- Processed Food

- Organic Food and Beverages Market

Organic Food and Beverages Market Size, Share, and Growth Forecast, 2026 – 2033

Organic Food and Beverages Market by Product Type (Organic Food, Organic Beverages), Distribution Channel (Supermarket, Convenience Stores, Specialty Stores), End-user (Households, Commercial, Food Service, Others), and Regional Analysis 2026 – 2033

Organic Food and Beverages Market Size and Trends Analysis

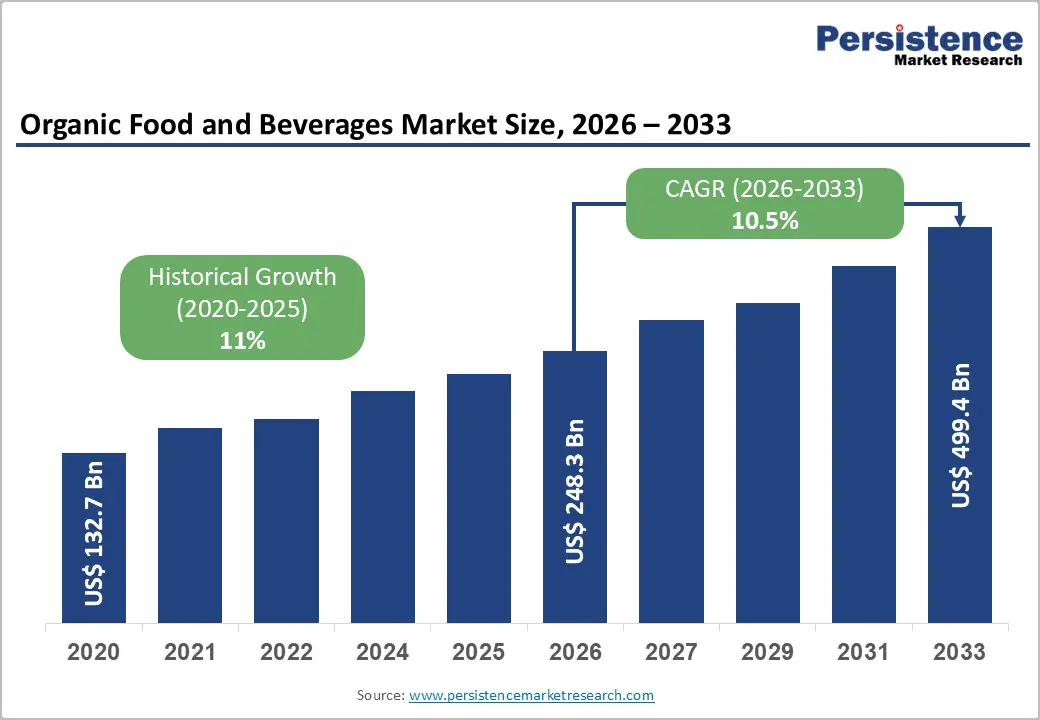

The global organic food and beverages market size is likely to be valued at US$248.3 billion in 2026 and is expected to reach US$499.4 billion by 2033, growing at a CAGR of 10.5% during the forecast period from 2026 to 2033, driven by evolving consumer preferences toward clean-label and natural nutrition, which are significantly boosting adoption across diverse global demographics.

Stringent regulations on the use of chemical inputs in agriculture are supporting the expansion of certified organic supply chains, further strengthening market growth. At the same time, increasing health awareness is accelerating demand for organic products, as consumers actively seek safer and more transparent food options. Advancements in traceability technologies, including track-and-trace systems, are enhancing transparency and building consumer trust, particularly in premium segments. Additionally, ongoing consolidation among major consumer packaged goods manufacturers is improving distribution efficiency and expanding the global reach of organic food and beverage products.

Key Industry Highlights:

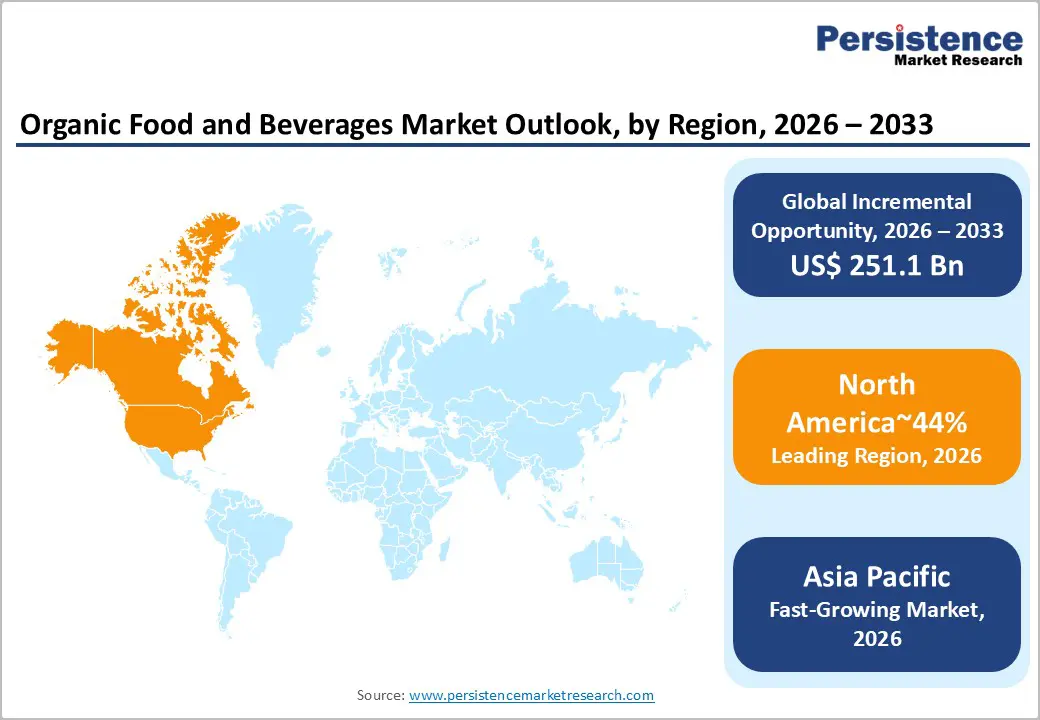

- Leading Region: North America is projected to lead, accounting for approximately 44% share in 2026, supported by mature retail ecosystems, advanced certification technologies, and robust purchasing dynamics.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by accelerating urbanization metrics, expanding middle-class purchasing power, and proactive government health initiatives.

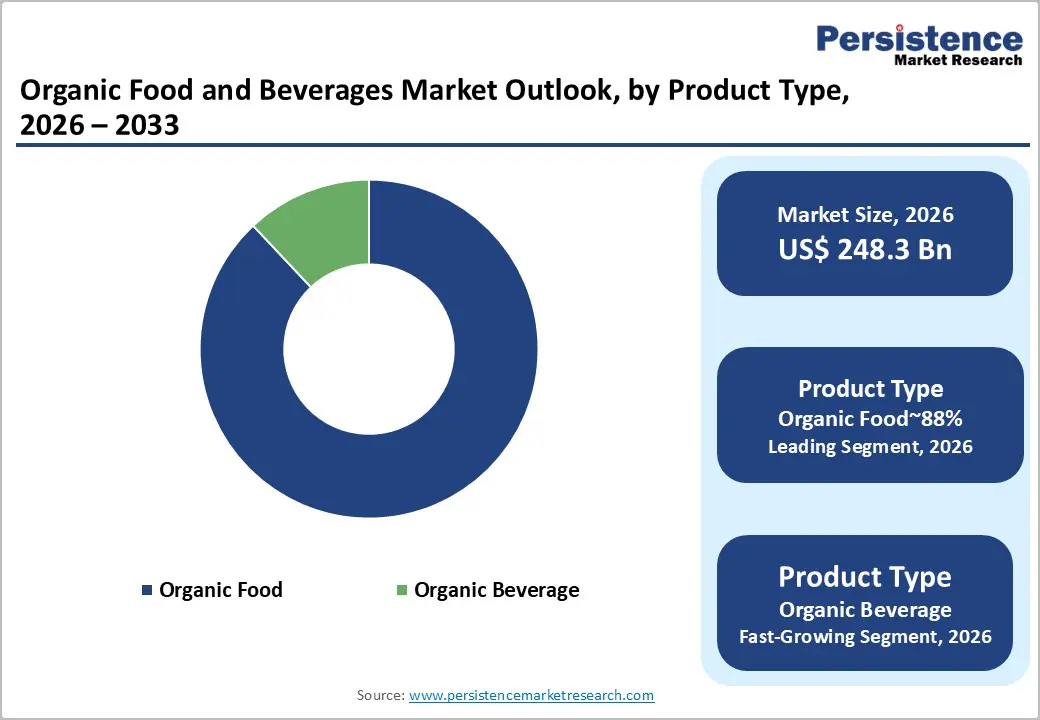

- Leading Product Type: The organic food is expected to lead, accounting for approximately 88% share in 2026, anchored by established dietary staples, comprehensive agricultural conversions, and broad retail availability.

- Leading End-user: Households are projected to dominate, holding approximately 73% share in 2026, driven by sustained home-cooking trends, rising family wellness prioritization, and direct-to-consumer accessibility.

| Key Insights | Details |

|---|---|

|

Organic Food and Beverages Market Size (2026E) |

US$248.3 Bn |

|

Market Value Forecast (2033F) |

US$499.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Escalating Demand for Regenerative Agriculture Certified Nutrition

Heightened environmental awareness among global consumers is projected to drive demand for regenerative farming outputs. Shifting purchasing behaviors toward ecologically responsible products is anticipated to accelerate core market expansion metrics. Manufacturers utilizing certified supply chains are positioned to capture escalating premium segment momentum effectively. Investments in soil health restoration initiatives are expected to yield resilient agricultural sourcing network capabilities. Danone with Horizon Organic is positioned to leverage these regenerative agriculture trends for sustained growth.

Enhanced traceability protocols within agricultural networks are likely to validate premium pricing strategies for brands. Transparent sourcing methodologies are projected to elevate consumer trust across highly competitive retail grocery environments. Strategic marketing campaigns emphasizing ecological benefits are expected to stimulate household purchasing frequency consistently. Collaborations between farmers and producers are anticipated to stabilize volatile raw material procurement cost fluctuations. General Mills, with Annie's Homegrown, is projected to capitalize on these verifiable sustainability sourcing frameworks.

Health Consciousness Elevating Clean-Label Demand

Rising health awareness propels consumers toward pesticide-free options, expanding market penetration across urban demographics. Demand for functional beverages surges as millennials prioritize immunity-boosting profiles over conventional sugars. This shift strengthens supplier incentives to scale certified production capacities efficiently. Plant-based alternatives gain traction, aligning with vegan lifestyles that amplify volume in non-dairy categories. Danone S.A., with Activia Organic Yogurt, leads this wave by innovating probiotic blends that capture wellness seekers. Consumer education campaigns further embed organic choices into routine purchases, fostering long-term loyalty.

Strategic expansions by Nestlé S.A. with Nespresso Organic Coffee variants illustrate how brand investments in sustainable sourcing drive category leadership. These moves capitalize on premium pricing tolerance, enhancing margins amid inflationary pressures. Technology in traceability apps empowers buyers to verify origins, accelerating adoption rates. Hain Celestial Group, with Earth's Best Organic Baby Food, extends reach into family segments, projecting deeper ecosystem integration. Forward implications position agile players to capture share from traditional incumbents effectively.

Barrier Analysis – Premium Pricing Limiting Mass Adoption

Elevated production costs from certified inputs constrain affordability for price-sensitive demographics worldwide. Limited scale in organic farming inflates logistics expenses, squeezing distributor margins consistently. This structural gap slows penetration into low-income households, capping volume potential. Danone S.A., with Activia Organic Yogurt, faces pushback in value segments despite brand strength. Perception of luxury positioning alienates budget shoppers, hindering trial rates.

Downstream impacts ripple to retailers, who stock fewer SKUs amid shelf competition pressures. End-users trade down during economic squeezes, eroding loyalty gains laboriously built. Nestlé S.A., with Nespresso Organic Coffee, navigates this by tiering offerings selectively. Manufacturers invest in yield-boosting tech to mitigate, yet timelines lag demand curves. Distributors pivot to private labels cautiously, balancing risk profiles.

Inflationary Pressures Constraining Premium Category Purchasing Power

Macroeconomic volatility across global markets is projected to restrict disposable income allocations for premium groceries. Escalating utility and processing costs are anticipated to force manufacturers into implementing aggressive retail markups. Widespread household budget tightening is expected to temporarily stall conversion rates among price-sensitive consumer segments. Retailers emphasizing private-label alternatives are likely to challenge established brand dominance during extended inflationary cycles. Whole Foods Market with 365 Everyday Value is positioned to leverage value-oriented purchasing behaviors effectively.

Elevated packaging material expenses are projected to compress profit margins across mid-tier organic beverage manufacturers. Surging energy prices are anticipated to increase operational overhead within complex food production and extrusion facilities. Value-conscious shoppers are expected to migrate toward conventional alternatives lacking stringent organic certification pricing premiums. Promotional discounting requirements are positioned to dilute brand equity for historically rigid premium-positioned companies. The Hershey Company, with Dagoba Organic Chocolate, is anticipated to face significant pricing elasticity pressures internally.

Opportunity Analysis – Advanced Bioplastic Packaging Innovations Elevating Sustainable Brand Positioning

Intensifying regulatory pressures against single-use plastics are projected to accelerate bioplastic packaging adoption across markets. Consumer preference for comprehensive ecological responsibility is anticipated to reward brands utilizing fully compostable materials. Technological breakthroughs in plant-based polymers are expected to match the protective barrier properties of conventional synthetic packaging. Scaled production of biodegradable materials is likely to drive down historically prohibitive sustainable packaging costs. Hain Celestial, with Celestial Seasonings, is positioned to enhance its ecological footprint through advanced packaging integration.

Closed-loop recycling initiatives are projected to strengthen brand loyalty among environmentally conscious consumer purchasing demographics. Marketing narratives highlighting zero-waste commitments are anticipated to differentiate products within densely saturated retail environments. Collaborative industry consortia are expected to standardize compostable packaging infrastructure across fragmented municipal waste management systems. Innovative lightweight packaging designs are positioned to reduce transportation emissions while maintaining structural product integrity. Nestle with Garden of Life is expected to pioneer sustainable packaging architectures within premium nutritional segments.

Integration of Functional Ingredients into Clean-Label Portfolios

Rising consumer prioritization of holistic wellness is projected to drive demand for functionally fortified organics. Innovations blending adaptogens with certified organic bases are anticipated to command exceptional premium retail pricing. Specialized cognitive health formulations are expected to penetrate rapidly expanding professional demographic target audience segments. Advanced extraction technologies are likely to preserve delicate bioactive compounds throughout intensive thermal manufacturing processes. Suja Life with Suja Organic Cold-Pressed Juice is positioned to dominate this highly lucrative functional beverage opportunity.

Clinical validations supporting functional ingredient efficacy are projected to legitimize emerging premium health beverage categories. Strategic partnerships between biotechnology firms and food manufacturers are anticipated to accelerate novel ingredient integrations. Consumer education initiatives are expected to demystify complex nutritional profiles within specialized wellness product portfolios. Retailers curating dedicated functional organic sections are positioned to capture concentrated high-margin wellness consumer footfall. Clif Bar & Company, with Clif Nut Butter Bar Organic, is expected to expand its functional nutritional offerings.

Category–wise Analysis

Product Type Insights

Organic food is anticipated to dominate the market’s product type segment, accounting for approximately 88% share in 2026, anchored by established dietary staples and comprehensive agricultural conversions. Consumer transitions toward holistic health paradigms are projected to solidify baseline demand for clean-label pantry essentials. Expanded retail shelf-space allocations are anticipated to normalize these products within conventional grocery shopping routines. Rigorous certification standards are likely to sustain premium positioning while fostering deep consumer brand trust. Industrial shifts toward regenerative agricultural sourcing are expected to stabilize critical long-term raw material availability. Technology in cold-chain logistics preserves freshness, enabling wider assortments without quality loss. Danone S.A., with Horizon Organic Milk, and General Mills, with Cascadian Farm Organic Fruits, exemplify leadership through regenerative sourcing that aligns with clean-label mandates. Consumer behavior tilts toward pesticide avoidance, propelling shelf dominance further. Danone, with Horizon Organic and General Mills, and Annie's Homegrown are positioned to dominate this foundational category. Robust regulatory frameworks are anticipated to shield established market leaders from non-compliant specialized competitive threats.

Organic beverages are projected to be the fastest-growing segment, driven by emerging unmet needs for functional hydration solutions. Advancements in cold-press extraction technologies are anticipated to preserve delicate nutrient profiles within premium liquid formats. Rapid urbanization is expected to accelerate demand for convenient, on-the-go, clean-label refreshment and energy solutions. Online channels accelerate trials among urban millennials seeking hydration alternatives. PepsiCo Inc., with Tropicana Organic Pure Premium and Califia Farms with Organic Oat Milk, launched variants in 2025 that capture wellness traffic effectively. Synergistic blending of adaptogens and botanicals is likely to capture sophisticated consumer segments seeking targeted performance. Suja Life with Suja Organic Cold-Pressed Juice and SunOpta with Sown Organic Oat Creamer are anticipated to lead this category expansion. Accelerated product lifecycle innovations are projected to continually stimulate consumer interest across highly dynamic beverage portfolios.

End-user Insights

Households are expected to dominate the end-user segment of the market, accounting for approximately 73% share in 2026, anchored by sustained home-cooking trends and rising family wellness prioritization. Expanding millennial demographics are projected to drive consistent purchasing volumes for certified safe pediatric nutritional products. Enhanced digital grocery platforms are anticipated to facilitate seamless subscription models, ensuring predictable household inventory replenishment. Widespread consumer education regarding synthetic pesticide dangers is likely to cement organic preferences within domestic kitchens. Arla Foods with Arla ØKO and Amy's Kitchen with Amy's Organic Bowls are positioned to secure these recurring household expenditures. Health trends reinforce integration into meal preps, sustaining dominance. Nestlé S.A., with Gerber Organic Baby Food, and The Hain Celestial Group, with Earth's Best Organic Pouches, secure loyalty via trusted formulations. Stable macroeconomic conditions within developed regions are expected to support continuous premium dietary household spending patterns. Clean-label demands evolve preferences toward traceable origins consistently.

Health & wellness centers are projected to be the fastest-growing segment, driven by workflow gaps requiring integrated nutritional rehabilitation solutions. Institutional transitions toward holistic patient care models are anticipated to embed organic nutrition into recovery protocols. Specialized dietary programming is expected to mandate verifiable clean-label sourcing for institutional food service procurement contracts. Increasing privatization of premium medical facilities is likely to expand budgets for high-quality certified patient nutrition. Rising memberships amplify procurement scales organically. Clif Bar & Company with Clif Organic Recovery Drinks and Organic Valley with organic protein shakes. Nestlé with Garden of Life, and Clif Bar & Company, with its Clif Nut Butter Bar Organic, is anticipated to penetrate these institutional ecosystems. Strategic vendor partnerships are projected to establish robust commercial pipelines within specialized wellness recovery architectures.

Regional Insights

Asia Pacific Organic Food and Beverages Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapidly modernizing retail infrastructures facilitate unprecedented consumer access. Expanding middle-class demographics are projected to drive massive dietary shifts toward premium imported health product categories. Heightened awareness regarding food safety vulnerabilities is anticipated to accelerate conversion toward certified clean-label alternative options. Government-sponsored nutritional initiatives are likely to cultivate highly receptive environments for novel organic functional food introductions. Suja Life with Suja Organic Cold-Pressed Juice and SunOpta with Sown Organic Oat Creamer are positioned to penetrate these rapidly emerging markets. Aggressive localized manufacturing investments are expected to reduce historically prohibitive import tariff pricing pressures gradually.

China is projected to operate as the central acceleration engine shaping the entire regional market momentum. Explosive expansion of sophisticated mobile commerce platforms is anticipated to completely bypass traditional physical retail limitations. Evolving state-level agricultural policies are expected to incentivize massive domestic transitions toward sustainable certified farming practices. Intense urbanization dynamics are likely to concentrate highly lucrative target demographics within efficiently serviceable metropolitan hubs. Danone with Horizon Organic is anticipated to deploy aggressive localized omnichannel marketing campaigns targeting these dense populations. Rapid cold-chain logistical buildouts are projected to ensure reliable nationwide distribution for highly perishable premium organic goods.

North America Organic Food and Beverages Market Trends

North America is expected to remain the leading regional market, accounting for approximately 44% share in 2026, supported by mature retail ecosystems and advanced certification technologies. High disposable income levels are projected to sustain robust demand for premium functional nutritional product categories. Comprehensive governmental regulatory frameworks are anticipated to ensure strict compliance, thereby maintaining absolute consumer confidence. Strategic consolidation among major food conglomerates is likely to optimize domestic supply chain operational efficiency continuously. Danone with Horizon Organic and Danone S.A. with Activia Organic Shelf Displays and General Mills with Cascadian Farm Organic Aisles command prime real estate through proven demand signals. Advanced agricultural infrastructure investments are expected to mitigate potential raw material shortages across this sophisticated market.

The U.S. is projected to act as the primary structural anchor driving North American momentum. Stringent USDA organic certification enforcement is anticipated to create high barriers to protecting established domestic manufacturing operations. Venture capital investments flowing into specialized food-tech startups are expected to accelerate localized category innovation pipelines. Aggressive expansion of digital grocery delivery architectures is likely to unlock new suburban demographic purchasing potential. General Mills, with Annie's Homegrown, is anticipated to capitalize heavily on these dynamic domestic consumption patterns. Favorable policy incentives supporting regenerative agricultural transitions are projected to secure resilient long-term domestic sourcing capabilities.

Europe Organic Food and Beverages Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in deeply ingrained ecological consumer values. Stringent cross-border environmental mandates are projected to force continuous operational optimizations across regional food manufacturing facilities. High baseline consumer awareness is anticipated to drive stable replacement cycles for essential organic pantry staples. Expanding legislative restrictions against synthetic agricultural chemicals are likely to favor certified organic operational frameworks permanently. Arla Foods with Arla ØKO and Nestle with Garden of Life are positioned to navigate these highly regulated European market environments. Continuous infrastructural investments in clean-energy production processes are expected to align with regional carbon neutrality directives.

Germany is projected to anchor this structurally mature European market through immense localized processing technological leadership. Robust consumer preference for localized verifiable sourcing is anticipated to drive continuous domestic agricultural conversion rates. Federal sustainability policies are expected to mandate extensive ecological audits for all operating commercial food entities. Intense competitive dynamics among discount grocery retailers are likely to democratize organic accessibility across diverse income brackets. The Hershey Company, with Dagoba Organic Chocolate, is anticipated to adapt precisely to these stringent localized German compliance standards. Forward-looking institutional procurement mandates are projected to guarantee stable volume demand across public sector catering services.

Competitive Landscape

The global organic food and beverages market is expected to remain moderately fragmented, balancing consolidated multinational dominance with agile localized startup proliferation. Established industry titans are projected to leverage immense capital resources to acquire disruptive, specialized dietary brands systematically. Danone, with Horizon Organic, and Nestle, with Garden of Life, are positioned to define premium quality benchmarks globally. Aggressive portfolio diversification into functional wellness categories is expected to shield incumbents against narrow niche competitive threats. Market leaders are anticipated to continuously deploy sophisticated data analytics to anticipate rapidly shifting consumer dietary preferences.

Horizontal differentiation strategies are projected to stratify product tiers catering to distinct demographic purchasing power capabilities. Ecosystem partnerships between specialized material suppliers and major distributors are expected to accelerate overall market penetration rates. Amy's Kitchen with Amy's Organic Bowls and Whole Foods Market with 365 Everyday Value are anticipated to exploit distinct competitive positioning architectures. D2C platform evolution is projected to gradually erode traditional physical retail dependencies for emerging agile brand archetypes.

Key Industry Developments:

- In February 2026, General Mills pivoted its 2026 strategy toward "Remarkable Innovation" in protein, fiber, and weight-management foods. This move aligns the company’s organic brands, such as Annie’s Homegrown, with the rising consumer trend of nutrient-dense eating driven by the increasing adoption of anti-obesity medications.

- In February 2026, Danone announced the expansion of its "Impact Journey" sustainability roadmap with new adult-focused sugar reduction targets. Danone's stricter health standards are driving major brands to reduce sugar content, setting a new, healthier benchmark for products across the grocery aisle. This initiative shifts the focus of the organic food market from just farming methods to the actual nutritional value for consumers.

- In January 2026, Nestlé launched a global precautionary recall of infant formula batches due to an ingredient safety detection. This incident underscores the critical importance of stringent quality control and supply chain transparency in the organic sector, temporarily impacting market share while reinforcing the company’s commitment to safety standards above regulatory minimums.

Companies Covered in Organic Food and Beverages Market

- Danone

- Nestle

- General Mills

- Pepsi Co, Inc.

- Coca-Cola Company

- Organic Valley

- Amul

- Sun Opta

- Hain Celestial

- Arla Foods

- Amy’s Kitchen

- Clif Bar & Company

- Eden Foods

- The Hershey Company

- Stonefield Farms

- Oatly Group AB

- Califia Farms

Frequently Asked Questions

The global organic food and beverages market is projected to be valued at US$ 248.3 billion in 2026. By the end of the forecast period in 2033, the market is anticipated to reach US$ 499.4 billion. This represents substantial quantitative expansion driven by structural industry shifts.

The primary driver is the escalating global consumer demand for regenerative agriculture and verifiable clean-label nutrition. Shifting demographic preferences toward ecologically responsible and functionally fortified products are expected to propel sustained adoption. Expanded e-commerce accessibility is also likely to accelerate comprehensive market penetration architectures.

The organic food and beverages market is expected to grow at a CAGR of 10.5% over the forecast period, reflecting a steady acceleration compared to previously observed historical growth rates.

North America is expected to lead the global market, accounting for approximately 44% share in 2026. This dominance is anticipated to be supported by mature retail infrastructures and highly capitalized industry participants.

Prominent organizations driving global market dynamics include Danone, Nestle, General Mills, Hain Celestial Group, and Organic Valley. These enterprises are projected to maintain significant influence through sustained technological and supply chain investments. Arla Foods and Whole Foods Market are also expected to dictate crucial retail consumption trends continually.