- Processed Food

- U.S. Full Service Restaurants Market

U.S. Full Service Restaurants Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Full Service Restaurants Market by Cuisine (Asian, European, Latin American, Middle Eastern, North American, Others), by Outlet (Chained, Independent), Location (Leisure, Lodging, Retail, Standalone, Travel), Regional Analysis, 2026 - 2033

U.S. Full Service Restaurants Market Size and Trend Analysis

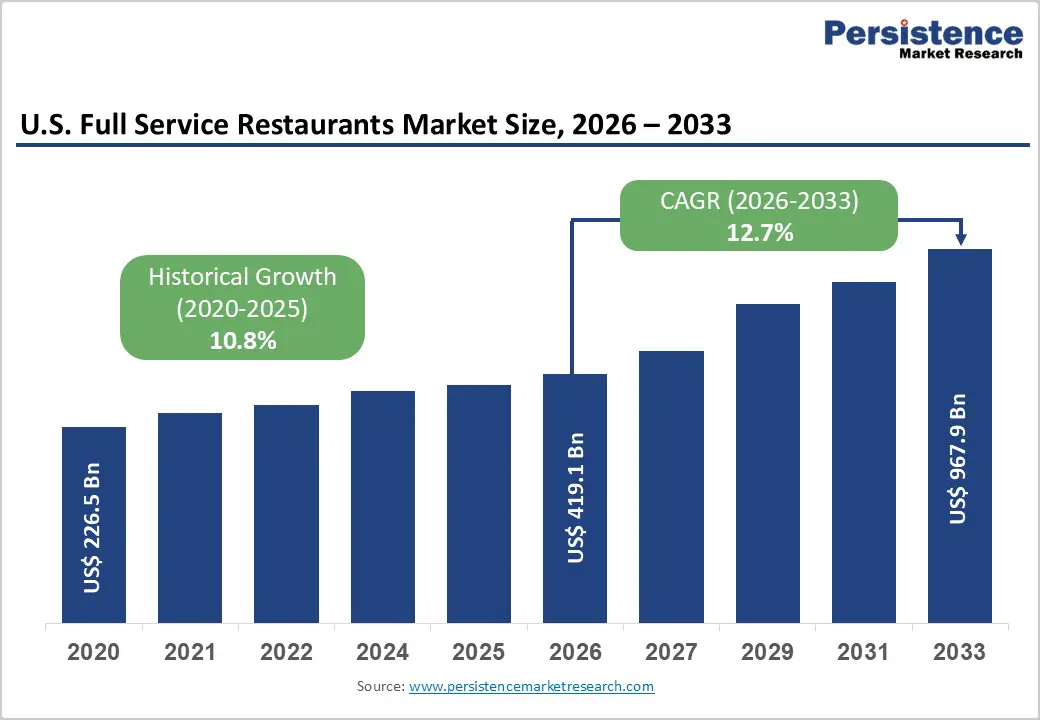

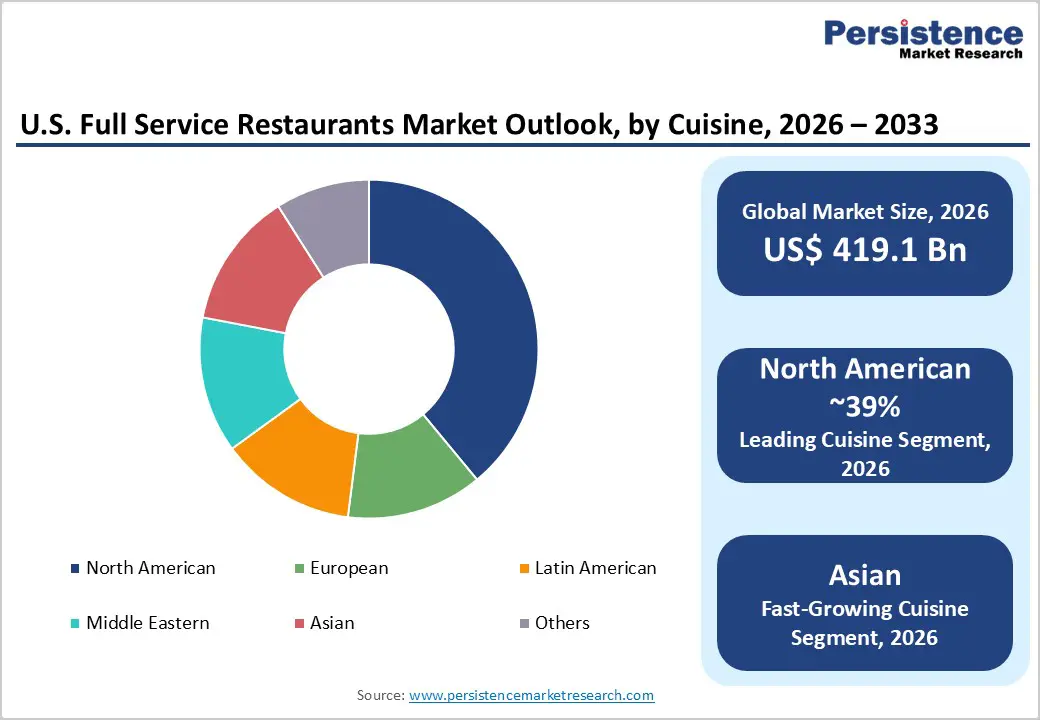

The U.S. full service restaurants market size is expected to be valued at US$ 419.1 billion in 2026 and projected to reach US$ 967.9 billion by 2033, growing at a CAGR of 12.7% between 2026 and 2033.

It represents a significant segment of the foodservice industry, characterized by establishments where customers are seated and served by waitstaff. These restaurants typically offer diverse menus, including appetizers, main courses, desserts, and beverages, catering to a wide range of consumer preferences.

Rising disposable incomes, changing dining habits, and growing demand for experiential dining. It includes casual dining, fine dining, and family-style restaurants. Increasing preference for convenience, digital reservations, and delivery integration is also shaping growth. Despite challenges like labor costs and inflation, the sector remains resilient due to strong consumer demand.

Key Industry Highlights:

- Leading Zone - Southeast leads U.S. FSR market with 28% share, driven by population growth, HQ concentration, and suburban expansion.

- Fastest Growing Zone - Southwest grows fastest at 14.5% CAGR, fueled by migration, tourism-driven dining, and diverse consumer demographics.

- Dominant Segment - North American cuisine holds 39% share, supported by widespread steakhouse, seafood, and comfort food chain penetration.

- Fastest Growing Segment - Asian cuisine expands fastest due to demographic shifts, mainstream acceptance, and premium experiential dining growth.

- Key Market Opportunity - Airports, resorts, and entertainment venues drive high-growth FSR expansion with strong travel spending and premium footfall.

Market Dynamics

Drivers - Increasing Preference for In-Person Dining Among Gen Z and Millennials

Several millennial and Gen Z consumers in the U.S. are increasingly demanding in-person dining experiences that provide quality service, personalization, and a sense of occasion. The National Restaurant Association stated that in 2025, sales across full-service restaurants are predicted to rise by 5.5%, reaching approximately US$ 400 Bn. This rapid shift from convenience and fast food is specifically high in suburban and urban areas. In these areas, consumers are showing a keen interest in dining and social gatherings due to entertainment and leisure.

The shift in demographics with high incomes is likely to push the market forward. The younger demographics are mainly spending on experiences over material goods. OpenTable, for example, found in its 2024 survey that nearly 61% of diners aged 25 to 40 years prefer sit-down meals at restaurants that provide quality interaction, curated menus, and ambiance over fast-casual chains. The trend for experience economy is also rising owing to an increasing consumer interest in sustainable dining, chef-led concepts, and regional cuisines. It further encourages restaurant operators to experiment with novel dining options instead of choosing common quick-service options.

Restraints - Cost Sensitivity and Shrinking Margins To Threaten Growth

High inflationary pressures are expected to be a significant factor hindering the U.S. full service restaurant market growth to a certain extent. In 2024, food costs in the country surged by around 4.8%, according to the U.S. Department of Agriculture (USDA). It has compelled several restaurant operators to either lower portion sizes or increase menu prices, which can affect cost-sensitive consumers. These restaurants are typically more sensitive to ingredient price fluctuations, mainly for premium and fresh items, unlike quick-service restaurants that rely on low-cost models.

Full-service restaurants also have narrower margins compared to quick-service restaurants. Saltgrass Steak House, a Texas-based chain, declared in its Q4 2024 earnings that despite strong footfall, high beef prices had negatively affected profit margins. Consumer behavior also plays a significant role in hampering growth. Even if dine-in experiences show steady demand, a few consumers are becoming cautious about their spending due to the ongoing economic uncertainty.

Opportunities - Focus of restaurants on loyalty programs and digital tools

Increasing adoption of loyalty programs and digital tools by full service restaurants is anticipated to create lucrative opportunities in the U.S. Several restaurants are incorporating technologies, including tableside payment options, online reservation systems, AI-backed loyalty programs, and mobile ordering to enhance their operational efficiency. They are also planning to refine their dining experience to attract a more digitally savvy and broader clientele. As per online studies in 2024, nearly 57% of consumers in the U.S. reported that the availability of online payment and digital ordering options positively influenced their decision to visit a restaurant.

Digital loyalty programs are further helping full service restaurants to create strong consumer advocacy and brand communities. They are shifting toward experiential rewards such as private dining discounts, early access to new menu items, or exclusive chef’s table events, away from conventional point-based systems. Yard House, based in California, introduced a loyalty program in 2024. It provides members with early reservations for high-demand events such as beer festivals, resulting in 12% surge in loyalty sign-ups in just six months.

Category-wise Insights

Cuisine Insights

Based on cuisine, the market is divided into Asian, European, Latin American, Middle Eastern, and North American. Among these, the North American segment is predicted to command a dominant share of nearly 39% in 2026. This is attributed to high popularity of traditional North American dishes such as chicken wings, sandwiches, and burgers, which remain the most ordered food items in the U.S. Also, rising consumer preference for sustainable food options and locally sourced products will likely encourage restaurants to provide more organic and plant-based options.

At the same time, they are estimated to maintain their original menu offerings that have historically attracted diners in the U.S. Surging number of steakhouses in the country is another key factor poised to propel the segment.

Middle Eastern cuisine, on the other hand, is speculated to showcase considerable growth through 2032. Increasing consumer demand for exotic and diverse flavors from the Middle East is projected to contribute to growth. The popularity of various traditional items such as hummus, tahini, and dips has recently surged in the U.S. due to their innovative flavor profile, vegetarian options, and use of fresh ingredients. This type of cuisine is gaining momentum among health-conscious consumers and those looking for new culinary experiences.

Outlet Insights

Based on outlet, the market is bifurcated into chain and independent. Out of these, independent outlets are assessed to account for about 75.2% of the U.S. full service restaurants market share in 2025. The growth is attributed to the ability of these restaurants to experiment with new items, introduce community outreach programs, and initiate promotional activities. They aim to generate long-term consumer loyalty with local communities. Independent restaurants, especially those with one or two locations have recently witnessed enhanced adaptability and resilience in catering to consumer expectations associated with ambiance and dining experiences.

Chained outlets are projected to reveal a positive CAGR from 2026 to 2033. These outlets are constantly adopting innovative technologies such as self-service kiosks that can help improve cost-effectiveness and service speed. Large-scale operators are also gaining access to new markets due to the chained model. It has successfully blended the potential for globalization with the rising demand for online meal ordering. In addition, various operators are inclined toward franchising over company-operated outlets due to lower operational risks and reduced capital requirements.

Zone Insights

West U.S. Full Service Restaurants Market Trends

In West U.S., states such as Oregon, Washington, and California are well-known for their robust dining cultures. These are speculated to be the leading hubs for fast-service restaurant operators. A few markets, however, are likely to face certain challenges for regulatory compliance, real estate prices, and labor costs. In April 2024, for example, the minimum wage for retail and fast-food workers in California increased to US$ 20 per hour. It compelled various full service restaurants to raise wages to gain a competitive advantage.

The California Restaurant Association stated that this wage hike is estimated to lead to a 7 to 10% surge in operating costs for restaurants in the state, pushing small-scale establishments to shut down or scale back their operations. Despite these challenges, restaurants in Los Angeles, Seattle, and San Francisco are adopting QR-based ordering, AI-based recommendation engines, and automation to optimize operations while offering top-notch service. Upscale chains, including Canlis and Lazy Bear have already embraced dynamic pricing models for reservations replicating the airline industry. These models have helped them enhance revenue generation during peak hours.

Southeast U.S. Full Service Restaurants Market Trends

States such as Tennessee, Florida, North Carolina, and Georgia in the Southeast are witnessing considerable growth due to the booming tourism industry. With a rising influx of international and domestic travelers, cities, including Savannah, Charleston, Orlando, and Miami, are showing significantly high year-round foot traffic. Sophisticated restaurant groups such as Tavistock Restaurant Collection and José Andrés Group have extended their operations in Florida after realizing the state’s skyrocketing demand for hospitality.

According to a new report, in 2023, the number of full service restaurant openings rose by around 9% in Orlando alone. It was mainly supported by increasing travel activities around the Orange County Convention Center and Walt Disney World. The Southeast further benefits from a favorable economic and regulatory environment, unlike the West. Restaurant operators can flexibly manage labor costs as minimum wage levels are lower in various states in the Southeast U.S., ranging from US$ 7.25 to US$ 10 per hour. It has encouraged national chains and independent restaurant operators to extend their presence across this zone.

Midwest U.S. Full Service Restaurants Market Trends

The Midwest is expected to hold a share of around 29.6% in 2025. Growth is attributed to high demand for value-oriented experiences and community-centric dining preferences. Kansas City, Indianapolis, Minneapolis, and Chicago are considered the key markets for restaurant operators. The relatively lower cost of real estate has attracted several operators to the Midwest to extend their footprint and generate a high share. Ohio's Cooper’s Hawk Winery & Restaurants and Michigan-based Andiamo have experienced success in extending their presence into Tier-II cities due to easy access to loyal consumer bases and favorable leasing rates.

Competitive Landscape

The U.S. full service restaurants market is competitive with the presence of various large-scale as well as emerging players. Their success in the market is highly reliant on an operator’s ability to adapt to evolving consumer preferences and ongoing technological innovations. Small-scale players focus on improving consumer experience, integrating digital tools, and updating their menus. A few operators are also enhancing operational efficiency, investing in staff training, and developing robust loyalty programs.

Key Developments

- In January 2025, Yella’s, offering unique hand-spun milkshakes, piled-high sub sandwiches, and juicy burgers, opened a restaurant in Central Jersey. The fast-casual, family-owned, nearly 60-year-old eatery aims to bring fresh taste to the local community, providing good music, vibrant décor, and delicious meals.

U.S. Full Service Restaurants Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 226.5 billion |

| Current Market Value (2026) | US$ 419.1 billion |

| Projected Market Value (2033) | US$ 967.9 billion |

| CAGR (2026 - 2033) | 12.7% |

| Dominant Cuisine | North American, 39% share (2025) |

| Top-Ranking Outlet | Chained, 61% share (2025) |

| Incremental Opportunity | US$ 548.8 billion (Absolute Dollar Opportunity) |

Companies Covered in U.S. Full Service Restaurants Market

- BJ's Restaurants Inc.

- Bloomin' Brands Inc.

- Brinker International Inc.

- Cracker Barrel Old Country Store Inc.

- Darden Restaurants Inc.

- Red Lobster Hospitality LLC

- DFO LLC

- Dine Brands Global Inc.

- Texas Roadhouse Inc.

- The Cheesecake Factory Restaurants Inc.

- Others

Frequently Asked Questions

The U.S. full service restaurants market is poised to be valued at US$ 419.1 billion in 2026.

Increasing consumer preferences for dining out and the desire for exotic cuisines are the key market drivers.

The U.S. full service restaurants market is poised to witness a CAGR of 12.7% from 2025 to 2032.

The emergence of consumer loyalty programs and rising focus on digital tool integration are the key market opportunities.

BJ's Restaurants Inc., Bloomin' Brands Inc., and Brinker International Inc. are a few key market players.