- Food Ingredients & Additives

- U.S. Sugar Alternatives Market

U.S. Sugar Alternatives Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

U.S. Sugar Alternatives Market by Product Type (HFCS, Sugar Alcohol, Sucralose, Aspartame, Stevia, Saccharin, Others), Intensity (High, Low), Application (Food, Beverage, Healthcare and Personal Care), Distribution Channel (B2B, B2C), and Zonewise Analysis from 2026 to 2033

U.S. Sugar Alternatives Market Share and Trends Analysis

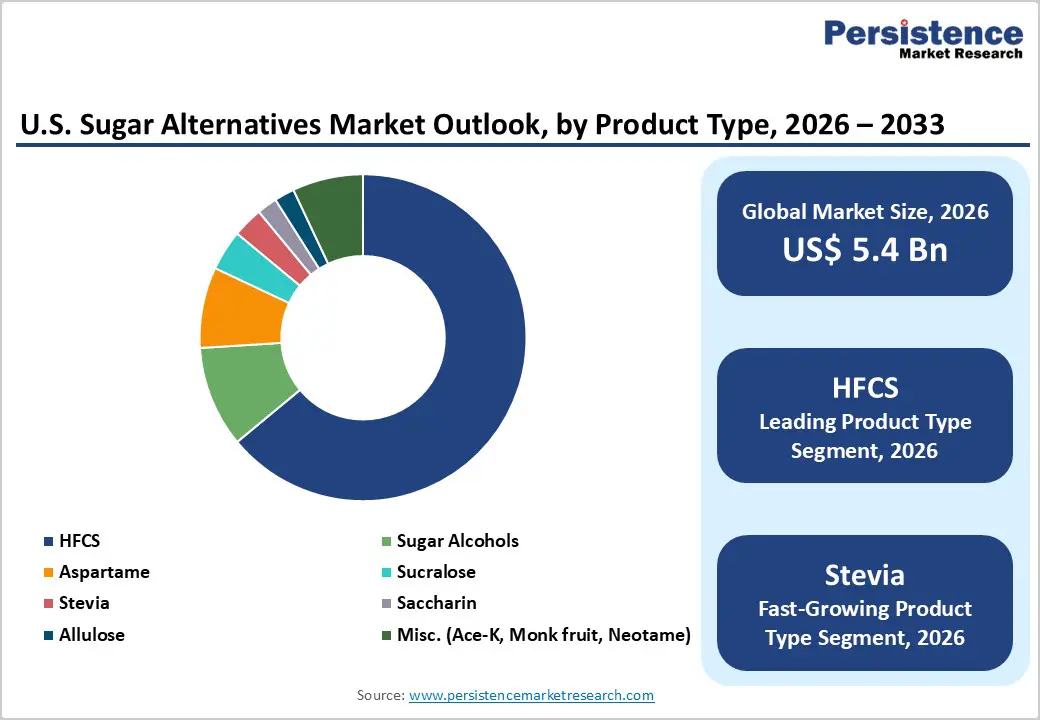

The U.S. sugar alternatives market size is estimated to grow from US$ 5.4 billion in 2026 to US$ 6.9 billion by 2033, projected to expand at a CAGR of 3.6% during the forecast period from 2026 to 2033.

It is evolving into a high-impact innovation space where health priorities and formulation science intersect. Strong momentum in clean-label ingredients and functional beverages is redefining how sweetness is delivered across everyday consumption.

Key Industry Highlights

- Leading Application: Beverages dominate with 58% share (2025), driven by strong demand for low-calorie, clean-label drink options across soft drinks, teas, and RTD beverages.

- Fastest Growing Product Type: Stevia is expected to register the highest growth, supported by its plant-based origin, zero-calorie profile, and improved taste performance through advanced formulations.

- Growth Indicator: Rising prevalence of Diabetes and prediabetes is accelerating the shift toward low-glycemic and non-nutritive sweeteners.

- Challenges: Limitations in replicating sugar’s taste, texture, and mouthfeel continue to restrict adoption across complex food applications.

- Key Opportunity: Collaborative innovation between companies such as Ajinomoto and Shiru is enabling development of next-generation sweet proteins and clean-label solutions.

Market Dynamics

Driver: Rising Diabetes Burden Accelerating Sugar Alternative Adoption

The increasing prevalence of metabolic disorders, particularly Diabetes and prediabetes, is significantly reshaping dietary patterns in the U.S. According to the Centers for Disease Control and Prevention, over 37 million Americans are living with diabetes, while nearly 97.6 million adults are prediabetic. This expanding at-risk population is actively seeking alternatives to traditional sugar to better manage blood glucose levels and overall health. Growing awareness around the link between excessive sugar consumption and chronic conditions is accelerating the shift toward low-calorie and low-glycemic sweetening solutions.

Non-nutritive sweeteners such as Saccharin and Aspartame are widely used due to their minimal impact on blood sugar levels, making them suitable for diabetic-friendly diets. Additionally, increased labeling transparency and public health initiatives are reinforcing consumer confidence in these alternatives. As preventive healthcare gains importance, sugar substitutes are evolving from niche products into mainstream dietary components, supporting long-term health management and fueling sustained market growth.

Restraint: Challenges in Replicating Sugar’s Sensory Profile

A key restraint in the U.S. sugar alternatives market is the difficulty in replicating sugar’s complete sensory experience, which extends beyond sweetness to include texture, mouthfeel, and flavor enhancement. Traditional sugar plays a critical functional role in products such as baked goods, sauces, and confectionery, where it contributes to structure, browning, and overall palatability. Many substitutes, including Aspartame and Sucralose, often fail to fully match these attributes, sometimes leaving noticeable aftertastes that affect consumer acceptance. Even natural options like Stevia can introduce off-notes, limiting their use in certain formulations.

Additionally, lingering consumer skepticism around artificial sweeteners and their perceived long-term health effects continues to influence purchasing decisions. This creates a dual challenge for manufacturers: improving taste and functionality while addressing trust concerns. As a result, significant investment in formulation science and ingredient blending is required, slowing product development cycles and constraining broader adoption across mainstream food categories.

Opportunity: Collaborative Innovation Accelerating Sugar Alternative Development

Strategic collaborations are emerging as a powerful opportunity in the U.S. sugar alternatives market, enabling companies to co-develop next-generation sweetening solutions. Partnerships such as the collaboration between Ajinomoto and Shiru highlight how combining fermentation expertise with AI-driven ingredient discovery can accelerate the creation of novel sweet proteins. These innovations aim to replicate the taste and functionality of sugar while aligning with consumer demand for natural, minimally processed ingredients derived from sustainable sources.

Such alliances allow companies to pool technological capabilities, reduce R&D timelines, and enhance product differentiation in an increasingly competitive landscape. By leveraging complementary strengths, businesses can develop solutions that address both sensory performance and clean-label expectations. This collaborative approach also expands market reach, enabling faster commercialization across beverages, specialty foods, and functional nutrition categories. As consumer focus intensifies on health, transparency, and sustainability, partnerships will play a critical role in unlocking scalable and innovative sugar alternatives.

Category-wise Analysis

By Product Type Insights - Stevia is expected to show promising growth during the forecast period

Stevia is projected to witness strong growth in the U.S. sugar alternatives market, driven by rising health consciousness and the shift away from calorie-dense sugars linked to conditions such as Diabetes and Obesity. Derived from the leaves of Stevia rebaudiana, stevia offers a zero-calorie solution that aligns with consumer demand for weight management and blood sugar control. Its positioning as a natural, plant-based sweetener further strengthens its appeal among consumers seeking clean-label and minimally processed food ingredients.

The segment is also benefiting from the growing adoption of plant-based and vegan diets, where stevia fits seamlessly as a naturally sourced ingredient. Additionally, advancements in extraction and formulation technologies have significantly improved its taste profile, reducing the bitterness historically associated with earlier variants. These improvements are enabling broader applications across beverages, bakery, and packaged foods, positioning stevia as a key growth driver within the evolving sugar alternatives landscape.

By Application Insights - Beverages dominate the U.S. sugar alternatives market

The beverages segment leads the U.S. sugar alternatives market, accounting for approximately 58% share in 2025, driven by strong consumer demand for low-calorie and health-oriented drink options. Sugar substitutes such as stevia, monk fruit, and allulose are widely adopted across soft drinks, flavored waters, teas, and ready-to-drink alcoholic beverages, as they provide sweetness without contributing to calorie intake or glycemic spikes. Both established brands and emerging players are actively reformulating products to align with clean-label expectations and reduced-sugar trends, making beverages a primary innovation hub within the market.

Companies like Suntory Holdings Ltd. are advancing this space by developing functional beverages that combine high-intensity sweeteners with amino acids to enhance sweetness perception while minimizing aftertaste. In parallel, improvements in taste-masking technologies and ingredient synergies are enabling more refined flavor profiles. As consumers increasingly prioritize transparency and wellness, the beverage category continues to drive large-scale adoption of sugar alternatives.

Competitive Landscape

The U.S. sugar alternatives market is becoming increasingly dynamic, shaped by strong consumer demand for healthier diets and ongoing pressure to reduce sugar consumption. Manufacturers are investing heavily in advanced formulation technologies, cleaner extraction processes, and natural ingredient systems to deliver low- and zero-calorie sweeteners with improved taste and functionality. Companies such as ADM are leveraging integrated ingredient platforms that combine sweeteners with functional additives to enhance texture and nutritional value. At the same time, players like Ingredion Incorporated are emphasizing the sustainability and performance benefits of next-generation stevia variants.

Regulatory oversight from the U.S. Food and Drug Administration plays a critical role in shaping innovation and market entry. GRAS approvals and evolving labeling standards are pushing companies toward greater transparency and reformulation. In response, brands are refining communication strategies to build consumer trust while maintaining compliance, positioning the U.S. as a key hub for sugar-reduction innovation.

Key Industry Developments:

- In March 2026, HOWTIAN showcased its advanced stevia-based sugar reduction and flavor solutions at FIC 2026 in Shanghai, highlighting innovation in food formulation and clean-label sweetening.

- In February 2026, Tate & Lyle and Manus launched a premium stevia-derived sweetener under the Yume brand, delivering a sugar-like taste profile and marking the first product from The Sweetener Alliance.

- In February 2025, Oobli partnered with Ingredion to expand access to next-generation sweetener systems. The collaboration aims to accelerate the commercialization of natural, clean-label alternatives by combining Ingredion’s stevia capabilities with Oobli’s proprietary sweet protein technology.

- In July 2024, Roquette and Bonumose, announced a Cooperation Agreement to advance the development of tagatose, a natural-origin sweetener with clinically proven health benefits. The partnership aims to bring innovative, healthier sugar alternatives to the market.

U.S. Sugar Alternatives Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.4 Bn |

| Projected Market Value (2026) | US$ 5.4 Bn |

| Projected Market Value (2033) | US$ 6.9 Bn |

| CAGR (2026 - 2033) | 3.6% |

| Dominant Application | Beverages, 58% share |

| Top-ranking Product Type | HFCS, 64% share |

| Incremental Opportunity | US$ 1.5 Bn |

Companies Covered in U.S. Sugar Alternatives Market

- Cargill, Inc

- Ingredion

- Tate & Lyle

- IFF

- ADM

- Ajinomoto Co., Inc.

- Celanese Corporation (Nutrinova)

- Roquette

- Cumberland Packing Corp.

- Whole Earth Brands

- Heartland Food Products Group

- Pyure Brands LLC

- B&G Foods, Inc.

- Sweegen

- Merck KGaA

- GLG Life Tech Corp.

- Others

Frequently Asked Questions

The U.S. Sugar Alternatives market is projected to be valued at US$ 5.4 Bn in 2026.

The increasing prevalence of diabetes is fueling the adoption of sugar alternatives in the U.S. market.

The U.S. Sugar Alternatives market is poised to witness a CAGR of 3.6% between 2026 and 2033.

Collaborative innovation accelerating sugar alternative development is key opportunity in the U.S. Sugar Alternatives market.

Cargill, Inc, Ingredion, Tate & Lyle, IFF, ADM, Ajinomoto Co., Inc., Celanese Corporation (Nutrinova), Roquette, and Whole Earth Brands.