- Non-food Packaging

- Sustainable Packaging Market

Sustainable Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Sustainable Packaging Market by Packaging Type (Rigid, Flexible), Material (Plastics, Paper & Paperboard, Glass, Metal), Process (Recyclable, Reusable, Biodegradable), Application (Food & Beverages, Personal Care & Cosmetics, Healthcare, Others), and Regional Analysis for 2025 - 2032

Sustainable Packaging Market Size and Trends Analysis

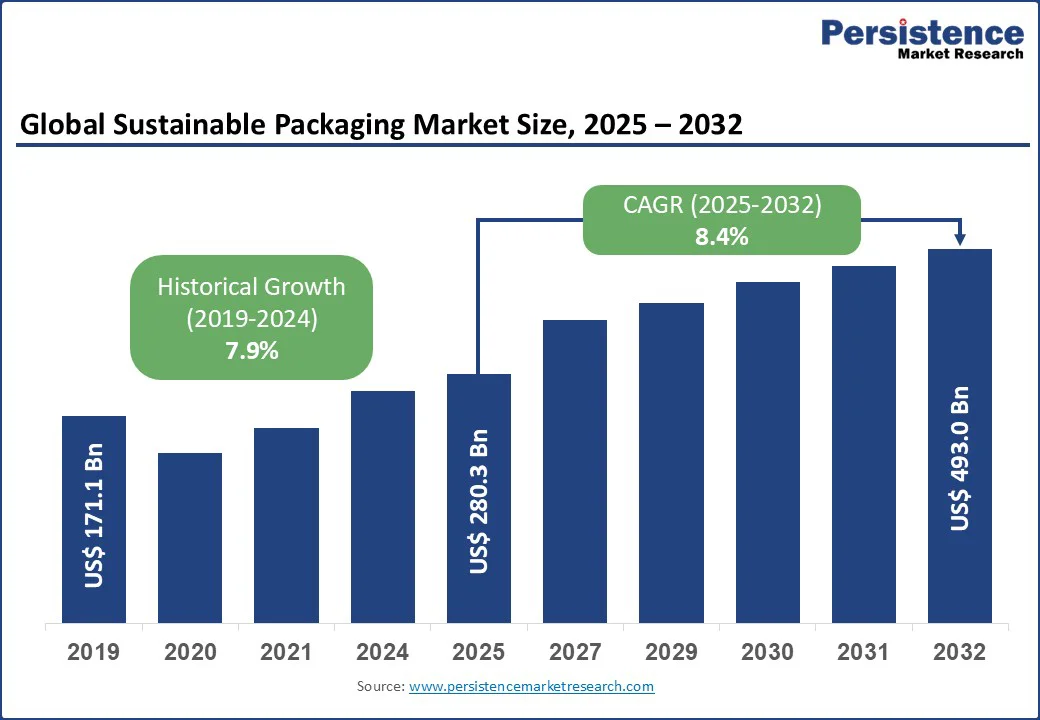

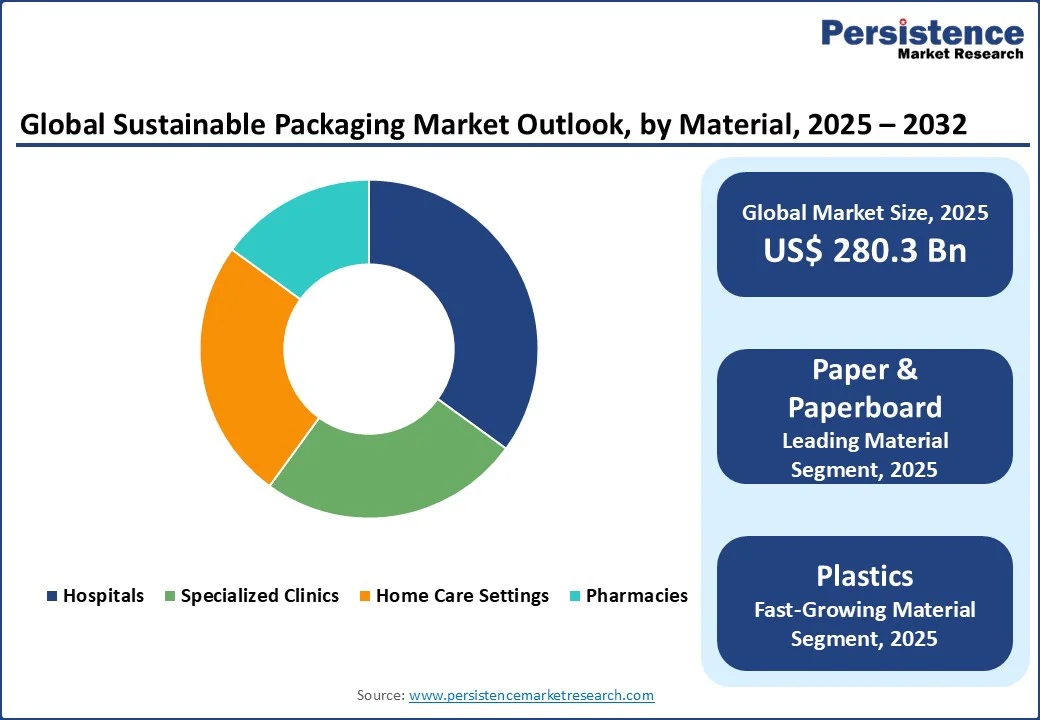

The global sustainable packaging market size is likely to be valued at US$ 280.3 Bn in 2025 and estimated to reach US$ 493.0 Bn by 2032, with growing at CAGR of 8.4% during the forecast period from 2025 to 2032, driven by increasing consumer awareness, stringent regulatory frameworks, and technological advancements in bio-based materials.

Key Industry Highlights:

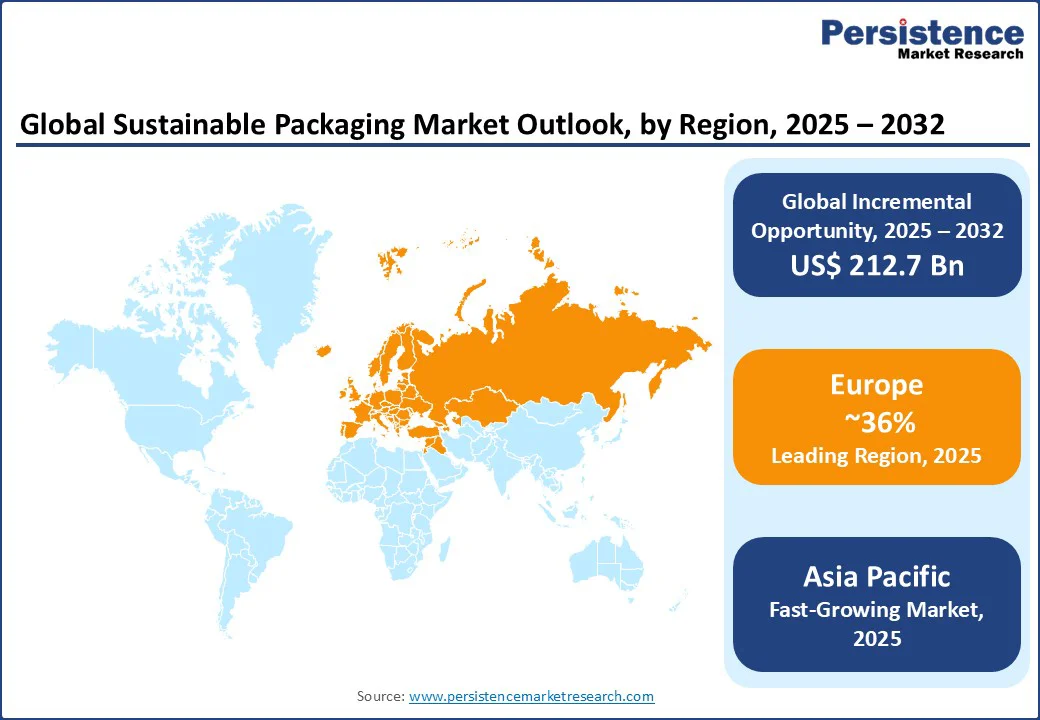

- Leading Region: Europe, holding a 36% market share in 2025, driven by stringent regulations and high consumer awareness in Germany and France.

- Fastest-growing Region: Asia Pacific, fueled by urbanization, e-commerce growth, and government initiatives in China and India.

- Dominant Packaging Type: Rigid packaging, commanding 60% market share, due to its durability in food & beverages and healthcare applications.

- Leading Application: Food & Beverages, accounting for 45% of market revenue, driven by demand for eco-friendly food packaging.

- Fastest-growing Material: Plastics (bio-based and recycled), due to advancements in sustainable polymers.

- Market Opportunity: Smart packaging integration, enhancing traceability and sustainability.

| Key Insights | Details |

|---|---|

| Sustainable Packaging Market Size (2025E) | US$ 280.3 Bn |

| Market Value Forecast (2032F) | US$ 493.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.9% |

Market Dynamics

Drivers: Stringent Government Regulations and Policies

Global regulatory frameworks aimed at reducing plastic pollution are a primary driver of the sustainable packaging market. In the U.S., California's Extended Producer Responsibility (EPR) laws, effective from 2025, mandate that 50% of packaging materials be recyclable by 2030, resulting in a 20% surge in demand for biodegradable alternatives.

In the Asia Pacific, China's 2025 regulation to eliminate non-degradable plastics in postal services has led to a 25% rise in biodegradable film adoption, supported by government subsidies of US$ 2 Bn annually.

India’s Plastic Waste Management Rules 2022 have enforced a phased ban on single-use plastics, prompting companies such as Reliance Industries to invest US$ 500 Mn in compostable packaging solutions.

These regulations not only enforce compliance but also offer tax incentives and grants, with the EU allocating €10 Bn for circular economy initiatives in 2025, driving a projected 15% annual growth in the recyclable process segment. The global push for sustainability, coupled with penalties for non-compliance ensures that regulatory pressure remains a key catalyst for the green packaging market growth.

Restraints: Higher Costs of Sustainable Materials

The production of sustainable materials, such as bio-based plastics such as polylactic acid (PLA) and recycled paper, is significantly more expensive than conventional plastics, posing a challenge to widespread adoption. For instance, biodegradable PLA packaging costs approximately US$ 1,500 per ton compared to US$ 1,000 per ton for virgin polyethylene, a 50% cost premium, according to Plastics Europe.

This cost disparity is particularly pronounced in price-sensitive markets such as South Asia and Sub-Saharan Africa, where small and medium enterprises (SMEs) account for 60% of the packaging industry but lack the capital to invest in sustainable alternatives.

The high cost of establishing recycling infrastructure, estimated at US$ 5 Bn for a single large-scale facility, further limits scalability in developing regions. Additionally, the energy-intensive production processes for bio-based materials, which can consume 30% more energy than traditional plastics, increase operational costs, impacting profit margins and slowing adoption in cost-conscious sectors such as retail and foodservice.

Opportunities: Integration of Smart Packaging Technologies

The integration of smart technologies, such as QR codes, RFID tags, and IoT-enabled sensors, into sustainable packaging presents a transformative opportunity for the market. The global smart packaging market enhances traceability, improves recycling rates, and engages consumers by providing product information, with Tetra Pak’s QR code-enabled cartons increasing recycling rates by 15% in Europe in 2025.

In healthcare, smart packaging with tamper-evident features, such as Gerresheimer AG’s biodegradable vials with NFC tags, ensures product safety while aligning with sustainability goals. In Asia Pacific, where e-commerce is expected to reach US$ 3 Tn by 2030, smart packaging reduces waste by 20% through optimized logistics and consumer-driven recycling programs.

R&D investments, totaling to US$ 2 Bn globally in 2025, are driving innovations such as edible sensors and compostable labels, creating new revenue streams in food & beverages and personal care. This convergence of technology and sustainability positions smart packaging as a key growth driver for the sustainable packaging market.

Category-wise Analysis

Packaging Type Insights

Rigid packaging dominates the sustainable packaging market, holding approximately 60% share in 2025. Its leadership is driven by its ability to provide superior protection for high-value products, such as beverages, dairy, and pharmaceuticals, ensuring safety during transportation and storage. Rigid packaging, including glass bottles and metal cans, aligns with circular economy goals, with recycling rates exceeding 70% in North America and Europe.

Flexible packaging is the fastest-growing segment. Its growth is driven by its lightweight nature, lower carbon footprint, and adaptability to e-commerce and personal care applications. Flexible packaging, such as biodegradable films and paper-based pouches, reduces material usage by up to 30% compared to rigid alternatives, lowering shipping costs and emissions. UFlex Limited’s compostable films, used in cosmetics and food packaging, decompose within 180 days, appealing to eco-conscious consumers.

Material Insights

Paper & Paperboard leads the material segment, commanding approximately 42% share in 2025. Its dominance is attributed to its inherent biodegradability, high recyclability, and cost-effectiveness compared to plastics. Paper-based packaging, including corrugated boxes and kraft paper, is widely adopted in food & beverages and e-commerce, with recycling rates reaching 80% in Europe, according to CEPI. DS Smith and Smurfit Kappa offer corrugated solutions that reduce logistics emissions by 25%, supporting sustainability goals in retail.

Plastics (bio-based and recycled) are the fastest-growing material segment. Advancements in bio-based plastics, such as polylactic acid (PLA) and polyhydroxyalkanoates (PHA), have improved their environmental profile, making them viable alternatives to traditional plastics. Berry Global’s recycled PET solutions, used in beverage bottles, reduce virgin plastic use by 30%, aligning with circular economy principles

Process Insights

Recyclable processes dominate the sustainable packaging market, accounting for approximately 50% share in 2025. The segment’s leadership is driven by well-established recycling infrastructure in developed regions and regulatory mandates, such as the EU’s 90% recycling target for packaging by 2030. Smurfit Kappa’s recyclable corrugated solutions, used in food & beverages, achieve recovery rates of 85%, supported by advanced sorting technologies

Biodegradable processes are the fastest-growing, driven by increasing demand for compostable packaging in foodservice and organic waste management, particularly in Europe and Asia Pacific. Novamont’s Mater-Bi films, which decompose in 6 months, are widely used in single-use applications such as food packaging, reducing landfill waste by 30%. The segment’s growth is further supported by consumer preference for zero-waste solutions and regulatory incentives for compostable materials.

Application Insights

Food & beverages leads the application segment, holding a 45% share in 2025, driven by the need to reduce food waste and plastic pollution, with sustainable packaging solutions such as Tetra Pak’s renewable cartons cutting plastic use by 40%.

The global food packaging market, relies on eco-friendly options to meet consumer demand, with 70% of shoppers choosing brands with green packaging. The segment’s growth is supported by innovations in barrier technologies, ensuring product freshness while maintaining sustainability, and corporate commitments to zero-waste packaging.

Personal care & cosmetics is the fastest-growing application, driven by eco-conscious consumers and brand sustainability initiatives. The global cosmetics market, is shifting toward recycled plastic and paper-based packaging, with L’Oréal and Huhtamaki launching biodegradable tubes that reduce waste by 25%. Innovations in refillable packaging, such as Elevate Packaging’s reusable containers, and minimalist designs further accelerate growth, making this segment a key focus for eco-friendly packaging market expansion.

Regional Insights

North America Sustainable Packaging Market Trends

North America holds a 28% share in 2025, driven by strong consumer awareness and corporate sustainability initiatives. The U.S. leads with investments in recycling infrastructure, totaling US$ 12 Bn in 2025, and corporate pledges such as Walmart’s Project Gigaton, aiming to eliminate 1 Gt of emissions by 2030 through sustainable packaging.

The food & beverages sector, accounting for 50% of the region’s sustainable packaging demand, benefits from recyclable paperboard and glass, with Sonoco Products offering solutions that reduce material usage by 20%. Canada’s zero-waste policies, with cities such as Vancouver achieving 70% recycling rates, support growth in biodegradable packaging.

The region is fueled by regulatory support, such as the U.S.’s Packaging and Recycling Infrastructure Modernization Act, and consumer preference for eco-friendly brands, with 75% of shoppers choosing sustainable products.

Europe Sustainable Packaging Market Trends

Europe dominates with a 36% share in 2025, led by Germany, France, and the U.K. Germany’s Packaging Act mandates 90% recyclability by 2030, driving a 25% increase in paper & paperboard adoption, with Smurfit Kappa leading in corrugated solutions for food & beverages. France’s Anti-Waste Law promotes reusable packaging, with Constantia Flexibles offering biodegradable films for healthcare that decompose in 90 days.

The EU’s Circular Economy Action Plan, backed by €10 Bn in funding, supports innovations in bio-based plastics. The food & beverages sector, accounting for 55% of demand, benefits from consumer preference for eco-labels, with 70% of shoppers choosing sustainable packaging. Companies such as Tetra Pak are expanding renewable carton production, reducing carbon emissions by 15% in dairy and beverage applications.

Asia Pacific Sustainable Packaging Market Trends

Asia Pacific holds a 30% market share in 2025, with China and India as key drivers. China’s 2025 ban on non-degradable plastics in e-commerce has spurred a 30% increase in biodegradable packaging, with UFlex Limited supplying compostable films for retail. India’s e-commerce market, valued at US$ 100 Bn in 2025, drives demand for flexible packaging, with Atlantic Packaging offering recyclable pouches that cut emissions by 15%.

Japan’s focus on sustainable food packaging, with Tetra Pak’s 80% renewable cartons, supports growth in the beverage sector. The region is fueled by rapid urbanization, rising disposable incomes, and government incentives, such as China’s US$ 1 Bn green manufacturing fund. South Korea and Southeast Asia are emerging markets, with a 20% increase in bio-plastic adoption driven by regulatory support and consumer demand.

Competitive Landscape

The global sustainable packaging market is highly competitive, with key players including Sonoco Products Company, Smurfit Kappa, Berry Global Inc., Tetra Pak, Elevate Packaging, Huhtamaki Oyj, Mondi, DS Smith, Atlantic Packaging, UFlex Limited. These companies hold over 65% of the market share, leveraging innovation and strategic partnerships to maintain leadership.

Their strategies often focus on developing recyclable, biodegradable, and compostable packaging solutions to align with evolving regulatory standards and rising consumer demand for eco-friendly alternatives. Strategic initiatives such as partnerships, mergers and acquisitions, joint ventures, and investments in advanced materials enable them to strengthen portfolios and expand geographic reach.

Key Developments

- In January 2024, Sealed Air launched a compostable protein packaging tray at IPPE 2024, introducing the CRYOVAC brand compostable overwrap tray made from biobased, food-contact grade resin. This tray is certified as industrial compostable and soil and marine biodegradable, offering a sustainable alternative to traditional EPS foam trays. Company’s commitment to sustainability includes designing recyclable or reusable packaging solutions and incorporating recycled or renewable content.

- In December 2023, Novolex, through its brand Waddington North America (WNA), introduced food packaging containers that are recyclable and made with a minimum of 10% post-consumer recycled (PCR) content. These new products include various items, such as dessert cups, tamper-evident containers, cake containers, and bakery clamshells. The containers are designed to enhance food presentation and come in different sizes and shapes to cater to various needs.

Companies Covered in Sustainable Packaging Market

- Sonoco Products Company

- Smurfit Kappa

- Berry Global Inc.

- Tetra Pak

- Elevate Packaging

- Huhtamaki Oyj

- Mondi

- DS Smith

- Atlantic Packaging

- UFlex Limited

- Constantia Flexibles

- Genpak

- Reynolds Packaging

- Crown Holdings, Inc.

- Gerresheimer AG

- Novamont S.p.A.

- WestRock Company

- Ernest Packaging Solutions

Frequently Asked Questions

The global sustainable packaging market is projected to reach US$ 280.3 Bn in 2025.

Stringent regulations, consumer demand for eco-friendly packaging, and e-commerce growth drive the market.

The sustainable packaging market is expected to grow at a CAGR of 8.4% from 2025 to 2032.

Integration of smart packaging, circular economy models, and expansion in emerging markets offer significant opportunities.

Key players include Sonoco Products Company, Smurfit Kappa, Berry Global Inc., Tetra Pak, and Mondi.