- Inks, Coatings, Adhesives & Sealants (ICAS)

- Adhesive Films Market

Adhesive Films Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Adhesive Films Market by Resin Type (Acrylic, Rubber, Silicone, Epoxy, Polyurethane, Others), Film Material (Polypropylene, Polyvinyl Chloride, Polyethylene, Polyester, Others), Application (Packaging, Automotive, Electronics, Medical, Construction, Graphics & Signage, Others), by Regional Analysis, 2025 - 2032

Adhesive Films Market Size and Trend Analysis

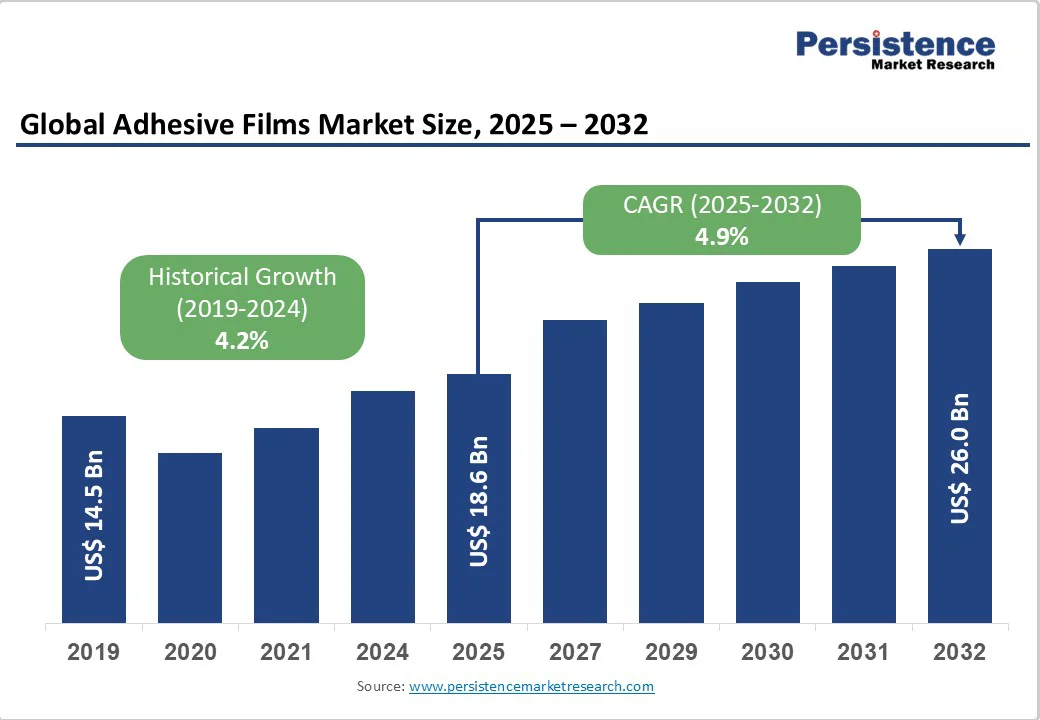

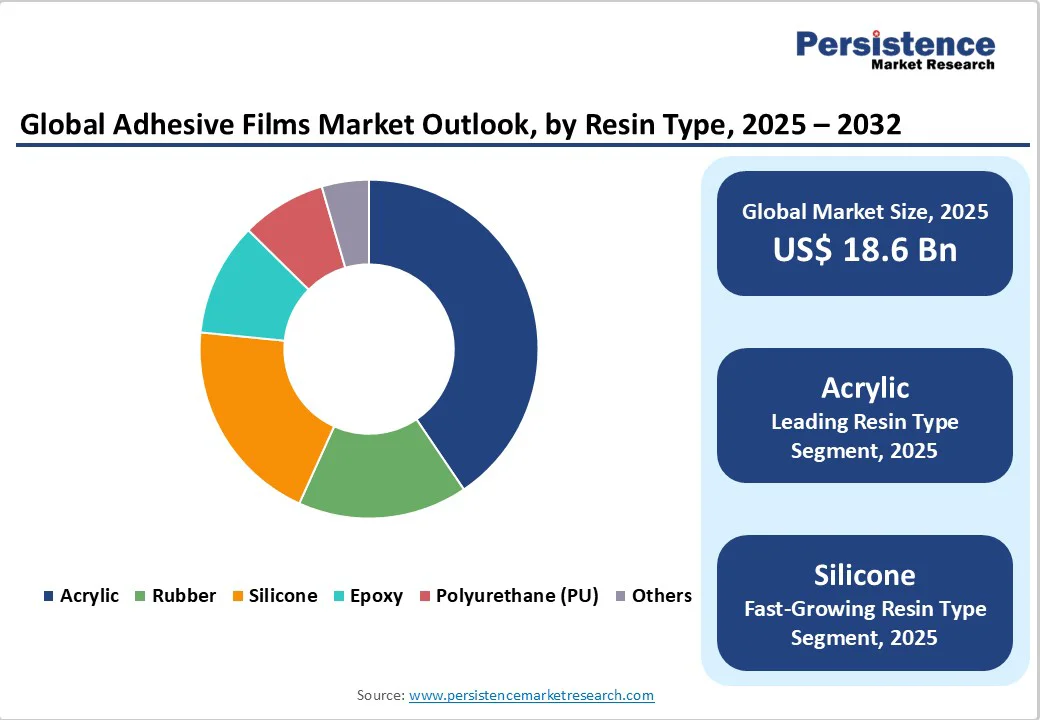

The global adhesive films market size is likely to be valued at US$18.6 billion in 2025 and is projected to reach US$26.0 billion by 2032, growing at a CAGR of 4.9% between 2025 and 2032.

Rising demand from the packaging and automotive sectors and innovation in high-performance polyurethane and silicone films drive expansion. Additionally, stringent environmental regulations are prompting a shift toward recyclable polyester films, underpinning steady adoption across applications.

Growth in e-mobility and medical device assembly further accentuates uptake, supported by advancements in low-outgassing acrylic formulations.

Key Market Highlights:

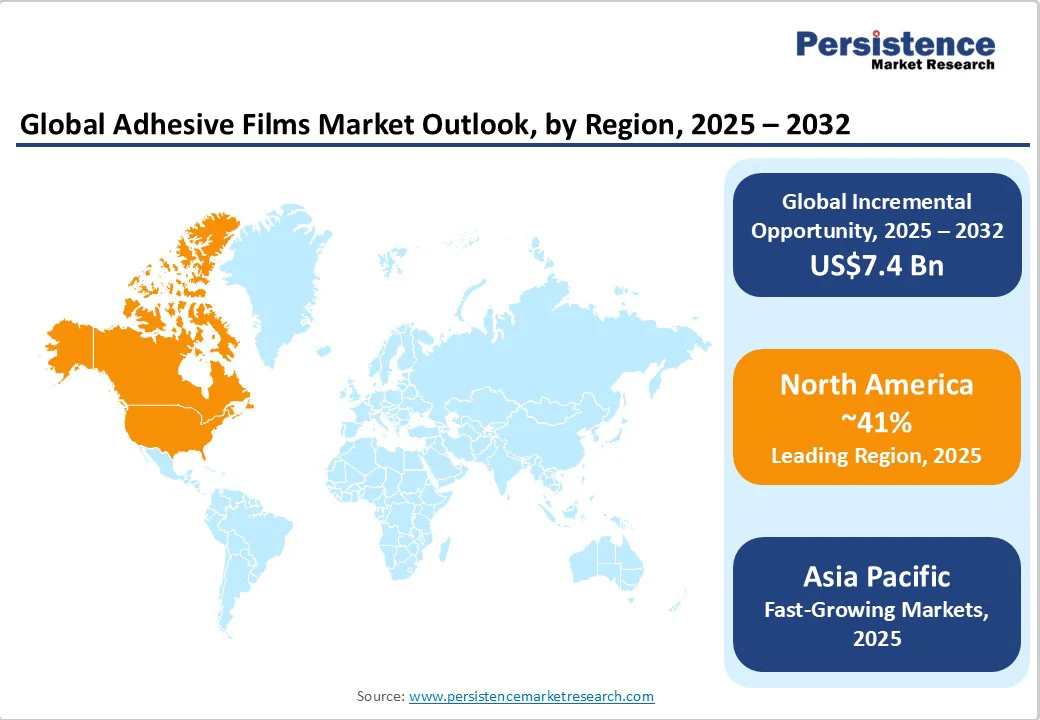

- Leading Region: North America retains leadership in adhesive films, driven by medical device approvals and EV incentives that boost film adoption across automotive and healthcare sectors.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, with China, Japan, and India expanding electronics and packaging capacity, underpinned by government industrial initiatives.

- Leading Resin Type Segment: Acrylic resin films dominate globally, commanding a significant share due to versatile adhesion performance in electronics and medical applications.

- Fastest-Growing Film Material Segment: Recyclable polyester films are the fastest-growing segment, driven by sustainability mandates and a shift towards eco-friendly packaging solutions.

- Key Market Opportunity: Smart packaging integration offers a major growth opportunity, leveraging conductive films for RFID and sensor embedding in pharmaceuticals and food safety applications.

| Key Insights | Details |

|---|---|

| Adhesive Films Market Size (2025E) | US$ 18.6 billion |

| Market Value Forecast (2032F) | US$26.0 billion |

| Projected Growth CAGR (2025 - 2032) | 4.9% |

| Historical Market Growth (2019-2024) | 4.2% |

Market Dynamics

Driver - Rising Adoption of E-Mobility Components Driving High-Performance Adhesive Film Demand

The accelerating adoption of electric vehicles (EVs) is driving demand for advanced adhesive films, especially polyurethane and silicone-based types. These films provide essential properties, such as superior thermal stability, vibration damping, and electrical insulation, which are crucial for securing battery modules, motor assemblies, and electronic circuits.

According to the International Energy Agency, global EV sales rose by around 40% in 2024, creating a direct boost in adhesive film consumption for glazing, wiring, and interior component attachment. Strategic collaborations between automakers and adhesive manufacturers are further advancing high-performance, heat-resistant materials that meet evolving safety and efficiency standards in e-mobility applications.

Sustainability Mandates Accelerating Shift Toward Recyclable and Eco-Friendly Adhesive Films

Rising sustainability mandates are reshaping packaging material choices, encouraging the use of recyclable polyester and polyethylene adhesive films. These films enable lightweight, durable, and eco-friendly packaging solutions that comply with tightening environmental regulations across Europe and North America.

The Ellen MacArthur Foundation projects that more than 60% of plastic packaging could become reusable or recyclable by 2025, spurring adhesive film makers to innovate thinner, high-strength variants. With growing emphasis on circular economy goals, adhesive film suppliers are focusing on reducing plastic waste and developing bio-based formulations to align with global sustainability objectives.

Restraint - Volatile Raw Material Prices Impacting Production Stability

Fluctuations in petroleum-derived resin costs, including polypropylene and polyurethane feedstocks, continue to exert significant margin pressure on adhesive film manufacturers. The U.S. Energy Information Administration reported a 15% increase in crude oil prices in 2024, which directly elevated polymer resin and solvent costs. This cost instability makes product pricing less predictable, discouraging bulk purchasing among price-sensitive end-users, particularly in the packaging sector.

Such volatility disrupts supply chain planning and erodes profitability, forcing manufacturers to either absorb rising input costs or pass them on to consumers. Consequently, the unpredictability of raw material prices remains a major restraint on consistent production and sustainable growth within the adhesive films market.

Stringent Regulatory Compliance Hindering Market Expansion

Tightening global chemical safety and emissions regulations are creating barriers for adhesive film producers, particularly in regions governed by the European Union’s REACH framework. These policies require extensive product testing, documentation, and registration for resin formulations used in silicone and epoxy-based films.

According to the European Chemicals Agency, compliance costs have risen by nearly 20% over the past two years, significantly impacting smaller and mid-sized manufacturers. The added financial and administrative burden slows innovation cycles, delays new product launches, and limits companies' ability to expand into regulated markets. As a result, stringent compliance norms act as a key restraint on market expansion and competitiveness.

Opportunity - Rising Demand for Adhesive Films in Medical Device Assembly

The growing preference for disposable, adhesive-based components in the medical sector is unlocking significant opportunities for adhesive film manufacturers. These films are increasingly used in wound dressings, catheter linings, and diagnostic device assembly due to their sterility, flexibility, and ease of application. Silicone and acrylic adhesive films with proven biocompatibility are projected to witness demand growth exceeding 6% CAGR through 2032.

Recent FDA approvals for innovative film-based surgical tapes highlight the market’s shift toward products that combine strong adhesion with gentle removal from sensitive skin. This trend is creating a lucrative niche for manufacturers developing high-performance, medical-grade adhesive films that meet stringent safety and patient comfort standards.

Integration of Smart Packaging Technologies Creating High-Value Opportunities

Smart packaging technologies are emerging as a dynamic growth avenue for adhesive film producers, particularly in the pharmaceutical and food safety sectors. Advanced conductive polyester films are enabling RFID and sensor integration without compromising barrier integrity or durability. These innovations support temperature tracking, authenticity verification, and freshness monitoring across supply chains.

According to a 2025 study by the Institute of Packaging Professionals, global smart packaging adoption is expected to expand by nearly 25% annually. This trend is driving demand for functional adhesive films engineered for electronic connectivity, data transmission, and real-time traceability, positioning them as key enablers of next-generation intelligent packaging solutions.

Category-wise Insights

Resin Type Analysis

Acrylic-based adhesive films dominate the global market owing to their strong adhesion, UV resistance, and excellent compatibility with various substrates such as glass, metal, and plastic. Their consistent performance under fluctuating temperatures and superior peel strength make them indispensable in electronics, medical, and automotive applications. These films ensure long-term stability and durability, making acrylic the preferred resin type across diverse industrial uses.

Silicone-based films are emerging as the fastest-growing category due to their superior heat resistance, flexibility, and biocompatibility. They are increasingly used in electric vehicle battery insulation, electronic components, and medical device assembly, where performance under extreme conditions is crucial. Their expansion is further supported by the growing demand for high-performance materials in critical and high-value applications.

Film Material Analysis

Polyester (PET) films hold the leading position among film materials thanks to their exceptional tensile strength, dimensional stability, and recyclability. Their clarity and ability to maintain mechanical integrity under stress make them the top choice for packaging, labeling, and industrial lamination. PET films also enable thinner material usage without compromising strength, offering cost-efficient and sustainable performance advantages.

On the other hand, polyethylene (PE) films are witnessing rapid growth as industries shift toward lightweight, recyclable packaging materials. Known for their moisture resistance and flexibility, PE films are widely used in food, hygiene, and protective packaging. Advances in coextrusion and recyclable multilayer technology are driving their rising adoption within sustainable and circular packaging systems.

Application Analysis

Packaging remains the dominant application segment, accounting for the largest share of global adhesive film consumption. The surge in e-commerce and demand for tamper-evident, eco-friendly packaging solutions continues to propel their usage. Adhesive films enhance sealing, labeling, and protection capabilities, supporting the transition toward lightweight and sustainable packaging across industries.

Electronics applications represent the fastest-growing segment, driven by the proliferation of electric vehicles, smartphones, and wearable devices. Adhesive films play a vital role in component bonding, insulation, and protection, ensuring reliability under heat and mechanical stress. As device miniaturization and performance demands increase, adhesive films are becoming essential for next-generation electronic assemblies.

Regional Insights

North America Adhesive Films Trends

North America retains a dominant position in the adhesive films market, supported by strong automotive and medical device industries. U.S. manufacturers are increasingly adopting silicone-based adhesive films for electric vehicle battery insulation, supported by policy incentives under the Inflation Reduction Act that promote domestic EV production. The FDA’s accelerated review pathways for medical adhesives have also spurred innovation and faster commercialization of advanced film technologies.

In Canada, sustainability initiatives are reshaping packaging practices. Provincial regulations restricting single-use plastics have driven a 7% annual increase in the adoption of recyclable film. The region’s shift toward eco-friendly materials reflects broader sustainability commitments across packaging, healthcare, and mobility sectors, ensuring steady demand for advanced adhesive film solutions.

Europe Adhesive Films Trends

Europe’s adhesive films market is strengthened by cohesive regulations such as REACH and the EU Single-Use Plastics Directive. Germany and France are leading adopters of epoxy-based films for automotive lightweighting, supported by national incentives for CO2 reduction and sustainable mobility. These trends are promoting innovation in high-performance, low-emission adhesive technologies.

The U.K. and Spain are emerging as growth nodes in the region. The U.K. has recorded a 10% increase in demand for PET film for signage and graphics, driven by urban redevelopment and retail expansion. Spain’s growing silicone film extrusion industry, supported by the Mediterranean manufacturing cluster, is reinforcing Europe’s industrial self-sufficiency in specialty adhesive film production.

Asia Pacific Adhesive Films Trends

Asia Pacific represents the fastest-growing regional market, led by robust industrialization in China, Japan, and India. China’s thriving electronics manufacturing ecosystem has boosted demand for polyester-based adhesive films, with annual growth of 12% across device assembly and circuit protection. Japan’s automotive manufacturers are incorporating epoxy adhesive films to improve bonding in lightweight composite structures.

In India, the adhesive films sector is accelerating due to expanding packaging and consumer goods industries. Government-backed “Make in India” initiatives are spurring local film production and innovation, particularly in flexible and recyclable formats. Rising domestic consumption and manufacturing capacity continue to position the Asia Pacific as the global hub for adhesive film development and export.

Competitive Landscape

The adhesive films market is moderately consolidated, with a few leading players holding a significant global presence. These companies are heavily investing in R&D to develop advanced, sustainable, and high-performance adhesive films that cater to evolving industry needs. Strategic collaborations with automotive and electronics manufacturers are driving innovation in lightweight and high-temperature-resistant film technologies.

Emerging participants are carving out space in specialized areas such as smart packaging and medical-grade films. Their agility and focus on tailored solutions enable them to address niche market demands quickly. Regional production expansion, especially across Asia Pacific, remains central to maintaining competitiveness and supply chain resilience.

Key Market Developments:

- In March 2025, Avery Dennison Corporation developed an eco-friendly polyester film designed for recyclable packaging applications. The film combines high strength and durability with sustainability, addressing growing regulatory and consumer demand for environmentally responsible packaging solutions across industries, supporting the circular economy, and enhancing brand appeal.

- In November 2024, 3M Company launched a high-temperature silicone adhesive film specifically for electric vehicle battery modules. The product provides superior thermal stability, electrical insulation, and long-term reliability under extreme conditions. This innovation supports the expanding e-mobility sector, enabling safer and more efficient EV battery assembly.

- In July 2024, Henkel AG & Co. KGaA inaugurated a new polyurethane (PU) film production line in the Asia Pacific region to meet rising demand. The facility boosts local manufacturing capacity, ensures timely supply for automotive, electronics, and packaging applications, and strengthens Henkel’s regional market presence.

Companies Covered in Adhesive Films Market

- Henkel AG & Co. KGaA

- 3M Company

- Avery Dennison Corporation

- H.B. Fuller Company

- Arkema Group

- Sika AG

- RPM International Inc.

- LINTEC Corporation

- Huntsman Corporation

- Illinois Tool Works Inc.

- Wacker Chemie AG

- UPM-Kymmene Oyj

- Toray Industries, Inc.

- Eastman Chemical Company

- Magnum Tapes & Films

- Bostik SA

- Nitto Denko Corporation

Frequently Asked Questions

The market was US$ 18.6 billion in 2025 and is expected to reach US$ 26.0 billion by 2032 at a 4.9% CAGR.

The growth of electric vehicles, which require thermally stable silicone and polyurethane films for battery insulation and component bonding, is a key demand driver.

Acrylic-based films lead with around 36% share due to superior adhesion, UV resistance, and excellent peel strength across electronics and medical applications.

North America leads, supported by the U.S. medical device industry’s rapid approvals and government incentives for EV production boosting silicone film usage.

Smart packaging integration using conductive polyester films for RFID and sensor embedding in pharmaceuticals and food safety represents a significant opportunity.

Major companies include Henkel AG & Co. KGaA, 3M Company, Avery Dennison Corporation, H.B. Fuller Company, and Sika AG.