends has increased among health-conscious households and young professionals, who are currently seeking convenient, premium meal options that align with their lifestyle goals. Supermarkets, modern grocery chains, and online platforms are continuously expanding distribution, which has improved access to certified organic poultry, raised product visibility, and reinforced consumer confidence in the category.

Industrial and small-scale producers have been investing in scalable organic production systems so they can respond to this rising demand in a reliable way. Supply chains are evolving with stronger cold-chain infrastructure, more robust traceability systems, and greater use of automated processing, which has enabled wider distribution coverage and more consistent quality standards. Ready-to-cook and other value-added product formats are currently resonating with busy urban consumers and foodservice operators, supporting growth in both retail and commercial channels. At the policy level, government initiatives that promote sustainable agriculture and stricter food safety standards have been providing regulatory clarity and are likely to have encouraged further private investment in organic farming by 2033.

Competitive Landscape

The global organic chicken market structure has remained moderately consolidated, where a limited number of leading producers have captured a significant share while several specialized firms have been focusing on niche product formats and regional distribution requirements. Key participants such as Perdue Farms, Tyson Foods , Applegate Farms, and Organic Valley have played a central role in shaping competitive dynamics through strong production capabilities, rigorous quality standards, and diversified product portfolios. These companies have supported demand across retail, online, and foodservice channels by offering fresh, frozen, and value-added organic poultry products that meet evolving consumer expectations for safety, nutrition, and sustainability.

These established players have collectively accounted for a substantial portion of overall revenues, supported by widespread retail presence, trusted brand recognition, and continuous product innovation. Their emphasis on animal welfare, clean-label production, and scalable processing operations has enabled penetration across households and institutional buyers. Smaller participants have catered to niche segments such as ready-to-eat products, specialty cuts, or region-specific preferences

Key Industry Developments

- In August 2025, Farmer Focus unveiled its new Chicken for Good campaign to highlight organic practices, humane standards, and farm traceability by letting consumers scan a label code to learn how their chicken was raised and where it came from.

- In July 2025, Tyson Foods simplified its chicken nugget formula by introducing new simple-ingredient nuggets made with all-natural white meat chicken, cheese, and seasonings to meet rising consumer demand for cleaner labels and high-protein options.

- In May 2025, Amylu Foods launched certified organic chicken sausages in four flavors, meeting rising consumer demand for clean-label, convenient, and flavorful organic protein options. The sausages are made with no antibiotics, nitrates, or artificial ingredients, and feature natural casings.

Companies Covered in Organic Chicken Market

- Perdue Farms

- Tyson Foods, Inc.

- Applegate Farms, LLC

- Organic Valley

- Bell & Evans

- Mary's Chickens.

- Plukon Food Group

- Amylu Foods

Frequently Asked Questions

The global organic chicken market is projected to reach US$ 5.4 billion in 2026

The market is driven by rising health awareness, food safety concerns, demand for antibiotic- and hormone-free protein, and increasing disposable income.

The market is poised to witness a CAGR of 13.9% from 2026 to 2033.

Key market opportunities include product innovation, value-added offerings, clean-label differentiation, and expanding retail and online distribution channels.

Key players in the market include Perdue Farms, Tyson Foods, Inc., Applegate Farms, LLC, Organic Valley, and Bell & Evans.