- Semiconductor Materials & Components

- Smartphones Market

Smartphones Market Size, Share, and Growth Forecast 2026 - 2033

Smartphones Market by Operating System (Android, iOS, Others), Price Range (Low Range, Mid-Range, High Range), Distribution Channel (Online, Offline), and Regional Analysis for 2026-2033

Smartphones Market Size and Trend Analysis

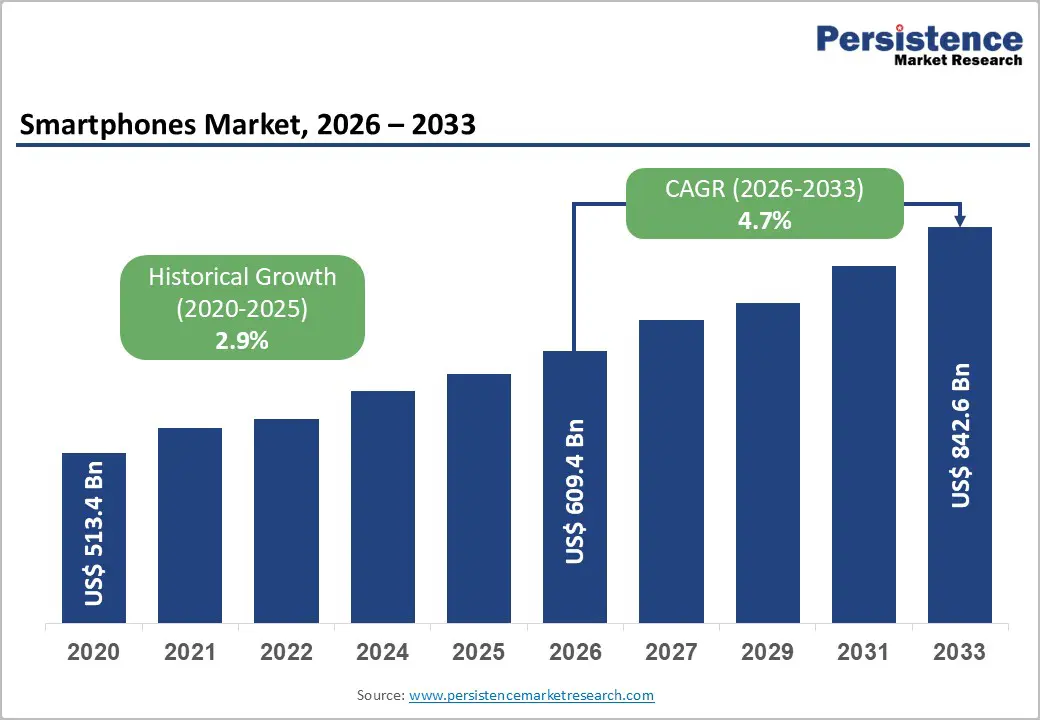

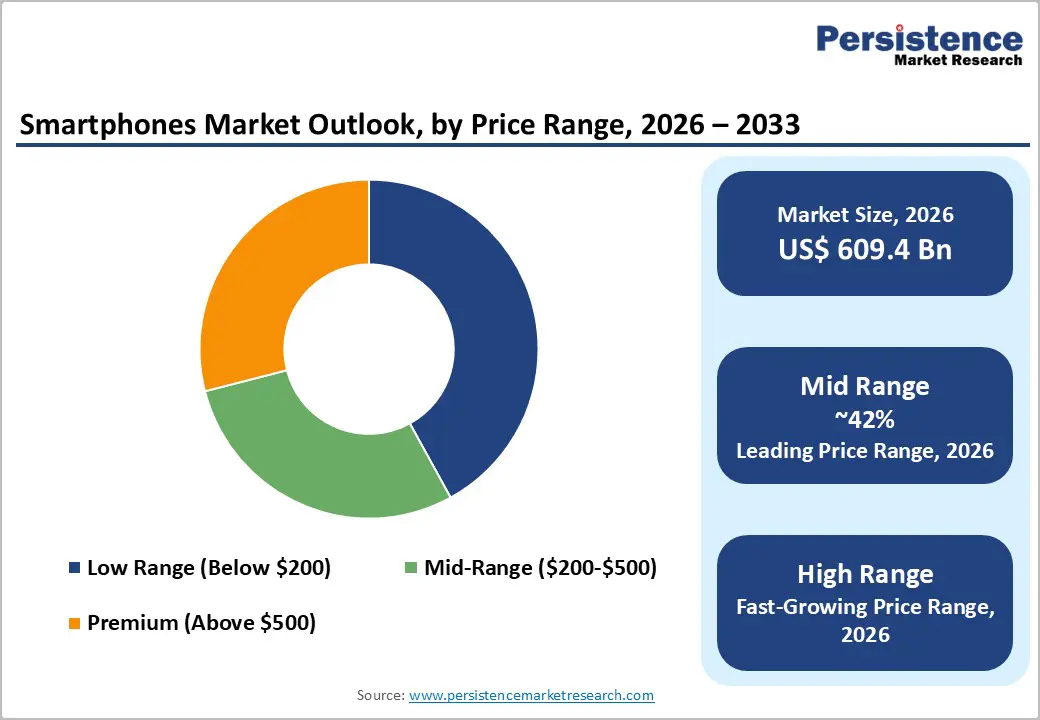

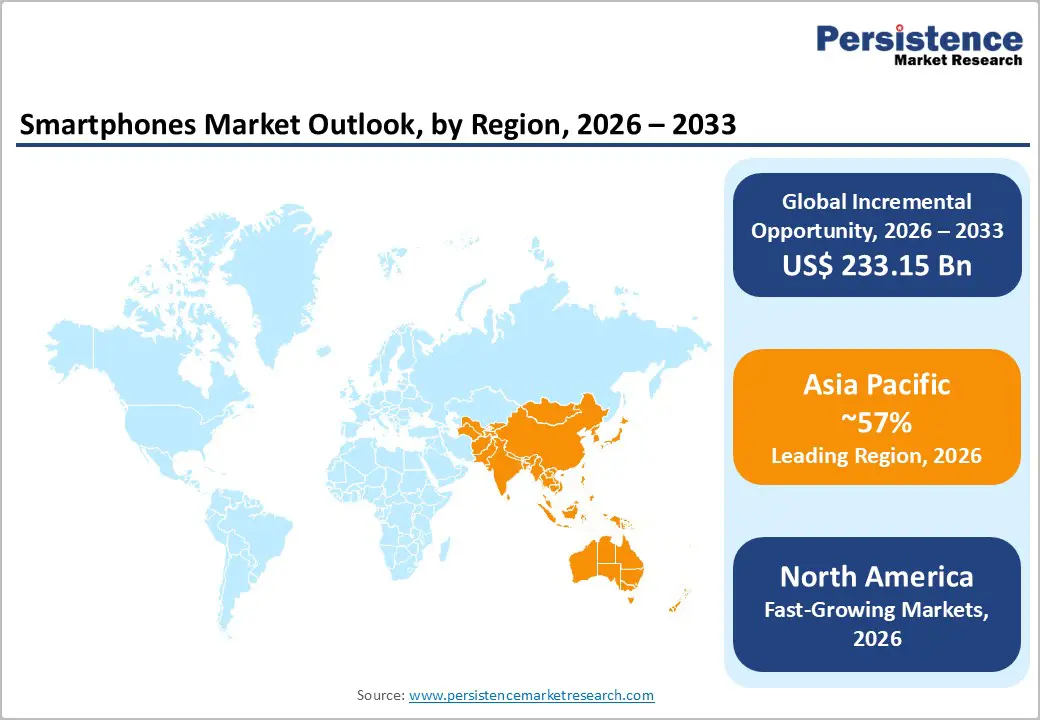

The global Smartphones market size is supposed to be valued at US$ 609.4 Bn in 2026 and is projected to reach US$ 842.5 Bn by 2033, growing at a CAGR of 4.7% between 2026 and 2033.

The smartphone industry continues to expand, driven by technological innovations including 5G network proliferation and artificial intelligence integration, which enhance user experiences across communication, productivity, and entertainment applications. The emergence of advanced camera systems, improved battery technologies, and on-device AI processing capabilities are attracting consumers to upgrade their devices more frequently, particularly in emerging economies where smartphone penetration rates are accelerating alongside rising disposable incomes and expanding digital infrastructure.

Key Market Highlights

- Leading Region: Asia Pacific dominates the global smartphones market with approximately 57% of worldwide shipment volumes in 2024, driven by massive consumer populations in China and India, rapidly expanding middle-class demographics, and established manufacturing ecosystems.

- Fastest Growing Region: North America emerges as the fastest growing market, with the region generating premium revenue concentrations driven by affluent consumer purchasing power and elevated average selling prices exceeding $850-900 for flagship devices.

- Dominant Segment: Android operating system maintains commanding market leadership with approximately 71% global market share in 2025, driven by open-source architecture enabling adoption across diverse price segments, manufacturer flexibility, and prevalence in emerging markets.

- Fastest Growing Segment: Mid-Range smartphones priced between $200-$500 constitute the fastest-growing price segment, capturing approximately 42% market share through strategic positioning balancing advanced features, including multi-lens cameras, high refresh rate displays, and 5G connectivity with accessible pricing.

- Key Market Opportunity: Foldable smartphones and innovative form factors represent high-margin opportunities commanding substantial price premiums, with shipments experiencing double-digit growth rates as production maturity reduces manufacturing defects and component costs decline toward mainstream accessibility.

| Global Market Attributes | Key Insights |

|---|---|

| Smartphones Market Size (2026E) | US$ 609.4 Bn |

| Market Value Forecast (2033F) | US$ 842.5 Bn |

| Projected Growth CAGR (2026-2033) | 4.7% |

| Historical Market Growth (2020-2025) | 2.9% |

Market Dynamics

Market Growth Drivers

5G Network Expansion and Advanced Connectivity Infrastructure

The rapid global deployment of 5G networks serves as a crucial driver for the expansion of the smartphone market, as consumer demand for high-speed connectivity continues to rise, particularly for data-intensive applications. In 2024, 5G devices accounted for more than 52% of total smartphone shipments, surpassing 4G technology just four years after its commercial introduction. This transition is expected to gain momentum, with forecasts indicating that the share of 5G smartphones will exceed 70% by 2027, as telecommunications operators systematically retire legacy network infrastructure.

The incorporation of 5G chipsets into mid-range and entry-level devices, achieved without eroding manufacturer profit margins, has broadened access to advanced connectivity. This development has facilitated innovations such as cloud gaming, augmented reality, and real-time video streaming, capabilities that were once limited to premium devices, thereby invigorating replacement cycles across a wide range of consumer demographics.

Artificial Intelligence Integration Enhancing User Experience

The integration of generative AI capabilities directly into smartphone hardware architecture is fundamentally reshaping consumer expectations and enhancing device functionality across several key areas, including photography, communication, and productivity. Industry projections suggest that by 2027, over 1 billion smartphones equipped with generative AI features will be shipped, marking a significant transition from cloud-based processing to on-device intelligence, facilitated by advanced chipsets such as MediaTek's Dimensity 9300 and Qualcomm's Snapdragon 8 Gen 3.

Prominent manufacturers, including Samsung, Google, and Apple, are focusing on AI-enhanced features such as object removal in images, real-time language translation, intelligent message composition, and predictive user behavior analysis. These advancements not only set premium offerings apart but are also increasingly accessible within mid-range segments, encouraging consumers to upgrade their devices. This evolution allows users to benefit from enhanced computational photography, voice-activated assistance, and personalized content curation, ultimately improving their daily digital interactions.

Market Restraints

Market Saturation in Developed Economies

The smartphone markets in developed regions, particularly in North America and Western Europe, are encountering notable growth constraints due to high penetration rates that exceed 85% and extended device replacement cycles. Consumers in these mature markets are increasingly retaining their smartphones for longer periods, typically averaging 3 to 4 years. This trend is largely attributed to incremental technological advancements that often do not justify frequent upgrades, especially given that devices continue to receive timely software updates and maintain sufficient performance for everyday tasks.

The decreasing novelty associated with successive generations of smartphone releases, coupled with rising average selling prices for flagship models, has further discouraged premature replacements. As a result, unit shipment growth rates are being compressed even though revenue continues to expand, driven by premiumization trends among existing users who prioritize quality over the frequency of upgrades.

Supply Chain Vulnerabilities and Component Shortages

The smartphone manufacturing ecosystem is highly vulnerable to supply chain disruptions that impact critical components such as semiconductors, display panels, and battery materials. These disruptions can significantly constrain production capacity and increase manufacturing costs. Geopolitical tensions, export restrictions on advanced chipset technologies, and the concentration of production facilities in specific geographic regions contribute to this vulnerability, leading to localized disruptions that can have widespread effects on global supply networks.

Periodically, component shortages compel manufacturers to prioritize the production of flagship models, which limits the availability of more affordable devices in price-sensitive emerging markets. Furthermore, rising raw material costs for lithium batteries and rare earth elements essential for camera sensors and processors are compressing profit margins. This situation is particularly challenging for smaller brands that struggle to achieve economies of scale comparable to industry leaders.

Market Opportunities

Emerging Market Expansion in Asia Pacific and Africa

The emerging consumer markets in developing regions, particularly in India, Southeast Asia, and Sub-Saharan Africa, present significant opportunities for growth, as smartphone penetration remains below 65% in many countries despite advancements in telecommunications infrastructure. Government initiatives aimed at digitization, the expansion of 4G and 5G networks in rural areas, and the increasing availability of affordable devices priced under $200 are driving first-time smartphone adoption among hundreds of millions of potential users.

India's smartphone market exemplifies this potential, with government production-linked incentive schemes attracting investments in manufacturing that help reduce import duties and enhance the local availability of competitively priced devices. Manufacturers focusing on tailored feature sets, including regional language support, optimized battery performance for areas with inconsistent power supply, and durable construction suitable for diverse environmental conditions, are well-positioned to capture significant market share in these high-growth demographics. In these regions, smartphone ownership increasingly reflects economic participation and social connectivity.

Premium Segment Growth Through Foldable and Innovative Form Factors

The emergence of foldable smartphones and innovative form factors presents a significant high-margin opportunity for manufacturers to stimulate replacement demand within saturated premium segments while maintaining elevated price points. Samsung has established leadership in this domain through its Galaxy Z Fold and Z Flip series, with the Galaxy Z Fold 7 achieving notable success in 2025.

The shipments of foldable devices are growing at double-digit rates as production processes mature, reducing defects and lowering component costs, thereby expanding accessibility beyond ultra-premium tiers. Companies investing in advanced hinge mechanisms, flexible display technologies, and optimized multi-screen software experiences are well-positioned to secure competitive advantages. Additionally, Apple’s potential entry into the foldable category could legitimize the form factor among mainstream consumers, significantly enlarging the addressable market.

Category-wise Insights

Operating System Analysis

Android continues to dominate the global smartphone market, holding approximately 71% share in 2025. This leadership is primarily attributed to its open-source architecture, which facilitates adoption across diverse price segments and manufacturer portfolios. The platform’s flexibility enables leading brands such as Samsung, Xiaomi, Oppo, and Vivo, along with numerous regional players, to customize user interfaces while ensuring compatibility through Google Play Services. Android’s presence is particularly strong in price-sensitive regions across Asia, Africa, and Latin America, where devices under $300 account for the majority of sales.

Conversely, iOS secures around 29% market share exclusively through Apple devices, generating disproportionate revenue via premium pricing strategies with average selling prices exceeding $850. Apple’s ecosystem achieves exceptional user retention near 95%, supported by seamless integration, prioritized updates, and proprietary Apple Silicon architecture delivering superior efficiency and performance.

Price Range Analysis

The mid-range smartphone segment, priced between $200 and $500, represents the fastest-growing category, accounting for approximately 42% of global market share. This growth is driven by a strategic positioning that combines advanced features with affordability for mainstream consumers. The segment benefits from technology cascading from flagship models, including multi-lens cameras with AI-enhanced photography, high-refresh-rate displays exceeding 90Hz, rapid charging above 65W, and robust processing power for gaming and multitasking.

Leading manufacturers such as Xiaomi, Oppo, Realme, and Samsung compete aggressively in this space, leveraging economies of scale to maintain profitability while compressing price points. This category appeals to budget-conscious buyers in emerging markets and value-driven consumers in developed regions. Pricing between $300 and $400 offers an optimal balance, delivering 5G connectivity, capable cameras, and multi-year software support.

Distribution Channel Analysis

Offline distribution channels have regained prominence, accounting for nearly 63% of global smartphone sales and reversing prior trends favoring online platforms. This resurgence reflects manufacturers’ recognition of the strategic value of physical touchpoints, particularly for premium products and consumers in smaller cities. The sustained growth in offline shipments for eight consecutive months, while online deliveries declined for seven months, was driven by brands expanding retail presence beyond e-commerce.

Offline stores offer distinct advantages, including hands-on product evaluation, immediate availability, reliable after-sales service, and paper-based financing options critical in regions with limited credit penetration. Leading brands such as Xiaomi and Motorola, once reliant on online channels, are now investing in Moto Hubs and branded experience centers across Tier 2 and Tier 3 cities to influence purchase decisions.

Regional Insights

North America Smartphones Market Trends

North America exhibits a distinct market profile dominated by iOS, with Apple commanding nearly 58% of regional smartphone share, well above global averages, driven by strong brand loyalty, carrier partnerships, and consumer preference for integrated ecosystems. The United States leads this growth, supported by high disposable incomes exceeding $70,000 annually, advanced telecommunications infrastructure with nationwide 5G coverage, and a cultural inclination toward premium technology.

Major carriers such as Verizon, AT&T, and T-Mobile facilitate access to flagship devices priced above $1,000 through installment plans, reducing upfront costs. Innovation hubs like Silicon Valley accelerate the adoption of emerging features, including AI-powered photography, augmented reality, and biometric security. Regulatory emphasis on privacy and sustainability further shapes design priorities, while market maturity sustains a projected CAGR of 7.5% through 2034, driven by premiumization over volume expansion.

Europe Smartphones Market Trends

Europe demonstrates varied smartphone adoption patterns across its member states, with Android maintaining a dominant 66% market share, reflecting consumer preferences for device diversity, competitive pricing, and flexibility across economic segments. Key markets such as Germany, the United Kingdom, France, and Spain exhibit sophisticated consumer behavior, prioritizing build quality, camera performance, and long-term software support. Germany, in particular, emphasizes technical specifications and brand reputation, favoring Samsung, Apple, and increasingly Google Pixel devices offering extended update cycles.

Regulatory frameworks under EU directives, including the Digital Markets Act and Digital Services Act, significantly shape market strategies through interoperability mandates, alternative app store provisions, and standardized USB-C charging requirements. Sustainability initiatives and right-to-repair legislation further encourage longer device lifespans, while growing environmental awareness drives demand for refurbished devices and trade-in programs.

Asia Pacific Smartphones Market Trends

Asia Pacific remains the dominant force in global smartphone markets, accounting for nearly 57% of worldwide shipments in 2024. This leadership is driven by vast consumer bases in China and India, a rapidly expanding middle class, and well-established manufacturing ecosystems. China serves as both the largest market and primary production hub, hosting leading domestic brands such as Xiaomi, Oppo, Vivo, and Huawei, alongside global assemblers like Foxconn.

Chinese manufacturers have achieved technological parity with global competitors through significant R&D investments in camera systems, fast-charging solutions, and display innovations, while leveraging integrated supply chains for cost efficiency. India, the fastest-growing major market, is projected to achieve a 7.32% CAGR through 2035, supported by government PLI schemes, rural broadband expansion, and rising first-time smartphone adoption across underserved regions.

Competitive Landscape

Market Structure Analysis

The global smartphone market reflects moderate concentration, with the top five manufacturers, Samsung, Apple, Xiaomi, Oppo, and Vivo, collectively accounting for nearly 81% of worldwide shipments in 2024, underscoring oligopolistic dynamics. Market leaders capitalize on economies of scale, robust distribution networks, and substantial R&D investments to maintain a competitive advantage. Samsung secures leadership through a diversified portfolio spanning entry-level devices under $150 to ultra-premium foldable models priced above $1,800, ensuring global reach across all segments. Apple leverages vertical integration, combining proprietary silicon, operating system control, and a monetized services ecosystem to generate recurring revenue streams. Chinese brands pursue aggressive international expansion to offset domestic saturation, targeting emerging regions with competitively priced devices featuring flagship-level specifications. Differentiation increasingly emphasizes software-driven intelligence, complemented by service-based models such as cloud storage, extended warranties, and trade-in programs.

Key Market Developments

- January 2025: Samsung launched the Galaxy S25 series featuring advanced AI integration and improved battery efficiency, receiving strong market reception and helping maintain 20% premium smartphone market share globally.

- September 2025: Google achieved recognition as a top five premium smartphone vendor in the first half of 2025 by doubling its global premium device sales compared to the same period in 2024, driven by Pixel 9 series success.

- July 2025: Samsung introduced the Galaxy Z Fold 7 with significant hardware improvements, including enhanced hinge durability and expanded screen real estate, solidifying leadership in the foldable smartphone segment and addressing previous generation concerns.

Top Companies in the Smartphones Market

Samsung Electronics (Seoul, South Korea) maintains global market leadership through diversified product portfolio spanning all price segments, early 5G chipset access via its internal semiconductor division, and innovation in foldable form factors, including the commercially successful Galaxy Z series. The company's vertical integration across display manufacturing, memory chips, and camera sensors provides cost advantages and supply chain resilience, while extensive offline distribution networks across 160+ countries ensure market access.

Apple Inc. (Cupertino, U.S.) commands premium market dominance through proprietary Apple Silicon architecture delivering industry-leading performance efficiency, a tightly integrated iOS ecosystem generating 95% user retention rates, and services revenue exceeding $85 billion annually from App Store, iCloud, and subscription offerings. The company's brand equity supports premium pricing strategies with average selling prices above $850, generating disproportionate profit share exceeding 75% of total industry profits despite 19% unit market share.

Xiaomi Corporation (Beijing, China) has established itself as a leading value-focused brand capturing significant market share in Asia, Europe, and emerging markets through aggressive pricing strategies, rapid feature innovation, and an extensive product portfolio, including flagship Mi series and budget-oriented Redmi lineup. The company's international expansion accelerated through Latin America and Eastern Europe entry, while an integrated IoT ecosystem, including smart home devices, creates platform effects encouraging Android smartphone adoption within Xiaomi's hardware environment.

Companies Covered in Smartphones Market

- Samsung

- Apple

- Xiaomi

Frequently Asked Questions

The global smartphones market is projected to reach US$ 842.5 Bn by 2033, growing from US$ 609.4 Bn in 2026 at a CAGR of 4.7% during the forecast period.

The primary growth drivers include rapid 5G network expansion, with over 52% of shipments being 5G-enabled in 2024, artificial intelligence integration enabling advanced photography and user experience features, and expanding smartphone adoption in emerging markets driven by affordable devices and improving telecommunications infrastructure.

Android maintains dominant market leadership with approximately 71% global market share in 2025, driven by its open-source architecture enabling adoption across diverse price segments and manufacturer flexibility. iOS holds approximately 29% market share but generates disproportionate revenue through premium pricing.

Asia Pacific dominates the global smartphone market, accounting for approximately 57% of worldwide shipment volumes in 2024. This leadership is driven by massive consumer populations in China and India, rapidly expanding middle-class demographics, established manufacturing ecosystems, and accelerating first-time smartphone adoption in rural areas.

Key opportunities include emerging market expansion in Asia Pacific and Africa where smartphone penetration remains below 65%, and premium segment growth through foldable smartphones and innovative form factors that command substantial price premiums. Additionally, AI-powered features and 5G-enabled applications present opportunities for device differentiation.

Key market players include Samsung Electronics, Apple Inc., Xiaomi Corporation, Oppo Electronics, Vivo Mobile, Google (Pixel), Motorola Mobility, OnePlus Technology, Huawei Technologies, and Realme. Samsung and Apple collectively control significant market share, with top five manufacturers accounting for approximately 81% of global shipments.