- Inks, Coatings, Adhesives & Sealants (ICAS)

- PUR Adhesives in Electronics Market

PUR Adhesives in Electronics Market Size, Share, and Growth Forecast 2026 - 2033

PUR Adhesives in Electronics Market by Component Type (Thermal Conductive, Electrically Conductive, UV Curing, and Others), Application (Surface-mount devices, Potting & Encapsulation, Conformal Coatings, and Others), and Regional Analysis 2026 - 2033

PUR Adhesives in Electronics Market Size and Share Analysis

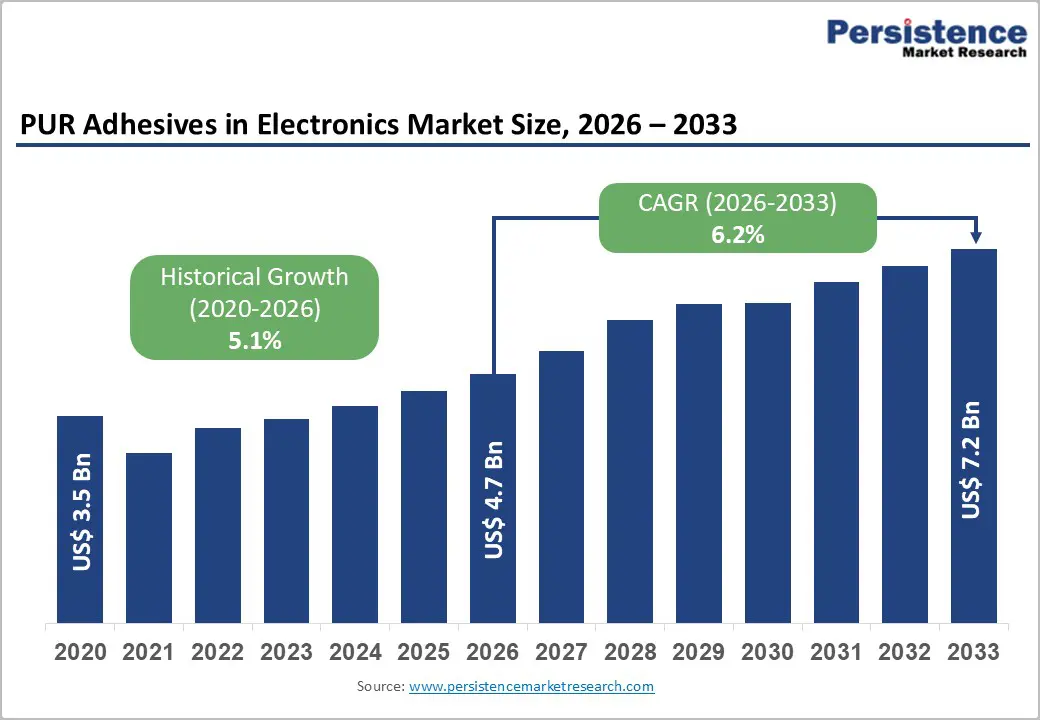

The global PUR Adhesives in Electronics Market size is likely to be valued at US$ 4.7 billion in 2026 and is projected to reach US$ 7.2 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Rising penetration of miniaturized, high-power electronic devices and electric mobility platforms is accelerating the adoption of polyurethane-reactive (PUR) systems that combine structural strength with flexible, low-stress bonding. Demand is further reinforced by regulatory and OEM preferences for low-VOC, solvent-free chemistries, and by the need for thermally and electrically optimized materials for advanced packaging, automotive electronics, and power electronics assemblies.

Key Industry Highlights:

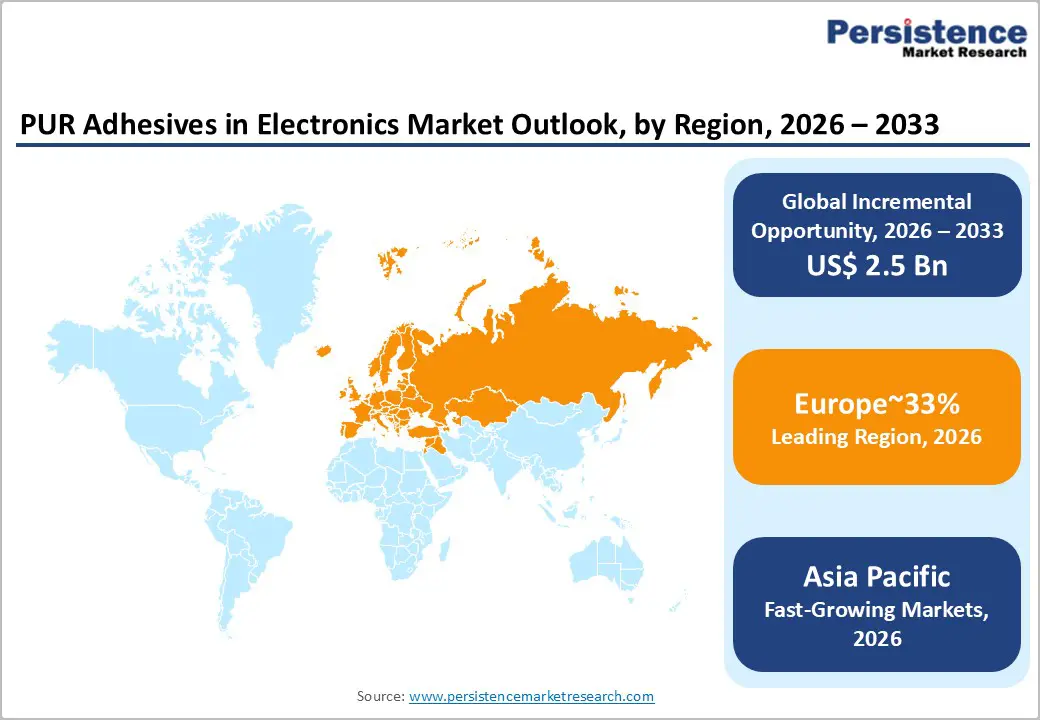

- Leading Region: Europe currently leads the PUR Adhesives in Electronics Market, supported by strong automotive and industrial electronics production, stringent REACH and RoHS regulations favoring solvent-free polyurethane systems, and ambitious decarbonization policies.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, underpinned by its role as the manufacturing hub for consumer electronics and semiconductors, rapid EV adoption in China and ASEAN, and increasing relocation of electronics production to India and Southeast Asia.

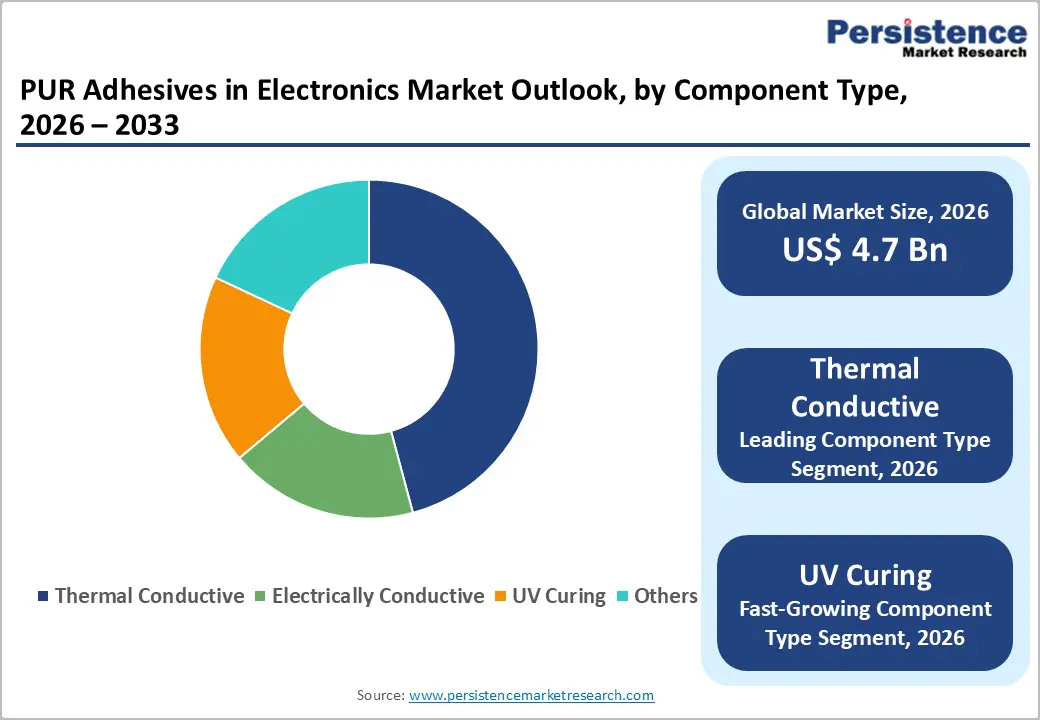

- Dominant Component Type: Among component types, thermal conductive PUR adhesives dominate due to their ability to provide both structural bonding and heat dissipation in power modules, battery packs, and LED drivers, achieving thermal conductivities above 0.8 W/m·K while maintaining electrical insulation and mechanical toughness suitable for automotive and industrial duty cycles.

- Leading Application: Potting & encapsulation is the largest segment, as flexible polyurethane systems offer superior stress relief compared with rigid epoxies, improving reliability of control units, sensors, and inverters exposed to moisture, vibration, and wide temperature swings across automotive, renewable-energy, and industrial markets.

- Key Opportunity: The key market opportunity lies in next-generation thermally conductive and UV/ PUR-hybrid systems for EV power electronics, wearables, and flexible devices, where OEMs seek materials that combine fast cure, reworkability, low VOCs, and robust thermal-mechanical performance, enabling lighter, more compact, and more reliable electronic assemblies.

| Key Insights | Details |

|---|---|

|

PUR Adhesives in Electronics Market Size (2026E) |

US$ 4.7 Bn |

|

Market Value Forecast (2033F) |

US$ 7.2 Bn |

|

Projected Growth CAGR (2026-2033) |

6.2% |

|

Historical Market Growth (2020-2025) |

5.1% |

Market Dynamics

Drivers - Shift Toward High-Power, Miniaturized Electronics Requiring Thermal and Mechanical Reliability

Growing power densities in consumer, automotive, and industrial electronics are a primary demand driver for thermally conductive PUR adhesives, which provide both mechanical fixation and heat dissipation. The International Energy Agency (IEA) estimates that global electricity demand from data centers, AI, and crypto could reach 1,000 TWh by 2026, intensifying focus on reliable power electronics and thermal management at the board and module level. PUR systems filled with thermally conductive but electrically insulating fillers such as aluminum oxide can achieve thermal conductivities above 0.8 W/m·K while maintaining high volume resistivity and mechanical toughness, making them attractive for inverters, battery modules, and LED drivers.

OEMs increasingly specify such materials in design rules to ensure long-term reliability under thermal cycling from 40°C to 125°C, especially in automotive traction inverters and on-board chargers. These adhesives maintain bond integrity after 1,000+ cycles, reducing failure rates in high-reliability applications. Advanced filler dispersion techniques prevent hot spots, ensuring uniform heat spreading across 50-100 W/cm² power densities typical in SiC/GaN modules.

Preference for Low-VOC, Solvent-Free, and Highly Automated Assembly Solutions

Global regulatory frameworks such as EU REACH, RoHS, and regional VOC limits are pushing electronics manufacturers toward cleaner chemistries and higher levels of process automation. PUR hot-melt adhesives offer one-part dispensing, rapid green strength after cooling, and moisture-curing to full structural strength over 24–48 hours, reducing work-in-process time and enabling automated, high-throughput assembly lines. Leading OEMs in consumer electronics and automotive segments now prioritize adhesives that are solvent-free and compatible with jetting or robotic bead application, cutting manual labor and improving consistency.

In practice, manufacturers report cycle-time reductions of 20–30% when replacing two-part systems with one-part PUR for certain bonding and potting steps, while also simplifying inventory and mixing requirements. Jetting speeds exceed 300 mm/s with dot sizes down to 200 µm, enabling 0.1 mm bond lines in smartphone camera modules. Open time flexibility from 30 seconds to 5 minutes accommodates diverse production rhythms without scrap losses.

Restraints - Moisture Sensitivity, Shelf-Life, and Handling Constraints

Their intrinsic sensitivity to ambient moisture, which can cause premature curing, viscosity increase, or foaming if storage and handling are not tightly controlled is one of the key restraints for PUR adhesives in electronics. Many PUR systems require dry nitrogen blanketing, sealed cartridges, or refrigerated storage to maintain shelf life, increasing logistics and inventory costs for electronics OEMs and EMS providers.

Production lines operating in high-humidity regions such as Southeast Asia face additional process control burdens, including desiccant-equipped dispensing equipment and controlled-environment rooms, which raise capital expenditure and operating complexity. Shelf life typically limited to 6-12 months at 5-10°C creates inventory turnover challenges for high-mix, low-volume production. Pot life monitoring adds QC overhead, diverting engineering resources from process optimization.

Competition from Established Epoxy and Silicone Adhesive Technologies

Electronic assembly has long relied on epoxy and silicone chemistries for potting, encapsulation, and structural bonding, and these incumbents remain strong alternatives to PUR. High-temperature epoxies can withstand continuous operating temperatures above 150°C, while silicones provide exceptional flexibility and stability up to 200–250°C, outperforming many PUR systems in extreme environments such as power modules and under-hood automotive electronics.

Existing qualification databases, UL listings, and field performance histories for these chemistries reduce the perceived risk of switching to PUR, particularly in mission-critical aerospace, medical, or high-reliability industrial applications. Re-qualification cycles average 12-18 months with JEDEC and AEC-Q100 testing protocols. Supply chain maturity favors epoxies with 99.9% on-time delivery versus PUR logistical complexities.

Opportunity - Development of Advanced Thermally Conductive and Electrically Insulating PUR Systems for Power Electronics

The rapid electrification of vehicles, renewable energy systems, and industrial drives is creating strong demand for materials that combine thermal conductivity, electrical insulation, and mechanical compliance. Patent literature describes thermally conductive polyurethane adhesive compositions with optimized filler surface treatments that maintain high lap=shear strength and elongation even at high filler loadings, enabling thermal conductivities above 1.0 W/m·K while preserving workable viscosities. These formulations are well suited to bonding power modules to cooling plates, battery modules to thermal interface structures, and high-brightness LED assemblies.

With automotive electronics projected to account for nearly 50% of global electronics-adhesive demand by 2025, suppliers that offer UL-94-rated, flame-retardant PUR systems meeting automotive and IEC standards can capture significant premium opportunities. Hybrid filler systems combining BN, AlN, and graphite achieve anisotropic conductivity up to 5 W/m·K in-plane. Low CTE matching to Si substrates prevents delamination during 200°C reflow soldering.

Expansion in Consumer and Wearable Electronics Through Light-Cure and Hybrid PUR Technologies

Miniaturized form factors in smartphones, wearables, and hearables require thin bond lines, fast curing, and reworkability, an area where light-cure and PUR-hybrid systems provide distinct advantages. Vendors are developing UV-curable PUR adhesives that deliver instant handling strength upon exposure while continuing to moisture-cure for full structural performance, aligning with high-speed assembly lines that operate at cycle times below 5 seconds per unit. These systems can be formulated to remain optically clear for bezel-less displays and camera modules while providing impact resistance and flexibility superior to brittle UV-epoxies.

As global shipments of wearables surpassed 500 million units in 2023, and flexible electronics adoption accelerates, PUR suppliers that tailor low-modulus, skin-safe, and low-outgassing formulations for these applications will access high-growth, design-driven niches within the broader electronics adhesives space. Dual-cure mechanisms enable <1 second tack-free time via 365 nm UV, followed by ambient moisture development over 4-6 hours. Peel strength exceeds 10 N/cm on PI flex circuits after 85°C/85% RH aging, ensuring IP68 sealing integrity.

Category-wise Analysis

Component Type Insights

Within component types, thermal conductive PUR adhesives are emerging as the leading segment, accounting for an estimated 36% share of the PUR adhesives in the electronics market. This dominance is underpinned by their dual role as structural bonds and heat-spreading media in power electronics, LED lighting, automotive batteries, and high-density PCBs. Thermally conductive yet electrically insulating fillers such as aluminum oxide, aluminum hydroxide, and boron nitride enable these systems to dissipate heat from components while maintaining the dielectric strength required by safety standards.

With global electric vehicle sales surpassing 14 million units in 2023 and installed solar PV capacity projected to exceed 5,000 GW by 2030, demand for thermally managed electronic assemblies is surging. As OEMs redesign modules to reduce reliance on mechanical fasteners and thermal pads, integrated thermally conductive PUR adhesives are capturing attach and potting applications previously dominated by silicone or epoxy solutions.

Application Insights

Across application, potting & encapsulation represents the leading segment, holding roughly 41% of market share for PUR adhesives in electronics. Potting compounds based on two-component or hot-melt PUR systems provide robust environmental protection against moisture, vibration, and chemicals while offering lower modulus than epoxies, reducing stress on sensitive components and solder joints. In sectors such as automotive electronics, where control units, sensors, and onboard chargers must endure harsh under-hood conditions, and renewable energy inverters exposed to outdoor environments, PUR encapsulants balance flexibility, adhesion, and thermal performance.

Case studies from inverter and charger manufacturers show field-failure reductions of up to 30% after transitioning from rigid epoxies to flexible PUR potting materials in certain designs, primarily due to improved resistance to thermal cycling and shock. As design trends favor compact, densely populated modules, the stress-relieving properties of PUR encapsulants further support their continued leadership in this application category.

Regional Insights

North America PUR Adhesives in Electronics Market Trends

In North America, particularly the United States, the PUR adhesives in electronics market benefit from a strong innovation ecosystem in semiconductors, automotive electronics, aerospace, and defense. The U.S. CHIPS and Science Act, which earmarks over US$ 52 Bn for domestic semiconductor manufacturing and R&D, is catalyzing investment in advanced packaging and electronic assembly lines that rely on high-performance adhesive technologies, including PUR systems for structural bonding and thermal management. Automotive OEMs and Tier-1 suppliers concentrated in the region are accelerating electrification programs, with electric vehicles representing more than 9% of new light-duty vehicle sales in 2023, creating additional demand for thermally conductive and flame-retardant polyurethane adhesives in battery packs and power electronics.

Regulatory frameworks such as UL 94 flammability classifications and IPC standards for electronic assemblies set stringent performance baselines that PUR suppliers must meet, encouraging continuous material innovation. North American manufacturers also prioritize localized technical support and secure supply chains, favoring suppliers with regional production or application-engineering centers. Companies like Henkel AG & Co. KGaA, 3M, and Dow Chemical Company maintain significant R&D and manufacturing footprints in the region, enabling rapid customization of PUR formulations to customer-specific processes and qualification requirements, reinforcing North America’s role as a technology-leading market.

Europe PUR Adhesives in Electronics Market Trends

Europe represents a technologically advanced and highly regulated market for PUR adhesives in electronics, driven by strong automotive, industrial, and renewable-energy sectors. Countries such as Germany, France, and the U.K. host leading OEMs and Tier-1 suppliers for power electronics, e-mobility, and industrial automation, all of which increasingly utilize thermally conductive PUR adhesives in inverters, drives, and battery systems. The European Union’s Green Deal and Fit for 55 package, targeting at least 55% greenhouse-gas reduction by 2030, accelerates electrification and energy-efficiency investments, indirectly boosting demand for advanced electronic materials, including polyurethane encapsulants and bonding agents.

Regulatory harmonization through REACH, RoHS, and ELV directives favors low-VOC, haloge-free chemistries, positioning PUR systems, often formulated solvent-free, as attractive options compared with legacy materials. Germany serves as a hub for specialty chemical and adhesive innovation, with companies like Sika AG, DELO Industrie Klebstoffe, and Henkel developing PUR technologies tailored to automotive and power electronics. The U.K. and Spain are also expanding renewable-energy and EV infrastructure, driving uptake of thermally conductive and flame-retardant PUR adhesives in grid-connected inverters and charging equipment. As European OEMs push for lifecycle carbon-footprint reductions, there is growing interest in bio-based polyurethane systems and recyclable module designs, offering further opportunities for differentiated PUR adhesive solutions.

Asia Pacific PUR Adhesives in Electronics Market Trends

Asia Pacific is the manufacturing epicenter for consumer electronics, semiconductors, and increasing volumes of electric vehicles, making it the largest and fastest-growing regional market for PUR adhesives in electronics. China, Japan, South Korea, and Taiwan collectively account for the majority of global smartphone, display, and PC production, where PUR-based structural and potting adhesives are used for display modules, camera assemblies, and battery packs. The China Association of Automobile Manufacturers reports EV sales surpassing 9 million units in 2023, intensifying demand for thermally conductive and flame-retardant PUR systems in traction battery and powertrain electronics.

Japan and South Korea lead in advanced semiconductor packaging and automotive electronics, where stringent reliability requirements drive the use of polyurethane encapsulants that manage stress in fine-pitch and flexible circuits. At the same time, India and ASEAN countries (such as Vietnam, Thailand, and Malaysia) are emerging as alternative electronics manufacturing hubs, supported by government incentives like India’s Production-Linked Incentive (PLI) schemes and regional tax benefits. These markets favor cost-effective yet robust adhesive solutions, opening opportunities for regional producers of PUR systems tailored to local climatic conditions and production capabilities. Manufacturers in the Asia Pacific benefit from proximity to key raw-material suppliers and large-scale chemical production, enabling competitive pricing and rapid scaling of new PUR adhesive formulations targeted at global OEMs.

Competitive Landscape

The PUR Adhesives in Electronics Market is moderately consolidated at the top, with a handful of global chemical and adhesive majors accounting for a significant share, alongside specialized regional players focusing on niche formulations and application support. Leading companies such as Henkel AG & Co. KGaA, 3M, Dow Chemical Company, and H.B. Fuller leverage extensive R&D pipelines, global manufacturing footprints, and deep OEM relationships to capture high-value design-in opportunities in automotive, consumer electronics, and industrial electronics.

Differentiation is driven by proprietary polyurethane chemistries, thermally conductive and flame-retardant technologies, and the ability to provide end-to-end technical support, including simulations, reliability testing, and process optimization. Emerging business models include co-development programs with device manufacturers, supply agreements tied to platform lifecycles, and sustainability-oriented solutions such as low-isocyanate or bio-based PUR systems, which align with evolving ESG requirements in major markets.

Key Market Developments

- In February 2024, Henkel AG & Co. KGaA introduced a new generation of thermally conductive polyurethane potting materials for EV onboard chargers and inverters, formulated to meet UL 94 V-0 and automotive OEM reliability standards while enabling reduced module weight and improved thermal cycling performance.

- In June 2024, 3M expanded its Scotch-Weld PUR portfolio for electronics assembly with low-VOC, fast-curing grades optimized for automated dispensing and jetting, targeting smartphone modules and wearable devices requiring thin bond lines and high impact resistance.

- In October 2024, Sika AG announced investment in a new polyurethane adhesive production line in Asia Pacific to support demand from automotive electronics and renewable-energy customers, emphasizing thermally conductive and flame-retardant polyurethanes for inverters and battery systems.

Companies Covered in PUR Adhesives in Electronics Market

- Henkel AG & Co. KGaA

- 3M

- H.B Fuller

- Dow Chemical Company

- Sika AG

- Avery Dennison

- Master Bond Inc.

- Lord Corporation

- Huntsman Corporation

- Permabond

- DELO Industries Adhesives

- Panacol

- ITW Polymers Adhesives

Frequently Asked Questions

By 2033, the PUR Adhesives in Electronics Market is expected to reach approximately US$ 7.2 Bn, up from US$ 4.7 Bn in 2026, reflecting a robust CAGR of 6.2% driven by electrification, miniaturization, and thermal‑management requirements in automotive, industrial, and consumer electronics applications.

Key demand drivers include the shift toward high‑power, compact electronic assemblies requiring thermally conductive yet electrically insulating materials, regulatory and OEM preference for low‑VOC and solvent‑free chemistries, and the need for one‑part, automation‑friendly adhesives.

Thermal conductive PUR adhesives lead the component type segment with an estimated 36% share, as they combine structural bonding with efficient heat dissipation for power electronics, battery modules, and LED drivers, achieving thermal conductivities above 0.8 W/m·K while maintaining electrical insulation and mechanical flexibility.

Europe currently holds the largest regional share, supported by its strong automotive and industrial electronics base, stringent environmental and materials regulations such as REACH and RoHS, and substantial investments in EVs and renewable‑energy infrastructure that demand thermally conductive and flame‑retardant polyurethane adhesives for power electronics and battery systems.

The most attractive opportunity lies in developing advanced thermally conductive and UV/ PUR‑hybrid systems tailored to EV power electronics, flexible and wearable devices, and compact consumer electronics, where manufacturers seek fast‑curing, reworkable, low‑VOC materials that deliver high thermal performance, electrical insulation, and long‑term reliability under severe thermal and mechanical stress.