- Inks, Coatings, Adhesives & Sealants (ICAS)

- Polyvinyl Acetate Adhesives Market

Polyvinyl Acetate Adhesives Market Size, Share, and Growth Forecast, 2025 - 2032

Polyvinyl Acetate Adhesives Market by Product Type (Water-based, Solvent-based, Hot Melt, Others), Application (Woodworking, Packaging, Construction, Textiles, Others), and Regional Analysis for 2025 - 2032

Polyvinyl Acetate Adhesives Market Size and Trend Analysis

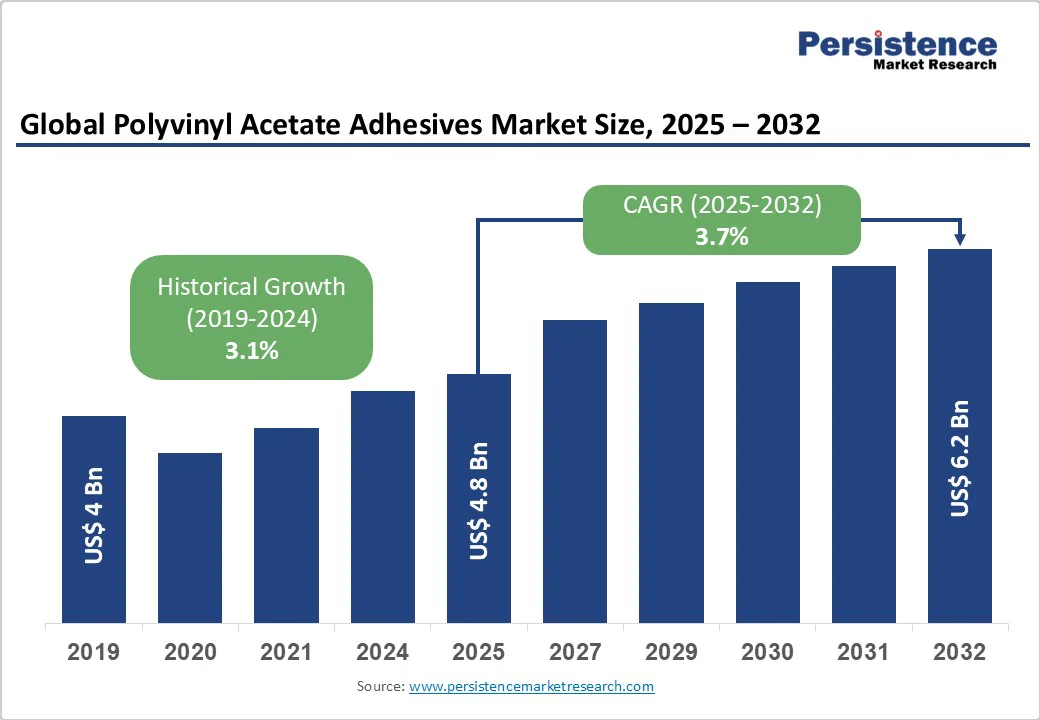

The global polyvinyl acetate adhesives market size is likely to value at US$4.8 Bn in 2025 and reach US$6.2 Bn by 2032, growing at a CAGR of 3.7% during the forecast period from 2025 to 2032.

The polyvinyl acetate adhesives market is witnessing steady growth, driven by increasing demand from key industries such as woodworking, packaging, and construction, where strong bonding, versatility, and eco-friendliness are critical.

Polyvinyl acetate adhesives, known for their excellent adhesion, quick setting time, and low toxicity, are essential for bonding wood, paper, and other porous materials.

Key Industry Highlights:

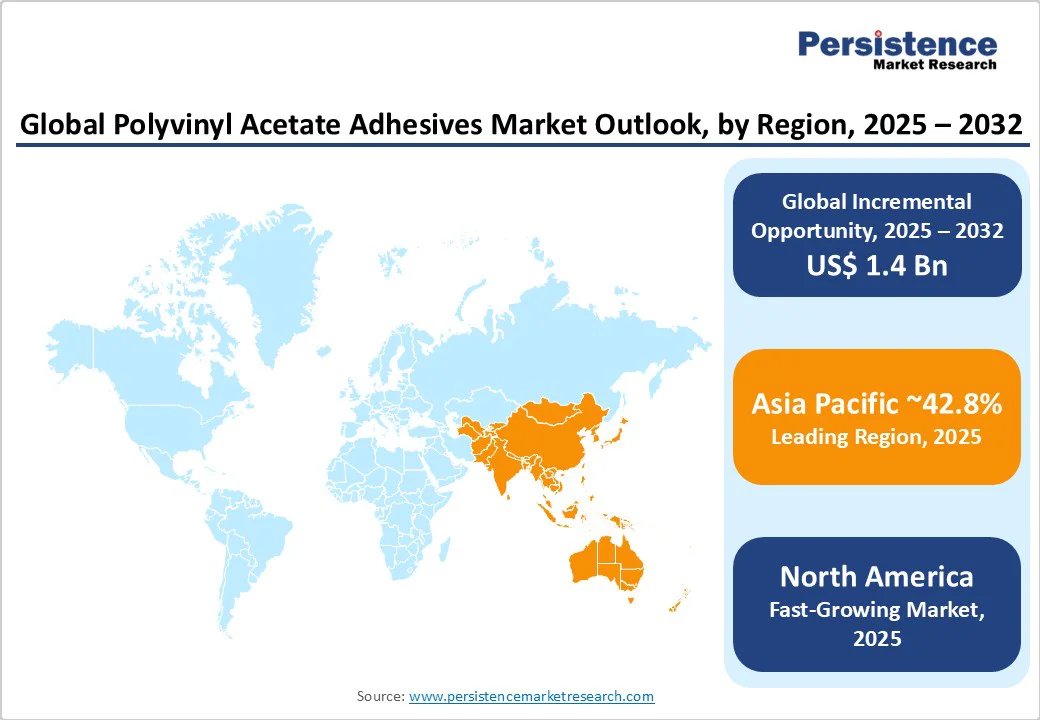

- Leading Region: Asia Pacific holds 42.8% market share of the polyvinyl acetate adhesives market in 2025, propelled by rapid urbanization, infrastructure investments, and high manufacturing output in countries such as China and India.

- Fastest-growing Region: North America is the fastest-growing region, driven by robust woodworking and packaging sectors in the U.S. and Canada, supported by advanced industrial infrastructure.

- Investment Plans: China’s National Development and Reform Commission announced a 2022 plan to expand packaging and construction capacities by 2035, boosting demand for polyvinyl acetate adhesives in sustainable applications.

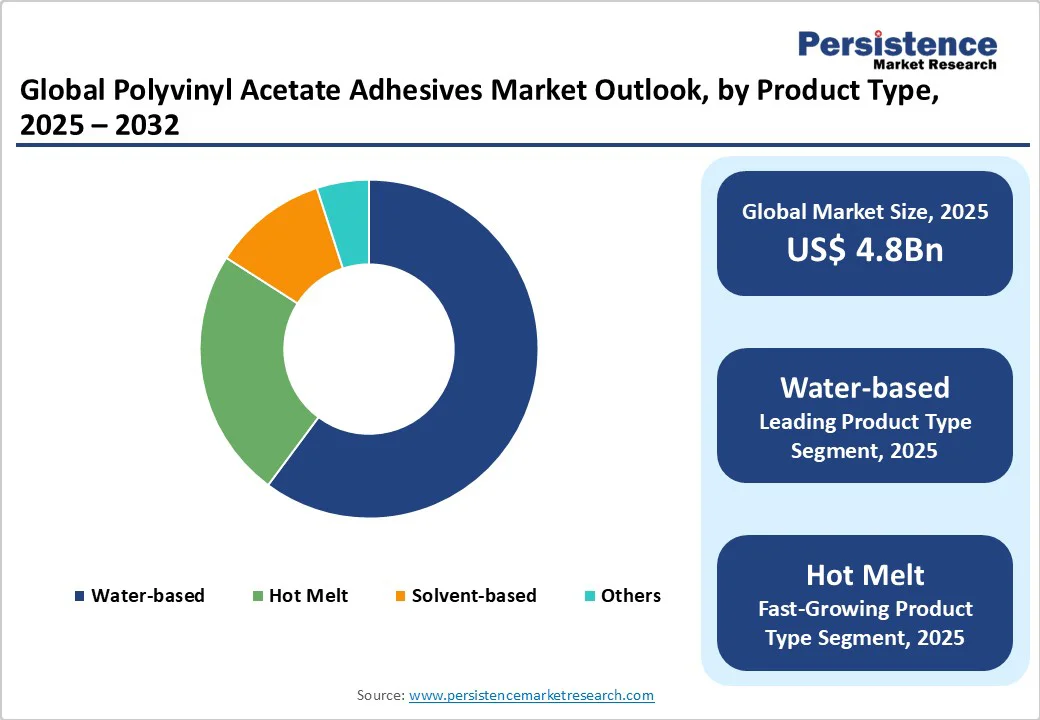

- Dominant Product Type: Water-based, accounting for nearly 59.8% of the market share, due to its environmental compliance and cost-effectiveness for everyday bonding needs.

- Leading Application: Packaging, contributing over 38.45% of market revenue, driven by global e-commerce growth and sustainable packaging trends.

| Key Insights | Details |

|---|---|

| Polyvinyl Acetate Adhesives Market Size (2025E) | US$ 4.8Bn |

| Market Value Forecast (2032F) | US$ 6.2Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.1% |

Market Dynamics

Driver: Growing Infrastructure and Construction Activities Fuel Market Expansion

The global polyvinyl acetate adhesives market is experiencing significant growth due to the surge in infrastructure and construction activities worldwide. Polyvinyl acetate adhesives are critical in construction for bonding wood panels, flooring, and insulation materials, offering reliable performance in both residential and commercial projects.

According to the G20’s Global Infrastructure Hub (GI Hub), global infrastructure investment needs are expected to reach $94 trillion by 2040, with a significant portion allocated to emerging economies.

In Asia Pacific, China’s Belt and Road Initiative and India’s Smart Cities Mission drive demand for eco-friendly adhesives in construction applications. The American Society of Civil Engineers reports that over 45,000 U.S. bridges require repair or replacement, further increasing the need for durable polyvinyl acetate adhesives.

Companies such as Henkel AG & Co. KGaA reported a sales increase in construction-grade adhesives in 2024. Government-led initiatives and rising urbanization ensure sustained demand, positioning construction as a key driver for market growth through 2032.

Restraint: Volatility in Raw Material Prices and Competition from Alternative Adhesives

The polyvinyl acetate adhesives market is under pressure due to several compounding challenges. A major issue is the volatility in raw material costs, particularly vinyl acetate monomer (VAM) and energy, both of which experienced significant price fluctuations in 2023. This instability raises production costs, squeezing profit margins, especially for smaller manufacturers, making it harder for them to remain competitive.

Furthermore, PVA adhesives are increasingly challenged by alternative formulations such as epoxy and polyurethane, which offer superior performance in demanding, high-stress applications. Adoption of PVA is also hampered in certain regions by the lack of product standardization and environmental concerns, especially over VOC emissions in solvent-based variants. In cost-sensitive markets, these factors reduce demand and limit growth potential, pushing manufacturers to innovate or diversify to maintain market relevance.

Opportunity: Rising Demand in the Packaging and Sustainable Furniture Sectors

The increasing focus on sustainable packaging and eco-friendly furniture presents significant opportunities for the polyvinyl acetate adhesives market. Polyvinyl acetate adhesives are essential in packaging for sealing cartons and laminating materials, aligning with the shift toward recyclable solutions.

The International Trade Centre projects global sustainable packaging demand to grow by 2.5 times by 2030, with e-commerce investments driving the need for quick-drying adhesives. In the furniture sector, polyvinyl acetate adhesives are used in assembly and finishing processes for wood-based products.

Companies such as 3M Company are innovating with low-emission, water-based formulas for sustainable furniture manufacturing, aligning with green trends. Government incentives, such as the EU’s Circular Economy Action Plan, further encourage investments in eco-technologies, creating opportunities for manufacturers to develop advanced, biodegradable polyvinyl acetate adhesives to meet evolving industry needs through 2032.

Category-wise Insights

By Product Type

- Water-based holds the largest market share, approximately 59.8% in 2025, due to its low environmental impact and versatility in everyday applications. Widely used in woodworking and packaging, water-based polyvinyl acetate adhesives are favored for their ease of application, quick drying, and compliance with stringent VOC regulations. Companies such as H.B. Fuller Company and Sika AG lead with extensive portfolios, catering to demand in sustainable construction and paper industries across North America and the Asia Pacific. These adhesives offer excellent adhesion to porous substrates such as wood and paper, making them ideal for high-volume production environments where cost-efficiency and safety are paramount.

- Hot Melt is the fastest-growing product segment, driven by its rapid bonding capabilities and suitability for automated processes in fast-paced industries. Its adoption is rising in textiles and automotive assembly, where heat-activated adhesion provides strong, durable bonds without solvents. Brands such as Dow Inc. and Bostik SA are expanding offerings in high-speed packaging lines in Europe and the Asia Pacific, supported by growing demand for efficient, residue-free solutions.

By Application

- The packaging sector accounts for over 38.45% of market revenue in 2025, driven by global e-commerce expansion and the need for reliable sealing solutions. Polyvinyl acetate adhesives are critical for carton closing, labeling, and laminate bonding in the paper and board industry. Major players such as Henkel AG & Co. KGaA supply high-performance variants for projects in the U.S. and China, where investments in recyclable packaging fuel demand. This application's growth is underpinned by the surge in online retail, which requires adhesives that maintain integrity during shipping and storage, while supporting lightweight, sustainable designs.

- The woodworking sector is the fastest-growing application, propelled by rising demand for custom furniture and interior fittings. Polyvinyl acetate adhesives excel in edge banding, joint assembly, and veneer application, offering clear, strong bonds that resist moisture. Companies such as Franklin International and Pidilite Industries Limited innovate for precision woodworking in the Asia Pacific and the Middle East, where residential construction booms. This segment's expansion is tied to DIY trends and modular housing, emphasizing adhesives that provide gap-filling properties and easy cleanup.

By End-use

- The paper & packaging end-use accounts for over 35.67% of the market revenue of the polyvinyl acetate adhesives market in 2025, driven by the global shift toward lightweight and recyclable materials. Polyvinyl acetate adhesives are vital for bookbinding, envelope sealing, and flexible packaging, providing flexible yet robust adhesion. Major players such as 3M Company and Arkema Group supply specialized formulas for high-speed converting operations in the U.S. and Europe, where e-commerce and food safety standards drive innovation. This end-use thrives on the adhesive's compatibility with cellulosic fibers, enabling efficient production of consumer goods such as boxes and labels.

- The building & construction end-use is the fastest-growing segment, fueled by investments in green buildings and renovations. Polyvinyl acetate adhesives support tile installation, drywall finishing, and insulation bonding, offering water resistance and mold prevention. Companies such as Sika AG and Wacker Chemie AG develop enhanced variants for seismic zones in the Asia Pacific and Latin America, aligning with energy-efficient standards. Growth here is accelerated by urbanization, with adhesives enabling faster assembly in prefabricated structures and sustainable retrofits.

Regional Insights

Asia Pacific Polyvinyl Acetate Adhesives Market Trends

Asia Pacific leads the global polyvinyl acetate adhesives market, accounting for approximately 42.8% share in 2025. This is driven by rapid urbanization, robust infrastructure development, and expanding manufacturing activity in key economies such as China and India.

China, as a global manufacturing hub, creates strong demand across construction, packaging, and textile applications. In India, government initiatives such as the Make in India campaign have significantly boosted domestic manufacturing and packaging, particularly in the fast-growing e-commerce sector, where water-based PVA adhesives are preferred for their eco-friendly and cost-effective properties.

Additionally, the region's thriving textiles and furniture industries further accelerate adhesive demand. Leading companies such as Pidilite Industries Limited and H.B. Fuller Company are expanding their operations and distribution networks in the region to capitalize on this growth. Government-backed infrastructure and industrial projects are expected to sustain the region’s upward trajectory in the PVA adhesives market through 2032.

North America Polyvinyl Acetate Adhesives Market Trends

North America is the fastest-growing region in the polyvinyl acetate adhesives market, fueled by strong demand from the woodworking, construction, and packaging industries, particularly in the U.S. and Canada. The region benefits from a highly developed industrial infrastructure that supports large-scale production and innovation. In the U.S., the booming packaging industry, driven by retail, e-commerce, and logistics, relies significantly on PVA adhesives due to their sustainability, versatility, and compatibility with paper-based materials.

Canada’s construction sector is expanding steadily, increasing demand for durable, low-VOC adhesives that meet both performance and environmental standards, as highlighted by the Canadian Home Builders' Association. Leading manufacturers such as 3M Company and Franklin International maintain a strong foothold in the region, offering advanced adhesive solutions tailored to furniture manufacturing, interior remodeling, and commercial construction.

Additionally, growing consumer preference for eco-friendly and high-performance adhesives continues to reinforce North America’s competitive edge in the global market.

Europe Polyvinyl Acetate Adhesives Market Trends

Europe stands as the second fastest-growing region in the polyvinyl acetate adhesives market, fueled by a combination of environmental regulations, industrial innovation, and sectoral demand.

Stringent EU policies, particularly under the European Green Deal, are pushing industries toward low-emission, sustainable adhesive solutions, especially in construction and renovation projects. The regions' mature automotive and textile sectors increasingly adopt PVA adhesives for their environmental compatibility and performance.

The European packaging industry further supports market growth, with rising demand for water-based adhesives suited for recyclable and biodegradable materials. In Germany and France, infrastructure development and high-end furniture manufacturing drive the consumption of hot melt variants.

Key players such as Henkel AG & Co. KGaA and Bostik SA are actively innovating to deliver products that meet both performance requirements and sustainability standards. Europe’s strong commitment to circular economy principles and high-quality regulations ensures that the region remains a dynamic and progressive market for PVA adhesives.

Competitive Landscape

The global polyvinyl acetate adhesives market is highly competitive, dominated by extensive product portfolios and global distribution networks. The polyvinyl acetate adhesives market is characterized as a fragmented market based on competitors.

This is due to the presence of numerous domestic and international players, ranging from large, established companies to smaller, regional manufacturers. Regional players such as Pidilite Industries Limited focus on localized offerings in the Asia Pacific. Companies are investing in advanced formulations and bio-based additives to enhance market share, driven by demand for eco-friendly adhesives in the packaging and construction sectors.

Key Industry Developments:

- May 2024: Anhui Wanwei Bisheng Co., Ltd. has announced the launch of a new line of polyvinyl alcohol (PVA) products, marking a significant step forward in material innovation. These advanced PVA products offer enhanced bonding strength, superior water resistance, and excellent film-forming properties, making them ideal for applications in textiles, paper, construction, and packaging industries. In addition to performance improvements, Wanwei has integrated environmentally friendly manufacturing processes to reduce carbon emissions and pollutants, aligning with global sustainability initiatives.

Companies Covered in Polyvinyl Acetate Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Arkema Group

- Sika AG

- Dow Inc.

- Ashland Global Holdings Inc.

- Avery Dennison Corporation

- Bostik SA

- Franklin International

- Pidilite Industries Limited

- Wacker Chemie AG

- Others

Frequently Asked Questions

The Polyvinyl Acetate Adhesives market is projected to reach US$4.8 Bn in 2025.

Growing infrastructure and construction activities, and expanding applications in sustainable packaging are the key market drivers.

The Polyvinyl Acetate Adhesives market is poised to witness a CAGR of 3.7% from 2025 to 2032.

The rising demand in the packaging and sustainable furniture sectors is the key market opportunity.

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, and Pidilite Industries Limited are key market players.