- Executive Summary

- Global Lamination Adhesives Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Food & Beverage Industry Overview

- Global Packaging Industry Overview

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 - 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Lamination Adhesives Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Global Lamination Adhesives Market Outlook: Resin

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Resin, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Resin, 2026-2033

- Acrylic

- Polyurethane

- Others

- Market Attractiveness Analysis: Resin

- Global Lamination Adhesives Market Outlook: Technology

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Technology, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Technology, 2026-2033

- Solvent-based

- Water-based

- Solvent-less

- Market Attractiveness Analysis: Technology

- Global Lamination Adhesives Market Outlook: End-use

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by End-use, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use, 2026-2033

- Packaging

- Automobile & Transportation

- Industrial

- Market Attractiveness Analysis: End-use

- Global Lamination Adhesives Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Lamination Adhesives Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Resin, 2026-2033

- Acrylic

- Polyurethane

- Others

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by Technology, 2026-2033

- Solvent-based

- Water-based

- Solvent-less

- North America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use, 2026-2033

- Packaging

- Automobile & Transportation

- Industrial

- Europe Lamination Adhesives Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Resin, 2026-2033

- Acrylic

- Polyurethane

- Others

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by Technology, 2026-2033

- Solvent-based

- Water-based

- Solvent-less

- Europe Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use, 2026-2033

- Packaging

- Automobile & Transportation

- Industrial

- East Asia Lamination Adhesives Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Resin, 2026-2033

- Acrylic

- Polyurethane

- Others

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by Technology, 2026-2033

- Solvent-based

- Water-based

- Solvent-less

- East Asia Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use, 2026-2033

- Packaging

- Automobile & Transportation

- Industrial

- South Asia & Oceania Lamination Adhesives Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Resin, 2026-2033

- Acrylic

- Polyurethane

- Others

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by Technology, 2026-2033

- Solvent-based

- Water-based

- Solvent-less

- South Asia & Oceania Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use, 2026-2033

- Packaging

- Automobile & Transportation

- Industrial

- Latin America Lamination Adhesives Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Resin, 2026-2033

- Acrylic

- Polyurethane

- Others

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by Technology, 2026-2033

- Solvent-based

- Water-based

- Solvent-less

- Latin America Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use, 2026-2033

- Packaging

- Automobile & Transportation

- Industrial

- Middle East & Africa Lamination Adhesives Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Resin, 2026-2033

- Acrylic

- Polyurethane

- Others

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by Technology, 2026-2033

- Solvent-based

- Water-based

- Solvent-less

- Middle East & Africa Market Size (US$ Bn) and Volume (Tons) Forecast, by End-use, 2026-2033

- Packaging

- Automobile & Transportation

- Industrial

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Henkel AG

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- 3M

- H.B. Fuller

- The Dow Chemical Company

- Arkema S.A.

- Sika AG

- DIC Corporation

- Pidilite Industries

- Flint Group

- Ashland Inc.

- Coim Group

- Henkel AG

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Non-food Packaging

- Lamination Adhesives Market

Lamination Adhesives Market Size, Share, and Growth Forecast 2026 - 2033

Lamination Adhesives Market by Resin (Acrylic, Polyurethane, Others), Technology (Solvent-based, Water-based, Solvent-less), Industry (Packaging, Automobile & Transportation, Industrial), and Regional Analysis for 2026 - 2033

Lamination Adhesives Market Size and Trend Analysis

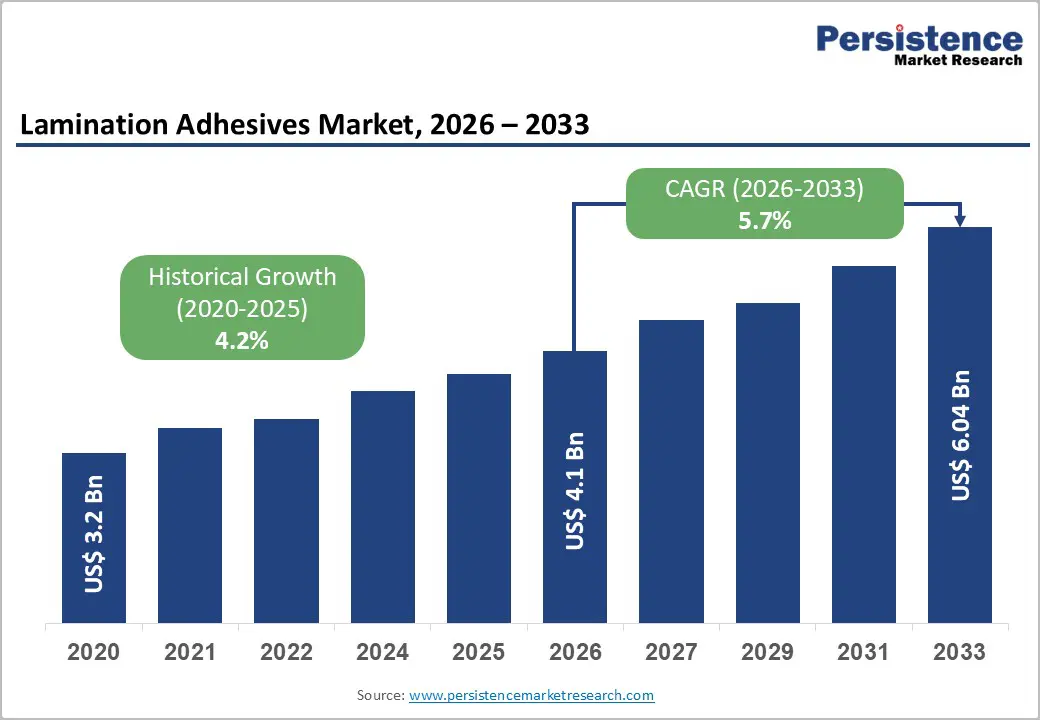

The global lamination adhesives market size is supposed to be valued at US$ 4.1 billion in 2026 and is projected to reach US$ 6.0 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033. The exponential rise in demand for flexible packaging across the food and beverage packaging market, coupled with the surging adoption of laminated materials in e-commerce packaging, driven by major platforms including Amazon and Alibaba, has encouraged the need for lamination adhesives.

The market expansion is primarily driven by the accelerating shift from rigid to flexible packaging formats across the food and beverage packaging industry, where multilayer film structures demand superior barrier protection and extended shelf life. Additionally, stringent environmental regulations, particularly in Europe and North America, are propelling the adoption of low-VOC and solvent-less adhesive technologies, with water-based adhesive adoption increasing by 15% annually as manufacturers align with EPA and REACH compliance standards.

Key Industry Highlights:

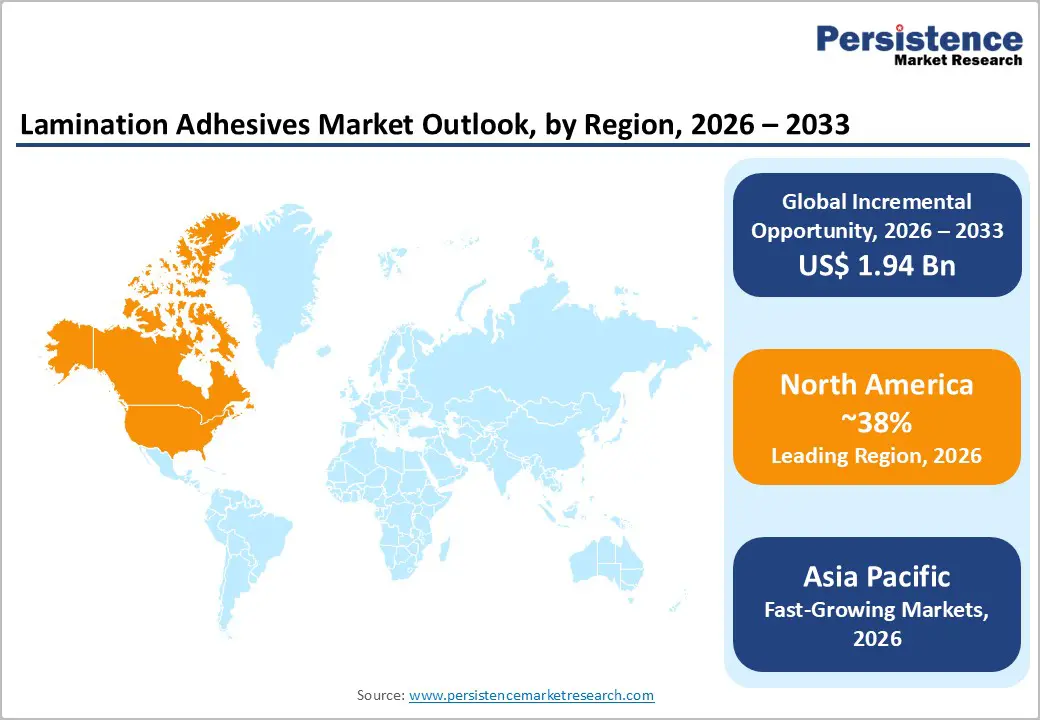

- Regional Leader: North America maintains a dominant market position, with 38% market share, characterized by innovation leadership, stringent regulatory frameworks including EPA and FDA approvals, and premium pricing for advanced laminating adhesive technologies.

- Fastest Growing Region: Asia-Pacific represents the fastest-growing region, driven by rapid industrialization, urbanization, e-commerce expansion anchored by platforms including Amazon and Alibaba, and manufacturing concentration in China, India, and Japan.

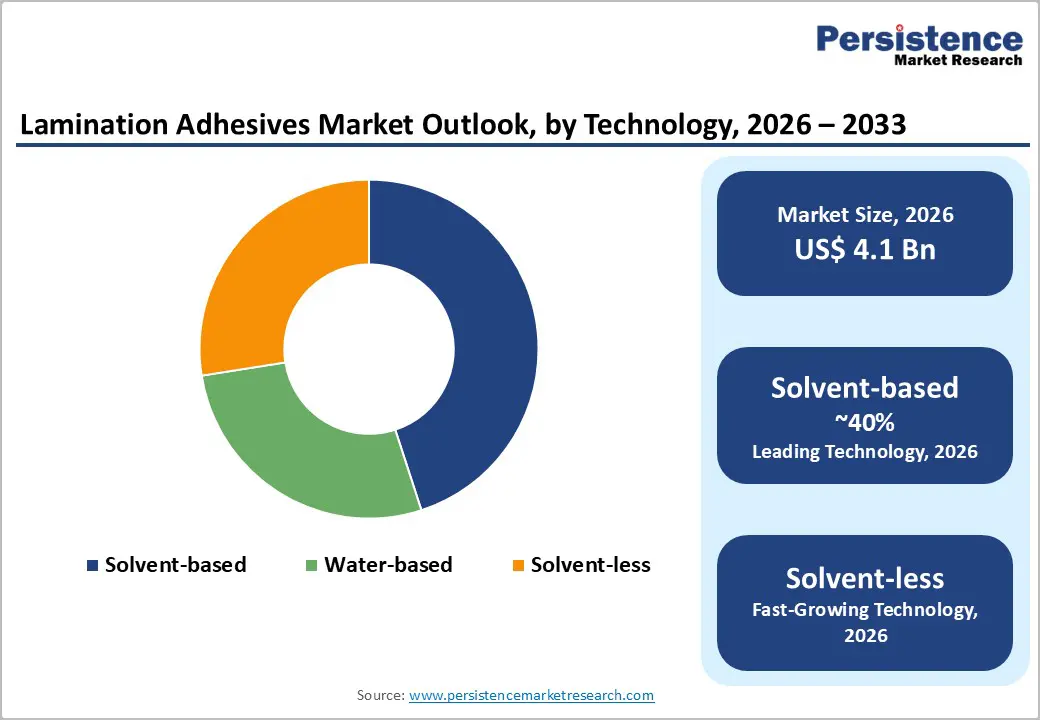

- Leading Segment: Solvent-based laminating adhesives currently hold a leading position with approximately 45% market share, supported by established manufacturing infrastructure, proven performance, and cost-effectiveness for high-volume production.

- Fastest Growing Segment: Solvent-less laminating adhesives represent the fastest-growing technology segment, driven by energy efficiency advantages, environmental regulatory compliance benefits, high-speed production line compatibility, and industry transition toward sustainable packaging solutions aligned with circular economy principles.

- Key Opportunity: Sustainable packaging and biodegradable adhesive solutions represent the most significant long-term market opportunity, supported by regulatory mandates for recyclable packaging by 2030.

| Key Insights | Details |

|---|---|

| Lamination Adhesives Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 6.0 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.7% |

| Historical Market Growth (2020 - 2025) | 4.2% |

Market Dynamics

Drivers - Accelerating Demand from Flexible Packaging and E-Commerce Expansion

The rapid expansion of global e-commerce, particularly in the Asia-Pacific region, has significantly reshaped packaging requirements, compelling companies to adopt durable, lightweight, and cost-efficient solutions for direct-to-consumer delivery. The Flexible Packaging Association reports sustained growth in flexible packaging due to its superior space efficiency and enhanced product protection during transit. Laminating adhesives are essential to this process, enabling the bonding of multiple substrates, such as polyethylene, polypropylene, polyester, and aluminum foil, into high-barrier structures that prevent the ingress of moisture and oxygen.

The food and beverage sector shows particularly strong demand for FDA-approved adhesives capable of maintaining integrity under extreme conditions, including hot-fill and boil-in-bag applications. Multilayer laminate structures utilizing polyurethane and acrylic-based adhesives provide critical barrier properties against moisture, oxygen, and light, thereby extending product shelf life and maintaining food safety standards. The rising consumption of ready-to-eat meals, convenience foods, and single-serve packaging formats, particularly in urbanized regions, is intensifying the need for high-performance laminating adhesives that can withstand retort sterilization processes at elevated temperatures and pressures.

Regulatory Compliance and Sustainability Mandates Driving Technological Innovation

Stringent environmental regulations, including the EU’s REACH framework, Clean Air Act VOC standards, and regional emission controls, are driving adhesive manufacturers to transition toward water-based and solvent-free technologies. The EU Packaging and Packaging Waste Regulation (PPWR) mandates full recyclability of packaging by 2030 and sets strict targets for recycled content, compelling the development of formulations aligned with circular economy principles.

In July 2025, Henkel AG introduced its Loctite Liofol LA 7837/LA 6265 solvent-free system for retort packaging, eliminating energy-intensive drying and reducing CO2 emissions. Similarly, 3M launched advanced solvent-free adhesives with UV-curable technology, enabling rapid curing and strong substrate bonding. These innovations address VOC reduction targets of up to 85% while improving operational efficiency. Manufacturers achieving commercial-scale water-based formulations report cost savings through reduced solvent disposal and enhanced workplace safety.

Restraints- Volatility in Raw Material Costs and Supply Chain Disruptions

The lamination adhesives market is highly vulnerable to fluctuations in raw material costs, particularly for polyol and isocyanate derivatives used in polyurethane formulations, as well as for petroleum-based solvents in traditional systems. Historical trends indicate ethylene prices can vary by 10 to15% in response to global oil price movements, creating unpredictable production costs that compress margins and necessitate frequent price adjustments.

Geopolitical tensions and persistent supply chain disruptions further constrain availability and elevate procurement costs for key chemical precursors sourced from China, Europe, and North America. These pressures disproportionately affect smaller manufacturers that lack vertical integration or long-term contracts, thereby reducing their competitiveness. Additionally, growing demand for alternative feedstocks and bio-based components to meet sustainability mandates introduces formulation complexity and escalates research and development expenses, further straining profitability in price-sensitive market segments.

Regulatory Complexity and Compliance Costs Impeding Market Entry

Adhesive manufacturers face increasing regulatory complexity across global markets, driven by frameworks such as the EU’s REACH regulation, U.S. EPA VOC emission standards, California Proposition 65, and emerging chemical restrictions in China. Compliance with these fragmented regulations requires significant R&D investment to reformulate products, adapt manufacturing processes, and conduct extensive testing to meet jurisdiction-specific requirements. For instance, Henkel AG increased R&D spending by 20% to develop VOC-compliant laminating adhesives in response to tightening European standards. Approval timelines for new formulations often extend 18 to 24 months, delaying product launches and creating competitive disadvantages.

Smaller regional players struggle to absorb compliance costs, favoring established companies like Henkel, Arkema, and 3M. Additionally, California’s Proposition 65 listing of vinyl acetate, effective December 2025, further escalates labeling and reformulation expenses, while the lack of regulatory harmonization prolongs time-to-market for innovative technologies.

Opportunities - Acceleration of Sustainable Packaging and Circular Economy Adoption

The global shift toward circular economy principles and extended producer responsibility (EPR) frameworks is creating significant opportunities for manufacturers of biodegradable and compostable lamination adhesives. Under the European Commission’s Circular Economy Strategy, all plastic packaging must be recyclable or reusable by 2030, compelling converters and brand owners to adopt sustainable adhesive solutions. The 2024 introduction of Tecbond 214B, the first fully certified biodegradable hot-melt adhesive with 45% biobased content and compliance with ASTM D6400 and EN 13432, demonstrates the commercial viability of advanced, eco-friendly technologies.

Biodegradable laminating adhesives enable mono-material packaging designs that enhance recyclability and support industrial composting, aligning with ESG commitments and Scope 3 emission-reduction targets. Companies investing in sustainable adhesive portfolios are well-positioned to secure premium contracts with environmentally conscious brands and achieve long-term growth through regulatory leadership and competitive differentiation.

Expansion in Lightweight Vehicle Manufacturing

The global automotive industry’s transition toward electric vehicles and lightweight composite structures is driving significant demand for advanced laminating adhesives. These adhesives enable reliable bonding of materials such as carbon fiber-reinforced polymers, aluminum composites, and thermoplastic laminates, which are essential for reducing vehicle weight without compromising safety. According to the U.S. Department of Energy, a 10% reduction in vehicle weight can improve fuel efficiency by 6 to 8%, creating strong regulatory and consumer incentives for adoption.

Laminating adhesives support multi-material construction while ensuring structural integrity, thermal stability, and crash resistance required by automotive standards. Leading manufacturers, including H.B. Fuller, Sika AG, and The Dow Chemical Company, are developing formulations with enhanced thermal and chemical resistance to meet assembly line requirements. This opportunity is particularly pronounced in the Asia-Pacific region, where concentrated automotive production in China, India, and Japan is fueling regional demand.

Category-wise Analysis

Resin Insights

Polyurethane resins hold a dominant position in the lamination adhesives market, accounting for approximately 47% of the total share. This leadership is attributed to their superior flexibility, strong interfacial adhesion, and compatibility with diverse substrates, including PET, PP, and aluminum foil. Polyurethane adhesives deliver exceptional performance in demanding applications, including hot-fill food packaging, pharmaceutical laminates, and industrial thermal insulation, supported by rapid curing and high glass transition temperatures that ensure efficiency under extreme conditions. Their market strength reflects long-standing supply relationships, broad regulatory approvals across major regions, and ongoing innovation in low-VOC and solvent-free formulations.

Meanwhile, acrylic-based adhesives are gaining traction, expanding at a CAGR of 7.9% through 2033, driven by excellent transparency, UV resistance, and adhesion to challenging substrates, making them ideal for premium packaging and specialty laminates in electronics and photovoltaic applications.

Technology Insights

Solvent-based laminating adhesives currently hold a leading position with approximately 45% market share, supported by established manufacturing infrastructure, proven performance, and cost-effectiveness for high-volume production. These adhesives employ volatile organic carriers, such as toluene, xylene, and ester-alcohol blends, to deliver adhesive components, ensuring rapid initial tack and strong final bond strength, which are essential for flexible packaging applications. However, this technology faces increasing regulatory pressure due to VOC emissions, requiring significant investment in capture and control systems to maintain compliance with stringent air quality standards.

In contrast, water-based adhesives are gaining traction, driven by regulatory exemptions in regions such as Taiwan, California, and the European Union. These formulations eliminate VOC emissions, enhance workplace safety, and align with sustainability goals. Industry data indicate that adoption of solvent-free adhesives is accelerating at a 7.3% CAGR, positioning water-based technologies for substantial growth through 2033.

Industry Insights

Packaging applications dominate the lamination adhesives market, accounting for nearly 63% of overall demand. This segment relies heavily on multi-layer laminated structures to ensure product protection, extend shelf life, and enhance brand differentiation. It includes diverse sub-applications such as snack food pouches, boil-in-bag meal packages, flexible pharmaceutical containers, and retort-sterilizable medical laminates, each requiring specialized adhesive chemistries tailored to processing conditions ranging from ambient dry-lamination to heated roller bonding and in-line heat sealing.

Growth in this segment is reinforced by the expansion of the food and beverage packaging industry, driven by urbanization and the accelerating shift toward sustainable solutions incorporating recyclable and compostable materials. Automotive and transportation represent the second-largest Industry segment, while industrial applications, such as thermal insulation and electrical lamination, are growing steadily, supported by innovations in solvent-free technologies and enhanced durability formulations.

Regional Insights

North America Lamination Adhesives Market Trends

North America remains the most innovation-driven market for lamination adhesives, distinguished by stringent regulatory frameworks such as the EPA Clean Air Act VOC standards and FDA food-contact approvals, which set global benchmarks for safety and performance. Market leadership in the region is supported by substantial investments in R&D, pilot manufacturing facilities, and technical support infrastructure, enabling rapid commercialization of advanced low-VOC and water-based technologies.

Key players, including 3M, H.B. Fuller, and Henkel AG, maintain significant operations across the United States, Canada, and Mexico. Growth is fueled by e-commerce expansion and rising demand for premium flexible packaging in food, pharmaceutical, and medical device applications. Additionally, automotive manufacturers like General Motors, Ford, and Tesla drive the adoption of high-performance adhesives for lightweight and electric vehicle components. Despite market maturity, North America is projected to grow at a moderate CAGR of 4.8% through 2033.

Europe Lamination Adhesives Market Trends

Europe represents a mature and highly regulated market, defined by stringent environmental governance, advanced manufacturing capabilities, and a strong focus on sustainability and circular economy principles. The lamination adhesives sector is primarily driven by the EU’s REACH regulations, which enforce comprehensive chemical approval requirements, and the EU Green Deal, which sets ambitious targets for plastic reduction and recyclability.

Germany is the region’s leading manufacturing hub, supported by robust research infrastructure and established partnerships with the automotive and packaging industries. Secondary growth markets include France, the United Kingdom, and Italy, where demand for high-performance, food-safe adhesives remains strong. The adoption of solvent-free and bio-based adhesives is accelerating, supported by regulatory incentives and VOC-control exemptions. Arkema S.A., through its Bostik division, exemplifies regional leadership, strengthened by strategic acquisitions and innovation in sustainable adhesive technologies.

Asia Pacific Lamination Adhesives Market Trends

Asia-Pacific is emerging as the fastest-growing region in the lamination adhesives market, driven by rapid industrialization, urbanization, and concentrated manufacturing in emerging economies. China dominates the region as the world’s largest producer of flexible packaging materials, supported by strong domestic consumption and export demand. Its booming e-commerce sector, led by platforms such as Alibaba, fuels significant demand for laminated packaging across food, cosmetics, and electronics.

India is the fastest-growing market, with adhesive consumption rising by nearly 18% annually, supported by initiatives such as “Make in India” that attract global manufacturers. Japan and South Korea specialize in high-performance applications for electronics and semiconductors, whereas ASEAN countries, including Vietnam, Thailand, and Indonesia, exhibit accelerating adoption, driven by rising consumer spending and investment in pharmaceutical packaging.

Competitive Landscape

The lamination adhesives market exhibits moderate concentration, characterized by clear differentiation between global leaders and regional specialists. Competitive advantage in this market hinges on technological sophistication, regulatory compliance, sustainability credentials, and customized solutions for packaging, automotive, and industrial applications. Strategic acquisitions, such as Arkema S.A.’s US$150 million purchase of Dow’s flexible packaging adhesives business in December 2024, have reshaped competition. Regional players like Pidilite Industries and DIC Corporation focus on cost-effective formulations and localized support, while smaller innovators target niche, high-margin segments.

Key Developments:

- July 2025: Henkel AG launched Loctite Liofol LA 7837/LA 6265, a solvent-free polyurethane adhesive system for retort packaging with ultra-low monomer content, high-temperature resistance up to 134°C, and reduced CO2 emissions through elimination of energy-intensive drying processes.

- May 2024: Arkema has agreed to acquire Dow’s flexible packaging laminating adhesives business, one of the leading producers of adhesives for the flexible packaging market, generating annual sales of around US$250 million. The proposed acquisition will significantly expand Arkema’s portfolio of solutions for flexible packaging, enabling the Group to become a key player.

- April 2024: Henkel AG completes acquisition of Seal for Life Industries, expanding protective coating and sealing portfolio in infrastructure maintenance for renewable energy, gas, and water supply sectors as part of maintenance, repair, and overhaul growth strategy.

Top Companies in the Lamination Adhesives Market

- Henkel AG (Düsseldorf, Germany) maintains global market leadership through its integrated portfolio of solvent-based, water-based, and solvent-free laminating adhesive products under the Loctite Liofol brand, supported by extensive research and development capabilities, manufacturing infrastructure spanning multiple continents, and technical expertise addressing diverse Industry applications.

- Arkema S.A. (Colombes, France) operates as a specialty materials leader through its Bostik adhesive solutions division, strengthened by its December 2024 acquisition of Dow's flexible packaging laminating adhesives business, creating a powerhouse competitor with comprehensive product coverage spanning solvent-based, solvent-free, and heat-seal coating technologies.

- 3M Company (Saint Paul, U.S.) competes through diversified product portfolios including solvent-free laminating adhesives, UV-curable systems, and water-based formulations supported by substantial innovation investments, global technical support infrastructure, and strong customer relationships across automotive, packaging, and industrial segments.

Companies Covered in Lamination Adhesives Market

- Henkel AG

- 3M Company

- H.B. Fuller Company

- The Dow Chemical Company

- Arkema S.A.

- Sika AG

- DIC Corporation

- Pidilite Industries

- Flint Group

- Ashland Inc.

- Coim Group

Frequently Asked Questions

The global lamination adhesives market is projected to reach US$ 6.0 billion by 2033, expanding from US$ 4.1 billion in 2026, representing a CAGR of 5.7% driven by rising demand for flexible packaging, regulatory compliance initiatives, and technological innovations in solvent-free and water-based adhesive formulations.

Market growth is fundamentally driven by accelerating flexible packaging adoption across the food and beverage industries, electric vehicle manufacturing expansion requiring lightweight structural adhesives for battery assembly and vehicle body applications, and pharmaceutical and medical device packaging requirements for biocompatibility.

Polyurethane resins maintain a dominant market position with approximately 47% share, driven by superior flexibility, strong bond strength across diverse substrates, rapid curing characteristics enabling high-speed production, and extensive regulatory approvals in major markets including the European Union and North America.

Asia-Pacific represents the fastest-growing geographic region, expanding at rates exceeding 6% CAGR, driven by rapid industrialization, urbanization, e-commerce growth concentrated in China and India, manufacturing expansion across packaging and automotive sectors, and growing customer adoption of sustainable packaging solutions supporting market expansion through 2033.

Sustainable packaging solutions and biodegradable laminating adhesives represent the most substantial market opportunity, supported by regulatory mandates requiring all plastic packaging to be recyclable or reusable by 2030, emerging compostable adhesive certifications meeting ASTM D6400 and EN 13432 standards, premium pricing supporting innovation-driven competitive differentiation, and brand owner sustainability commitments creating structural demand for advanced environmental compliance solutions.

Market leadership is concentrated among Henkel AG, Arkema S.A., 3M Company, and regional specialists Pidilite Industries, Sika AG, and H.B. Fuller Company, leveraging cost-effectiveness, localized support, and specialized application expertise.