- Processed Food

- Organic Beef Market

Organic Beef Market Size, Share, and Growth Forecast 2026 - 2033

Organic Beef Market by Beef Type (Fresh Meat, Processed Meat), by Sales Channel (B2B, B2C), and by Regional Analysis, 2026-2033

Organic Beef Market Share and Trends Analysis

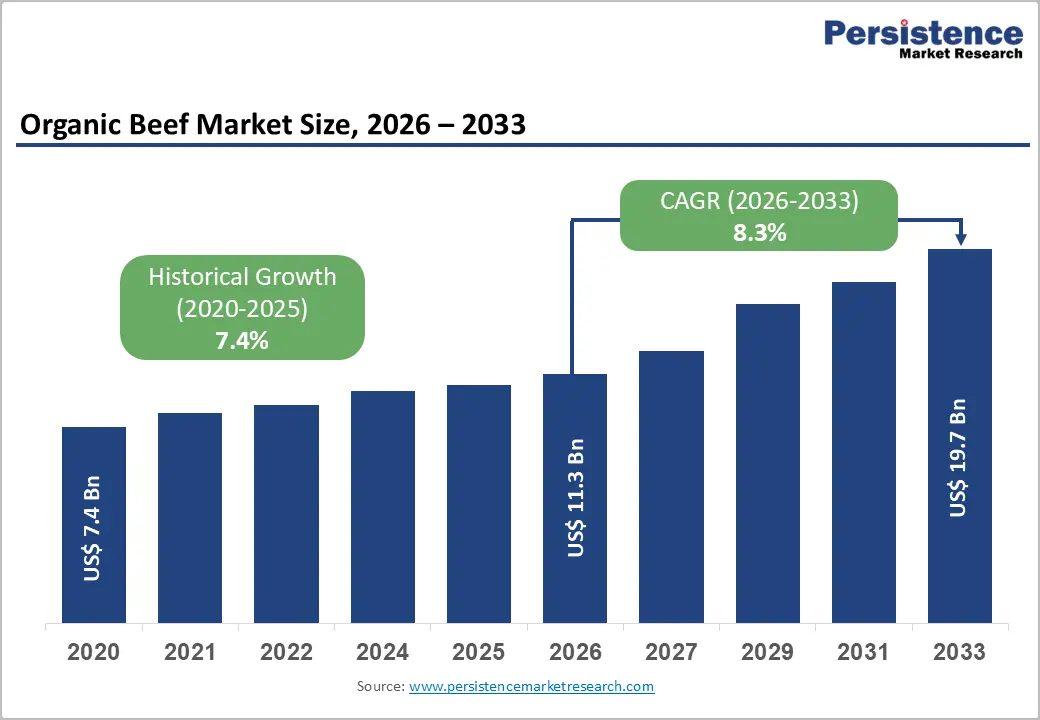

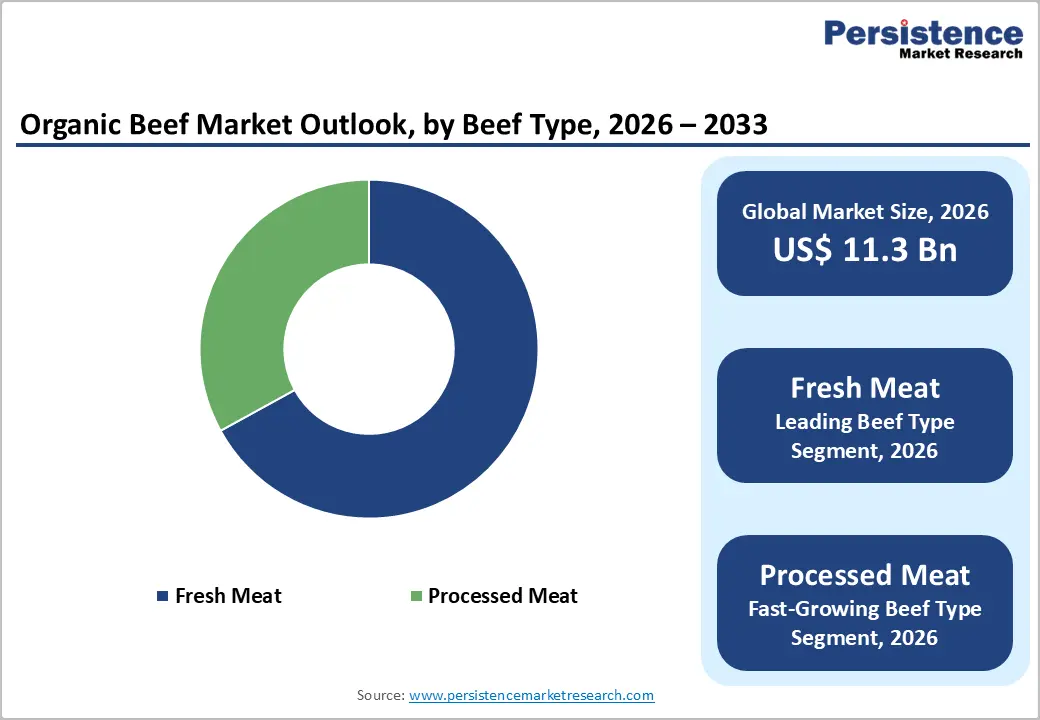

The global Organic Beef market size is expected to be valued at US$ 11.3 billion in 2026 and projected to reach US$ 19.7 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033

The organic beef market is shifting from a niche ethical choice to a structured, premium protein category shaped by health awareness, sustainability mandates, and modern retail formats. Clean-label credibility, supply-chain transparency, and convenience-led innovation are now defining competitive advantage across regions.

Key Industry Highlights

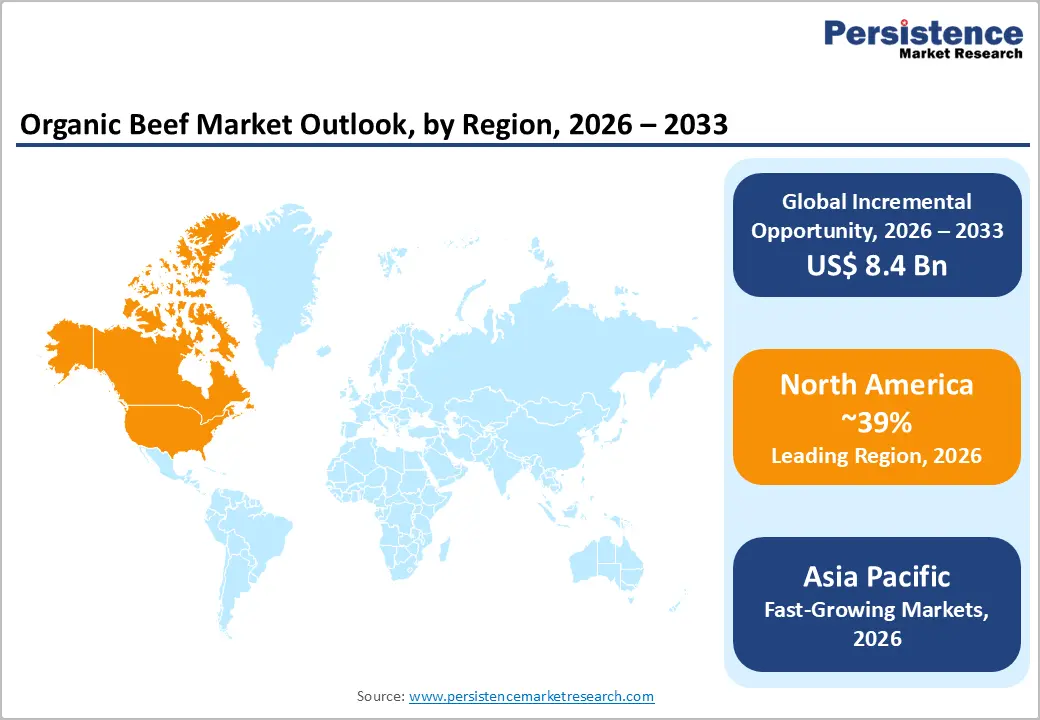

- Leading Region: North America holds 39% market share, supported by strong consumer trust in USDA organic certification, widespread availability across mass retail and DTC channels, and high awareness of hormone-free, antibiotic-free meat benefits.

- Fastest-Growing Region: Asia Pacific is the fastest-expanding market, driven by rising middle-class incomes, food safety concerns in China, premium import demand, and growing acceptance of organic beef as a health-focused luxury protein.

- Dominant Beef Type Segment: Fresh Meat leads with approximately 67% share, as consumers associate whole, unprocessed organic cuts with superior nutrition, authenticity, and quality assurance in premium retail environments.

- Market Drivers: Growing demand for clean-label, hormone-free proteins is accelerating adoption, reinforced by public concern over antimicrobial resistance, child nutrition priorities, and government-backed organic farming incentives.

- Opportunities: Expansion of organic processed meat, RTE, and RTC formats presents strong upside, supported by innovation in natural preservation, high-pressure processing, and convenience-focused product design.

- Key Developments: In May 2025, Hewitt Foods USA launched The Organic Meat Co. with USDA-certified organic beef across 193 Giant Co. stores. In March 2025, Yeo Valley Organic entered the meat category with organic grass-fed beef burgers sold through Tesco.

| Key Insights | Details |

|---|---|

| Global Organic Beef Market Size (2026E) | US$ 11.3 Bn |

| Market Value Forecast (2033F) | US$ 19.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.4% |

Market Dynamics

Driver – Growing Consumer Demand for Clean-Label and Hormone-Free Proteins

A primary driver for the Organic Beef Market is the escalating public awareness regarding the long-term health implications of synthetic inputs in conventional livestock farming. Consumers are actively seeking meat products that guarantee the absence of antibiotic residues and artificial growth promoters. According to the World Health Organization (WHO), the rise of antimicrobial resistance is a critical global threat, leading to a shift where 70% of global consumers now state they prefer meat produced without sub-therapeutic antibiotics. This health-centric motivation is particularly strong among millennial parents who prioritize organic nutrition for their children. The Organic Trade Association (OTA) has noted that organic meat is often the "entry point" for households transitioning to an entirely organic lifestyle, as the perceived safety benefits of meat outweigh those of other food categories.

Increasing Government Incentives for Sustainable and Organic Farming

The proliferation of organic beef is significantly supported by institutional frameworks that encourage livestock producers to transition from conventional to organic systems. For instance, the USDA recently launched the Organic Transition Initiative, a US$ 300 million program designed to help farmers overcome the technical and financial hurdles of obtaining organic certification. Similarly, the European Green Deal’s Farm to Fork Strategy aims for 25% of the EU's agricultural land to be under organic farming by 2030. These policies provide subsidies for organic feed production and technical assistance for pasture management, which directly enhances the supply of organic cattle. By reducing the financial risk associated with the three-year transition period, these government-led initiatives are ensuring a steady pipeline of organic beef to meet the surging retail and foodservice demand.

Restraints – High Production Costs and Premium Pricing Barriers

The most significant barrier to the mass adoption of organic beef remains the substantial price premium compared to conventional beef, often ranging from 30% to 50% higher at the retail level. This disparity is rooted in the high cost of organic-certified feed, which can be double the price of conventional grain. Additionally, organic standards require lower stocking densities and longer finishing times on pasture, which reduces the overall throughput of organic ranches. According to the Economic Research Service (ERS) of the USDA, organic livestock operations face higher labor and certification costs that many producers find difficult to recoup without high retail prices. In an environment of global food inflation, price-sensitive consumers may revert to conventional options, limiting the market’s penetration into lower-income demographics.

Opportunity – Expansion of Organic Processed Meat and Ready-to-Eat Segments

There is a massive untapped opportunity in the Processed Meat segment, particularly for convenience-oriented organic products such as pre-cooked patties, organic beef jerky, and deli meats. As modern lifestyles become increasingly time-constrained, the demand for Ready-to-Cook (RTC) and Ready-to-Eat (RTE) organic solutions is outpacing the growth of whole-muscle cuts. Manufacturers like Applegate Farms (a subsidiary of Hormel Foods) have seen significant success by offering organic sausages and hot dogs that satisfy the convenience needs of urban professionals. Innovations in high-pressure processing (HPP) and natural preservative systems, such as celery powder instead of synthetic nitrates, are allowing organic processed beef to achieve the shelf stability required for global distribution without compromising organic standards.

Integration of E-commerce and Direct-to-Consumer (DTC) Subscription Models

The rise of digital commerce is revolutionizing how organic beef reaches the end user. DTC platforms and subscription-based services like ButcherBox and Good Ranchers, Inc. are bypassing traditional retail bottlenecks by delivering frozen or chilled organic beef directly to the consumer’s doorstep. This model allows producers to tell their "farm-to-table" story directly, emphasizing animal welfare and pasture-raised qualities, which justifies the premium price. Furthermore, the COVID-19 pandemic accelerated the adoption of online grocery shopping, with the Food Industry Association (FMI) reporting a 25% increase in online meat sales. For organic beef producers, this digital shift provides a high-margin sales channel that fosters long-term brand loyalty and provides valuable data on consumer preferences for specific cuts and packaging formats.

Category-wise Analysis

Beef Type Analysis

The Fresh Meat segment dominated the Organic Beef Market in 2025, holding a significant 67% market share. This dominance is attributed to the consumer perception that fresh, unprocessed cuts are the most nutritious and authentic form of protein. In high-end retail chains such as Whole Foods Market and Erewhon, the demand for fresh organic ribeye, sirloin, and ground beef remains the primary driver of category revenue. Fresh meat allows consumers to verify quality through visual cues like marbling and color, which are critical in the premium organic segment. However, the Processed Meat segment is identified as the fastest-growing category. This growth is fueled by the rising popularity of organic convenience foods among younger demographics who seek the health benefits of organic beef but lack the time for traditional meal preparation. The shift toward organic snack foods, such as grass-fed beef sticks, is further accelerating the volume growth of the processed segment.

Sales Channel Analysis

The B2C (Business-to-Consumer) segment held the leading market share of approximately 72% in 2025. The majority of organic beef consumption occurs at the household level, as health-conscious families integrate organic proteins into their daily diets. Retail giants like Costco Wholesale and Walmart have significantly expanded their organic beef offerings, making the product more accessible to a broader consumer base. The B2C segment benefits from clear on-pack labeling and certifications that directly influence the purchasing decisions of grocery shoppers. Conversely, the B2B (Business-to-Business) segment, primarily comprising the foodservice and hospitality industries, is the fastest-growing end-use category. High-end restaurant chains and premium burger outlets, such as Shake Shack and Bareburger, are increasingly adopting organic beef to differentiate their menus and cater to the "flexitarian" diner who prioritizes quality over quantity when dining out.

Region-wise Insights

North America Organic Beef Market Trends and Insights

North America remains the dominant region in the global landscape, accounting for 39% of the market share in 2025. The region’s leadership is anchored in the United States, where the organic food industry has matured into a mainstream economic force. According to the USDA, the U.S. has over 2 million acres of organic-certified pastureland, reflecting a robust supply chain. A key trend in this region is the convergence of "Organic" and "Grass-fed" labels; consumers in the U.S. and Canada often view these two certifications as synonymous with the highest tier of meat quality.

The regulatory framework in North America, governed by the National Organic Program, ensures a high level of market transparency. Recent developments include the Origin of Livestock final rule, which closed loopholes regarding the transition of dairy cows to organic beef, further strengthening the integrity of the label. Furthermore, the innovation ecosystem in the U.S. is driving the adoption of sustainable packaging, such as compostable trays and vacuum-skin packaging, to align with the eco-conscious values of organic beef buyers. Major players like Tyson Foods Inc. and Perdue Farms are increasingly investing in organic-certified subsidiaries to capture this high-margin market.

Asia Pacific Organic Beef Market Trends and Insights

The Asia Pacific region is the fastest-growing market for organic beef, expected to witness a high CAGR through 2032. This rapid growth is primarily driven by the burgeoning middle class in China, India, and ASEAN countries, where rising disposable incomes are being channeled into high-quality, safe food products. In China, a history of food safety scandals has led to a massive demand for imported, certified organic beef from Australia and New Zealand. Organizations like Meat & Livestock Australia (MLA) have noted that organic beef is viewed as a "luxury health product" in urban centers like Shanghai and Beijing.

Japan also represents a sophisticated market where consumers prioritize longevity and health, leading to a steady increase in organic beef consumption in both the retail and premium "Yakiniku" (grilled meat) sectors. Governments in the region are also beginning to support organic transitions; for instance, India’s APEDA (Agricultural and Processed Food Products Export Development Authority) is promoting organic animal husbandry to tap into the lucrative export markets. The modernization of the retail sector, including the proliferation of high-end supermarkets and cold-chain logistics, is significantly enhancing the accessibility of organic beef across the region.

Market Competitive Landscape

The Organic Beef Market is moderately fragmented, featuring a mix of large-scale meat processors and specialized organic brands. Major industry players like Tyson Foods Inc. and JBS USA (through subsidiaries such as Acres Organic) utilize their massive distribution networks to place organic products in mainstream retail. However, specialized entities like Verde Farms and Perdue Farms maintain a competitive edge by focusing exclusively on high-integrity organic and pasture-raised supply chains. Strategies for growth include vertical integration, where companies own the organic feed mills and processing plants to ensure total traceability. There is also a notable trend toward "Regenerative Organic" certification, which goes beyond standard organic rules by requiring soil health and carbon sequestration metrics, serving as a key differentiator for market leaders.

Key Developments:

- In May 2025, Hewitt Foods USA unveiled The Organic Meat Co., a new premium brand offering USDA-certified organic, grass-fed and grass-finished beef, launched through a strategic retail partnership with The Giant Co. The range rolled out across all 193 Giant Co. stores in Pennsylvania, Maryland, Virginia, and West Virginia,

- In March 2025, Yeo Valley Organic expanded beyond dairy with the launch of its first-ever organic beef burger line, marking a strategic diversification into premium meat. Produced using 100% British, free-range, organic grass-fed beef, the beef-steak burgers emphasize high animal welfare and sustainable farming credentials.

- In February 2025, Charcutnuvo, a fourth-generation family-owned brand, announced a partnership with Regenerative Organic Certified® (ROC™) farms to launch a new line of Regenerative Organic Certified beef sausages.

Companies Covered in Organic Beef Market

- Perdue Farms

- Nicholas Meat LLC.

- Verde Farms

- Oreganic Beef Co.

- Good Ranchers, Inc.

- Primal Beef

- Eversfield Organic Ltd.

- Pipers Farm

- Tyson Foods Inc

- Danish Crown

- Others

Frequently Asked Questions

The global Organic Beef Market is expected to be valued at US$ 11.3 billion in 2026, growing steadily from its historical base of US$ 7.4 billion in 2020.

The primary drivers include rising health consciousness regarding antibiotic-free proteins, the Clean Label movement, and increasing government support for sustainable agricultural transitions through initiatives like the USDA Organic Transition Initiative.

North America is the leading region, holding a 39% market share in 2025, supported by a mature regulatory framework and high consumer awareness in the United States.

Significant opportunities lie in the expansion of Processed Meat products (like organic jerky and RTC meals) and the adoption of Direct-to-Consumer (DTC) subscription models for home delivery.

The market features prominent players such as Perdue Farms, Verde Farms, Oreganic Beef Co., Eversfield Organic Ltd., Pipers Farm, Tyson Foods Inc., and Danish Crown.