- Specialty & Fine Chemicals

- U.S. Automotive Engine Oils Market

U.S. Automotive Engine Oils Market Size, Share, and Growth Forecast 2026 – 2033

U.S. Automotive Engine Oils Market by Oil Type (Mineral, Fully Synthetic, Semi Synthetic), Vehicle Type (Passenger Cars, Commercial Vehicles, Other), Engine Type (Gasoline, Diesel, Other), and Regional Analysis for 2026–2033

U.S. Automotive Engine Oils Market Size and Trend Analysis

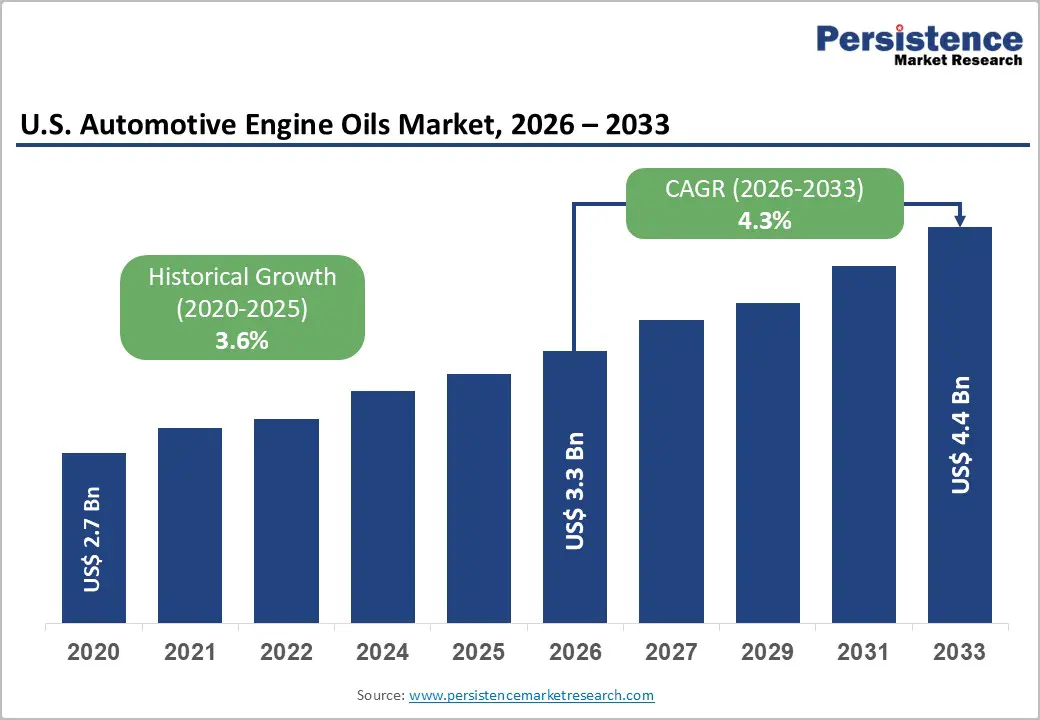

The U.S. Automotive Engine Oils market size is supposed to be valued at US$ 3.4 billion in 2026 and is projected to reach US$ 4.4 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033.

The market is underpinned by a robust and expanding national vehicle fleet, which the U.S. Department of Transportation estimates at over 280 million registered vehicles, creating a consistent base demand for engine lubrication products. Accelerating consumer preference for fully synthetic oils, which offer superior engine protection and longer drain intervals, coupled with increasingly stringent emissions standards mandated by the U.S. Environmental Protection Agency (EPA), is compelling both original equipment manufacturers (OEMs) and aftermarket suppliers to reformulate and innovate.

Key Industry Highlights:

- Leading Region: The Midwest U.S. leads with approximately 28% revenue share, driven by its automotive manufacturing heritage, major freight corridors along I-80 and I-90, and extreme climate conditions demanding premium full-synthetic lubricants year-round.

- Fastest Growing Region: The West U.S., driven by California's stringent CARB emission mandates, high ride-sharing fleet activity, and growing hybrid vehicle penetration, is the fastest growing regional market for advanced synthetic automotive engine oils.

- Dominant Segment: Fully synthetic engine oils command approximately 45% Oil Type category share, propelled by OEM mandates for turbocharged engines, ILSAC GF-6 compliance requirements, and consumer preference for extended drain intervals up to 15,000 miles.

- Fastest Growing Segment: Commercial vehicles is the fast-growing segment, fueled by expanding U.S. freight volumes, API CK-4 specification mandates, and sustained ICE dominance in Class 6–8 heavy-duty trucking through at least 2035.

- Key Opportunity: Fully synthetic oil upgrades targeting turbocharged GDI and diesel platforms, aligned with upcoming API GF-7 specifications expected by 2027, offer high-margin co-development partnerships for leading lubricant manufacturers and OEM suppliers.

DRO Analysis

Drivers

Expanding U.S. Vehicle Fleet and Rising Maintenance Awareness

The United States maintains one of the world's largest per-capita vehicle populations, with the U.S. Department of Transportation reporting approximately 283 million registered motor vehicles. Each vehicle requires periodic engine oil changes, typically every 3,000 to 10,000 miles, depending on oil type and engine specifications, generating a recurring and largely recession-resilient demand cycle. According to the Auto Care Association, the U.S. automotive aftermarket generated over US$ 490 billion in total economic output, encompassing products such as engine lubricants.

Growing consumer awareness regarding preventive vehicle maintenance, driven by OEM recommendations and dealer service campaigns, continues to support stable volumes. The proliferation of quick-lube service chains across suburban and rural markets has further normalized regular oil change intervals, sustaining consistent demand for engine oils across all vehicle categories and reinforcing the market's structural resilience through the forecast horizon.

Stringent Emission Standards and OEM Specification Upgrades

Regulatory mandates from the U.S. Environmental Protection Agency (EPA) and the California Air Resources Board (CARB) are continuously tightening tailpipe emission ceilings, compelling automakers to adopt low-viscosity, high-performance engine oils that reduce friction and improve fuel economy. The American Petroleum Institute (API), in collaboration with the International Lubricants Standardization and Approval Committee (ILSAC), introduced the API SP / ILSAC GF-6 specification in 2020 to address evolving emission and fuel economy requirements across the U.S. vehicle fleet.

According to the U.S. Department of Energy (DOE), widespread adoption of lower-viscosity grades such as 0W-20 and 0W-16 can improve fuel efficiency by 0.5% to 3% compared to higher-viscosity alternatives. These regulatory tailwinds are directly driving the shift toward premium synthetic formulations, sustaining market momentum throughout the 2026–2033 forecast period.

Restraints

Accelerating Adoption of Battery Electric Vehicles (BEVs)

The growing penetration of battery electric vehicles represents a significant structural headwind for the automotive engine oils market. Unlike internal combustion engine (ICE) vehicles, BEVs do not require conventional engine oil, eliminating a key recurring revenue stream for lubricant manufacturers. The U.S. Energy Information Administration (EIA) reports that plug-in electric vehicle sales in the U.S. surpassed 1.4 million units in 2023, accounting for roughly 7.6% of new vehicle sales.

The target of 50% EV share in new vehicle sales by 2030, reinforced by the Inflation Reduction Act's EV tax credits, signals a medium-to-long-term decline in ICE vehicle penetration. This structural transition, while gradual, is expected to compress the total addressable market for traditional engine lubricants, particularly in the passenger car segment, over the projection horizon through 2033.

Crude Oil Price Volatility and Raw Material Cost Pressures

Base oils derived from crude oil refining constitute the primary feedstock for most engine oil formulations, making the market inherently sensitive to fluctuations in global crude oil prices. The U.S. Energy Information Administration (EIA) has documented significant crude price swings. West Texas Intermediate (WTI) crude oscillated between approximately US$ 70 and US$ 95 per barrel during 2023-2024, translating directly into margin pressures for lubricant blenders and formulators.

Additives such as antiwear agents, viscosity index improvers, and detergents, sourced from petrochemical supply chains, also experience cost inflation during periods of crude price elevation. Smaller independent blenders with limited pricing power face acute vulnerability, potentially constraining short-term volume growth as end-users defer non-critical maintenance during periods of broader economic stress.

Opportunities

Surging Demand for Fully Synthetic Engine Oils in Premium and Performance Segments

Fully synthetic engine oils present the most significant and rapidly expanding opportunity within the U.S. engine oil landscape. Consumer preference is decisively shifting toward synthetic formulations owing to their superior thermal stability, extended drain intervals of up to 15,000 miles or beyond, and measurable fuel economy benefits, attributes increasingly aligned with both regulatory mandates and consumer sustainability priorities. The American Chemistry Council’s study indicates that synthetic lubricants account for a growing and increasing share of the overall U.S. lubricants market by volume.

The proliferation of turbocharged GDI (Gasoline Direct Injection) engines in mainstream passenger vehicles, which operate at higher temperatures and pressures, necessitates synthetic lubrication even in mid-range vehicles, broadening the addressable consumer base. This segment offers premium pricing and higher margins, making it a strategic priority for market participants targeting profitable growth.

Growth in Heavy-Duty Commercial Vehicle Fleet and Fleet Electrification Delay

The commercial vehicle segment, encompassing Class 6–8 heavy-duty trucks, represents a high-value growth opportunity for engine oil manufacturers. According to the American Trucking Associations (ATA), the U.S. trucking industry operates approximately 3.5 million heavy-duty trucks, each requiring specialized, high-performance diesel engine oils meeting API CK-4 and FA-4 specifications.

The electrification of heavy commercial vehicles remains significantly behind the passenger car segment due to range limitations, payload constraints, and infrastructure gaps, ensuring continued ICE dominance and consequently sustained engine oil demand in this segment through at least 2035, according to projections from the U.S. Department of Transportation. Fleet operators prioritize extended drain interval oils to minimize downtime, creating consistent and high-margin demand for premium commercial lubricant formulations, providing a durable revenue opportunity across the 2026–2033 forecast horizon.

Category-wise Analysis

Oil Type Insights

Fully synthetic engine oils account for the largest share of the U.S. Automotive Engine Oils market, commanding an estimated 45% of total market revenue. This dominance is primarily attributable to widespread OEM mandates for synthetic lubricants across major automakers, including General Motors, Ford, and Toyota, which specify fully synthetic grades in their latest turbocharged and high-output engine designs.

The Auto Care Association observes that fully synthetic oil usage has grown substantially in the do-it-yourself (DIY) segment, driven by consumer awareness about engine longevity. Extended drain intervals, up to 10,000–15,000 miles for synthetics versus 3,000–5,000 miles for mineral oils, offer compelling value propositions despite higher upfront costs, cementing synthetic dominance in both OEM and aftermarket distribution channels.

Vehicle Type Insights

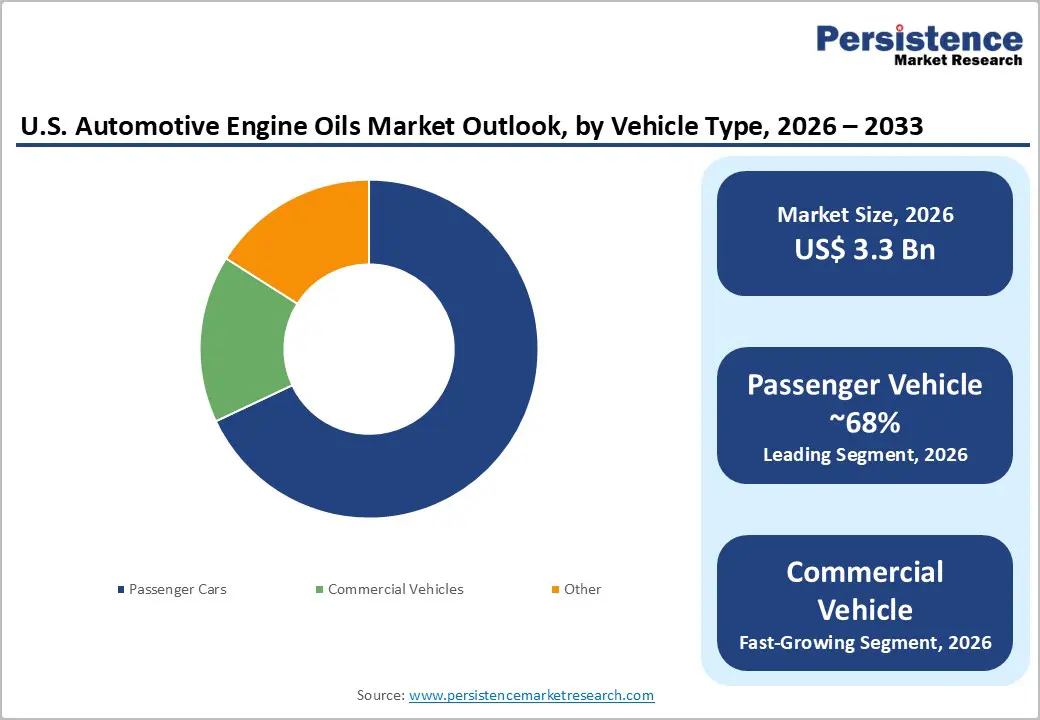

Passenger cars represent the dominant vehicle type segment in the U.S. Automotive Engine Oils market, accounting for approximately 68% of total market share. The United States Census Bureau estimates that nearly 91% of American households own at least one vehicle, and most of the registered vehicle fleet comprises light-duty passenger cars and SUVs.

The sheer volume of the U.S. passenger vehicle parc, exceeding 230 million units within the light-duty category, sustains consistent and recurring demand for engine lubrication products across both OEM and aftermarket channels. Rising average vehicle age, which S&P Global Mobility data places at approximately 12.6 years for U.S. light vehicles, further amplifies oil change frequency and aftermarket oil consumption, reinforcing the passenger car segment's undisputed market leadership position through the forecast period.

Engine Type Insights

Gasoline engines constitute the leading engine type segment in the U.S. Automotive Engine Oils market, with an estimated 62% market share. This dominance reflects the broader composition of the U.S. vehicle fleet, which is predominantly gasoline-powered across both passenger and light commercial categories. According to the U.S. Department of Energy's Alternative Fuels Data Center, gasoline vehicles account for approximately 80% of the total U.S. vehicle registrations.

The diesel engine segment, while smaller in unit count, commands a premium in oil specification requirements and holds a significant share within the heavy-duty commercial vehicle sub-segment, where CARB-compliant and API CK-4 rated products are widely specified.

Regional Analysis

Midwest U.S. Market Trends & Analysis

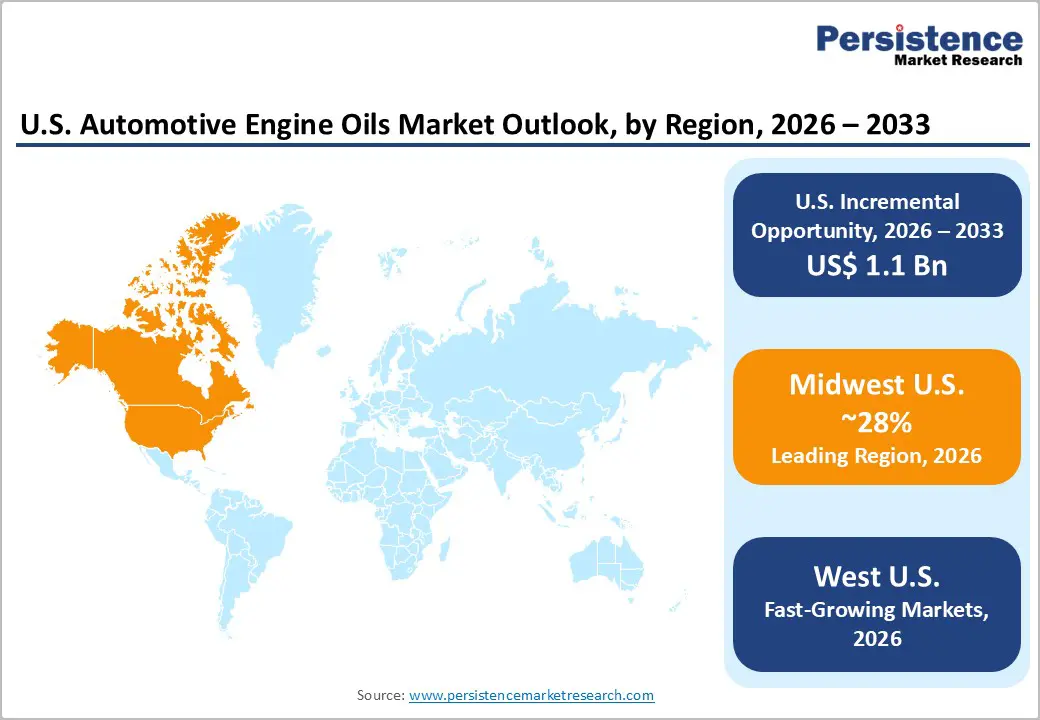

The Midwest U.S. commands the leading position in the U.S. Automotive Engine Oils market, accounting for approximately 28% of total market revenue. The region's dominance is underpinned by its dense industrial base, significant commercial trucking activity along major freight corridors including Interstate 80 and Interstate 90, and a large, registered vehicle population across states such as Ohio, Michigan, Illinois, and Indiana.

Michigan serves as the epicenter of U.S. automotive manufacturing, housing the headquarters of the "Detroit Three", General Motors, Ford Motor Company, and Stellantis, along with a vast supplier ecosystem that drives disproportionate fleet maintenance activity. Extreme temperature variations, from harsh winters to hot summers, necessitate premium full-synthetic lubricants capable of maintaining viscosity across a wide thermal range.

The region's exposure to recent U.S. tariffs on imported goods has indirectly reinforced local procurement of lubricants, benefiting regional blenders and distributors and strengthening domestic supply chain resilience across the lubricant value chain.

West U.S. Market Trends, Drivers, & Insights

The West U.S. region, led by California, is the fastest-growing market for automotive engine oils, driven by a confluence of regulatory, demographic, and technological factors. California, under the authority of the California Air Resources Board (CARB), enforces the most stringent vehicle emission standards in the nation, compelling automakers and end-users to adopt advanced, low-viscosity synthetic lubricants that contribute to improved fuel economy and reduced tailpipe emissions.

The state's Low Carbon Fuel Standard (LCFS) and ongoing Advanced Clean Cars II regulations are accelerating the specification of environmentally compatible engine oils. California's high population density, extensive commuter vehicle usage, and the proliferation of ride-sharing operations, including Lyft and Uber fleets, generate above-average oil change frequencies. Nevada, Arizona, and Washington are also experiencing rapid population and vehicle fleet growth, further amplifying regional demand for premium synthetic engine lubricants through the forecast period.

Southeast U.S. Market Drivers & Analysis

The Southeast U.S. represents the second largest regional market for automotive engine oils, with 23% market share, characterized by a large and rapidly growing vehicle fleet, high per-capita vehicle miles traveled (VMT), and an expanding logistics and commercial trucking sector. States such as Texas, Florida, Georgia, and North Carolina are experiencing significant population inflows driven by domestic migration trends, directly expanding the registered vehicle base.

According to the Federal Highway Administration (FHWA), southeastern states consistently rank among the highest in total vehicle miles traveled nationally. Recent U.S. tariffs on Chinese goods impacting supply chain costs have prompted several Southeast-based fleet operators to explore domestic lubricant sourcing, creating near-term opportunities for regional blenders and distributors.

Competitive Landscape

The U.S. Automotive Engine Oils market exhibits a moderately consolidated competitive structure, with the top five players, ExxonMobil, Shell, Chevron, Castrol, and Valvoline, collectively holding a substantial portion of total market revenue. These incumbents leverage decades of brand equity, extensive distribution networks, and deep OEM partnerships to maintain competitive moats.

Mergers, acquisitions, and joint ventures are prominent across the landscape, with Valvoline's strategic repositioning toward service retail serving as a notable example. Emerging players and private-label brands are gaining traction in the value segment via e-commerce channels, intensifying price competition while spurring innovation at the premium end of the market.

Key Developments:

- March 2026: Shell plc announced an agreement to sell Jiffy Lube International and its subsidiary Premium Velocity Auto to Monomoy Capital Partners for approximately $1.3 billion, marking a strategic divestment in the automotive engine oil and lubricants ecosystem.

- January 2026: Phillips 66 Lubricants announced its return as a sponsor of Honda Racing Corporation USA (HRC US) for the 2026 IMSA WeatherTech SportsCar Championship, marking the second consecutive year of collaboration.

- March 2026: Valvoline Global Operations announced the launch of its next-generation passenger car motor oil formulations aligned with the new ILSAC GF-7 standard, marking a significant advancement in engine oil technology.

Top Companies in the U.S. Automotive Engine Oils Market

ExxonMobil Corporation (Irving, U.S.) is the market leader in U.S. automotive engine oils, anchored by its iconic Mobil 1 brand, among the most recognized and widely specified synthetic engine oil brands globally. The company benefits from extensive OEM approval agreements and a broad product portfolio spanning conventional, synthetic-blend, and fully synthetic formulations across all API and ILSAC performance categories, enabling comprehensive coverage across consumer and commercial fleet segments.

Shell plc (London, U.K.)’s Pennzoil and Shell Helix brands command significant U.S. market presence across retail, dealer, and quick-lube channels. Shell's proprietary PurePlus Technology, producing synthetic base oil from natural gas, differentiates it in the premium synthetic segment. Extensive distribution agreements with major quick-lube chains amplify Shell's nationwide retail footprint, supporting consistent volume generation and strong brand visibility across consumer-facing channels.

Valvoline Inc. (Lexington, U.S.) operates as both a lubricant manufacturer and a retail service provider through its Valvoline Instant Oil Change (VIOC) network. This vertically integrated model, spanning product development, blending, and consumer-facing service delivery, creates strong brand loyalty and repeat purchase behavior, positioning Valvoline uniquely among its peers in capturing aftermarket consumer spend in the evolving U.S. engine oil landscape.

Companies Covered in U.S. Automotive Engine Oils Market

- ExxonMobil Corporation

- Shell plc

- Chevron Corporation

- Castrol Limited

- TotalEnergies SE

- AMSOIL INC.

- Valvoline Inc.

- Phillips 66 Lubricants

- Lucas Oil Products, Inc.

- Fuchs SE

Frequently Asked Questions

The U.S. Automotive Engine Oils market is valued at approximately US$ 3.4 billion in 2026 and is projected to reach US$ 4.4 billion by 2033, expanding at a CAGR of 4.3% during the 2026–2033 forecast period, driven by fleet expansion, OEM specification upgrades, and rising synthetic oil penetration.

The primary demand drivers include the expansive U.S. vehicle fleet of over 280 million registered vehicles, rising consumer preference for fully synthetic oils, API SP / ILSAC GF-6 OEM specification mandates, and regulatory emission mandates from the EPA and CARB compelling adoption of advanced, low-viscosity engine oil formulations across passenger and commercial vehicle segments.

Fully synthetic engine oils represent the dominant Oil Type segment, accounting for approximately 45% of total market revenue, driven by widespread OEM mandates for turbocharged engine platforms, ILSAC GF-6 compliance requirements, and growing consumer awareness about long-term engine protection and extended drain interval benefits of synthetic lubrication.

The Midwest U.S. holds the leading regional position with an estimated 28% revenue share, supported by its automotive manufacturing heritage anchored by General Motors, Ford, and Stellantis, extensive commercial freight activity along I-80 and I-90, and severe climatic conditions necessitating high-performance synthetic lubricant adoption throughout the year.

Significant growth opportunities exist in the fully synthetic segment, driven by turbocharged GDI engine proliferation and upcoming API GF-7 specifications expected by 2027, and in the heavy-duty commercial vehicle segment, where sustained ICE dominance through at least 2035 ensures durable demand for premium API CK-4 and FA-4 rated lubricants across the 3.5 million-strong U.S. heavy truck fleet.