- Processed Food

- U.S. Hummus Market

U.S. Hummus Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

U.S. Hummus Market by Product Type (Classic, White Bean, Olive, Garlic, Others), Nature (Organic, Conventional), Sales Channel (Hypermarket/Supermarket, Grocery Stores, Convenience Stores, Online Retail, Others), and Regional Analysis from 2026 - 2033

U.S. Hummus Market Share and Trends Analysis

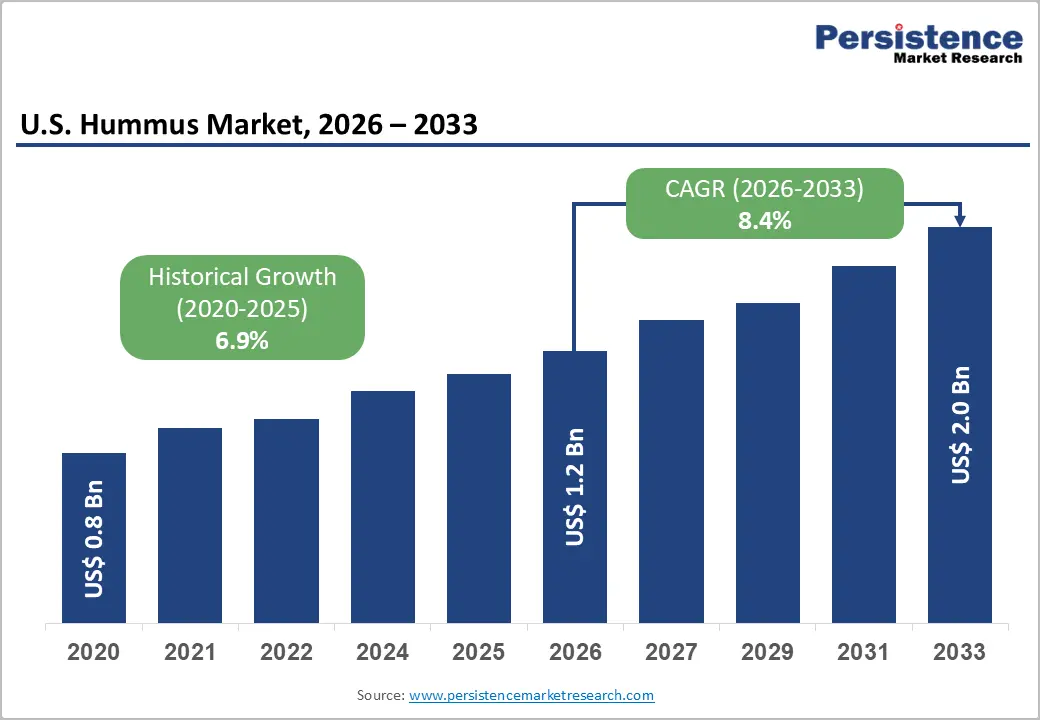

The U.S. hummus market size is likely to be valued at US$ 1.2 billion in 2026 and grow to US$ 2.0 billion by 2033, growing at a CAGR of 8.4% during the forecast period from 2026 to 2033. The rise in global and ethnic cuisine exploration among modern U.S. consumers is anticipated to boost demand during the evaluation period. The popularity of Mediterranean cuisine, especially hummus, has increased dramatically as consumers seek real exotic flavors and ingredients. Companies such as Cedar's and Athenos have jumped on this trend by offering a variety of handmade hummus products inspired by classic Middle Eastern recipes. They have also frequently used premium, organic ingredients to attract consumers.

The proliferation of Mediterranean food trucks and restaurants serving Middle Eastern cuisine has further introduced consumers to hummus in a variety of ways. These places have launched traditional dips as well as promoted its use in gourmet dishes like hummus bowls or as a spread on wraps. In addition to satisfying consumers' growing desire for international flavors, this culinary experiment enhances the market's perception of hummus's authenticity.

Key Industry Highlights

- In terms of nature, the organic hummus segment is likely to dominate at a CAGR of 9.6% by 2033 amid rising demand for ethically sourced food items.

- Based on type, classic hummus is anticipated to lead at a CAGR of 8.2% through 2033, owing to rising preference for its timeless taste.

- Consumers’ appetite for global cuisine fuels interest in Mediterranean foods, making hummus a popular choice in diverse culinary experiences.

- Launch of ready-to-eat and convenient snack options is projected to augment the U.S. hummus market growth by 2033.

- Key players are strengthening their distribution channels, such as online grocery platforms, to meet the rising demand from untapped areas.

- The introduction of functional hummus products enriched with superfoods is projected to help attract health-focused consumers seeking added nutritional benefits.

| Key Insights | Details |

|---|---|

|

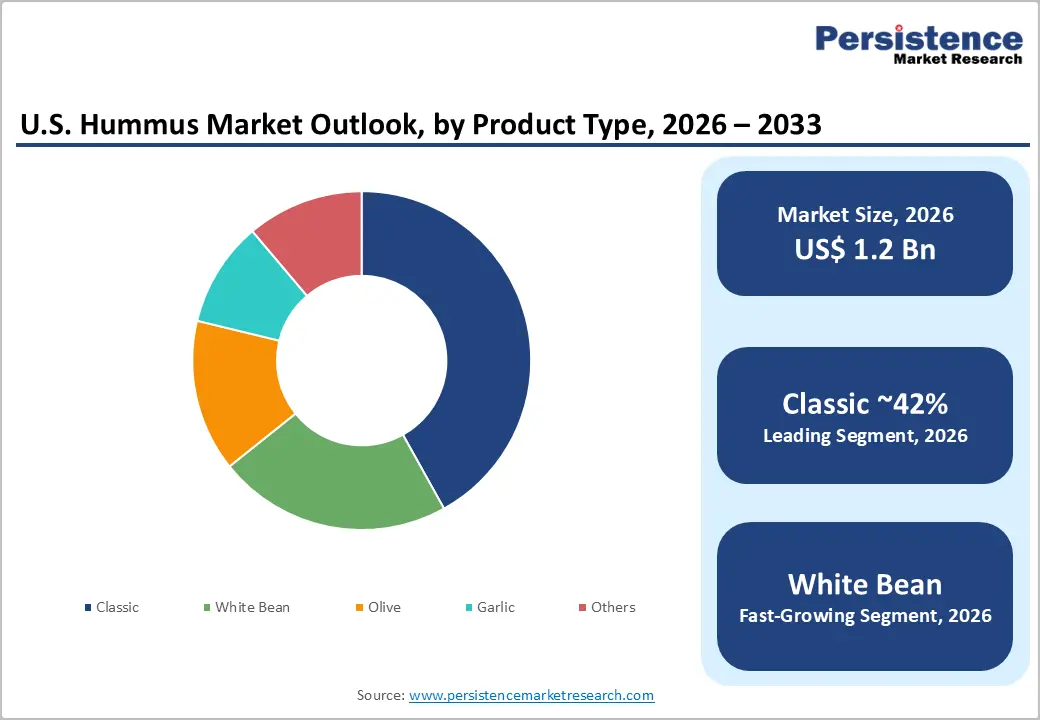

USA Hummus Market Size (2026E) |

US$ 1.2 Bn |

|

Market Value Forecast (2033F) |

US$ 2.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.9% |

Market Dynamics

Driver - Rising Demand for Convenient, On-the-go Snacking Options to Push Sales

As a nutritious, plant-based snack high in protein, fiber, and essential nutrients, hummus attracts a broad consumer base. It appeals especially to those prioritizing fitness, wellness, and healthy lifestyle choices. As snacking increasingly substitutes for traditional meals, whether during a hectic workday or while traveling, hummus has become a preferred option across diverse demographics. Its versatility and satisfying nature make it an ideal pairing with popular dippable items like vegetables, pita chips, and crackers, adding to its appeal as a convenient, energy-sustaining grab-and-go snack.

Manufacturers have enhanced hummus’s portability and convenience through innovative portion-controlled, single-serve packaging. These individual packs appeal to health-conscious consumers. At the same time, these help align with sustainability efforts and cater to consumers who prioritize waste reduction.

Brands have also broadened their flavor offerings in single-serve hummus, introducing varieties such as spicy, garlic, roasted red pepper, and even dessert flavors. This diversification enables a broad consumer reach, addressing diverse taste preferences while reinforcing its position as a versatile, nutritious snacking choice in the evolving market.

Launch of Hummus with Functional Ingredients to Bolster Demand

Hummus has recently gained traction in the U.S. as a functional food with added health benefits beyond basic nutrition. The use of superfoods and nutrient-dense ingredients in hummus recipes, which appeal to consumers seeking more than simply a conventional snack, is driving this trend. For instance,

- U.S.-based companies such as Hope Foods and Lantana have recently launched hummus varieties enhanced with anti-inflammatory and antioxidant-rich ingredients, including kale, beets, and turmeric. These cutting-edge products appeal to consumers concerned about their health and seeking functional foods that support wellness goals such as strengthening immunity or enhancing digestion.

Customers are expected to be drawn to products that offer ingredient transparency and additional health benefits, which supports the demand for specialized hummus. This trend also coincides with the rapid shift toward clean-label products.

Restraints - Competition to be Intense from Plant-based Dips and Spreads

The U.S. hummus market is facing rising competition from a growing variety of plant-based dips and spreads, as consumers increasingly seek options beyond traditional chickpea hummus. Brands are introducing alternatives such as avocado guacamoles, almond and cashew-based dips, black bean spreads, and lentil options. Each of these offers unique flavors, textures, and nutritional profiles that attract consumers seeking to explore new plant-based options.

A few of the alternative products also meet specific dietary needs, such as nut-free, dairy-free, and gluten-free requirements, which have become significant in today’s market. These new offerings challenge hummus’s position as a popular healthy dip. To stay competitive, leading brands must innovate by introducing new flavors, improving ingredient quality, and targeting diverse consumer preferences across the broader plant-based product market.

Opportunity - Brands Target Health-conscious Consumers with Single-serve Options

Hummus is becoming a popular option for health-conscious consumers as demand for high-protein, vegan-friendly choices rise in tandem with the growing popularity of plant-based diets. This change creates opportunities for businesses to go beyond conventional chickpea-based hummus by exploring avocado-, lentil-, or black bean-based options. Substitutes, such as gluten-free or low-carb products, are designed to satisfy both experimental eaters and people with specific dietary requirements.

Rising convenience trends are set to drive high demand for innovative packaging, such as single-serve and on-the-go formats, as well as snack packs with vegetables or crackers. These formats suit active lifestyles and align with the booming snacking culture across the U.S. Furthermore, as sustainability becomes a central consumer concern, companies can adopt eco-friendly packaging and sustainable ingredient sourcing. These mainly appeal to environmentally conscious buyers who prioritize responsible consumption.

Category-wise Analysis

By Product Type Insights

By product type, classic hummus is expected to dominate the U.S. market throughout the forecast period, supported by its widespread consumer acceptance and consistent demand across retail and foodservice channels. Prepared using core ingredients such as chickpeas, tahini, olive oil, garlic, and lemon juice, classic hummus offers a clean and familiar flavor profile that appeals strongly to younger consumers seeking simple, wholesome foods. Its mild taste and smooth texture make it easy to pair with vegetables, pita bread, sandwiches, and snack crackers, making it a convenient and versatile dietary staple.

Classic hummus has also benefited from the growing mainstream adoption of Mediterranean-inspired diets in the U.S., where hummus has transitioned from a niche ethnic food to an everyday snack. While innovation in flavored and specialty variants continues to expand shelf space, the traditional version remains a preferred choice due to its perceived nutritional value, plant-based protein content, and minimal ingredient complexity. Millennials in particular favor classic hummus for its balance of taste, health attributes, and ease of incorporation into daily meals, reinforcing its leading position within the product type segment.

By Nature Insights

The organic hummus segment in the U.S. market is gaining traction as modern consumers increasingly choose foods made without synthetic additives, pesticides, and GMOs, seeking greater transparency and sustainable sourcing. This shift aligns well with the broader health and wellness movement, where shoppers prioritize products perceived as healthier and more environmentally responsible. Reflecting this trend, the organic hummus category is expected to grow at a CAGR of around 9.6% through 2033, outpacing conventional variants as demand rises for clean-label, ethically produced food options.

U.S. brands are responding by expanding organic hummus offerings in multiple flavor profiles to attract a broader consumer base. The U.S. Department of Agriculture’s organic certification plays a significant role in purchase decisions by assuring quality and authenticity, which helps build consumer confidence. Organic hummus often carries a premium price, appealing to health-conscious and affluent buyers who value both taste and quality. As organic foods continue to become central in the health food sector and plant-based snacking trends, the organic hummus market in the U.S. is anticipated to grow significantly, driven by evolving consumer values and preferences for sustainable and nutritious products.

Competitive Landscape

The U.S. hummus market is moderately concentrated, with a few leading national brands complemented by regional players, private labels, and specialty producers. Historically, Sabra—a joint venture between PepsiCo and Strauss Group has held the largest share, though recent years have seen competition rising from brands such as Cedar’s Mediterranean Foods, Inc., Lakeview Farms, LLC, Hope Foods, LLC, and supermarket private labels. Key competitive differentiators include flavor innovation, product positioning (traditional vs. bold flavors), organic and clean-label credentials, and the ability to maintain consistent quality and shelf life across national distribution. Leading players also invest in marketing campaigns highlighting Mediterranean diet benefits, partnerships with retailers for in-store promotions, and expansion into adjacent categories such as refrigerated snack kits and bean-based dips.

Key Industry Developments:

- In April 2024, Washington-based Little Sesame Inc. successfully raised US$ 3 Mn from venture groups, fueling its growth and expansion efforts. This three-year-old consumer packaged goods brand specializes in fresh hummus made from organic chickpeas and counts Whole Foods among its investors.

- In October 2023, New York-based popular hummus maker, Sabra Dipping Company, LLC introduced Mediterranean Roasted Garlic and Spicy Harissa for Target stores and Amazon Fresh.

- In June 2023, Hope Foods, headquartered in Colorado, launched bold new packaging for its organic hummus and non-GMO plant-based dips. These were designed to highlight the vibrant flavors and underscore its Plastic Neutral certification.

Companies Covered in U.S. Hummus Market

- Lakeview Farms, LLC

- Hope Foods, LLC

- Zacca Hummus

- Boar’s Head Brand

- Nestlé S.A.

- Haliburton International Foods, Inc.

- Bakkavor Group Plc

- Strauss Group

- Cedar’s Mediterranean Foods, Inc.

- Lantana Foods

- Others

Frequently Asked Questions

The U.S. hummus market is projected to be valued at US$ 1.2 Bn in 2026.

Rising demand for plant-based snacks, clean-label foods, Mediterranean diets, and convenient protein-rich options among health-conscious consumers.

The global market is poised to witness a CAGR of 8.4% between 2026 and 2033.

Product innovation in organic and functional variants, expanding foodservice adoption, private-label growth, and penetration into mainstream convenience retail channels.

Lakeview Farms, LLC and Nestlé S.A. are a few leading brands in the U.S.