- Automotive

- Automotive Remote Diagnostics Market

Automotive Remote Diagnostics Market Size, Share, Trends, Growth. Forecasts 2026 to 2033

Automotive Remote Diagnostic Market by Component (Diagnostic Equipment, Software), Connectivity (3G/4G/5G, Wi-Fi, Bluetooth), Vehicle (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles), and Regional Analysis 2026 - 2033

Automotive Remote Diagnostics Market Share and Trends Analysis

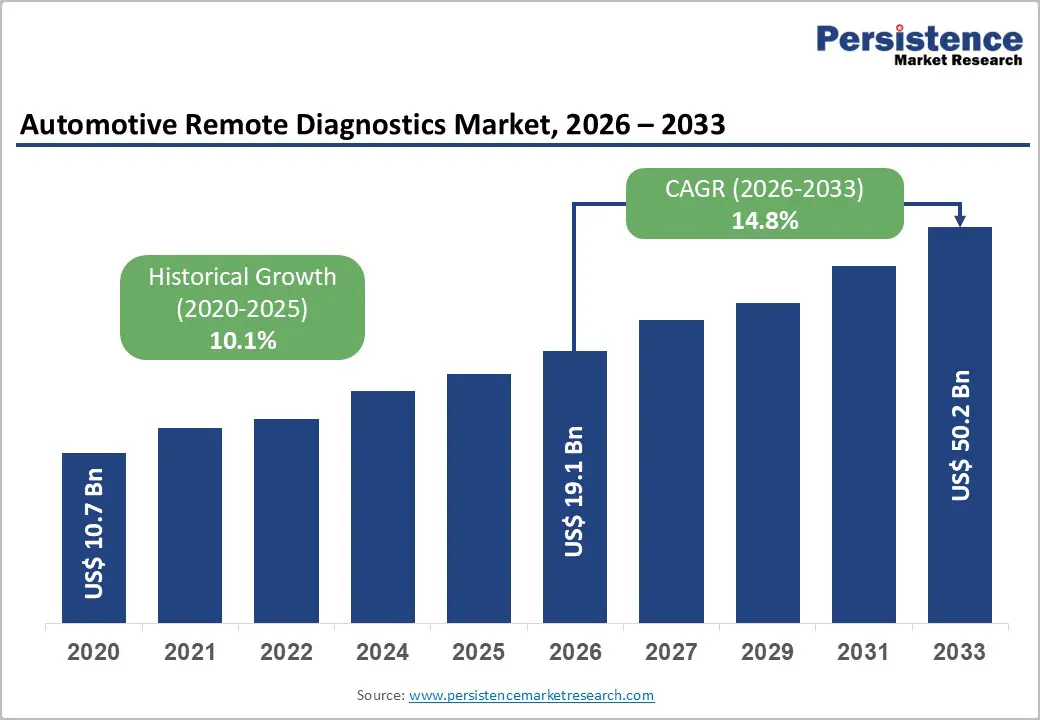

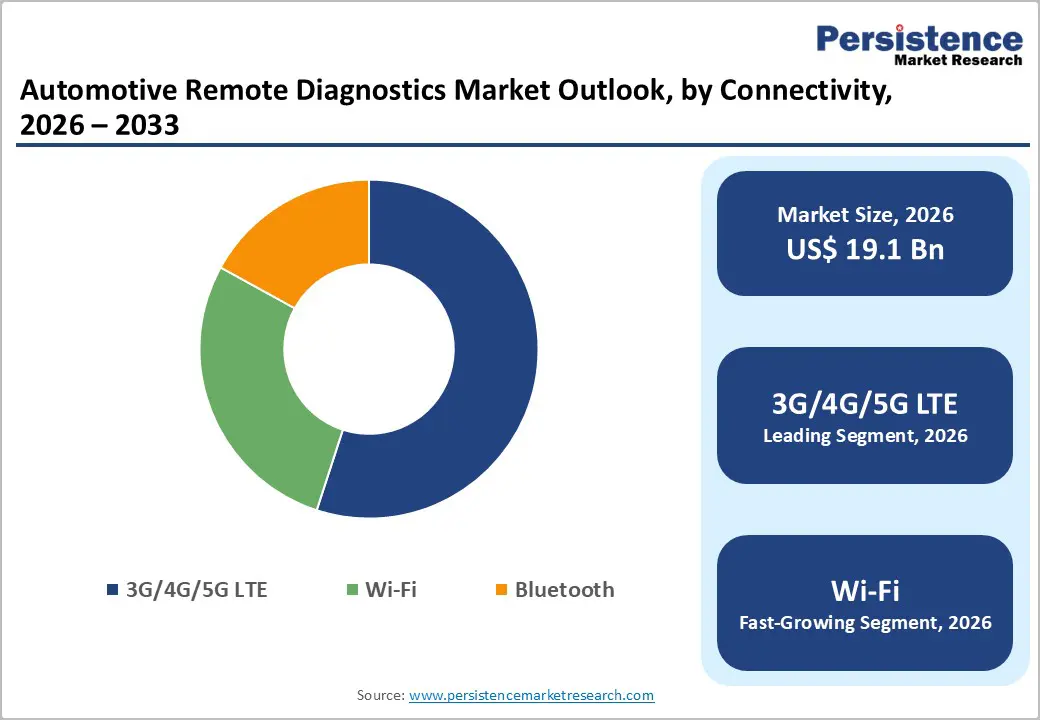

The global automotive remote diagnostics market size was valued at US$ 19.1 Bn in 2026 and is projected to reach US$ 50.2 Bn by 2033, growing at a CAGR of 14.8% between 2026 and 2033.

Growth is underpinned by rising connected-vehicle penetration, regulatory pressure for emissions and safety compliance (e.g., OBD, UNECE cybersecurity and software-update rules), and OEM investments in telematics-enabled predictive maintenance and over-the-air (OTA) services. Increasing adoption of electric and hybrid vehicles, higher fleet digitization, and expanding 4G/5G coverage globally further accelerate demand for data-driven remote diagnostics platforms.

Key Industry Highlights:

- Historical Performance: From 2020 to 2026, the market expanded from US$ 10.72 Bn to US$ 19.07 Bn, reflecting a historical CAGR of around 10.1%.

- Leading Product Segment: Diagnostic equipment holds about 63% share, underpinned by widespread deployment of telematics ECUs, OBD hardware, and embedded vehicle controllers.

- Fastest-Growing Product Segment: Software and subscription services are growing at roughly 16.5% CAGR, driven by cloud analytics, OTA management, and SaaS-based maintenance platforms.

- Connectivity Leadership: 3G/4G/5G LTE accounts for roughly 54% of the connectivity mix, with dedicated 5G slices growing fastest at a CAGR of about 16.45%.

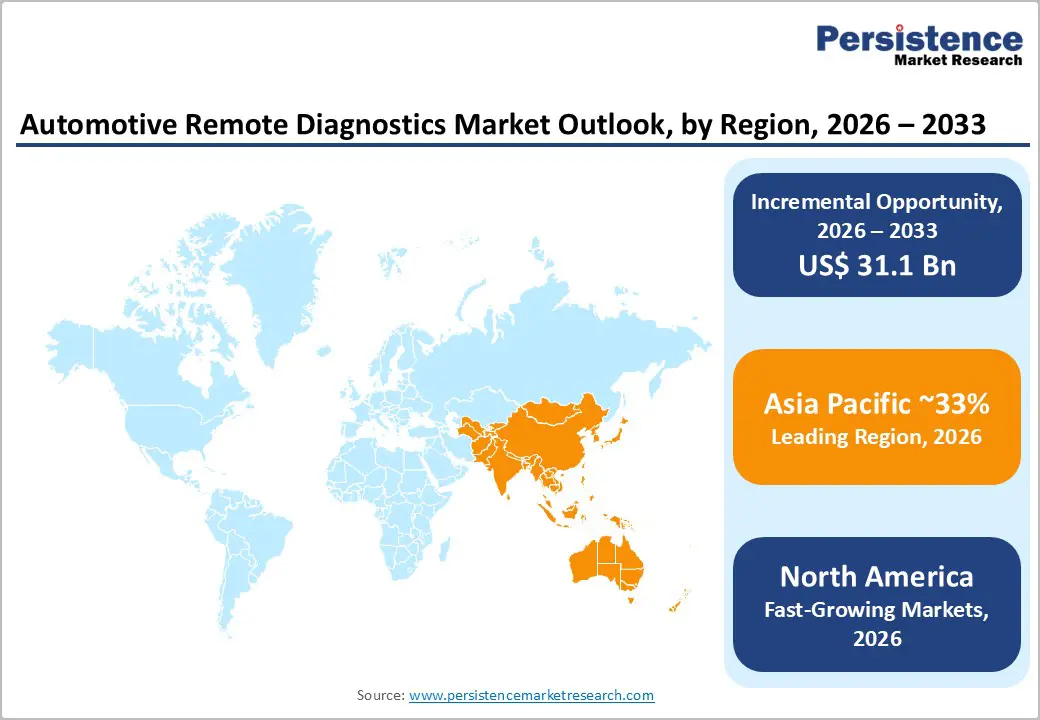

- Regional Leaders: Asia Pacific leads with a ~35% share and ≈an 15.8% CAGR, followed by Europe at ~24% share and 14.3% CAGR, while North America grows at around 15% CAGR, with high ARPU and strong fleet telematics penetration.

- Strategic Developments: Recent moves include Continental’s 2024 push toward software-defined, OTA-ready diagnostics, the 2023 Verizon-Telenor global IoT alliance, and Bosch’s AI-powered diagnostics investments, all of which reinforce integrated, service-centric business models.

| Key Insights | Details |

|---|---|

| Automotive Remote Diagnostics Market Size (2026E) | US$ 19.1 billion |

| Market Value Forecast (2033F) | US$ 50.2 billion |

| Projected Growth CAGR (2026 - 2033) | 14.8% |

| Historical Market Growth (2020 - 2025) | 10.1% |

Market Dynamics

Drivers - Expansion of Connected and Electrified Vehicle Parcels

Rapid growth in connected vehicles is a core structural driver of automotive remote diagnostics. Industry assessments indicate strong expansion in embedded connectivity across passenger and commercial vehicles, supported by telematics ECUs, cellular-V2X modules, and cloud-based analytics platforms. In parallel, global sales of electric cars surpassed 14 million units in 2023, bringing EVs to 18% of new-car sales, up from 4% in 2020, according to the International Energy Agency (IEA). These vehicles rely on continuous monitoring of the battery and power electronics, which requires robust remote diagnostic capabilities. The convergence of telematics hardware, cloud analytics, and OTA software support enables OEMs and fleet operators to proactively detect faults, schedule maintenance, and optimize lifetime costs. As connectivity and electrification scale, the addressable base for remote diagnostics expands, supporting sustained double-digit growth through 2033.

Shift Toward Predictive Maintenance and Fleet Efficiency Optimization

Fleet operators, leasing companies, and mobility-as-a-service providers increasingly rely on remote diagnostics to support predictive maintenance and utilization optimization. Predictive maintenance using telematics and cloud analytics has proven to significantly reduce vehicle downtime, while subscription-based services in automotive remote diagnostics are experiencing strong growth. Remote diagnostics enables continuous monitoring of engine health, braking systems, ADAS sensors, and EV batteries, with fault codes and performance anomalies flagged before failure. This allows fleets to consolidate service visits, reduce unscheduled breakdowns, and optimize residual values, critical in segments where vehicles can clock several hundred thousand kilometers annually. As global commercial-vehicle sales exceeded 23.4 million units in 2022, according to OICA, the economic rationale for remote diagnostics becomes compelling: even small gains in uptime and fuel efficiency translate to significant operating cost savings, accelerating enterprise adoption of integrated diagnostics platforms.

Restraints - High Integration Costs and Legacy-Fleet Constraints

Despite strong growth prospects, high upfront costs for telematics hardware, software integration, and cloud infrastructure remain a barrier, especially for smaller fleets and price-sensitive markets. Retrofitting legacy vehicles with telematics and remote diagnostic modules can require additional ECUs, communication units, and platform subscriptions, increasing the total cost of ownership. Integrating remote diagnostics into existing vehicle architectures can be expensive and technically complex, particularly where legacy ECUs and proprietary protocols are used. For many fleets with mixed-age vehicles, only a subset can justify advanced remote diagnostics, limiting penetration. These structural cost and complexity issues may slow adoption in emerging markets and independent aftermarket networks, tempering overall market growth below its theoretical potential.

Cybersecurity, Data Privacy, and Data-Access Challenges

Remote diagnostics relies on continuous data transfer from vehicles to cloud platforms, which raises cybersecurity and privacy concerns for regulators, OEMs, and end users. UNECE R155 explicitly requires cybersecurity management systems across the vehicle lifecycle. At the same time, EU data-access rules from 2025 will oblige OEMs to share vehicle operational data with independent repairers under strict governance frameworks. These regulations create compliance obligations, but also increase perceived risk regarding data misuse, hacking, and system manipulation. High-profile cyber incidents in connected vehicles, although still relatively rare, heighten OEM caution and can slow feature roll-outs. Additionally, ongoing debates over who controls and monetizes vehicle data (OEMs vs. fleets vs. third-party service providers) complicate ecosystem collaboration. Collectively, cybersecurity and data-governance challenges represent non-trivial restraints, requiring sustained investment in secure architectures and trust-building measures.

Opportunity - Service-Centric and Subscription-Based Business Models

The market is shifting from one-time hardware sales toward recurring service and analytics revenues. While diagnostic equipment has traditionally been a major revenue driver, subscription-based services are growing faster, underpinned by cloud-first architectures and OTA capabilities. As OEM-embedded solutions already control the majority of remote diagnostics share, independent repair networks are projected to grow significantly, thanks to new data-access rules, creating substantial opportunity to build neutral platforms serving both OEM and independent ecosystems. By 2033, a sizeable portion of the projected market could be attributable to software, data analytics, and service bundles rather than pure hardware. Vendors that design flexible subscription tiers (e.g., per-vehicle-per-month, outcome-based uptime guarantees) and integrate with insurance, leasing, and mobility platforms can capture high-margin recurring revenue streams.

Advanced Analytics, AI, and OTA-Driven Use Cases

Technological convergence of telematics, AI, and OTA updates opens further opportunities beyond basic fault-code monitoring. Industry assessments highlight the increasing dominance of OEM telematics and remote diagnostics services and the rising strategic importance of integrated OTA ecosystems. With regulations like UNECE R156 mandating secure update mechanisms, OEMs must invest in platforms capable not only of detecting issues but also of deploying software fixes and feature enhancements remotely. AI-driven analytics can identify failure patterns across millions of vehicles, optimize spare-parts inventory, and provide individualized maintenance recommendations. As the overall market expands, even modest penetration of AI-enhanced services and OTA-driven value-added features would constitute a substantial revenue pool. Technology vendors and Tier-1 suppliers that can deliver scalable, standards-compliant AI and OTA stacks stand to benefit disproportionately.

Category-wise Analysis

Product Type Insights

Diagnostic equipment dominates the product category, contributing about 63% of total market revenue. This reflects the entrenched base of OBD readers, telematics control units, and OEM-embedded diagnostic ECUs that underpin remote data collection and fault detection. Independent industry assessments indicate that hardware remains indispensable for enabling vehicle-to-cloud data transmission, on-board analytics, and real-time fault code detection. OEMs continue to deploy advanced telematics ECUs as standard fitment in new passenger cars, SUVs, and EVs commercial vehicles, reinforcing the equipment’s current dominance.

Software is the fastest-growing product segment, expanding at a CAGR of around 16.5%, driven by cloud-based platforms, analytics dashboards, and OTA update management systems. Subscription-based services leveraging these software layers are accelerating rapidly, supported by the growing adoption of connected-vehicle ecosystems, digital diagnostic workflows, and data-driven maintenance strategies. Vendors are migrating from standalone diagnostic tools to integrated SaaS platforms that aggregate data from multiple brands, support AI-assisted troubleshooting, and enable remote configuration changes. Over 2026 - 2033, incremental growth is expected to tilt in favor of software, progressively increasing its share and enhancing recurring revenue visibility for both OEMs and independent solution providers.

Connectivity Insights

On the connectivity axis, 3G/4G/5G LTE is the dominant segment with about 54% share, reflecting its role as the primary backbone for real-time remote diagnostics in both passenger and commercial vehicles. Independent assessments consistently highlight that the majority of diagnostic and telematics data exchange relies on cellular links due to their reliability, coverage, and bi-directional communication capability. As OEMs roll out dedicated 5G slices to support low-latency, safety-critical analytics, the cellular segment will continue to anchor the connectivity mix. With the overall market steadily expanding over the medium term, cellular-based remote diagnostics will remain the core revenue driver supported by increasing vehicle connectivity and data-centric service models.

3G/4G/5G LTE is also the fastest-growing connectivity segment, benefitting from rapid 5G deployment and automotive-grade eSIM adoption. The increasing availability of dedicated 5G network slices for automotive applications enables bandwidth-intensive diagnostics, continuous monitoring, and OTA update workloads at scale. At the same time, Wi-Fi-based connectivity is growing in prominence, particularly in workshop and depot environments, where vehicles connect to local networks for static updates, large software downloads, and bulk data uploads. Bluetooth remains important for short-range, in-cabin sensor pairing but contributes a smaller share of remote diagnostics revenues. Over the forecast horizon, multi-bearer architectures combining cellular, Wi-Fi, and Bluetooth will become standard, with cellular capturing the majority of incremental value.

Vehicle Type Insights

By vehicle type, passenger vehicles are the leading segment, with SUVs alone accounting for about 19% share of the automotive remote diagnostics market. This leadership reflects both the global shift in mix toward SUVs and the concentration of connectivity features in higher-value passenger vehicles. Global SUV sales have steadily increased as a share of new light-vehicle registrations, and connected services penetration is highest in premium and mid-to-upper-mass SUVs. Passenger cars are expected to remain the primary contributor to automotive remote diagnostic revenues, driven by regulatory OBD requirements and increasing integration of telematics in comfort, infotainment, and safety systems. OEMs leverage remote diagnostics in passenger vehicles to support warranty optimization, brand-specific connected-service bundles, and enhanced customer experience.

Passenger cars as a whole are the fastest-growing vehicle segment in remote diagnostics, driven by escalating ADAS content, EV penetration, and consumer willingness to pay for connected features. Within passenger cars, luxury models show the fastest growth, as virtually all new luxury vehicles are shipped with embedded telematics, OTA, and advanced analytics capabilities. At the same time, light commercial vehicles (LCVs) are also growing at a CAGR of around 14.2%, supported by e-commerce logistics, urban delivery fleets, and regulatory telematics mandates for commercial transport in markets like India (AIS-140) and the EU. Heavy commercial vehicles (HCVs) remain critical from a value perspective, given high utilization and fleet focus, but incremental volume growth and diagnostic penetration are strongest in passenger vehicles and LCVs through 2033.

Regional Market Insights

North America Automotive Remote Diagnostics Market Trends

North America is a prominently growing region with about 15% CAGR, anchored by the United States, which leads in connected-vehicle innovation and telematics adoption. Independent industry assessments consistently identify the USA as a key growth engine for automotive remote diagnostics, supported by an advanced fleet-management sector and substantial investments in telematics technologies. High penetration of 4G/5G networks, strong uptake of subscription-based connected services, and a large installed base of light trucks and SUVs provide a fertile environment for remote diagnostics. Regulatory pressure from U.S. safety agencies such as NHTSA on crash avoidance, emissions monitoring, and cybersecurity further encourages OEMs and fleets to deploy remote monitoring and OTA capabilities to maintain compliance and manage recalls efficiently.

In addition, the North American market benefits from a dense ecosystem of telematics and cloud providers, ranging from Verizon Connect and Geotab to major cloud platforms like AWS and Microsoft Azure, which offer modular solutions for OEMs, fleets, and insurers. The region’s competitive landscape is characterized by strong partnerships between automakers, Tier-1 suppliers, and software companies, with ongoing investments in AI-based predictive maintenance and cross-border telematics services. Given its ~15% CAGR profile and high average revenue per vehicle, North America remains a strategic focus region for premium diagnostics offerings and advanced analytics use cases.

Europe Automotive Remote Diagnostics Market Trends

Europe holds a considerable share of about 24% of the global automotive remote diagnostics market and is growing at an estimated 14.3% CAGR. Germany, the U.K., France, and Spain together account for a substantial portion of regional revenues, reflecting their strong automotive manufacturing bases and mature vehicle parc. Germany, in particular, is expanding at roughly 8.4% CAGR in broader remote diagnostics and connected-vehicle technologies, underpinned by its leadership in premium vehicles and precision engineering. EU-wide regulations, such as Euro 6/VI and forthcoming Euro 7 emissions standards, UN R155/R156 cybersecurity and software-update rules, and data-access requirements for independent repairers, create a highly regulated environment where robust remote diagnostics are essential for compliance and lifecycle management.

These regulations also drive regulatory harmonization across member states, enabling pan-European telematics and diagnostics platforms that serve fleets and OEMs across borders. Competitive intensity is high, with leading Tier-1 suppliers (Bosch, Continental, ZF, and others) headquartered in the region and actively advancing telematics and OTA technologies. Investment trends show increased spending on EV platforms, centralized vehicle compute, and software-defined cars, all of which rely on continuous remote diagnostics to support functionality and safety. Europe, therefore, remains a core market both for high-value OEM integrated solutions and, post-2025, for independent aftermarket platforms leveraging new data-access rights.

Asia Pacific Automotive Remote Diagnostics Market Trends

Asia Pacific is the leading region with around 35% global share and the fastest-growing, at approximately 15.8% CAGR. China, Japan, India, and ASEAN collectively anchor regional demand, with several reinforcing structural drivers. Independent outlooks confirm that the region’s growth is propelled by rapid EV adoption in China and expanding connected-vehicle infrastructure in ASEAN markets. China’s automakers increasingly export vehicles pre-equipped with telematics and diagnostics subscriptions, using connectivity to lock in aftermarket service revenues and differentiate internationally. Japan and South Korea contribute advanced hybrid, EV, and semiconductor capabilities, enabling sophisticated telematics hardware and in-vehicle compute for diagnostics.

In India and ASEAN, regulatory mandates and industrial policy also support remote diagnostics growth. India’s AIS-140 standard requires vehicle tracking and telematics features for commercial vehicles, while BS-VI emissions norms have led to more embedded telematics for engine and emission monitoring. ASEAN’s automotive market is expected to exceed US$ 100 billion in annual sales by 2035, and governments are promoting smart mobility and telematics infrastructure. The region’s manufacturing advantages, lower production costs, growing local electronics supply chains, and strong government incentives for EVs and connectivity make Asia Pacific a critical production hub and demand center. For vendors, localized hardware, compliance with country-specific data rules, and partnerships with regional OEMs are key to capturing a disproportionate share of global growth through 2033.

Competitive Landscape

The automotive remote diagnostics market is moderately consolidated at the platform and Tier-1 supplier level, with global leaders controlling meaningful but not dominant shares, leaving room for regional and niche specialists. Independent assessments acknowledge Bosch as one of the most influential players in the broader remote diagnostics landscape, reflecting its strong positioning in telematics, ECUs, and integrated diagnostic platforms. OEM-embedded solutions account for a significant majority of remote diagnostics deployments today, but evolving data-access regulations are enabling independent repair networks and telematics service providers to expand at above-market CAGRs. Competitive positioning is increasingly defined by depth of OEM partnerships, breadth of connectivity/OTA capabilities, and the ability to provide end-to-end solutions spanning hardware, software, analytics, and cybersecurity.

Strategic Developments

- In May 2024, Continental underscored the strategic need to decouple automotive software from hardware to accelerate feature rollouts, including remote diagnostics, across global OEM programs. This shift supports more frequent OTA updates and flexible deployment of diagnostic functions over vehicle lifecycles. For the remote diagnostics market, Continental’s modular, OTA-capable platform strengthens its competitive position in software-defined vehicles and enhances its ability to deliver scalable diagnostic services to OEMs.

- In July 2023, Verizon Business and Telenor IoT announced a strategic alliance to expand global IoT services, including eSIM-based connectivity, supporting international telematics and remote diagnostics applications. The partnership improves cross-border connectivity for fleets and OEMs, enabling consistent remote monitoring and maintenance services across regions. Strategically, this enhances Verizon Connect’s reach and attractiveness as a telematics partner for global fleet operators and automotive OEMs seeking unified connectivity for diagnostics.

Companies Covered in Automotive Remote Diagnostics Market

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Harman International

- Verizon Connect

- Geotab Inc.

- TomTom Telematics / Webfleet

- DENSO Corporation

- Hexagon AB

- Ford Motor Company

- General Motors

- Microsoft Corporation

- Amazon Web Services - AWS IoT

- Octo Group

Frequently Asked Questions

The Automotive Remote Diagnostics Market was valued at US$ 19.07 billion in 2026 and is projected to reach US$ 50.18 billion by 2033, reflecting strong, sustained expansion.

The market is driven by rising connected-vehicle and EV penetration, regulatory mandates on emissions, cybersecurity, and software updates (UN R155/R156, Euro standards, AIS-140), and fleet demand for predictive maintenance and uptime optimization.

Between 2026 and 2033, the Automotive Remote Diagnostics Market is forecast to grow at a compound annual growth rate of approximately 14.8%.

Key opportunities include high-growth demand in Asia-Pacific, expansion of subscription-based diagnostics services and AI-driven analytics, broader deployment of 4G/5G LTE and OTA platforms, and increased data-access rights enabling independent service networks.

Major players include Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Harman, Verizon Connect, Geotab, TomTom Telematics/Webfleet, DENSO, Hexagon, Ford, General Motors, Microsoft, AWS IoT, and Octo Group, supported by regional telematics specialists and cloud partners.