- Inks, Coatings, Adhesives & Sealants (ICAS)

- Automotive Adhesives & Sealants Market

Automotive Adhesives & Sealants Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Adhesives & Sealants Market by Resin Type (Polyurethane, Epoxy, Acrylic, PVA, EVA, Styrenic Block, Silicon, Others), Application (Paint Shop, Body-in-White, Assembly, UTH & Power Train, Battery Modules), Vehicle Type (Passenger Cars, HCV, LCV), and Regional Analysis for 2026 - 2033

Automotive Adhesives & Sealants Market Size and Trend Analysis

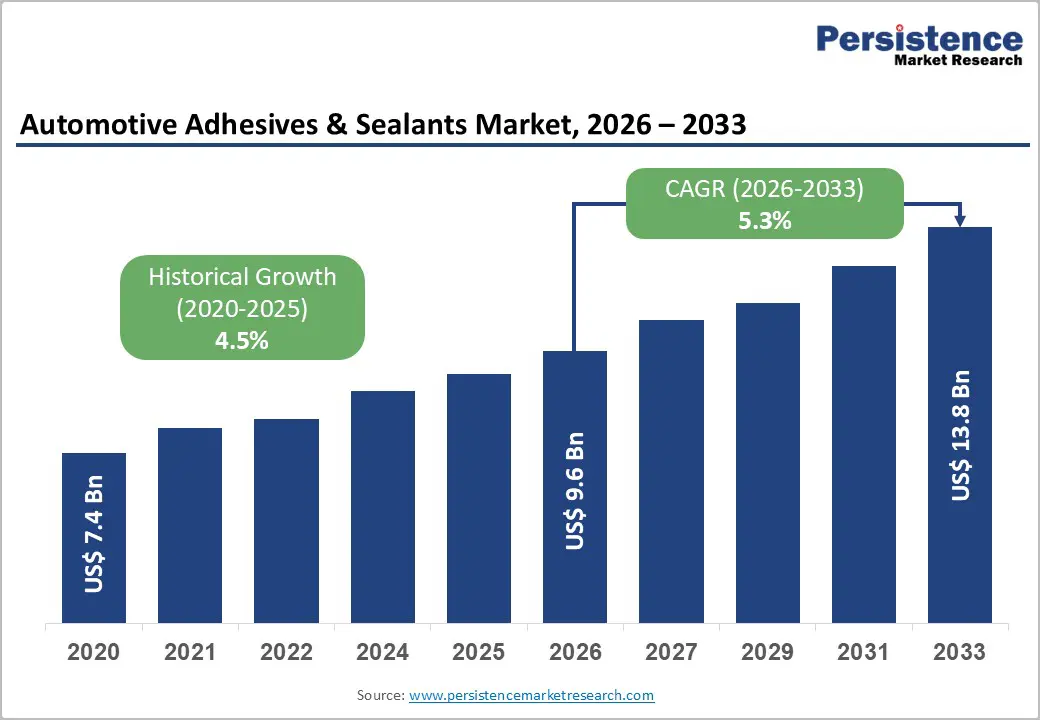

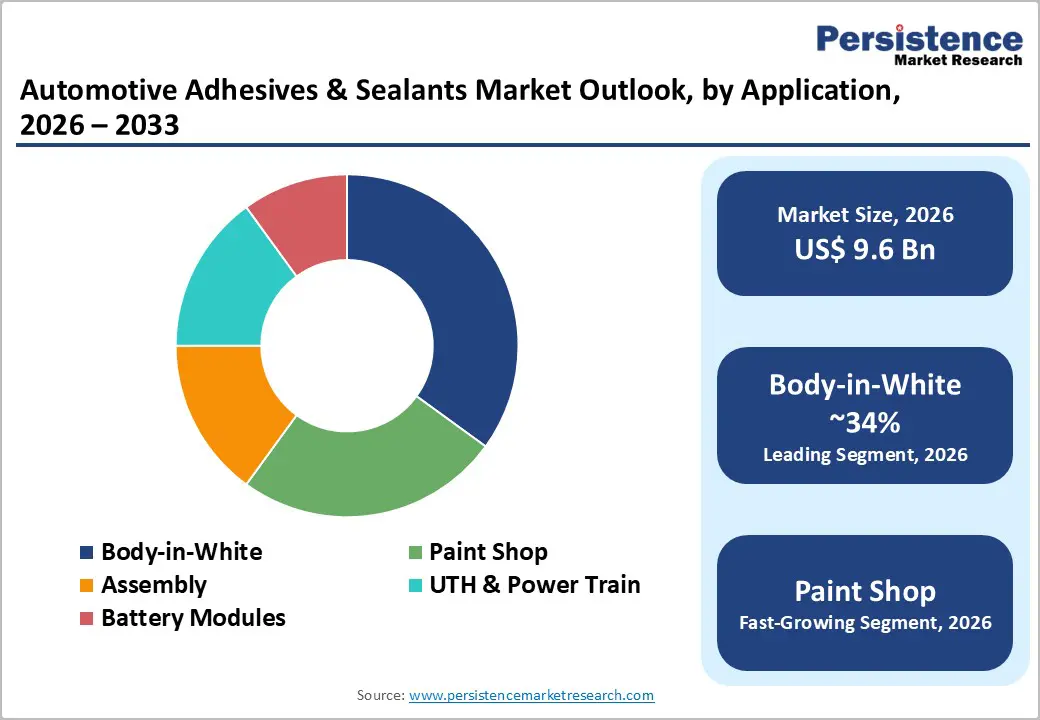

The global automotive adhesives & sealants market size is valued at US$ 9.6 Bn in 2026 and is projected to reach US$ 13.8 Bn by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

This growth trajectory is principally driven by the automotive industry's accelerating structural transition toward lightweight, multi-material vehicle platforms in compliance with binding global emission mandates, combined with the rapid electrification of passenger and commercial vehicle fleets. The European Commission's Automotive Package mandates a 90% tailpipe emissions reduction for new passenger cars from 2035, compelling original equipment manufacturers (OEMs) to replace conventional mechanical fasteners and spot welds with advanced structural adhesives across body-in-white, glazing, and closure applications.

Key Industry Highlights:

- Leading Region: Asia Pacific is the leading region in the global Automotive Adhesives & Sealants Market, driven by China's output of 31.28 million vehicles in 2024representing 34% of global production per OICA alongside rapidly maturing EV manufacturing ecosystems in India, Japan, and ASEAN nations.

- Fastest Growing Region: North America occupies a strategically significant position in the global Automotive Adhesives & Sealants Market, anchored by the United States' deep OEM assembly infrastructure, innovation-oriented specialty chemical industry, and an expanding policy ecosystem supporting automotive electrification.

- Leading Segment: Polyurethane is the dominant resin type, commanding approximately 34% of market share in 2026, supported by its unmatched functional versatility across structural bonding, sealing, and EV battery module applications and its compatibility with dissimilar-substrate multi-material vehicle architectures.

- Fastest Growing Segment: The Battery Modules application category is the fastest-growing segment, driven by global EV sales of 17.1 million units in 2024 per Rho Motion, with battery pack assembly creating structurally new and technically demanding demand for thermally conductive, electrically insulating, and vibration-resistant adhesive systems.

- Opportunities: The most significant near-term market opportunity resides in next-generation EV battery-grade adhesive systems encompassing two-component polyurethane structural adhesives, thermally conductive silicone gap fillers, and epoxy-based encapsulants where performance-differentiated formulations command premium pricing and long OEM qualification cycles create durable competitive moats.

| Key Insights | Details |

|---|---|

| Automotive Adhesives & Sealants Market Size (2026E) | US$ 9.6 Bn |

| Market Value Forecast (2033F) | US$ 13.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.5% |

Market Dynamics

Drivers - Stringent Emission Regulations and Vehicle Lightweighting Mandates Accelerating Adhesive Adoption

Tightening emissions standards across major global automotive markets represent the foremost structural demand driver for the Automotive Adhesives & Sealants Market. The European Union's Regulation (EU) 2019/631 established a binding passenger car fleet-average target of 81 grams of CO2 per kilometer for 2025, while the updated Automotive Package from the European Commission mandates a 90% tailpipe emissions reduction for all new passenger cars from 2035. Meeting these targets requires OEMs to adopt mixed-material body architectures integrating ultra-high-strength steels, aluminum alloys, and carbon fiber reinforced polymers substrates where conventional resistance welding is either technically unfeasible or structurally inadequate, making structural adhesives the solution of necessity.

Surge in Global Electric Vehicle Production Driving Demand for Battery-Grade Adhesive Systems

The global transition to electrified vehicle platforms is creating a structurally new, technically differentiated, and rapidly expanding demand category for advanced adhesive formulations in the Automotive Adhesives & Sealants Market. According to data published by Rho Motion, global electric car and light-duty vehicle sales reached 17.1 million units in 2024, a 25% increase over 2023, with China alone accounting for 11 million EV units sold, a 40% year-on-year advance. Battery pack assembly in Battery Electric Vehicle (BEV) and Plug-in Hybrid Electric Vehicle (PHEV) platforms require multi-functional adhesive solutions: polyurethane systems for vibration and impact management, epoxy formulations for structural rigidity and thermal resistance, and silicone-based thermal interface materials for battery cell heat dissipation.

Restraints - Raw Material Price Volatility Compressing Margins Across the Supply Chain

Sustained volatility in the prices of key petrochemical-derived inputs presents a material structural challenge for participants in the Automotive Adhesives & Sealants Market. Core feedstocks including methylene diphenyl diisocyanate (MDI), toluene diisocyanate (TDI), bisphenol-A epoxy resins, and acrylic monomers are highly sensitive to crude oil price cycles, refinery output disruptions, and demand-side competition from construction, electronics, and packaging sectors. This raw material unpredictability creates margin compression for adhesive formulators, particularly for small and mid-scale producers with limited hedging capacity. Downstream, automotive OEM suppliers face pricing renegotiation risk that can destabilize long-term supply agreements and delay product qualification cycles, constraining the pace of new formulation commercialization.

EU End-of-Life Vehicles Directive Limiting Permanent Adhesive Applications

The European Parliament's revised End-of-Life Vehicles (ELV) Directive, adopted in 2024, introduces explicit design-for-disassembly and recyclability requirements that directly constrain the use of permanent adhesive systems in vehicle assemblies. The directive limits the application of non-separable bonding solutions including permanent structural adhesives, overfolded joints, and thermally cured one-component systems unless material separation can be accomplished with minimal energy input and without irreversible substrate damage. This regulatory development creates a near-term substitution risk for conventional adhesive applications in body closures, glazing, and interior trim assemblies, particularly in the European market. Adhesive manufacturers face mounting pressure to reformulate toward reversible, debond-on-demand, and thermally reversible adhesive chemistries, adding R&D expenditure and extending product development timelines.

Opportunities

Battery Module Adhesives as the Fastest-Growing High-Value Application Opportunity

The electrification of automotive powertrains is structurally positioning Battery Modules as the highest-growth and most technically complex application segment within the Automotive Adhesives & Sealants Market, presenting manufacturers with a compelling product differentiation and revenue expansion opportunity. Battery pack architectures in modern BEV platforms demand precisely engineered adhesive solutions that simultaneously deliver structural bonding, thermal conductivity, electrical insulation, and vibration resistance multi-functional performance profile that standard-grade adhesive systems cannot fulfill without substantive reformulation investment.

Emergence of Intelligent and Functional Coatings

Intelligent coatings represent a transformative opportunity in the sector. These coatings incorporate responsive materials, embedded sensors, or adaptive visual properties to go beyond traditional decorative and protective roles. For example, coatings capable of changing color based on environmental stimuli or embedded with nano sensors for early detection of wheel stress showcase convergence between automotive engineering and materials science. This opens pathways for new service models, where coatings become active components in performance monitoring systems, enabling partnerships between OEMs, tier suppliers, and digital service providers.

Consumer demand for customizable aesthetics, coupled with connected car ecosystems, emphasizes functional coatings’ value in branding and personalization. Such technologies carry potential adoption first in premium and sports models, before diffusion into mainstream passenger vehicles as costs are optimized.

Category-wise Insights

Resin Type Analysis

Polyurethane is the leading resin type segment in the global Automotive Adhesives & Sealants Market, commanding approximately 34% of total market share in 2026. Its dominance is underpinned by an unmatched combination of flexibility, impact resistance, bonding strength across dissimilar substrates, and suitability for both structural and sealing applications across the broadest range of automotive assembly stages. Polyurethane-based systems are the chemistry of choice for windshield bonding, hem flange applications, underbody sealing, and increasingly for battery module encapsulation in EV platforms, where their ability to accommodate differential thermal expansion between aluminum, steel, and polymer cell casings is a critical performance attribute.

Application Insights

The Body-in-White (BIW) application segment leads to the Automotive Adhesives & Sealants Market by application, representing approximately 35% of total market share in 2026. BIW assembly has been the largest single adhesive and sealant consumption node in automotive manufacturing for over two decades, driven by the structural integrity requirements of modern vehicle architectures that depend on hem flange bonding, laser-weld bonding, and structural floor panel reinforcement. The progressive adoption of mixed-material BIW designs integrating press-hardened boron steels, aluminum stampings, and fiber-reinforced composite panels amplifies per-vehicle adhesive consumption given the incompatibility of these materials with conventional resistance welding. According to the European Automobile Manufacturers' Association (ACEA), while EU car production fell by 6.2% in 2024, the structural re-engineering of platforms toward lighter and more electrified architectures intrinsically increases the adhesive intensity per vehicle unit produced.

Vehicle Type Insights

The Passenger Cars segment is the leading vehicle type category in the Automotive Adhesives & Sealants Market, accounting for approximately 62% of total market share in 2026. This dominance reflects the global scale of passenger car production and its disproportionately high adhesive content per vehicle relative to commercial vehicle classes. Passenger car platforms incorporate adhesives across the widest range of assembly stages from BIW structural bonding and paint shop seam sealing to glazing installation, underbody deadener application, and EV battery module encapsulation. According to ACEA, global car manufacturing totaled 75.5 million units in 2024, with China commanding a 35.4% share of total output. The increasing engineering complexity of modern passenger car builds particularly in premium, battery electric, and plug-in hybrid segments drives greater adhesive specification per vehicle as OEMs seek to reduce weight, improve noise-vibration-harshness characteristics, and satisfy evolving crash safety and environmental compliance standards.

Regional Insights

North America Automotive Adhesives & Sealants Trends

North America occupies a strategically significant position in the global Automotive Adhesives & Sealants Market, anchored by the United States' deep OEM assembly infrastructure, innovation-oriented specialty chemical industry, and an expanding policy ecosystem supporting automotive electrification. The U.S. produced 10.56 million vehicles in 2024 per OICA data, with North America's total production reaching nearly 19.2 million units, of which the U.S. accounted for 55%.

At the regulatory level, the U.S. Environmental Protection Agency (EPA) and NHTSA continue to enforce progressively stringent vehicle fuel economy and emissions standards, sustaining OEM investment in lightweight multi-material architectures that require advanced structural adhesives. The Automotive Wheel Coating Market in North America mirrors these macro demand dynamics, with both coatings and bonding materials markets benefiting from parallel OEM investment in advanced surface and material performance technologies as components of integrated vehicle platform development strategies.

Europe Automotive Adhesives & Sealants Trends

Europe is one of the most technologically advanced and regulatory-driven regional markets for automotive adhesives and sealants, with Germany, France, the United Kingdom, and Spain collectively anchoring demand through their industrial-scale OEM assembly operations. Germany, home to Volkswagen Group, BMW Group, and Mercedes-Benz Group, is the region's largest consumption market, while France and Spain are driven by Stellantis and Renault Group production volumes.

Despite volume headwinds, the structural re-engineering of European vehicle platforms toward lighter, electrified, and recyclable designs is elevating adhesive specifications and increasing the value of adhesive content per vehicle unit produced. The European Green Deal, the binding CO2 reduction mandates, and the revised ELV Directive are collectively reshaping material selection criteria across OEM engineering departments, creating a sustained product innovation imperative for adhesive manufacturers operating in one of the world's most demanding regulatory markets.

Asia Pacific Automotive Adhesives & Sealants Trends

Asia Pacific is the dominant regional market for automotive adhesives and sealants, driven by China's position as the world's largest single vehicle producer, India's rapidly maturing automotive manufacturing base, and the continued relevance of Japan and South Korea as precision engineering hubs. China produced 31.28 million vehicles in 2024, a 4% year-on-year advance per OICA statistics, with the country's New Energy Vehicle (NEV) penetration reaching 37% of new light-duty vehicle sales in the first half of 2024 per ICCT data.

India produced over 6 million vehicles in 2024 per OICA, benefiting from sustained OEM investment under the Ministry of Heavy Industries' PLI scheme for Advanced Chemistry Cell Battery Storage. Japan and South Korea, despite experiencing production declines of 8.6% and 1.2% respectively in 2024 per ACEA, maintain high-specification automotive adhesive demand driven by hybrid platform innovation, hydrogen fuel cell vehicle development, and precision bonding applications in advanced driver assistance systems.

Competitive Landscape

The global automotive adhesives & sealants market exhibits a moderately consolidated competitive structure, with a small number of diversified global specialty chemical conglomerates commanding dominant positions in the premium structural adhesives and EV battery bonding segments, while a broader tier of regional and application-focused players compete in commodity sealants and aftermarket maintenance categories. Key differentiators employed by market leaders including Henkel AG & Co. KGaA, Sika AG, 3M Inc., and Dow Inc. Include proprietary polymer chemistry platforms, long automotive OEM qualification histories, technical application engineering services co-located at OEM assembly sites, and active investment in sustainable, low-VOC, and debond-on-demand formulations.

Key Developments:

- In July 2025, Henkel Adhesive Technologies India, a Henkel AG & Co. KGaA subsidiary, opened a new automotive warehouse in Chakan, Pune. The facility enhances Just-in-Time (JIT) deliveries and supports the region's manufacturing sector growth through 2030 and beyond.

- In April 2025, PPG Industries acquired Revocoat from the Axson Group to expand its automotive adhesive and sealant offerings. Revocoat operates eight manufacturing facilities and an R&D center globally.

Companies Covered in Automotive Adhesives & Sealants Market

- 3M Inc.

- PPG Industries, Inc.

- BASF SE

- Arkema SA

- H.B. Fuller Company

- Henkel AG & Co. KGaA,

- Huntsman International LLC

- Sika AG

- Dow Inc.

- Wacker Chemie AG

- Jowat SE

- Permabond LLC

- Hernon Manufacturing Inc.

- Other Key Players

Frequently Asked Questions

The global Automotive Adhesives & Sealants Market is valued at US$ 9.6 Bn in 2026 and is projected to reach US$ 13.8 Bn by 2033, growing at a CAGR of 5.3% during the forecast period.

The foremost demand drivers are stringent vehicle emissions regulations including the EU's 90% CO2 tailpipe reduction mandate from 2035 and U.S. CAFE standards compelling OEMs to adopt lightweight multi-material architectures requiring advanced structural adhesives, and the rapid global expansion of EV production, which reached 17.1 million units globally in 2024 per Rho Motion, creating sustained demand for battery-grade adhesive and thermal management sealant systems.

Polyurethane is the leading resin type segment, accounting for approximately 34% of total market share in 2026. Its dominance reflects unmatched functional versatility across BIW structural bonding, windshield glazing, underbody sealing, and battery module encapsulation, combined with broad substrate compatibility and a strong OEM qualification base maintained by leading suppliers including Henkel, Sika, and Dow.

Asia Pacific leads the global Automotive Adhesives & Sealants Market, anchored by China's vehicle production of 31.28 million units in 2024representing 34% of global output per OICA. The region benefits from the world's largest OEM assembly concentration, deep tier-1 supply chain infrastructure, and the fastest-growing EV production volumes, with China's EV sales advancing 40% in 2024 per Rho Motion.

Leading global companies in the Automotive Adhesives & Sealants Market include Henkel AG & Co. KGaA, Sika AG, 3M Inc., Dow Inc., BASF SE, PPG Industries, Inc., Arkema SA, H.B. Fuller Company, Huntsman International LLC, Wacker Chemie AG, Illinois Tool Works Inc., ThreeBond Holdings Co., Ltd., Jowat SE, Permabond LLC, and Hernon Manufacturing Inc., among others.