- Technology

- Internet of Things (IoT) Market

Internet of Things (IoT) Market Size, Share, and Growth Forecast, 2026 - 2033

Internet of Things (IoT) Market by Component Type (Software, Services, Hardware), Connectivity (Cellular (4G/5G), LPWAN (LoRaWAN, NB-IoT), Wi-Fi, Bluetooth/BLE, Satellite, and Misc), Organization Size (Large Enterprises and Small & Medium Enterprises (SMEs)), Deployment Mode (Cloud-Based, On-Premises, and Hybrid ) End Use Industry (Manufacturing, Healthcare, Automotive & Transportation, Retail, Energy & Utilities, Smart Cities & Buildings, Agriculture, Consumer Electronics, and Misc.) and Regional Analysis for 2026 - 2033

Internet of Things (IoT) Market Size and Trends Analysis

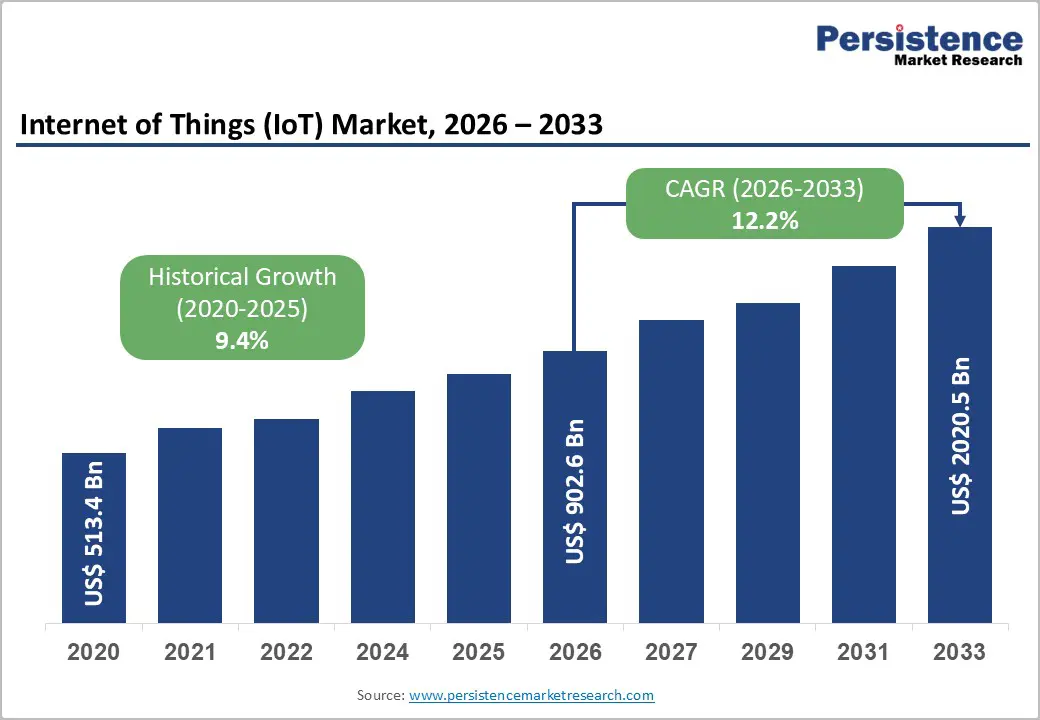

The Global Internet of Things (IoT) Market size was valued at US$ 902.6 billion in 2026 and is projected to reach US$ 2,020.5 billion by 2033, growing at a CAGR of 12.2% between 2026 and 2033. The market has already expanded from US$ 513.4 billion in 2020, reflecting a historical CAGR of 9.4%, underpinned by the proliferation of connected devices, cloud-native architectures, and enterprise digitalisation across manufacturing, healthcare, mobility, and smart infrastructure.

Structural shifts in B2B eCommerce, advances in industrial automation, and policy-driven digital initiatives in major economies reinforce demand for scalable IoT platforms and edge-to-cloud solutions. At the same time, state-led strategies in regions such as China and coordinated cybersecurity frameworks in North America and Europe are shaping standards, security baselines, and long-term competitive dynamics in the Internet of Things (IoT) Market.

Key Industry Highlights:

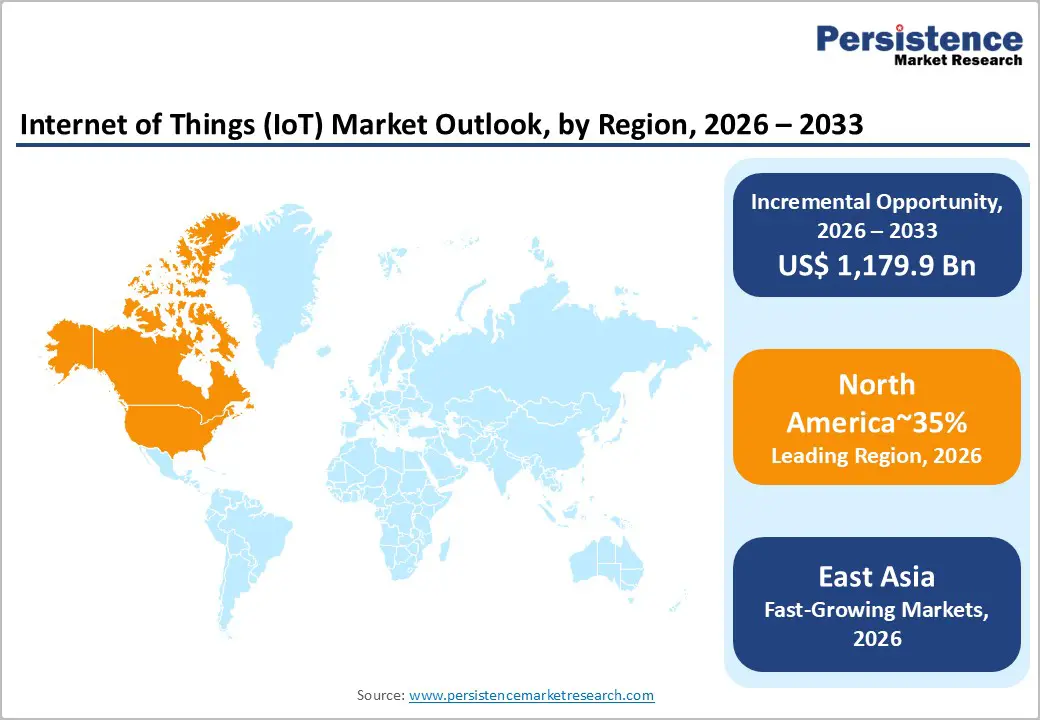

- Regional Leadership: North America leads the Global Internet of Things IoT Market with about 35 Percent share, driven by the presence of major cloud hyperscalers, strong telecom infrastructure, and large-scale deployments across energy storage, connected vehicles, and industrial automation.

- Strong European Adoption: Europe accounts for nearly 25 Percent share, supported by high consumer device penetration of around 70 Percent, robust industrial digitisation, and strict cybersecurity and data protection frameworks, accelerating enterprise IoT investments.

- Fast Rising East Asia Hub: East Asia holds roughly 23 Percent share, fueled by manufacturing dominance, state-led smart factory initiatives, expanding logistics networks, and rapid adoption of connected systems across China, India, and broader APAC economies.

- Leading Deployment Model: Cloud-based deployment dominates with 62.3 Percent share, benefiting from scalable compute, real-time analytics, and AI-enabled device orchestration offered by platforms such as AWS, Microsoft, and Oracle.

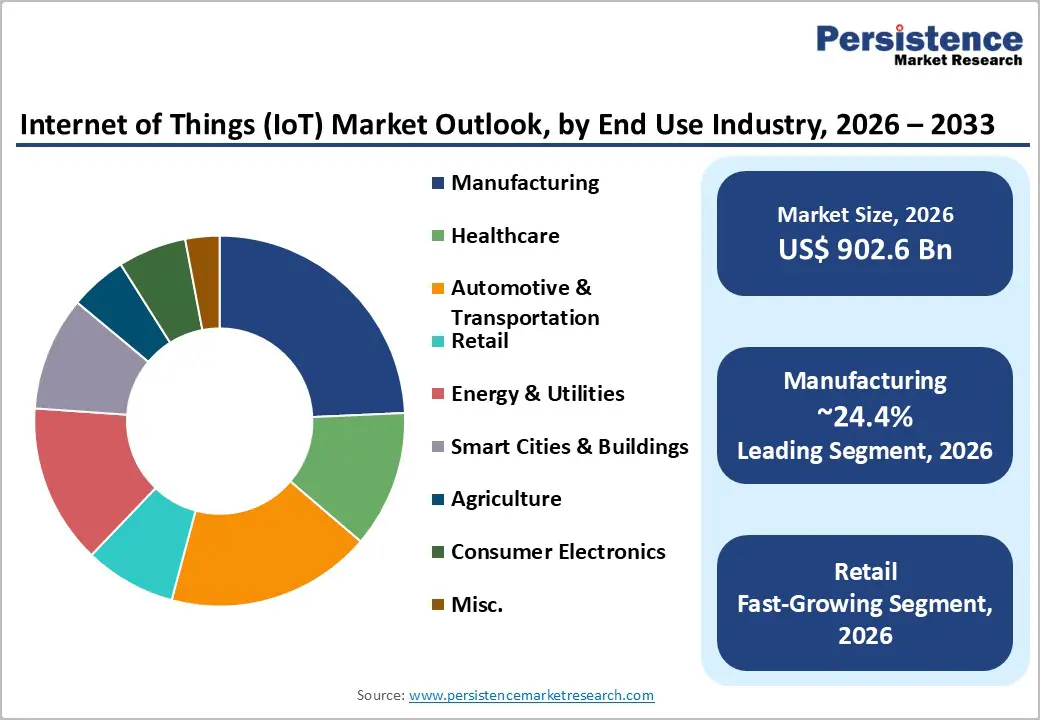

- Leading End Use Segment: Manufacturing commands 24.4 Percent share, driven by predictive maintenance, digital twins, asset monitoring, and Industry 4.0 modernisation across large-scale production facilities.

- Core Growth Driver: Rapid device proliferation and mainstream digital adoption, with nearly 70 Percent consumer IoT usage in the EU and 979 million internet users in India, continue to expand the installed base for IoT platforms, software, and lifecycle services.

| Key Insights | Details |

|---|---|

|

Internet of Things (IoT) Market Size (2026E) |

US$ 902.6 Bn |

|

Market Value Forecast (2033F) |

US$ 2,020.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.4% |

Market Dynamics

Growth Drivers

Device Proliferation and Mainstream Adoption Across Economies

The rapid expansion of connected devices across both consumer and enterprise environments is becoming a foundational driver of growth for the Internet of Things (IoT) Market. Rising internet penetration and greater digital familiarity are accelerating the use of smart products and connected systems, creating a broad installed base that continuously feeds demand for IoT platforms, hardware, and lifecycle services.

Eurostat data indicate that nearly 70 percent of EU citizens aged 16–74 used at least one internet-connected device in 2024, with adoption reaching 95 percent in the Netherlands and around 46 % in Poland, highlighting both widespread uptake and regional disparities. Consumer-oriented devices such as smart TVs, wearables, gaming consoles, and smart speakers account for the majority of usage, while healthcare-related IoT adoption remains comparatively low, suggesting substantial untapped potential in remote monitoring and assisted living.

Usage is also skewed toward younger demographics, with 84 percent penetration among individuals aged 16 to 24 compared to 45 percent among those aged 65 to 74, signalling long-term normalisation as digital-native populations mature. Collectively, this expanding ecosystem of connected devices is strengthening recurring opportunities for software platforms, security solutions, analytics, and managed services across the broader Internet of Things (IoT) Market.

Industrial and Enterprise Digitalization Across Major Regions

Industrial IoT and enterprise digitization are accelerating large-scale deployments of connected equipment, edge computing, and advanced analytics across the Internet of Things IoT) market. In India, adoption is supported by rapid internet expansion, with 979 million internet users by June 2025 and a telecom subscriber base of 1.21 billion, resulting in a tele density of 86.09 Percent, positioning the country among the largest digital ecosystems globally.

The telecom sector generated USD 43.42 billion in gross revenue in FY25, up from USD 39.22 billion in FY24, driven primarily by 4G and early 5G usage in data-intensive enterprise applications. At the same time, India hosts approximately 94 domestic companies focused on Industrial IoT, smart utilities, logistics, and connected consumer solutions, demonstrating a strong base of innovation and deployment. In Europe, the information and communication services sector contributed EUR 667 billion in value added, accounting for 6.6 Percent of the EU business economy in 2022, with labour productivity reaching EUR 92,800 per person, highlighting the high economic leverage of digital and IoT-enabled services. Together, these trends indicate rising enterprise investments in connected manufacturing, utilities, and logistics infrastructure, strengthening long-term growth opportunities in the Internet of Things IoT Market.

Cloud, AI, and Energy Transition Use Cases

Cloud native IoT platforms combined with global decarbonization initiatives are generating sustained demand for connected assets, remote monitoring, and intelligent control solutions across the Internet of Things IoT Market. According to the International Energy Agency Tracking Clean Energy Progress report, solar photovoltaic generation advanced 26 Percent in 2022, electric vehicle sales increased 55 Percent to exceed 10 million units globally, and grid-scale battery storage capacity is projected to reach nearly 970 gigawatts by 2030, almost 35 times the 2022 level.

Governments in China, the United States, India, and Europe continue to accelerate the deployment of clean energy and storage through incentives, regulatory reforms, and large-scale project pipelines, with global storage investment exceeding USD 20 billion in 2022 and projected to exceed USD 35 billion in 2023. These developments necessitate extensive IoT capabilities for asset monitoring, predictive maintenance, and remote operations across solar farms, storage systems, electric-vehicle charging infrastructure, and grid networks.

In parallel, cloud hyperscalers have spent years building scalable IoT platforms, with AWS alone reporting hundreds of millions of devices connected daily across its IoT services portfolio, embedding analytics and artificial intelligence into industrial and infrastructure environments. Collectively, the convergence of clean energy expansion and cloud-based IoT ecosystems is strengthening long-term demand across the Internet of Things IoT Market.

Market Restraining Factors

Cybersecurity, Data Privacy, and Geopolitical Risk

Security vulnerabilities, cross-border data flows, and geopolitical tensions impose structural constraints on the Internet of Things (IoT) Market. A U.S.–China Economic and Security Review Commission report highlights China’s state led IoT strategy, significant public funding, and efforts to influence international IoT standards, which could embed domestic technical norms into global systems.

The same study notes the need for further research into IoT security vulnerabilities and civil–military fusion, raising the risk of unauthorised access to devices and data, particularly as Chinese suppliers expand globally. Coupled with broad government data-access powers, this environment amplifies privacy and national security concerns in major importing markets, prompting regulators to tighten controls and raising compliance costs for multinational vendors.

Skills Gaps, Integration Complexity, and Uneven Adoption

Despite the broad penetration of connected technologies, IoT deployment remains uneven across company sizes and user groups, limiting the full-scale realisation of benefits in the Internet of Things IoT Market. Eurostat data indicate that perceived lack of necessity accounts for 41 Percent of non-adoption among EU citizens, while older demographics aged 65 to 74 report only 45 Percent device usage, reflecting slower digital engagement.

On the enterprise side, IoT adoption for condition-based maintenance reaches 56 Percent in large enterprises but only 26 Percent in small firms and stands at 36 Percent versus 15 Percent for production process optimisation, highlighting clear capability and investment gaps between business tiers. Smaller organisations often struggle to integrate information technology and operational technology systems, cybersecurity tools, and legacy infrastructure, which increases implementation timelines and costs. Limited access to skilled personnel and capital further restricts small and medium enterprises from executing end-to-end IoT modernisation strategies. Together, these disparities create structural barriers that temper the overall growth momentum of the Internet of Things IoT Market.

Key Market Opportunities

Smart Manufacturing, Digital Twins, and Industrial Automation

Industrial automation and advanced analytics create a multi-layer opportunity for vendors in the Internet of Things (IoT) Market to deliver software, hardware, and services across manufacturing value chains. Cognizant’s strategic collaboration agreement with AWS, announced in October 2024, focuses on smart manufacturing and Industry 4.0 solutions that leverage IoT, AI, and cloud technologies, including digital twins, simulations, and advanced manufacturing execution systems. Demonstration centers in the U.S. and India showcase real-time visibility, predictive maintenance, and AI driven decision support for global manufacturers.

This opportunity is reinforced by platform and ecosystem advancements. AWS launched AWS IoT TwinMaker and AWS IoT SiteWise to support digital twins and large-scale industrial data collection, while AWS IoT Greengrass and Greengrass Nucleus Lite extend secure edge processing even to devices with as little as 5 MB of memory, widening the scope of industrial IoT on constrained hardware. OMRON and Cognizant’s 2025 partnership to integrate IT and OT in automotive, semiconductor, and life sciences manufacturing illustrates how automation vendors and system integrators combine capabilities to drive productivity, sustainability, and remote operations. Together, these developments open opportunities for platform vendors, integrators, and device OEMs to deliver outcome-linked services and modular solutions in the Internet of Things (IoT) Market.

Retail, Consumer Experience, and Omnichannel Operations

Retail digitization and customer experience transformation create a fast-expanding demand pool within the Internet of Things (IoT) Market, particularly for software and services that orchestrate in store, online, and supply-chain data. Cognizant’s Stores 360 solution, launched in January 2025, exemplifies this trend: it uses IoT, AI, and generative AI to streamline store operations, monitor assets, and enable predictive workflows. The solution claims 30–40% reduction in operating expenses, 10–20 percent shorter new-store opening timelines, and up to 98 percent uptime of systems and assets, showing concrete business outcomes from IoT-enabled operations

On the consumer side, smart home and entertainment devices, such as connected TVs, wearables, and smart speakers, already exhibit broad adoption across the EU, providing a foundation for data-driven personalization and omnichannel engagement. Integrating these devices with in-store sensors, digital signage, and mobile apps enables demand sensing, frictionless checkout, and adaptive promotions, all of which support retail’s position as the fastest advancing end-use segment. For vendors, this translates into opportunities to bundle software platforms, managed services, and edge hardware for retailers that seek measurable ROI but often lack internal IoT integration capabilities in the Internet of Things (IoT) Market.

Category-wise Analysis

Product Type Insights

Software forms the backbone of value creation in the Internet of Things (IoT) Market, accounting for 40.2% of revenues in 2026. This reflects the centrality of device management platforms, data ingestion pipelines, digital twins, application enablement layers, and analytics engines in monetizing sensor data. AWS IoT, for example, has evolved from IoT Core to a broad software suite including Greengrass, TwinMaker, FleetWise, SiteWise, and Device Management, all delivering recurring, usage-based revenue. Similarly, industrial and telecom players build proprietary software layers to differentiate on visualization, orchestration, and AI-driven insights.

Services consulting, system integration, managed operations, and support constitute the fastest advancing component segment. Cognizant’s recognition as a Horizon 3 Leader in the 2024 HFS Horizons IoT services report underscores the market’s shift toward large-scale, service-heavy engagements using platforms like APEx, Neuro Edge, and OnePlant for asset performance and smart manufacturing. In retail, Stores 360 demonstrates how services plus software deliver operational KPIs, while IT-OT integration partnerships such as OMRON–Cognizant or Arviem–Tech Mahindra for IoT-enabled supply chains reinforce recurring services revenue. These dynamics supports higher attach rates of consulting and managed services alongside software and hardware in the Internet of Things (IoT) Market.

Deployment Mode Insights

Cloud-based deployment dominates the Internet of Things (IoT) Market, representing 62.3% of deployments in 2026. Cloud platforms provide elastic compute, storage, and analytics capacity necessary to handle large volumes of IoT data and support real-time processing. AWS’s decade-long IoT portfolio, with hundreds of millions of devices connected daily, exemplifies this scale, enabling automotive OEMs like Mercedes-Benz and Honda to migrate millions of vehicles and charging infrastructure to managed cloud IoT messaging, monitoring, and analytics services. Similar strategies by Oracle, Microsoft, and major telcos embed IoT into their cloud ecosystems.

On premises deployment advances most rapidly, driven by data sovereignty, low-latency control, and operational technology integration needs. Cisco’s launch of new cloud services within its IoT Operations Dashboard and integration with Cyber Vision illustrates how enterprises combine remote visibility with secure local management of industrial assets, aligning with IT and OT requirements. In sectors like energy, manufacturing, and defense, on-premises or hybrid models support deterministic performance and regulatory compliance while still leveraging cloud for aggregated analytics.

End Use Industry Insights

Manufacturing accounts for the largest share, 24.4%, of the Internet of Things (IoT) Market in 2026, reflecting long-standing adoption of IIoT for process optimization, asset performance, and quality control. Large enterprises are significantly ahead of smaller firms, with IoT usage for condition-based maintenance at 44 percent vs. 22 percent and for production process optimization at 36 percent vs. 15 percent, underscoring the concentration of capability in larger plants and multinationals. Solutions like AWS IoT SiteWise, FleetWise, and Cognizant’s OnePlant enable continuous data capture, contextualization, and analytics for manufacturing and logistics operations.

Regional Insights and Trends

East Asia Market Trend

East Asia accounts for around 23% of the Internet of Things (IoT) Market, driven by manufacturing dominance, state-led industrial policy, and rapidly expanding digital ecosystems. China’s IoT trajectory is deeply intertwined with its semiconductor and industrial strategies; government-backed programs and civil–military fusion has positioned the country as a credible competitor to the U.S. by aligning state, industry, and research institutions. The same policy direction raises international concerns over standards influence, cybersecurity, and data governance, prompting counterbalancing measures in other regions.

India’s IoT market is characterised by rapid adoption across both industrial and consumer domains. The country’s telecom sector counts 1.21 billion subscribers, 86.09 percent tele density, and 979 million internet users, supporting nationwide IoT deployment potential. A domestic ecosystem of around 94 IoT companies spans manufacturing automation, smart utilities, logistics, and consumer devices, positioning India as both a large demand market and a development hub. In parallel, East Asia is a leading player in B2B e-commerce, with APAC estimated to account for approximately 80 percent of global B2B e-commerce GMV (US$36,163 Bn) by 2026, reinforcing structural demand for IoT-enabled logistics, warehousing, and trade facilitation. Together, these factors underpin robust IoT investment in manufacturing, cities, and logistics across East Asia

North America Market Trend

North America accounts for approximately 35% of the global Internet of Things (IoT) Market, underpinned by leading hyperscale cloud providers, robust telecommunications infrastructure, and large enterprise IT budgets. The U.S. energy storage sector illustrates IoT’s role in critical infrastructure: operational battery storage exceeded 40 GW by 2025, up from 47 MW in 2010, with projections of 98 GW by 2030 and 5.6 GW installed in Q2 2025 alone. These assets depend on IoT for monitoring, forecasting, and grid integration. In telecom, the U.S. market supports AI- and IoT-ready network upgrades, as evidenced by Cisco’s 2025 secure network architecture launch, designed to support AI and IoT workloads and simplify IT/OT operations.

AWS’s decade-long IoT portfolio, used by automakers like Mercedes-Benz and Honda for connected vehicles and charging optimisation, anchors the cloud side of the ecosystem. Regulatory frameworks emphasise data protection and critical infrastructure security, with sector-specific rules for healthcare, utilities, and defence. Competitive dynamics are shaped by U.S.-headquartered cloud providers, networking vendors, and global systems integrators, many of which use North America as a launchpad for global IoT solutions. The combination of advanced infrastructure, robust energy-transition pipelines, and large industrial bases supports sustained double-digit investment in IoT in the region.

Europe Market Trend

Europe accounts for approximately 25% of the Internet of Things (IoT) Market, underpinned by robust regulatory frameworks, high digital adoption, and advanced industrial bases. The EU’s information and communication services sector contributed €667 Bn of value-added, 6.6% of the total business economy in 2022, with 7.2 million employees and high labour productivity. Consumer IoT is mainstream: 70% of citizens aged 16 to 74 used at least one connected device in 2024, with uptake as high as 95% in the Netherlands, and device usage led by connected TVs and wearables. These trends support smart-home, entertainment, and health-monitoring applications

On the enterprise side, European firms leverage IoT in industrial and infrastructure contexts, with a strong emphasis on cybersecurity and privacy via GDPR and related regulations. Operators such as Vodafone Business and Transatel are extending IoT connectivity and network APIs into cloud platforms like Oracle’s Enterprise Communications Platform, enabling secure, real-time device management across more than 180 countries. EU climate and energy policies, including strong support for storage and renewables, and European Commission recommendations on storage deployment further stimulate the use of IoT in energy and utilities. The regional market is competitive but regulated, with an emphasis on trusted providers, data residency, and adherence to emerging EU AI and cybersecurity frameworks.

Competitive Landscape

The Global Internet of Things (IoT) Market is largely consolidated at the platform and infrastructure level, with major players such as Microsoft, Amazon Web Services (AWS), Google, Cisco, and IBM dominating through comprehensive cloud-based IoT platforms, analytics, and enterprise integration solutions. Telecom and connectivity leaders like Huawei and Ericsson also play key roles by enabling large-scale device connectivity and global network orchestration, particularly for industrial and smart city applications. Beyond these top players, the market remains moderately fragmented, with numerous regional solution providers, systems integrators, and vertical specialists addressing niche needs.

Companies such as PTC, Siemens, and Samsara focus on industrial IoT, telematics, and asset management, often partnering with larger platforms for end-to-end solutions. This creates a multi-layered ecosystem where consolidation exists in cloud and connectivity services, while fragmentation persists in applications and services.

Key Industry Developments

- December 2025, Amazon Web Services (AWS) strengthened its end-to-end AWS IoT portfolio with hundreds of Bns of devices connected daily, reinforcing its full-stack IoT platform (IoT Core, Greengrass, TwinMaker, FleetWise, SiteWise) supporting large-scale industrial, automotive, healthcare, and smart infrastructure deployments globally.

- September 10, 2025, Cisco & Tata Communications Integrated Tata Communications MOVE’s global eSIM orchestration platform with Cisco IoT Control Centre, enabling enterprises to activate, manage, and scale IoT devices across multiple networks in 200-plus countries, simplifying global SIM lifecycle management for over 270 Bn connected IoT devices.

Companies Covered in Internet of Things (IoT) Market

- Microsoft Corporation

- Amazon Web Services (AWS)

- Google LLC

- Cisco Systems

- IBM

- Huawei Technologies

- Oracle Corporation

- SAP SE

- PTC Inc.

- Hitachi Vantara

- Accenture PLC

- Siemens AG

- Qualcomm Technologies

- Intel Corporation

- Samsara Inc.

Frequently Asked Questions

The global Internet of Things (IoT) Market is projected to be valued at US$ 902.6 Bn in 2026.

The Cloud-Based segment is expected to account for approximately 62.3% of the Global Internet of Things (IoT) Market by deployment mode in 2026.

The market is expected to witness a CAGR of 12.2% from 2026 to 2033.

Growth in the Internet of Things IoT Market is driven by rapid proliferation of connected consumer and enterprise devices, expanding industrial and enterprise digitization, and rising adoption of cloud, AI, and energy transition use cases that increase demand for smart monitoring, automation, and analytics solutions across sectors. .

Smart manufacturing and Industry 4.0 enable opportunities in digital twins, industrial automation, edge analytics, and outcome-based services across factories, while retail and consumer digitization drive demand for IoT enabled store operations, asset monitoring, omnichannel integration, and data driven customer experience solutions in the Internet of Things IoT Market.

Key players in the Internet of Things (IoT) Market include Microsoft, Amazon Web Services (AWS), Google, Cisco Systems, IBM, and Huawei Technologies.