- Bulk Chemicals

- Ceramic Tile Adhesive Market

Ceramic Tile Adhesive Market Size, Share, and Growth Forecast, 2026 - 2033

Ceramic tile adhesive market by Product Type (Cementitious Adhesive, Dispersion Adhesive, Reaction Resin Adhesive), Application (Residential, Commercial, Industrial), End-use (Construction, Renovation, Others), and Regional Analysis for 2026 - 2033

Ceramic Tile Adhesive Market Size and Trends Analysis

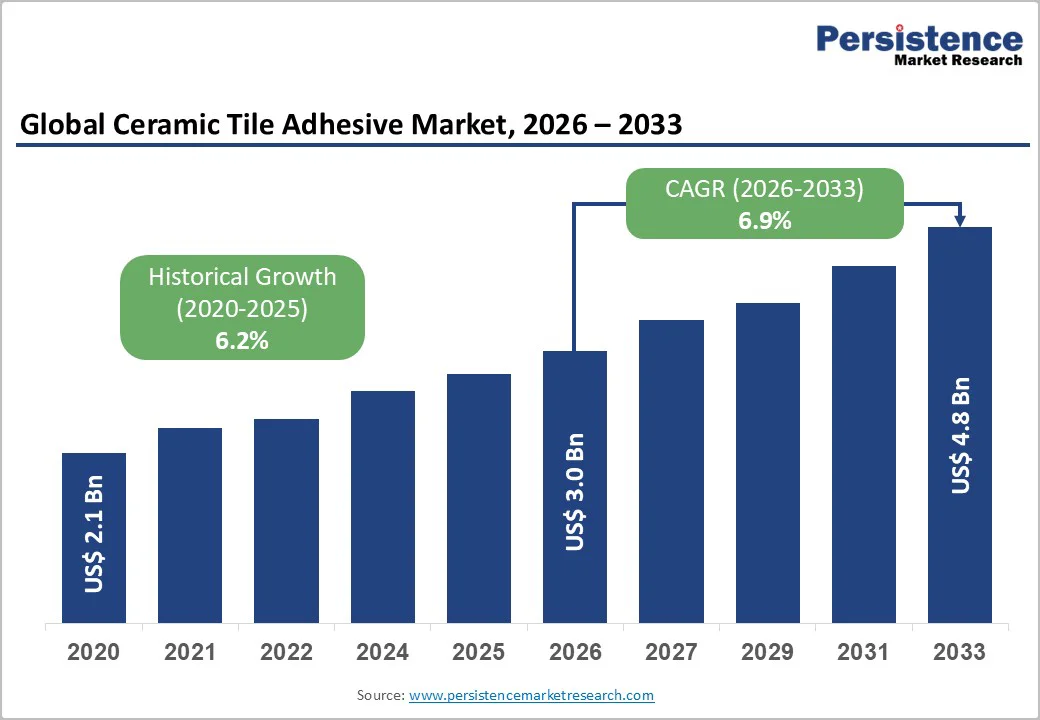

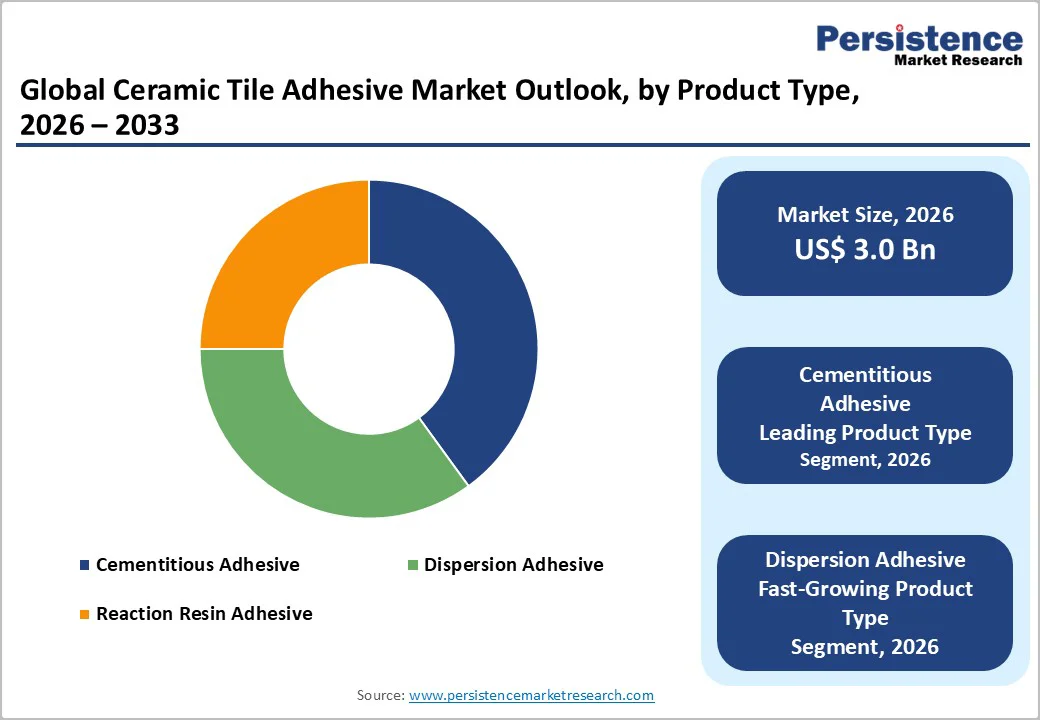

The global ceramic tile adhesive market is projected to be valued at US$3.0 Bn in 2026, reaching US$4.8 Bn by 2033, representing a CAGR of 6.9% from 2026 to 2033.

The ceramic tile adhesive industry is experiencing robust growth driven by the growing prevalence of home renovation projects, rising demand for high-bond-strength adhesives in commercial flooring, and advancements in polymer-based formulations. The need for durable, water-resistant bonding solutions, particularly in residential applications, has significantly boosted the adoption of ceramic tile adhesives across various demographics.

The market is further propelled by innovations in cementitious and dispersion types, catering to preferences for easy application and eco-friendly options. The growing acceptance of ceramic tile adhesives as essential for modern interiors, particularly in construction, is a key growth driver in the ceramic tile adhesive market.

Key Industry Highlights :-

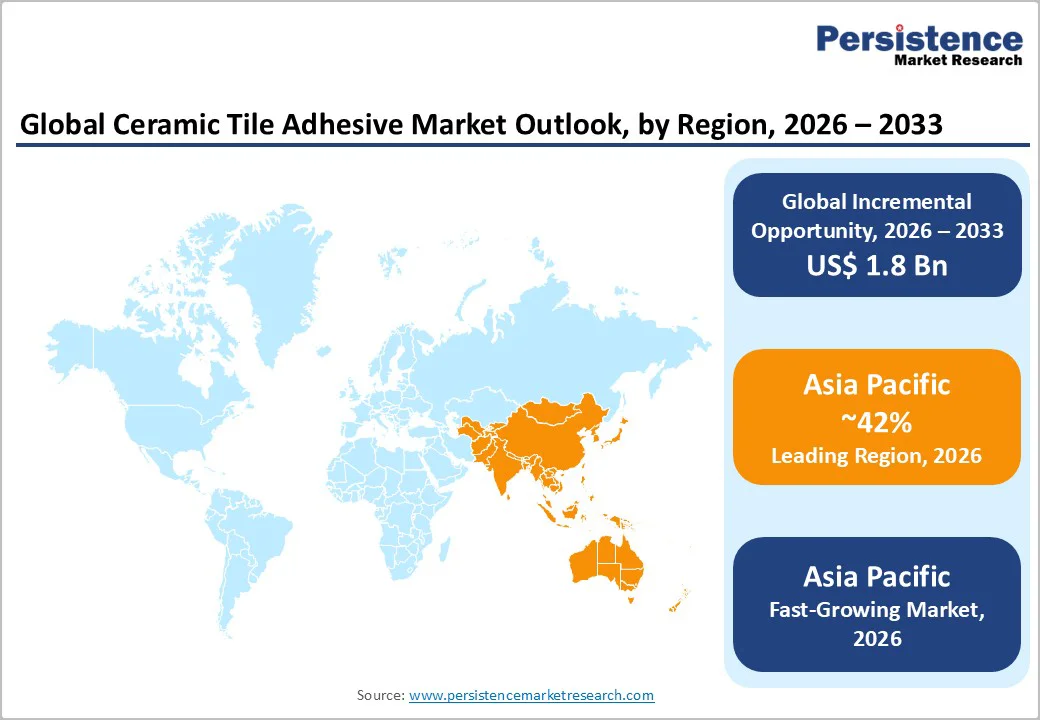

- Leading Region: Asia Pacific, anticipated a 50% market share in 2026, driven by a massive construction boom, high prevalence of urban renovation, and strong R&D activities in China.

- Dominant Product Type: Cementitious Adhesive, holding approximately 55% of the market share, due to cost-effectiveness and versatility.

- Leading Application: Residential, accounting for over 45% of market revenue, driven by home improvement needs.

- Leading End-use: Construction, contributing nearly 60% of market revenue, due to flooring projects.

- Key Market Driver: Surging global construction and renovation activities are accelerating demand for high-performance ceramic tile adhesives.

- Market Opportunity: Expansion in eco-friendly, low-VOC formulations creates strong opportunities for sustainable ceramic tile adhesive variants.

| Key Insights | Details |

|---|---|

| Ceramic Tile Adhesive Market Size (2026E) | US$3.0 Bn |

| Market Value Forecast (2033F) | US$4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Dynamics

Driver - Rising prevalence of home renovation projects and demand for high-bond strength adhesives

The rising prevalence of home renovation projects and the growing demand for high-bond-strength adhesives are major drivers of the ceramic tile adhesive market. With increasing consumer interest in upgrading kitchens, bathrooms, and flooring, renovation activity has surged across residential spaces.

Factors such as aging infrastructure, evolving interior design preferences, and the rise of homeownership have further accelerated this trend. DIY culture, supported by easy-to-apply adhesive formulations and widespread availability through retail and online channels, has also contributed to market growth.

As homeowners seek long-lasting and visually appealing finishes, high-bond strength adhesives have become essential for ensuring durable tile installations. These advanced adhesives offer superior adhesion, enhanced flexibility, and improved resistance to moisture, temperature fluctuations, and heavy foot traffic.

Their reliability makes them suitable not just for standard ceramic tiles but also for larger, heavier, and more premium tile formats increasingly used in modern homes. Professional installers and contractors prefer high-performance adhesives to reduce installation failures, minimize maintenance, and ensure long-term structural integrity.

Restraint - High development and environmental compliance costs

The high costs associated with development and environmental compliance of ceramic tile adhesives pose a significant restraint on market growth. Formulating these adhesives requires advanced polymers, rigorous shear testing, and low-VOC additives to ensure safety. These processes involve substantial financial investment, often exceeding millions of dollars, which can be a barrier for smaller manufacturers.

Regulatory bodies impose stringent requirements for emission limits and recyclability. Compliance with these standards, along with the need for certified facilities, increases overall costs and extends development timelines. For instance, creating reaction-resin variants can take years, with costs escalating due to multiple phases of toxicity testing.

Smaller firms struggle against players such as Sika AG. Furthermore, the complexity of water-resistant grades adds to production challenges, deterring innovation in regulated regions.

Opportunity - Advancements in low-VOC and eco-friendly adhesive formulations

Advancements in low-VOC and eco-friendly adhesive formulations have emerged as a major growth driver in the ceramic tile adhesive market, reshaping product development and industry standards. As global regulations tighten around indoor air quality and environmental sustainability, manufacturers increasingly prioritize formulations that minimize volatile organic compound (VOC) emissions.

These low-VOC adhesives not only reduce health risks for installers and occupants but also align with green building certifications such as LEED and BREEAM, boosting their adoption in residential, commercial, and institutional projects.

Innovation in bio-based polymers, waterborne systems, and solvent-free chemistries further accelerated the shift toward sustainable adhesive solutions. Companies invested heavily in R&D to create products offering high bonding strength, durability, and resistance to moisture while maintaining an environmentally responsible profile.

Advancements in raw material technology enabled the development of adhesives with improved flexibility, faster curing times, and enhanced compatibility with modern tiles and substrates.

Category-wise Analysis

Product Type Insights

Cementitious adhesive dominates the market, expected to account for approximately 55% of the market share in 2026. Its dominance is driven by affordability, ease of use, and strong bonding, making it preferred for residential. Cementitious adhesive, such as that from Henkel AG & Co. KGaA, provides a quick set, ensuring installation. Its versatility and cost make it preferred for contractors.

The dispersion adhesive is the fastest-growing segment, driven by its flexibility, strong bond strength, and growing use in commercial projects. Its excellent water resistance makes it ideal for wet areas such as bathrooms and kitchens. Advancements in polymer technology and rising demand for eco-friendly formulations further accelerated adoption, particularly in the Asia Pacific and Europe.

Application Insights

Residential leads the market, holding approximately 45% of the share in 2026, driven by strong demand for tile installations in kitchens, bathrooms, and living spaces. The rise of home renovation projects and growing DIY culture further support dominance. Easy availability of adhesives, affordability, and preference for modern interiors boost adoption across households.

Commercial is the fastest-growing segment, fueled by offices, retail spaces, hotels, and public facilities increasingly adopting ceramic tiles for durability and modern aesthetics. Large-scale construction and renovation projects require reliable, high-performance adhesives that ensure long-lasting installations. The need for efficient application, low maintenance, and strong bonding further accelerates adoption in high-footfall commercial environments.

End-use Insights

Construction dominates the market, contributing nearly 60% of revenue in 2026, due to the extensive use of tile adhesives in residential, commercial, and infrastructure projects. Large-scale building activities, renovation programs, and government-backed developments drive demand. Tile adhesives offer durability, efficiency, and strong bonding, making them the preferred choice for contractors and builders across diverse construction applications.

Renovation is the fastest-growing segment, driven by homeowners increasingly investing in upgrades, remodeling, and aesthetic improvements. Rising spending on home improvement, coupled with the desire for modern interiors, has accelerated demand for tile adhesives. Their versatility, ease of application, and compatibility with diverse tile types make them ideal for quick, efficient renovation projects, driving rapid adoption.

Regional Insights

North America Ceramic Tile Adhesive Market Trends

North America is projected to account for nearly 20% of the global Ceramic Tile Adhesive Market in 2026, driven primarily by increasing residential and commercial construction activity, remodeling projects, and infrastructure development across the U.S., Canada, and Mexico.

Rising consumer demand for high-quality, durable flooring and aesthetically appealing interiors has fueled the adoption of ceramic tiles, directly supporting growth in tile adhesive consumption. The market benefited from a shift toward modern construction techniques, in which high-performance adhesives are preferred for their durability, quick-setting properties, and strong bond strength.

Product innovation has been a key driver in North America. Manufacturers focused on eco-friendly, low-VOC, and solvent-free adhesives to meet strict environmental regulations and growing consumer preference for sustainable building materials. Ready-to-use, pre-mixed, and quick-setting adhesives have gained popularity among contractors and DIY consumers, offering convenience and efficiency.

The market also saw increased penetration through strategic partnerships, mergers, and acquisitions, which expanded production capacities and distribution networks. Growth in organized retail, specialty stores, and e-commerce platforms enhanced accessibility for both professional contractors and end-users.

Europe Ceramic Tile Adhesive Market Trends

Europe is expected a 25% of the share in 2026, driven by ongoing construction, renovation, and infrastructure projects across both residential and commercial sectors.

Countries such as Germany, France, Italy, and the U.K. emerged as key contributors due to high construction standards, increasing urban development, and government initiatives promoting energy-efficient and sustainable buildings. Rising consumer preference for modern interior designs, decorative tiles, and durable flooring solutions further bolstered demand for high-performance tile adhesives.

Product innovation played a significant role in shaping market trends. European manufacturers focused on eco-friendly, low-VOC, and solvent-free adhesives to comply with stringent environmental regulations and meet the growing consumer demand for sustainable building materials. Additionally, ready-to-use, quick-setting, and high-bond strength adhesives became popular in both DIY and professional construction projects, offering convenience and efficiency.

The market also benefited from strategic collaborations, mergers, and acquisitions, which enabled companies to expand production capacity, strengthen distribution networks, and enhance technological capabilities. Growth in organized retail, e-commerce, and professional contractor channels further improved product accessibility.

Asia Pacific Ceramic Tile Adhesive Market Trends

Asia Pacific is the dominating and fastest-growing market for ceramic tile adhesives, projected a 42% of the share in 2026, driven by rapid urbanization, infrastructure expansion, and strong construction activity.

Countries such as China, India, and Southeast Asian nations have witnessed a surge in residential, commercial, and industrial construction projects, fueling demand for high-performance tile adhesives. Increasing disposable income, evolving lifestyles, and a preference for aesthetically appealing interiors have further boosted the use of ceramic tiles, directly benefiting adhesive consumption.

Technological advancements and product innovation have also played a critical role in Asia Pacific’s growth. Manufacturers focused on eco-friendly, low-VOC, and solvent-free adhesives, catering to rising environmental regulations and consumer awareness about sustainability. The adoption of ready-to-use, quick-setting, and high-bond strength adhesives has enhanced efficiency in both large-scale construction projects and smaller residential applications.

Strategic initiatives such as partnerships, local manufacturing, and distribution expansion by leading players have strengthened market penetration across emerging economies. The growth of organized retail, e-commerce platforms, and modern trade channels has improved accessibility for contractors, retailers, and end consumers.

Competitive Landscape

The global ceramic tile adhesive market is highly competitive, characterized by a mix of multinational chemical giants and specialized regional players. In developed regions such as North America and Europe, companies such as BASF SE and Sika AG maintained leadership positions through extensive R&D investments, advanced formulation technologies, and well-established distribution networks.

Their focus on product innovation, high-performance adhesives, and compliance with stringent regional standards enabled them to sustain market dominance and cater to both commercial and residential construction sectors.

In the Asia Pacific region, Pidilite Industries strengthened its market presence by offering localized adhesive solutions tailored to regional construction practices, climatic conditions, and consumer preferences. The company’s ability to develop cost-effective, durable, and easy-to-use products enhanced its competitiveness in this rapidly growing market.

Companies prioritized eco-friendly and sustainable innovations, including low-VOC, solvent-free, and bio-based adhesives, which provided a significant competitive advantage. Strategic partnerships, mergers, and acquisitions reshaped the market landscape by expanding geographic reach, enhancing technological capabilities, and consolidating production capacities.

Key Developments

- In July 2024, Sika AG introduced SikaCeram-50 BH a ready-to-use, one-pack premixed thin-bed tile adhesive that requires only water to apply. It is designed for both floor and wall tiles, offering ease of use and reliable bonding.

- In June 2023, Pidilite Industries Ltd, a leading manufacturer of construction and specialty chemicals, announced the launch of its state-of-the-art manufacturing facilities under its two joint ventures, Pidilite Litokol Pvt Ltd (PLPL) and Tenax Pidilite Pvt Ltd (TPPL), in Amod, Gujarat. Litokol SPA Italy and Tenax SPA Italy have transferred technology to Pidilite as part of the Joint Venture. This event signifies a milestone development in technology transfer in India's stone and ceramic solutions industry.

Companies Covered in Ceramic Tile Adhesive Market

- BASF SE

- Sika AG

- Mapei S.p.A.

- Bostik (Arkema)

- Henkel AG & Co. KGaA

- Ardex Group

- H.B. Fuller

- Laticrete International, Inc.

- Fosroc International Limited

- Pidilite Industries

- Saint-Gobain Weber

- Terraco Group

- Others

Frequently Asked Questions

The global ceramic tile adhesive market is projected to reach US$ 3.0 Bn in 2026.

The rising prevalence of home renovation projects and demand for high-bond strength adhesives are key drivers.

The market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Advancements in low-VOC and eco-friendly adhesive formulations are key opportunities.

BASF SE, Sika AG, Mapei S.p.A., Bostik (Arkema), and Henkel AG & Co. KGaA are key players.