- Inks, Coatings, Adhesives & Sealants (ICAS)

- Anaerobic Adhesives Market

Anaerobic Adhesives Market Size, Share, and Growth Forecast 2026 - 2033

Anaerobic Adhesives Market by Product Type (Thread lockers, Retaining Compounds, Gasketing Sealants, Thread Sealants, Other), Chemistry (Acrylic, Methacrylate, Silicone-Modified, Butyl & Other), End-use Industry (Automotive, Industrial Machinery, Electrical & Electronics, Aerospace & Defense, Construction, Other), and Regional Analysis for 2026 - 2033

Anaerobic Adhesives Market Size and Trend Analysis

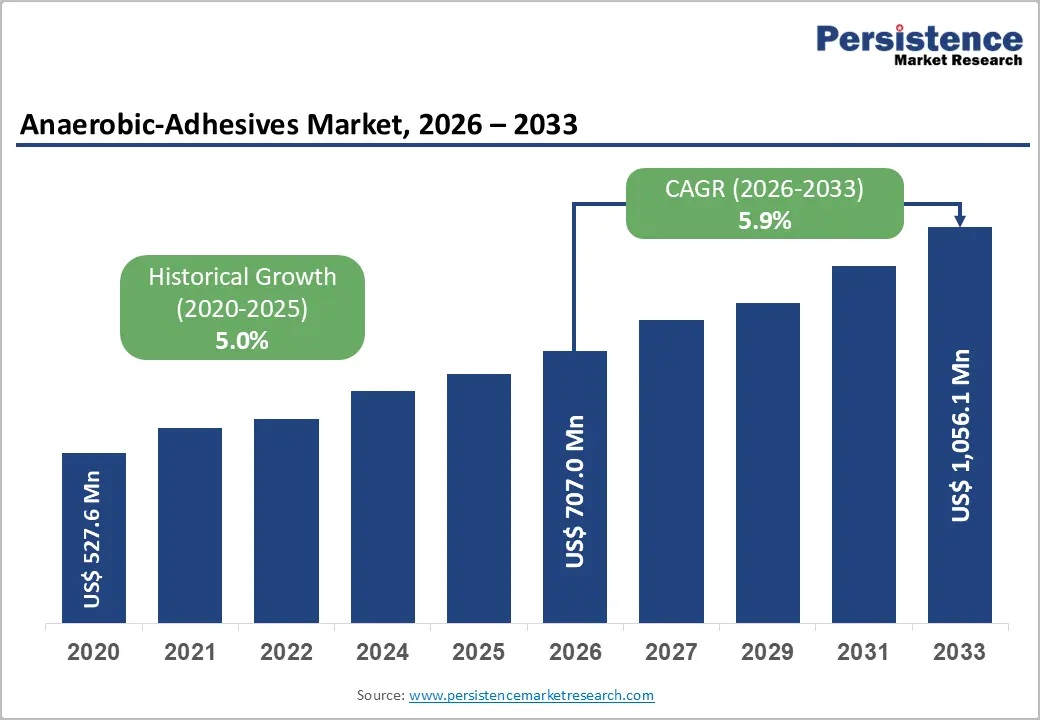

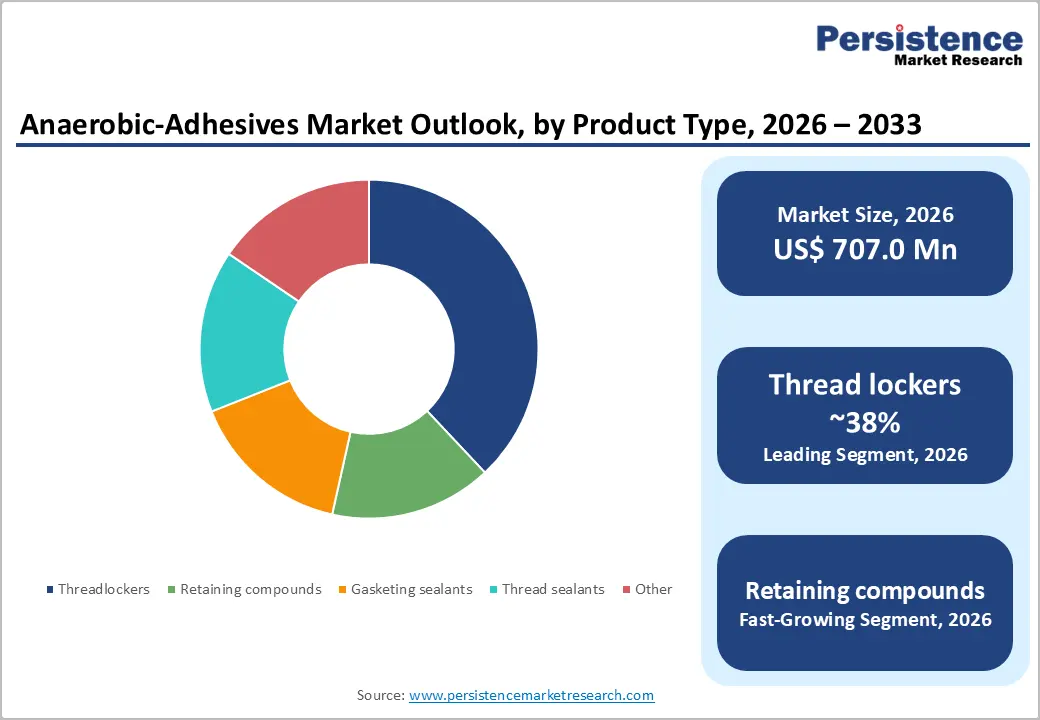

The global anaerobic adhesives market is valued at US$ 707.0 million in 2026 and is projected to reach US$ 1,056.1 million by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

The market is primarily propelled by surging automotive production, growing demand for vibration-resistant fastener locking solutions, and expanding applications in aerospace, electronics, and industrial machinery MRO.

The World Bank reports that global manufacturing value exceeded US$ 16 trillion in 2022, underlining the sheer scale of industrial activity that generates recurring demand for anaerobic adhesives. In the automotive sector, the International Organization of Motor Vehicle Manufacturers (OICA), an intergovernmental reference body, confirmed global vehicle production exceeded 93 million units in 2023, including rapidly scaling electric vehicle output.

Key Industry Highlights:

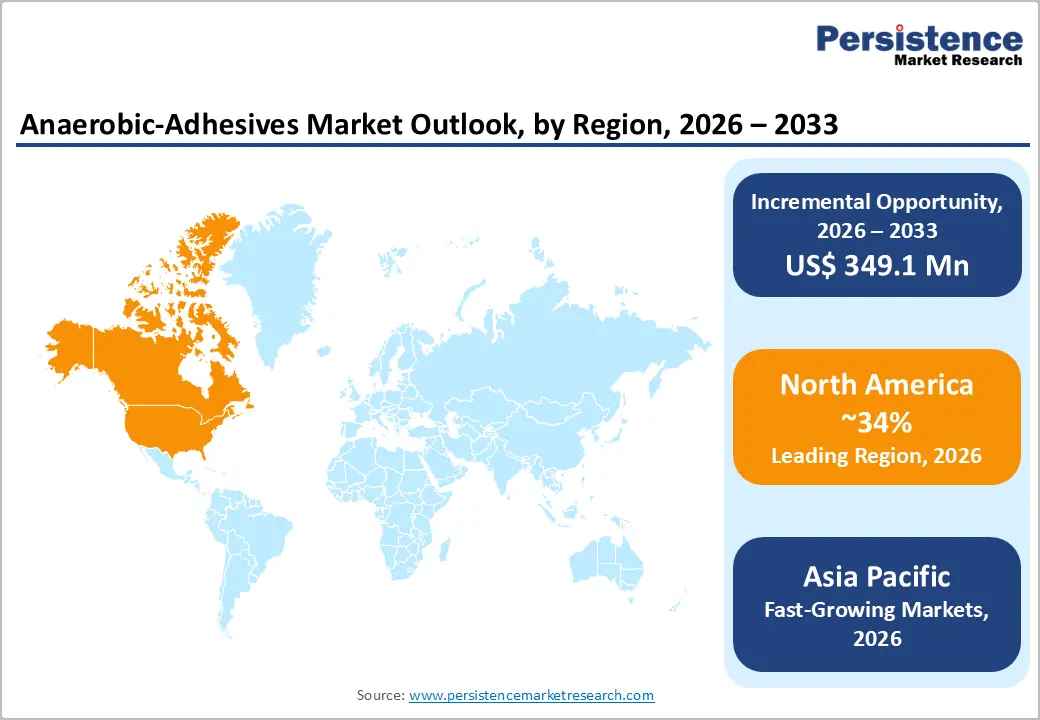

- Leading Region: North America dominates the global anaerobic adhesives market, with 34% of the global market, underpinned by robust automotive manufacturing, aerospace procurement, and industrial MRO demand, particularly in the United States.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market for anaerobic adhesives, driven by rapid industrialization, expanding automotive OEM activity, and booming electronics manufacturing in China, India, and Japan.

- Dominant Segment: Thread lockers lead the product type category with approximately 38% market share, driven by widespread adoption in automotive, aerospace, and industrial machinery assembly applications for vibration-resistant bolt locking.

- Fastest Growing Segment: Acrylic chemistry remains the fastest-adopted platform, favored for broad temperature tolerance, substrate compatibility, and mechanical performance in global OEM assembly.

- Key Market Opportunity: The expanding global aerospace and defense sector, with military expenditure surpassing US$ 2.2 trillion in 2023 per SIPRI, represents a high-value opportunity for manufacturers of specification-compliant, high-performance anaerobic adhesive formulations.

DRO Analysis

Drivers - Surging Automotive Production and Electric Vehicle Assembly Demand

The automotive industry stands as one of the most significant demand pillars for anaerobic adhesives, particularly for thread lockers and retaining compounds used in engine, transmission, and brake systems. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production exceeded 93 million units in 2023, with electric vehicle (EV) output expanding at a double-digit annual pace. Anaerobic adhesives are integral to EV drivetrain assemblies, where vibration resistance and torque retention are essential to operational safety and reliability.

As original equipment manufacturers (OEMs) increasingly substitute mechanical fasteners with adhesive bonding to reduce component weight and enhance fuel or range efficiency, demand for high-performance anaerobic formulations continues its upward trajectory. The shift toward electric mobility adds further momentum, given the precision bonding requirements of compact EV powertrain architectures.

Growth in Industrial Machinery and MRO Sector Applications

Industrial machinery maintenance, repair, and overhaul (MRO) represents a substantial and recurring demand base for anaerobic adhesives. The global manufacturing sector's ongoing expansion, especially across the Asia Pacific and North America, continues to drive consumption of retaining compounds, gasketing sealants, and thread sealants in pumps, gearboxes, valves, and hydraulic equipment. The International Federation of Robotics (IFR) reported that global robot installations reached approximately 541,000 units in 2022, highlighting the accelerating pace of factory automation.

Automated assembly lines demand adhesives with consistent cure profiles, reliable gap-filling, and chemical resistance. The growing preference for single-component, solvent-free anaerobic adhesive systems aligns well with tightening VOC emission regulations and occupational health standards enforced in major industrial economies, further supporting their adoption.

Restraints - Health and Safety Concerns Related to Methacrylate-Based Formulations

Anaerobic adhesives, particularly those based on methacrylate chemistry, contain reactive monomers that pose inhalation and dermal sensitization risks during routine handling and application. Regulatory bodies such as the European Chemicals Agency (ECHA) under the REACH framework and the U.S. Occupational Safety and Health Administration (OSHA) impose stringent labeling, handling, and storage requirements on these products.

The Globally Harmonized System (GHS) of Classification and Labelling further mandates rigorous compliance obligations for manufacturers and downstream users across European Union member states. These requirements increase operational costs for both producers and end-users, deterring smaller industrial operators from adoption and encouraging substitution with alternative bonding or fastening technologies in cost-sensitive market segments.

Surface Contamination Sensitivity and Substrate Compatibility Limitations

Anaerobic adhesives cure exclusively in the absence of oxygen through active metal ion catalysis, making them highly sensitive to surface contamination from lubricating oils, coatings, or passive metal substrates, including stainless steel and aluminum, which can inhibit polymerization unless specialized primers are applied. Technical guidelines published by adhesive industry standard bodies consistently identify inadequate surface preparation as a primary contributor to bond failure in anaerobic adhesive applications.

Such sensitivity elevates application complexity and process management costs, particularly in high-volume automated assembly environments. The additional requirement for primers and surface activators introduces incremental material and labor expenses that reduce the overall cost-competitiveness of anaerobic adhesives relative to conventional mechanical fastening methods in certain applications.

Opportunities - Expanding Aerospace and Defense Sector Procurement

The global aerospace and defense sector represents a compelling high-growth frontier for anaerobic adhesive manufacturers. The Stockholm International Peace Research Institute (SIPRI) reported that global military expenditure surpassed US$ 2.2 trillion in 2023, with ongoing procurement programs driving demand for advanced, specification-compliant assembly materials. Anaerobic adhesives are extensively used in airframe assembly, avionics enclosures, and engine component manufacturing due to their resistance to thermal cycling, hydraulic fluids, and structural vibration.

The commercial aerospace sector's post-pandemic recovery, with Airbus and Boeing both increasing production rates, adds to OEM adhesive consumption. Aerospace-grade anaerobic formulations meeting MIL-SPEC and AS9100 standards are gaining traction as manufacturers qualify next-generation products for structural and non-structural bonding in safety-critical applications.

Rise of Electronics Miniaturization and Precision Assembly

The rapid proliferation of miniaturized electronic devices, printed circuit boards (PCBs), and sensor assemblies is creating significant new demand channels for low-viscosity, high-precision anaerobic adhesives. According to the Semiconductor Industry Association (SIA), global semiconductor sales exceeded US$ 526 billion in 2023, reflecting the vast scale of global electronics manufacturing. Anaerobic adhesives are increasingly utilized for potting, encapsulation, and micro-assembly tasks in consumer electronics, industrial sensors, and automotive electronics modules.

The large-scale rollout of 5G infrastructure, proliferation of IoT devices, and expanding adoption of advanced driver-assistance systems (ADAS) are accelerating demand for adhesive formulations capable of precision application in tight geometries with fast, reliable cure performance. This trend aligns well with the growing deployment of automated dispensing systems across electronics manufacturing lines.

Category-wise Analysis

Product Type Insights

Thread lockers represent the dominant segment within the product type category, accounting for approximately 38% of the total anaerobic adhesives market in 2026. Their widespread adoption across automotive, industrial machinery, and aerospace sectors is rooted in their proven ability to prevent bolt loosening caused by vibration, shock, and thermal cycling. Available in varying strength grades, low, medium, and high, thread lockers offer application versatility across virtually all metallic fastener configurations.

The LOCTITE brand, a flagship product line under Henkel AG & Co. KGaA, is among the most globally recognized in this segment. The U.S. Department of Defense mandates the use of thread locking compounds in military vehicle and hardware assembly, reinforcing institutional demand. Continued growth in automotive and EV production globally underpins the sustained dominance of thread lockers in the anaerobic adhesives product portfolio.

Chemistry Insights

Acrylic-based anaerobic adhesives command approximately 52% of the chemistry segment, driven by their versatile performance across temperature ranges, broad substrate compatibility, and well-balanced mechanical strength profile. The acrylic chemistry platform forms the backbone of most standard thread lockers, retaining compounds, and thread sealant formulations used in mainstream industrial and automotive applications globally.

Technical publications document that acrylic anaerobic formulations deliver tensile shear strengths ranging from 10 to 30 MPa, depending on grade, making them suitable for a wide spectrum of assembly requirements. Their compatibility with automated dispensing equipment and extended shelf life under sealed ambient conditions are notable operational advantages. The dominance of acrylic chemistry is further reinforced by extensive OEM qualification data, well-established commercial supply chains, and the broad familiarity of engineers and applicators with acrylic-based adhesive systems.

End-use Industry Insights

The automotive industry accounts for approximately 34% of the total anaerobic adhesives market by end-use, confirming its position as the leading application segment. This dominance reflects the sector's intensive use of thread lockers, retaining compounds, and gasketing sealants in powertrain, chassis, and drivetrain assembly across passenger vehicles and commercial trucks. According to the OICA, global vehicle production exceeded 93 million units in 2023, with EV and hybrid vehicle output adding incremental adhesive content per vehicle due to compact, high-torque drivetrain architectures.

Modern automotive platforms utilize anaerobic adhesives in engine block assembly, wheel bearing retention, and fuel system sealing, where leak-proof performance and vibration resistance are non-negotiable. The expanding production of electric vehicles, with their precision assembly demands, further reinforces the automotive segment's leading position in the anaerobic adhesives market.

Regional Insights

North America Anaerobic Adhesives Market Trends & Analysis

North America is likely to hold a dominant share of the global anaerobic adhesives market, with 34% of the global market in 2026, underpinned by a well-established automotive manufacturing base, robust aerospace and defense procurement programs, and mature MRO industrial activity. The U.S. is the largest national contributor, with major automotive OEM facilities concentrated in Michigan, Ohio, and Tennessee, alongside aerospace supply chains serving leading prime contractors.

U.S. Anaerobic Adhesives Market Size

The U.S. is likely to account for approximately 85% of the regional anaerobic adhesives market in 2026, estimated at US$ 200 Mn. Growth is supported by expanding EV production, defense procurement, and semiconductor manufacturing activity. The U.S. Department of Defense's sustained investment in military hardware modernization drives significant demand for specification-compliant anaerobic compounds. Recent U.S. tariffs on Chinese imports, including chemical intermediates, have modestly elevated raw material costs for adhesive manufacturers but simultaneously created competitive advantages for domestic suppliers with established feedstock networks.

Europe Anaerobic Adhesives Market Trends, Drivers, & Insights

Europe is poised for 29% of the global market in 2026, characterized by a strong industrial machinery base, a globally significant automotive manufacturing sector, and rigorous regulatory oversight that has shaped product formulation strategies among leading adhesive manufacturers. The REACH regulation enforced by the European Chemicals Agency (ECHA) continues to drive manufacturers toward safer, compliant chemistries.

The European Union's ambitious carbon neutrality agenda has stimulated investments in electric mobility and wind energy infrastructure, both of which rely on reliable anaerobic adhesive bonding in assembly and maintenance applications.

Germany Anaerobic Adhesives Market Size

Germany is likely to account for an estimated 20% of the Europe anaerobic adhesives market in 2026, driven by its dominant automotive, mechanical engineering, and industrial automation sectors. Germany's leadership in mechanical engineering, precision manufacturing, and automotive production, encompassing original equipment manufacturers including BMW, Mercedes-Benz, and Volkswagen, drives elevated consumption of thread lockers and retaining compounds.

U.K. Anaerobic Adhesives Market Size

The United Kingdom market represents around 12% of the regional market, driven by aerospace and defense demand, with major industry participants including Rolls-Royce and BAE Systems as key consumers of high-grade anaerobic formulations for engine and airframe assembly.

France Anaerobic Adhesives Market Size

France is likely to represent approximately 10% of the Europe anaerobic adhesives market. The country's aeronautics sector, anchored by Airbus and Safran, along with its automotive industry (Stellantis, Renault) are the primary demand drivers for anaerobic adhesive consumption.

Asia Pacific Anaerobic Adhesives Market Drivers & Analysis

Asia Pacific is the fast-growing regional market for anaerobic adhesives, propelled by rapid industrialization, expanding automotive output, and the world's most dynamic electronics manufacturing ecosystem. Regional geopolitical developments, including ongoing U.S.-China trade tensions, have prompted supply chain realignment, with global adhesive manufacturers investing in regional manufacturing capacity to reduce dependence on any single country for critical inputs or markets.

China Anaerobic Adhesives Market Size

China represents approximately 18% of the global anaerobic adhesives market, underpinned by its position as the world's largest automotive producer and a global hub for electronics manufacturing. Strategic domestic investment in adhesive production capacity is also increasing China's self-sufficiency in specialty adhesive categories.

India Anaerobic Adhesives Market Size

India is among the fast-growing country-level markets, with 4% of the global market, driven by expanding automotive OEM activity, growing industrial infrastructure, and increasing adoption of precision bonding solutions in electronics assembly. Government-backed manufacturing incentives continue to attract investment from global adhesive manufacturers seeking to serve the Indian market.

Japan Anaerobic Adhesives Market Size

Japan is a mature yet technologically advanced anaerobic adhesives market, home to industry participants such as ThreeBond Holdings Co. and Nitto Denko Corporation. Demand is concentrated in automotive (Toyota, Honda) and electronics applications, where high precision and specialized formulation capabilities are critical differentiators.

Competitive Landscape

The global anaerobic adhesives market is moderately consolidated, with a small number of multinational corporations commanding substantial revenue shares while numerous regional and specialty players compete in niche applications. Henkel AG & Co. KGaA, through its globally dominant LOCTITE brand, holds the leading market position, followed by 3M Company, Illinois Tool Works (ITW), and H.B. Fuller Company.

Market leaders differentiate through broad portfolio coverage, deep OEM qualification networks, sustained R&D investment in next-generation formulations, and global distribution infrastructure. Strategic mergers and acquisitions remain prevalent growth tactics as larger players seek to expand specialty adhesive portfolios and regional market access.

Key Developments:

- April 2026: DELO Industrial Adhesives announced the expansion of its medical electronics portfolio with five new IBOA- and TPO-free anaerobic and light-curing adhesive solutions, targeting next-generation wearable and biosensor applications in the healthcare sector. The new DELO PHOTOBOND MG series adhesives were adapted from the company’s semiconductor and consumer electronics technologies to deliver enhanced biocompatibility for medical device manufacturing.

- April 2026: Henkel announced the launch of its global “Reliability Begins Here” program aimed at increasing awareness, adoption, and technical understanding of LOCTITE® threadlocking solutions for industrial assembly applications. The multi-year initiative focuses on improving assembly reliability, preventing fastener failures, and enhancing long-term operational performance across manufacturing industries.

- August 2024: H.B. Fuller Company announced the acquisition of HS Butyl Limited, the UK’s largest manufacturer and distributor of high-performance butyl tapes, strengthening its position in the global specialty adhesives and waterproofing solutions market. The acquisition expands H.B. Fuller’s capabilities in butyl tape technologies used across construction, infrastructure, automotive, and renewable energy applications.

Top Companies in Anaerobic Adhesives Market

- Henkel AG & Co. KGaA (Düsseldorf, Germany) is the undisputed global market leader in anaerobic adhesives through its widely recognized LOCTITE brand. The company's comprehensive product portfolio, spanning thread lockers, retaining compounds, gasketing sealants, and thread sealants, combined with deep OEM partnerships in automotive, aerospace, and industrial sectors, underpin its dominant and defensible market position worldwide.

- 3M Company (St. Paul, U.S.) offers a diversified range of adhesives and sealants, including anaerobic formulations, serving automotive, electronics, and industrial markets globally. Its expansive manufacturing footprint, strong R&D capabilities across multiple adhesive chemistries, and powerful brand recognition support its competitive positioning across both premium and standard anaerobic adhesive market segments.

- Illinois Tool Works (ITW) (Glenview, U.S.), through its Devcon and Permatex brands, holds an established position in the industrial adhesives and sealants market. ITW's diversified industrial segment serves MRO, automotive aftermarket, and OEM markets with a broad range of anaerobic thread lockers and gasketing compounds, backed by strong distribution networks and field technical service capabilities.

Companies Covered in Anaerobic Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Permabond LLC

- H.B. Fuller Company

- Illinois Tool Works (ITW)

- ThreeBond Holdings Co.

- DELO Industrial Adhesives

- Kisling AG

- Royal Adhesives & Sealants

- Parson Adhesives Inc.

- Cyberbond LLC

- Loxeal S.r.l.

- Anabond Limited

- Nitto Denko Corporation

Frequently Asked Questions

The global anaerobic adhesives market is valued at US$ 707.0 Mn in 2026 and is projected to reach US$ 1,056.1 Mn by 2033, expanding at a CAGR of 5.9% during the forecast period of 2026 - 2033.

The primary demand drivers include surging global automotive production, particularly the rapid expansion of electric vehicle manufacturing, and growing consumption in industrial machinery MRO applications. According to the OICA, global vehicle output exceeded 93 million units in 2023, generating robust and recurring demand for thread lockers and retaining compounds.

Thread lockers are the dominant product type segment, accounting for approximately 38% of the total anaerobic adhesives market. Their extensive use in automotive, aerospace, and industrial machinery applications, where vibration-resistant bolt locking is critical, drives their market leadership. The segment is anchored by globally recognized commercial brands and institutional mandates, including procurement specifications issued by the U.S. Department of Defense.

North America is the leading regional market, with 34% market share, supported by a robust automotive manufacturing sector, significant aerospace and defense procurement programs, and mature industrial MRO activity. Ongoing reshoring of manufacturing capacity and defense procurement continue to sustain North America's leadership position.

The most significant growth opportunities lie in expanding aerospace and defense procurement globally, supported by worldwide military expenditure exceeding US$ 2.2 trillion in 2023 as reported by SIPRI. Additionally, the rapid adoption of anaerobic adhesives in electronics miniaturization, driven by 5G rollout, IoT device proliferation, and advanced driver-assistance systems (ADAS) expansion, presents a compelling high-growth avenue for market participants capable of delivering precision, low-viscosity formulations at scale.

The global anaerobic adhesives market is anchored by leading multinational companies, including Henkel AG & Co. KGaA, 3M Company, Illinois Tool Works (ITW), H.B. Fuller Company, Permabond LLC, and ThreeBond Holdings Co., among others. These companies compete based on product portfolio breadth, OEM qualification depth, global distribution reach, and ongoing R&D investment in advanced adhesive chemistries.