- Inks, Coatings, Adhesives & Sealants (ICAS)

- Hot Melt Adhesive Market

Hot Melt Adhesive Market Size, Share, and Growth Forecast 2026 - 2033

Hot Melt Adhesive Market by Product Type (Ethylene Vinyl Acetate (EVA), Polyamide, Polyolefin, Polyurethane, Styrene Block Copolymers (SBC), Silane Modified Polymers, Bio-based), Technology (Thermoplastic Hot Melts, Hot Melt Pressure Sensitive Adhesives (HMPSA), Reactive Hot Melts (RHMs), Others), Industry, Distribution Channel (Offline Retail, Online Retail, OEM), and Regional Analysis, 2026 - 2033

Hot Melt Adhesive Market Size and Trend Analysis

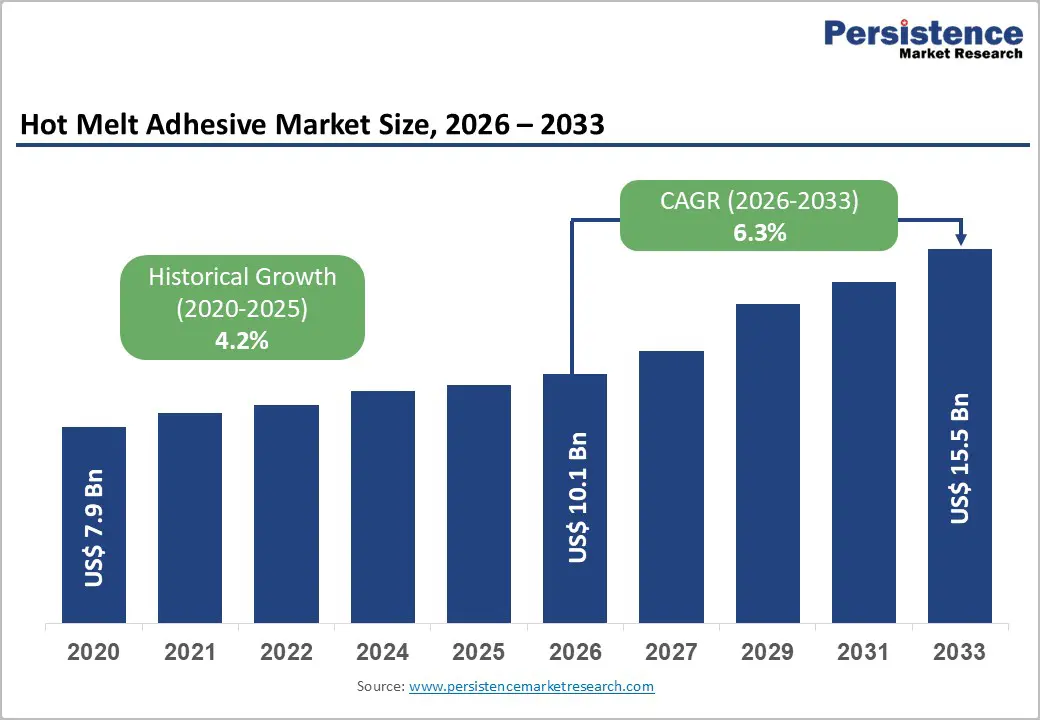

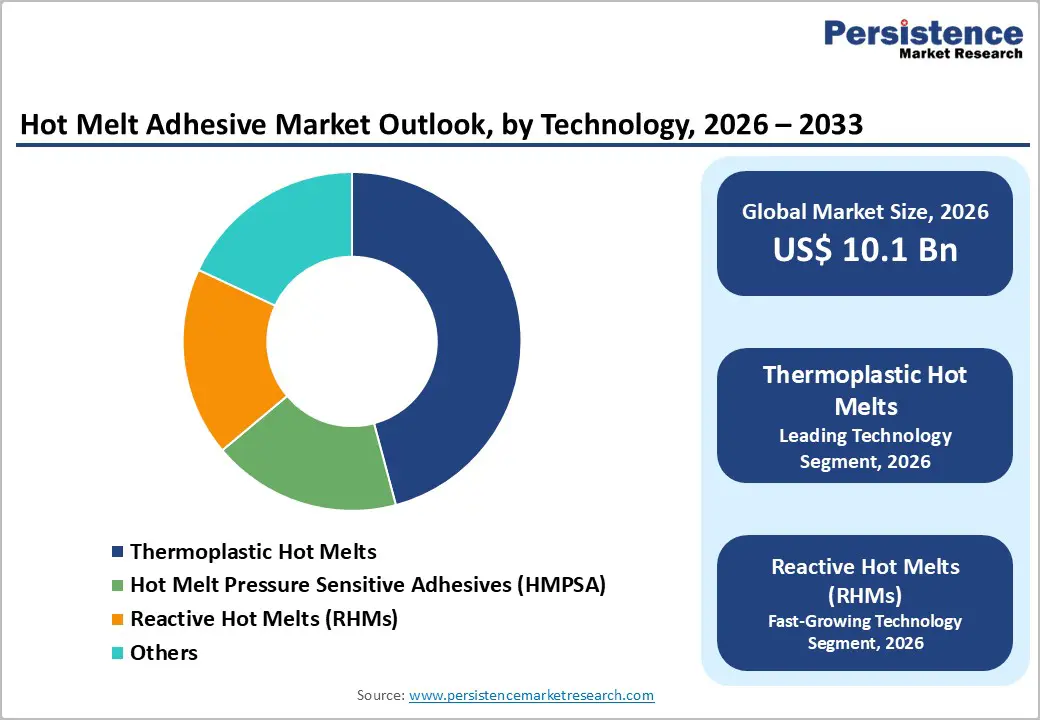

The global Hot Melt Adhesive market size is expected to be valued at US$ 10.1 billion in 2026 and projected to reach US$ 15.5 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033. This sustained growth trajectory is underpinned by accelerating demand across end-use industries, including packaging, automotive, nonwoven hygiene products, and electronics, where hot melt adhesives offer decisive advantages over solvent-based alternatives in terms of application speed, environmental compliance, and bond performance.

The global shift toward sustainable, low-VOC (volatile organic compound) bonding solutions is reinforcing hot melt adhesives as the technology of choice for manufacturers navigating tightening environmental regulations. Simultaneously, rapid industrialization across Asia Pacific and the structural expansion of e-commerce-driven packaging demand are creating high-volume, recurring consumption opportunities for adhesive manufacturers globally.

Key Industry Highlights

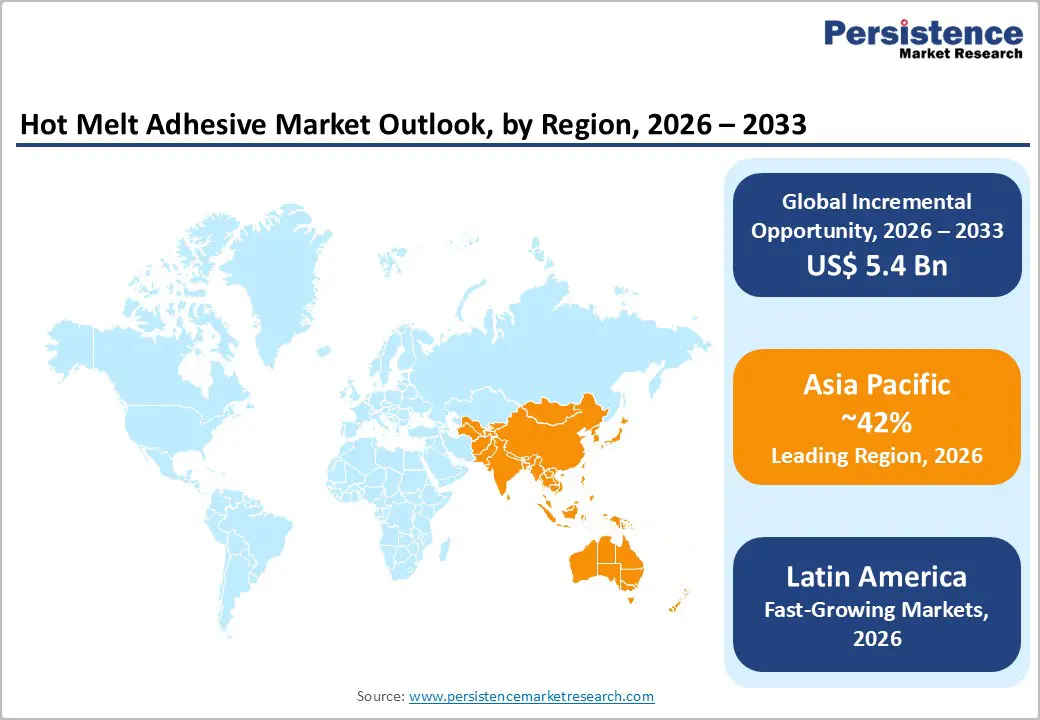

- Leading Region: Asia Pacific leads the global Hot Melt Adhesive market with approximately 42% share in 2025, driven by China’s dominant packaging, automotive, and nonwoven hygiene manufacturing base, supported by rapid industrialization across India and ASEAN nations.

- Fastest Growing Region: Latin America is among the fastest-growing regions in the Hot Melt Adhesive market through 2033, fueled by expanding e-commerce packaging demand, growth in organized retail, and increasing automotive production investment across Brazil, Mexico, and Argentina.

- Dominant Industry: Packaging is the dominant Industry segment, representing approximately 35% of global market share in 2025, anchored by the sector’s massive and growing volume of case sealing, carton closing, label application, and flexible packaging lamination operations worldwide.

- Fastest Growing Technology: Reactive Hot Melts (RHMs) represent the fastest-growing technology segment through 2033, driven by surging demand in electric vehicle battery assembly, electronics encapsulation, and aerospace applications where superior bond strength, heat resistance, and moisture durability are critical requirements.

- Key Opportunity: The development of bio-based and recyclability-compatible hot melt adhesive formulations represents the market’s most strategically important opportunity, aligned with EU PPWR mandates and global brand owner sustainability commitments that are reshaping adhesive specification requirements across the packaging value chain.

| Key Insights | Details |

|---|---|

|

Hot Melt Adhesive Market Size (2026E) |

US$ 10.1 Billion |

|

Market Value Forecast (2033F) |

US$ 15.5 Billion |

|

Projected Growth CAGR (2026–2033) |

6.3% |

|

Historical Market Growth (2020–2025) |

4.2% |

Market Dynamics

Drivers - Surging Packaging Demand Driven by E-commerce Expansion and Sustainable Bonding Requirements

The global e-commerce sector’s unprecedented expansion is one of the most powerful demand catalysts for hot melt adhesives, particularly in case sealing, carton closing, and label application functions. According to the United Nations Conference on Trade and Development (UNCTAD), global e-commerce sales have grown consistently year-on-year, with the sector valued at over US$ 26 trillion globally. Every parcel dispatched through e-commerce supply chains requires reliable, high-speed adhesive bonding at multiple stages of packaging. Hot melt adhesives excel in high-throughput automated packaging lines due to their instantaneous bonding characteristics and compatibility with a wide range of substrate types. Additionally, regulatory pressure to eliminate solvent-based adhesives, driven by U.S. Environmental Protection Agency (EPA) and European Chemicals Agency (ECHA) VOC reduction mandates, is accelerating reformulation toward hot melt alternatives across food-grade and industrial packaging applications globally.

Growing Automotive and Nonwoven Hygiene Industry Adoption Expanding Application Scope

The automotive sector’s transition toward lightweight vehicle architectures, driven by fuel efficiency mandates and the accelerating electrification of vehicle platforms, is creating robust and expanding demand for hot melt adhesives as structural and semi-structural bonding agents. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production exceeded 93 million units in 2023 and is expected to grow modestly through 2033, with electric vehicle platforms particularly adhesive-intensive due to battery module assembly, interior trim bonding, and wire harnessing requirements. Simultaneously, the global nonwoven and hygiene products sector, encompassing adult incontinence products, baby diapers, and feminine care items, is a major consumer of Hot Melt Pressure Sensitive Adhesives (HMPSA). The Association of the Nonwoven Fabrics Industry (INDA) reports continued growth in global nonwoven production, directly translating into sustained adhesive consumption growth in this segment.

Restraints - Raw Material Price Volatility Impacting Manufacturer Margins

Hot melt adhesives are derived from petroleum-based polymers including ethylene vinyl acetate (EVA), polyolefins, polyamides, and styrene block copolymers (SBC), making production costs highly sensitive to crude oil and petrochemical feedstock price movements. The U.S. Energy Information Administration (EIA) has documented significant crude oil price volatility over recent years, with benchmark prices fluctuating between US$ 60 and US$ 130 per barrel since 2020. These feedstock cost swings compress adhesive manufacturer margins and complicate long-term supply contract pricing, particularly for small and mid-sized producers. Downstream customers in price-sensitive industries such as packaging and bookbinding resist cost pass-through, creating persistent margin pressure that can constrain R&D investment and capacity expansion among adhesive producers operating in competitive market environments.

Environmental and Regulatory Scrutiny of High-Temperature Application Processes

Despite their classification as low-VOC alternatives to solvent adhesives, hot melt adhesives face growing regulatory and occupational health scrutiny regarding the fumes and particulates generated during high-temperature application processes. The European Agency for Safety and Health at Work (EU-OSHA) has published guidance on thermal degradation products associated with hot melt application, flagging potential respiratory exposure risks that require engineering controls in industrial settings. Compliance with these occupational safety standards adds equipment and process complexity for manufacturing users, particularly in food packaging environments where adhesive fume migration onto food-contact surfaces must be rigorously controlled. These regulatory dynamics may incrementally constrain adoption in certain sensitive end-use applications and add compliance cost burdens that disadvantage smaller adhesive users and contract packagers.

Opportunities - Reactive Hot Melt Adhesives Unlocking High-Performance Applications in Automotive and Electronics

Reactive Hot Melts (RHMs), which undergo a chemical cross-linking reaction after application to form thermoset bonds of exceptional strength, heat resistance, and moisture durability, represent one of the most commercially significant growth opportunities within the hot melt adhesive technology landscape. Unlike conventional thermoplastic hot melts, RHMs deliver bond performance approaching that of two-component structural adhesives, making them viable for demanding automotive, electronics, and aerospace applications where conventional hot melts were historically insufficient. Henkel AG & Co. KGaA and Sika AG have both made substantial R&D investments in polyurethane-reactive (PUR) hot melt platforms tailored to automotive interior assembly and electronics encapsulation. As electric vehicle (EV) production scales globally, with the International Energy Agency (IEA) projecting over 40% of new car sales to be electric by 2030, the demand for high-performance reactive hot melt adhesives in battery module assembly, structural glazing, and lightweight composite bonding is expected to accelerate materially through 2033.

Bio-Based and Sustainable Hot Melt Adhesive Development Aligning with Circular Economy Mandates

The global transition toward sustainable chemistry and circular economy packaging models is creating a strategically important opportunity for hot melt adhesive manufacturers to develop and commercialize bio-based and recyclability-compatible adhesive formulations. The European Union’s Packaging and Packaging Waste Regulation (PPWR), which entered legislative process in 2023 and is expected to be fully enforced by 2030, mandates that all packaging placed on the EU market be recyclable or compostable by defined deadlines. Adhesive formulations that inhibit paper fiber recycling, a known challenge with certain conventional hot melts, are coming under increasing scrutiny from packaging producers and brand owners. Companies including HB Fuller Company and Jowat SE have announced active development programs targeting adhesive formulations compatible with paper and board recycling streams. This regulatory alignment creates a first-mover advantage opportunity for adhesive producers capable of commercializing certified sustainable hot melt solutions ahead of mandated compliance timelines.

Category-wise Analysis

Product Type Insights

Ethylene Vinyl Acetate (EVA) is the dominant product type within the Hot Melt Adhesive market, accounting for approximately 38% of global market share in 2025. EVA-based hot melts have maintained market leadership due to their exceptionally broad applicability across end-use industries, including packaging, bookbinding, woodworking, and nonwoven hygiene, combined with favorable processing characteristics, cost competitiveness relative to specialty polymer alternatives, and compatibility with standard hot melt application equipment. EVA copolymers offer a tunable range of softening points and open times, enabling formulators to tailor adhesive performance for specific substrates and application conditions. The widespread availability of EVA polymer feedstocks from producers including DOW Inc. and Arkema S.A. ensures a secure and competitive supply base. While polyurethane reactive and polyolefin hot melts are gaining share in high-performance segments, EVA’s cost-performance balance and processing versatility sustain its dominant position across the broad market.

Technology Insights

Thermoplastic hot melts constitute the leading technology segment, commanding approximately 48% of market share in 2025. Thermoplastic hot melt adhesives, which soften upon heating, bond rapidly upon cooling, and can be remelted, represent the most widely deployed adhesive technology across packaging, woodworking, bookbinding, and general industrial assembly applications. Their dominance is rooted in a combination of mature application infrastructure, broad substrate compatibility, well-understood performance characteristics, and favorable economics relative to reactive or pressure-sensitive alternatives. Global packaging lines, particularly in food and beverage, consumer goods, and e-commerce fulfillment, are extensively equipped with thermoplastic hot melt dispensing systems from suppliers such as ITW Performance Polymers. The segment’s installed base advantage, supported by an enormous base of compatible dispensing equipment and formulation expertise accumulated over decades, creates substantial switching cost barriers that reinforce technology leadership through the forecast horizon.

Industry Insights

Packaging is the dominant Industry segment within the Hot Melt Adhesive market, representing approximately 35% of global market share in 2025. The packaging segment’s supremacy reflects hot melt adhesives’ fundamental role in primary, secondary, and tertiary packaging operations, encompassing case and carton sealing, tray forming, label application, flexible packaging lamination, and void fill bonding across food and beverage, consumer products, pharmaceutical, and industrial goods sectors. According to the World Packaging Organisation (WPO), the global packaging industry processes billions of packaging units daily, with adhesive bonding involved at multiple production stages across virtually all format types. The structural growth of organized retail, e-commerce fulfillment, and processed food consumption in emerging markets is sustaining packaging volume expansion. HB Fuller Company and Henkel AG & Co. KGaA maintain particularly strong positions in packaging adhesive formulations, offering specialized product lines for food-safe, high-speed automated packaging environments.

Distribution Channel Insights

OEM (Original Equipment Manufacturer) is the leading distribution channel within the Hot Melt Adhesive market, accounting for approximately 52% of market share in 2025. The OEM channel dominates because the bulk of hot melt adhesive consumption occurs within large-scale industrial manufacturing environments, automotive assembly plants, packaging machinery installations, hygiene product manufacturing lines, and woodworking facilities, where adhesives are specified, tested, and purchased directly by manufacturers as an integral input to their production processes. OEM relationships typically involve long-term supply agreements, technical co-development partnerships, and application engineering support, creating high switching costs and sticky customer relationships that favor established adhesive producers. Henkel AG & Co. KGaA, HB Fuller Company, and Jowat SE have developed extensive global OEM sales and technical service networks that enable them to deliver application-specific adhesive solutions and maintain preferred supplier status with major industrial customers across target end-use industries.

Regional Insights

North America Hot Melt Adhesive Market Trends and Insights

North America represents a mature and technologically sophisticated market for hot melt adhesives, characterized by strong end-use demand across packaging, automotive, nonwoven hygiene, and woodworking industries. The United States is the region’s primary market, benefiting from a highly developed manufacturing base, robust e-commerce-driven packaging growth, and an active regulatory environment that is accelerating the transition away from solvent-based adhesives. The U.S. EPA’s National Volatile Organic Compound Emission Standards for consumer and industrial products continue to create structural tailwinds for hot melt adhesive adoption as a preferred low-emission bonding technology across regulated application categories.

The North American automotive sector, anchored by major OEM assembly complexes in Michigan, Ohio, Tennessee, and Ontario, Canada, is a significant consumer of reactive and thermoplastic hot melts for interior assembly, underbody sealing, and wire harness applications. Domestic adhesive manufacturers including HB Fuller Company and global leaders such as 3M Company maintain strong regional supply networks and application development capabilities. Investment in bio-based and recyclability-compatible hot melt formulations is increasing within the region, aligned with sustainability commitments made by major consumer goods brands and packaging converters under Extended Producer Responsibility (EPR) legislation frameworks.

Europe Hot Melt Adhesive Market Trends and Insights

Europe is a pivotal market for hot melt adhesives, driven by the region’s world-class manufacturing industries, stringent environmental regulations, and progressive sustainability policy frameworks. Germany leads the European market, supported by its dominant automotive, woodworking, and packaging industries, and hosts key adhesive producers including Henkel AG & Co. KGaA and Jowat SE, both of which maintain global innovation leadership from German R&D centers. The European Chemicals Agency (ECHA) and the broader REACH regulation framework continue to shape adhesive formulation chemistry, effectively restricting certain solvent-based chemistries and incentivizing investment in hot melt alternatives across industrial applications.

The United Kingdom, France, and Italy are significant secondary markets within Europe, each hosting active packaging, hygiene products, and furniture manufacturing sectors that generate consistent hot melt adhesive demand. The EU’s Packaging and Packaging Waste Regulation (PPWR) and Circular Economy Action Plan are accelerating investment in recyclability-compatible adhesive formulations across the region, with major brand owners, particularly in fast-moving consumer goods and e-commerce packaging, placing recyclability compatibility requirements on their adhesive supply chains. Buhnen GmbH & Co. KG and Evonik Industries AG are among the European-headquartered specialists actively developing next-generation sustainable hot melt chemistries aligned with these regulatory transitions.

Asia Pacific Hot Melt Adhesive Market Trends and Insights

Asia Pacific is the largest regional market for hot melt adhesives, commanding approximately 42% of global market share in 2025, and is also positioned as one of the fastest-growing regions through 2033. China is the dominant country market within the region, underpinned by the world’s largest packaging industry, a rapidly expanding automotive and electric vehicle manufacturing base, and a massive nonwoven hygiene products sector. China’s 14th Five-Year Plan explicitly supports advanced manufacturing development, which is driving capital investment in sophisticated adhesive-intensive production facilities across packaging, electronics, and automotive sectors. Global and regional adhesive producers including Nanpow Resins Chemical Group and Adtek Malaysia SDN BHD maintain manufacturing and distribution presences tailored to serve Asia Pacific industrial customers.

India and ASEAN markets, including Vietnam, Indonesia, Thailand, and Malaysia, are emerging as high-velocity growth markets within the region, driven by rapid industrialization, expanding organized retail and e-commerce packaging demand, and the relocation of global manufacturing supply chains to Southeast Asian production hubs. India’s packaging industry, growing at a rate consistently outpacing GDP growth according to the Indian Institute of Packaging (IIP), is a primary demand driver for EVA and polyolefin hot melt adhesives. Japan and South Korea contribute sophisticated demand in electronics assembly and automotive applications, where reactive hot melts and hot melt pressure sensitive adhesives are deployed in precision, high-reliability bonding operations across consumer electronics, semiconductor packaging, and premium automotive interiors.

Competitive Landscape

The global hot melt adhesive market exhibits a moderately consolidated structure, characterized by the dominance of multinational specialty chemical manufacturers alongside a strong presence of regional and application-focused suppliers. Large integrated players benefit from diversified polymer portfolios, vertically integrated raw material sourcing, global production footprints, and strong technical service capabilities. Competitive differentiation is increasingly driven by formulation expertise across EVA, polyolefin, PUR, and pressure-sensitive systems, as well as the ability to support high-speed automated manufacturing lines in packaging, hygiene, automotive, and woodworking industries.

Strategic priorities are shifting toward sustainable chemistry innovation, including bio-based feedstocks, recyclability-compatible adhesives, and low-VOC solutions aligned with tightening environmental regulations. Expansion into high-performance reactive hot melt technologies for automotive lightweighting and electronics assembly is accelerating. Meanwhile, regional specialists compete through customized formulations, faster delivery cycles, cost competitiveness, and strong distributor networks, particularly in emerging Asian and Latin American markets. Competitive intensity is further reinforced by ongoing capacity expansions and targeted acquisitions to strengthen geographic and technological positioning.

Key Developments:

- November, 2025: BioBond Adhesives launched its BioMelt™ plant-based hot melt PSA products for labels, tapes, and industrial markets, offering USDA BioPreferred, PFAS-free, zero-microplastics solutions available for sampling in Q4 2025.

- July, 2025: Tex Year Group launched Asia’s first dedicated compostable hot melt adhesive production line at its Taoyuan facility, unveiling a sustainable materials innovation hub to advance biodegradable adhesive technologies and green manufacturing.

- April, 2025: Henkel launched a new hot melt adhesive specifically for PET bottle labelling, offering improved adhesion performance and processing stability to support lightweight, high-speed beverage packaging applications.

Companies Covered in Hot Melt Adhesive Market

- DOW Inc.

- Arkema S.A.

- Avery Dennison Corporation

- 3M Company

- HB Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- Sika AG

- ITW Performance Polymers

- Nanpow Resins Chemical Group

- Adtek Malaysia SDN BHD

- Buhnen GmbH & Co. KG

- IFS Industries Inc.

- Evonik Industries AG

- Super Bond Adhesive Pvt. Ltd.

- Beardow Adams Ltd.

- Paramelt B.V.

- Tex Year Industries Inc.

- BioBond Adhesives

Frequently Asked Questions

The hot melt adhesive market is valued at US$ 10.1 billion in 2026, growing steadily due to strong demand from packaging, hygiene, automotive, and woodworking industries.

Growth is driven by e-commerce-led packaging demand, automotive lightweight, and regulatory shifts toward low-VOC alternatives to solvent-based adhesives.

Asia Pacific leads with around 42% share, supported by manufacturing expansion in China, India, and Southeast Asia.

Bio-based and recyclability-compatible formulations present major growth opportunities amid tightening packaging sustainability regulations.

Key players include Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, DOW Inc., Arkema S.A., Sika AG, Jowat SE, Evonik Industries AG, and Avery Dennison Corporation.