- Specialty & Fine Chemicals

- Automotive Silicone Market

Automotive Silicone Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Silicone Market by Product Type (Rubber, Adhesives & Sealants, Coatings, and Other Products), Application (Interior & Exterior Parts, EDT System, Electrical System, Suspension System, Other Applications), by End-user (OEM, Aftermarket), and Regional Analysis for 2025 - 2032

Automotive Silicone Market Size and Trends Analysis

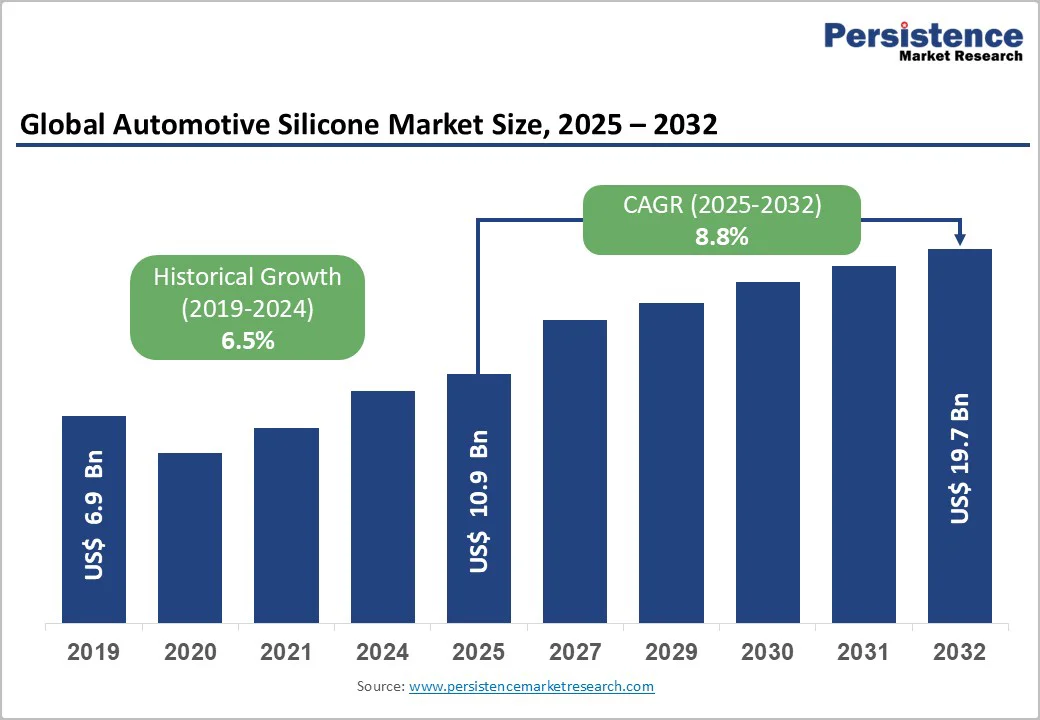

The global automotive silicone market size is valued at US$ 10.9 Billion in 2025 and is projected to reach US$ 19.7 Billion by 2032, growing at a CAGR of 8.8% between 2025 and 2032. This robust expansion is primarily driven by the accelerating adoption of electric vehicles requiring superior thermal management materials, stringent global emissions regulations mandating lightweight vehicle components, and the automotive industry's increasing focus on safety and performance enhancement through advanced silicone-based solutions. According to the IEA, global electric car sales exceeded 17 million in 2024, with EVs accounting for over 20% of new car sales.

Key Industry Highlights:

- Product Leadership: Rubber segment dominates with above 60% revenue share; adhesives & sealants represent fastest-growing category driven by lightweighting and multi-material vehicle construction trends

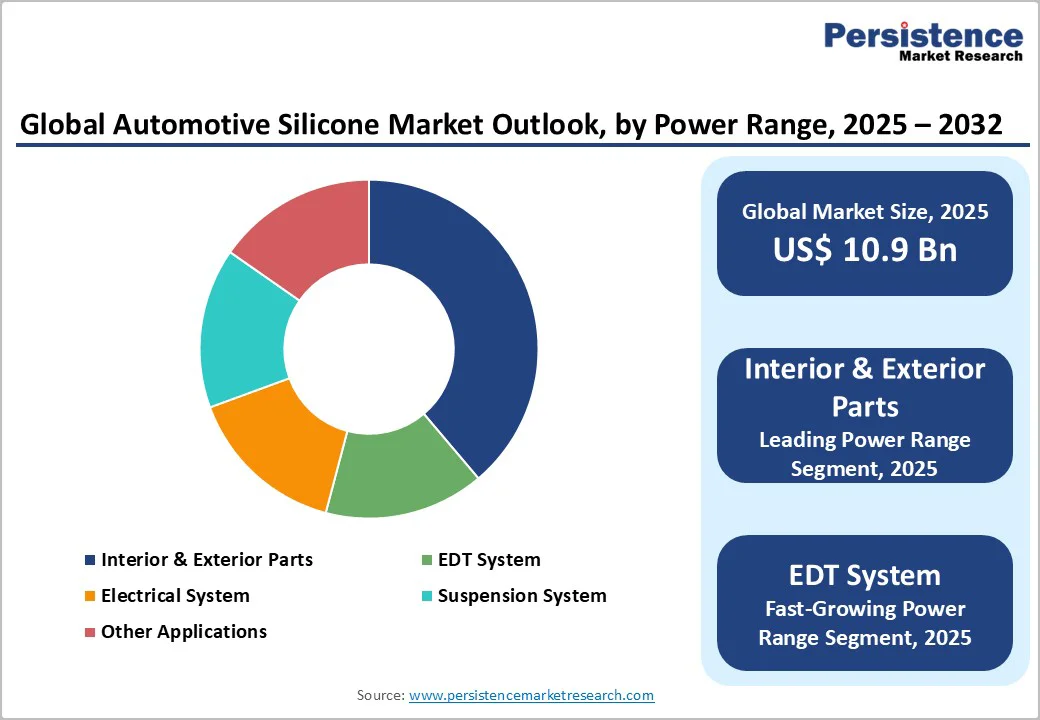

- Application Dynamics: Interior & exterior parts command above 35% revenue share; Engine & Drive Train (EDT) systems exhibit highest growth rate propelled by EV power electronics thermal management requirements

- End-user Distribution: OEM segment maintains above 70% market dominance through long-term supply agreements; aftermarket demonstrates fastest growth supported by aging vehicle fleets and expanding e-commerce distribution

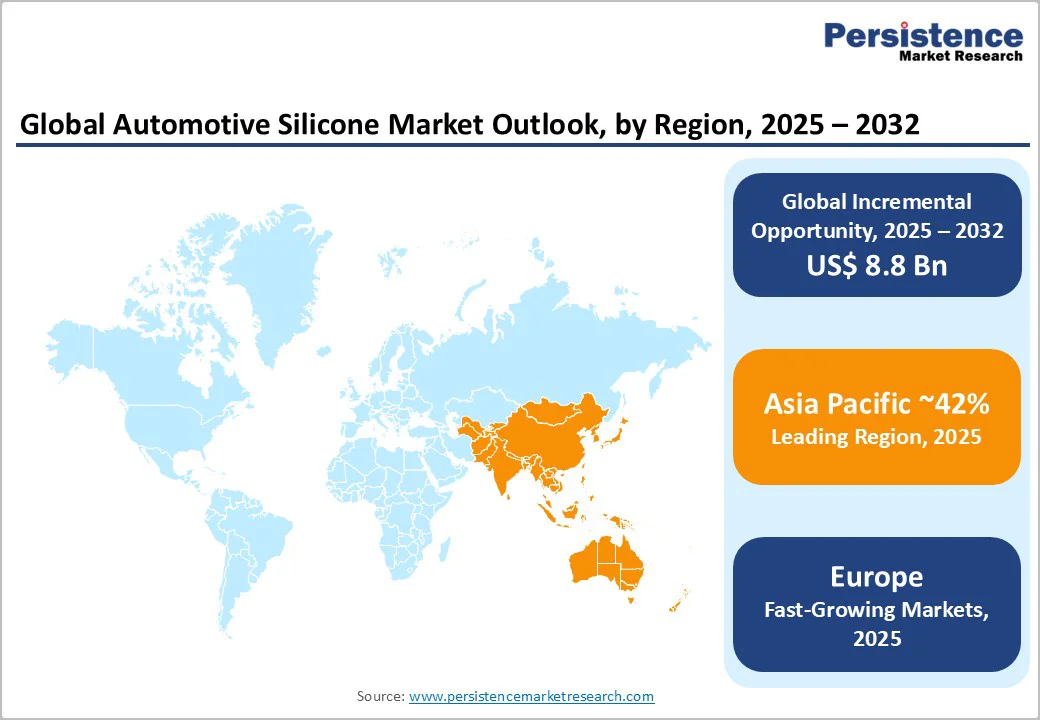

- Regional Leadership: Asia Pacific captures above 42% global market share with fastest growth trajectory led by China (26+ million vehicle production) and India (11-13% CAGR projection); Europe emerges as the fastest-growing developed region

- Strategic Momentum: Major consolidation activity, including KCC's acquisition of MPM Holdings (May 2024) and Trelleborg acquisition of Sico (May 2025); new product launches by Dow, Shin-Etsu, and Wacker targeting EV-specific applications

- Technology Drivers: Electric vehicle adoption exceeding 14 million units globally (2023) and projected 58% of passenger vehicle sales by 2040 creates sustained silicone demand growth across battery systems, thermal management, and power electronics applications

| Key Insights | Details |

|---|---|

|

Automotive Silicone Market Size (2025E) |

US$ 10.9 Bn |

|

Market Value Forecast (2032F) |

US$ 19.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.5% |

Market Dynamics

Drivers - Electric Vehicle Revolution and Thermal Management Requirements

The global transition toward electric mobility stands as the paramount growth driver for automotive silicone demand. Battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) require advanced thermal management solutions to maintain optimal operating temperatures, prevent thermal runaway, and extend battery lifespan. Silicone materials with thermal conductivity ranging from 1 W/m·K to 8 W/m·K are extensively deployed in battery pack encapsulation, gap fillers between battery modules and cooling systems, and thermal interface materials. Tesla's implementation of 4680 battery cells utilizes silicone adhesives with 3 W/m·K thermal conductivity to dissipate heat evenly across cell surfaces.

According to the IEA, global electric car sales exceeded 17 million in 2024, with EVs accounting for over 20% of new car sales. China led the market with more than 11 million EV sales, accelerating demand for advanced battery materials. CATL’s cell-to-pack integration technology, which removes metal module frames, increases reliance on silicone adhesives and sealants, boosting material consumption by around 40% per battery system and strengthening market growth.

Lightweighting Mandates and Fuel Efficiency Regulations

Stringent corporate average fuel economy (CAFE) standards and emissions regulations globally are compelling automotive manufacturers to pursue aggressive weight reduction strategies. The U.S. Environmental Protection Agency (EPA) mandates average fuel economy targets of 49 miles per gallon by 2026, while the European Union's CO2 emission standards require 95 grams CO2 per kilometer for new passenger cars.

Silicone-based structural adhesives and sealants enable manufacturers to replace traditional spot welding and mechanical fasteners, reducing vehicle weight by 15-20%. Ford Motor Company successfully reduced approximately 317 kilograms from the aluminum F-150 body structure using two-part epoxy and silicone bonds, which distribute loads over wider surface areas while enabling thinner panels. Life-cycle assessments conducted under ISO 14040 standards demonstrate that adhesive bonding consumes 30-40% less energy compared to resistance spot welding during manufacturing, further supporting sustainability objectives alongside weight reduction benefits.

Restraint - Regulatory Complexity and Environmental Compliance

The European Chemicals Agency (ECHA) has added several cyclic siloxanes including D4 (Octamethylcyclotetrasiloxane), D5 (Decamethylcyclopentasiloxane), and D6 (Dodecamethylcyclohexasiloxane) to the REACH Candidate List of Substances of Very High Concern (SVHC) due to persistent, bioaccumulative, and toxic (PBT) properties. While this listing does not constitute an immediate ban, it imposes strict communication requirements throughout supply chains and signals potential future authorization requirements or use restrictions.

Formulations containing D4 or D5 at concentrations ≥0.1% w/w face restrictions for certain applications in the European Union as of 2022. Compliance with REACH Regulation (EC No. 1907/2006) requires manufacturers to update Safety Data Sheets, notify customers, and potentially reformulate products, incurring development costs estimated at $500,000-2 million per product line. These regulatory burdens create competitive disadvantages for European manufacturers compared to regions with less stringent chemical oversight, potentially influencing investment location decisions and market dynamics.

Opportunity - Bio-Based and Sustainable Silicone Development

The automotive industry's commitment to circular economy principles and carbon neutrality targets creates significant opportunities for bio-based silicone materials. Wacker Chemie AG's ELASTOSIL® eco product line, certified under the REDcert2 standard, utilizes plant-based methanol derived from renewable feedstocks, reducing carbon footprint by approximately 40% compared to conventional petroleum-based production.

As major automotive OEMs including Volkswagen, BMW, and Mercedes-Benz commit to carbon-neutral production by 2039-2050, demand for sustainable materials with verified traceability will accelerate. The European Union's Circular Economy Action Plan and proposed Battery Regulation requiring minimum recycled content percentages create regulatory tailwinds for bio-based silicone adoption. Market analysts project the sustainable silicone segment could capture 15-20% of total automotive silicone demand by 2030, representing a $3-4 billion addressable market opportunity.

Category-wise Analysis

Product Type Insights

Silicone Rubber Dominates Automotive Silicone Demand While Adhesives And Sealants Surge with Lightweight Vehicle Innovation.

The automotive silicone market is strongly led by the rubber segment, which accounts for over 60% of revenue in 2025 due to its extensive use in gaskets, seals, hoses, vibration-dampening parts, and weatherstripping. Silicone rubber maintains performance across extreme temperatures ranging from –60°C to +300°C, offering superior compression set resistance and aging stability compared to traditional organic rubbers. HTV and RTV silicone rubbers support demanding under-hood environments, including turbocharger seals, emission system components, and cylinder head gaskets where durability is essential. Liquid silicone rubber (LSR) further enhances adoption by enabling high-precision injection molding, reducing manufacturing costs by 20–30%. Growing EV production is increasing silicone rubber use in battery pack sealing for achieving IP67/IP68 protection, supported by silicone foam gaskets that retain 90–95% compression across thermal cycles. Additionally, silicone weatherstripping outperforms EPDM by extending service life to 10–12 years, lowering warranty costs.

The adhesives and sealants segment is the fastest-growing category as OEMs accelerate lightweighting and multi-material vehicle design. Structural silicone adhesives enable bonding of mixed substrates like steel, aluminum, composites, and carbon fiber critical for modern body structures. Fast-curing two-component systems (under 30 minutes) support high-volume assembly, while gap-filling capabilities of 5–10 mm improve load distribution. Adhesive-bonded structures reduce vehicle mass by 7–10% and increase torsional rigidity by 15–20%, aligning with safety regulations and fuel-efficiency requirements.

Application Mode Insights

Interior and Exterior Components Dominate Automotive Silicone Demand While Engine and Drivetrain Applications Grow Rapidly.

Interior and exterior components remain the largest application segment in the automotive silicone market, accounting for more than 35% of total revenue due to their widespread use in sealing, bonding, insulation, and surface enhancement functions. Silicone-based weatherstrips and window gaskets significantly improve cabin comfort, reducing noise intrusion by 3–5 decibels compared to conventional materials. Premium vehicle manufacturers increasingly use soft-touch silicone coatings on dashboards, trims, and control surfaces to elevate tactile quality and enhance interior aesthetics. On the exterior, the shift toward LED and adaptive headlamp technologies is boosting the adoption of silicone optics and encapsulants, valued for their optical clarity, UV resistance, and long-term stability. Silicone sealants also play a key role in automotive glass bonding, enabling flush-mounted windshields that improve aerodynamics and contribute to a 0.01–0.02 Cd reduction in drag, translating to up to 2% better fuel efficiency.

The Engine and Drive Train (EDT) segment represents the fastest-growing application, driven by rising thermal loads in modern turbocharged engines that operate above 150°C. This environment demands silicone gaskets and seals with superior heat and chemical resistance. Electric vehicles further accelerate silicone demand through its vital role in inverter encapsulation, thermal interface materials, and motor insulation. High-performance SiC inverters operating at 175–200°C rely on thermally conductive silicone gap fillers capable of withstanding over 100,000 thermal cycles. Additionally, transmission systems are adopting silicone-based lubricants that maintain viscosity stability across broad temperature ranges, extend service life, and reduce environmental impact through fewer fluid changes.

End-user Insights

OEM dominance drives over 70% of automotive silicone demand while the aftermarket rapidly accelerates globally.

The automotive silicone market is strongly dominated by the OEM segment, which accounts for more than 70% of total revenue due to silicone’s deep integration into vehicle design, engineering, and assembly. OEMs typically engage in long-term, multi-year supply contracts with silicone manufacturers, often committing to annual volumes exceeding 1,000 metric tons for major vehicle platforms. These partnerships frequently involve joint formulation development to meet specific performance benchmarks such as thermal stability, material compatibility, and lifecycle durability.

Platform consolidation further strengthens OEM demand; for example, Volkswagen’s MEB EV platform used across more than ten models standardizes battery sealing and thermal management needs, increasing silicone consumption per platform. OEMs increasingly prioritize total cost of ownership rather than per-unit pricing, favoring silicone solutions that reduce warranty claims, extend component life, and improve assembly efficiency.

In contrast, the aftermarket segment is emerging as the fastest-growing end-use category, supported by aging global vehicle fleets, rising technical complexity, and growing DIY maintenance culture. With vehicle age in the U.S. reaching 12.5 years in 2023, demand for replacement seals, gaskets, and weatherstripping is rising, especially given silicone’s 50–80% longer service life compared to conventional materials. E-commerce platforms have accelerated access to premium silicone products, with online retailers reporting 25–30% annual growth. Additionally, the shift toward EVs where traditional maintenance declines redirects spending to silicone-intensive needs such as HVAC sealing, battery thermal management, and electronics protection, further boosting aftermarket expansion

Regional Insights

Asia Pacific Strengthens Its Leadership in Automotive Silicone As EV Growth And Global Expansion Accelerate Demand.

Asia Pacific continues to dominate the global automotive silicone market, accounting for over 42% of revenue in 2025, supported by its position as the world’s largest automotive manufacturing hub with more than 50 million vehicles produced annually. The growth of the region is driven by accelerating EV penetration, rising middle-class populations, and strong localization of automotive production.

China remains the core growth engine, representing 60–65% of regional silicone demand. In 2024, China produced nearly 30% of the world’s vehicles, more than double U.S. output, reinforcing its position as the largest automotive manufacturer and the leading global vehicle exporter. Beyond exports, Chinese automakers are rapidly establishing manufacturing plants in Europe, Southeast Asia, and South America, transforming China from a national industry leader into a truly global manufacturing force. This overseas expansion will further strengthen China’s market power and amplify demand for silicone materials used in EV batteries, thermal management, electronics, and high-performance components.

Japan contributes 15–18% of regional demand through hybrid and fuel-cell vehicle innovation, while India and ASEAN markets show strong double-digit growth. Combined with low-cost manufacturing advantages and over 200,000 metric tons of new silicone capacity being added in China by 2026, Asia Pacific’s leadership in the automotive silicone market will continue to intensify.

European Market Accelerates As the Fastest-Growing Automotive Silicone Market Driven By Electrification and Strict Sustainability Regulations.

Europe is emerging as the fastest-growing region in the global automotive silicone market, supported by strong regulatory momentum, rapid electrification, and rising demand for high-performance materials across premium vehicle segments. Europe benefits from robust compliance frameworks and sustainability-driven innovation rather than production volume expansion. Germany, the United Kingdom, France, and Spain collectively account for 65–70% of demand, reflecting Europe’s established automotive manufacturing base.

The European Union’s REACH regulation, the Green Deal target of carbon neutrality by 2050, and upcoming Euro 7 emission standards are accelerating OEM adoption of advanced silicone materials for lightweighting, thermal management, and durability enhancement. Circular Economy Action Plan requirements further support the shift toward long-life, recyclable silicone solutions.

Germany leads with 35–40% of regional demand, driven by premium OEMs such as Mercedes-Benz, BMW, Porsche, and Volkswagen, which rely heavily on specialty silicones for EV platforms and advanced electronics. France and the UK contribute 20–25% combined, supported by Stellantis’ manufacturing strength and growing EV battery investments. Spain, producing 2.1 million vehicles, remains a key Southern European hub. Europe’s competitive landscape is anchored by Wacker Chemie and Elkem, whose sustainability-certified silicone portfolios align with OEM decarbonization goals.

Competitive Landscape

The global automotive silicone market is moderately consolidated, with the top five companies, Dow, Wacker Chemie AG, Momentive Performance Materials, Shin-Etsu Chemical, and Elkem ASA, collectively holding 55–60% of the total market share. These industry leaders maintain their dominance through extensive, diversified product portfolios, long-standing OEM partnerships, and global production networks consisting of more than 60 manufacturing facilities. Their competitive edge is reinforced by continuous investment in R&D, strong technical service capabilities, and the ability to supply high-performance silicones tailored for advanced EV architectures, autonomous systems, and premium vehicle applications.

Mid-tier players such as Evonik Industries, KCC Corporation, Henkel AG, and Bluestar Silicones differentiate themselves through specialization, focusing on select product lines, regional strengths, or niche applications that require unique performance characteristics. Entering the market remains challenging due to stringent automotive qualification cycles lasting 18–36 months and substantial investments of USD 5–10 million for testing, application development, and OEM validation.

Regional manufacturers, particularly in China and Southeast Asia (e.g., Zhejiang Xinan Chemical), compete on cost efficiency by targeting standard-grade silicone applications. Meanwhile, global technology leaders are increasingly innovating in areas such as thermal management, electronics protection, and structural bonding to stay ahead in the fast-evolving EV landscape.

A clear example of rising innovation is Henkel’s launch of Loctite SI 5643 and SI 5637, advanced silicone potting compounds engineered for high-density EV power electronics, including inverters and onboard chargers. These products address a key industry challenge thermal buildup resulting from increasing “x-in-1” powertrain integration and demonstrate how leading suppliers are developing specialized solutions in close collaboration with OEMs and battery manufacturers to strengthen their competitive position.

Key Industry Developments

- In 2025, Trelleborg Group AB finalized the acquisition of Sico Gesellschaft für Siliconverarbeitung mbH and its Czech joint venture Sico Silicone s.r.o., strengthening its industrial solutions portfolio after previously holding a 50/50 stake in Sico since 2016.

- In March 2024, KCC Corporation entered into an agreement to fully acquire Momentive Performance Materials Group, resulting in the exit of minority shareholder SJL Partners and consolidating KCC’s position in the global silicones market.

- In 2024, BRB Silicones launched BRB SF 1802, an aminoalkyl functional polydimethylsiloxane designed for automotive care applications, offering enhanced storage stability and superior performance compared to reactive formulations.

- In 2023, Shin-Etsu Chemical developed a new silicone rubber optimized for molding applications, specifically engineered as insulation material for high-voltage automotive onboard cables used in electrified vehicles.

- In December 2022, Dow introduced its SILASTIC™ SA 994X Liquid Silicone Rubber (LSR) series, advancing smart, safe, and sustainable mobility technologies with next-generation LSR solutions.

Companies Covered in Automotive Silicone Market

- Henkel AG & Co. KGaA

- 3M Company

- Permatex

- Elkem ASA

- Basildon Chemicals

- Specialty Silicone Products, Inc.

- Dow

- ACC Silicones Ltd.

- Wacker Chemie AG

- Shin-Etsu Chemical Co.

- Other Market Players

Frequently Asked Questions

The Automotive Silicone market is estimated to be valued at US$ 10.9 Bn in 2025.

The key demand driver for the Automotive Silicone market is the rapid shift toward electric and technologically advanced vehicles, which require high-performance silicone materials for thermal management, insulation, sealing, bonding, and electronics protection.

In 2025, the Asia Pacific region will dominate the market with an exceeding 42% revenue share in the global Automotive Silicone market.

Among applications, interior & exterior parts have the highest preference, capturing beyond 35% of the market revenue share in 2025, surpassing other applications.

Specialty Silicone Products, Inc., Dow, ACC Silicones Ltd., Wacker Chemie AG, Shin-Etsu Chemical Co., are a few leading players in the Automotive Silicone market.