- Food Ingredients & Additives

- U.S. Egg Replacement Market

U.S. Egg Replacement Market Size, Share, and Growth Forecast, 2025 - 2032

U.S. Egg Replacement Market By Ingredient Type (Plant-protein Blends, Polysaccharide/Starch/Hydrocolloids-based, Legume-based), Application (Bakery and Confectionery, Convenience Foods), Distribution Channel, and Analysis for 2025 - 2032

U.S. Egg Replacement Market Size and Trends Analysis

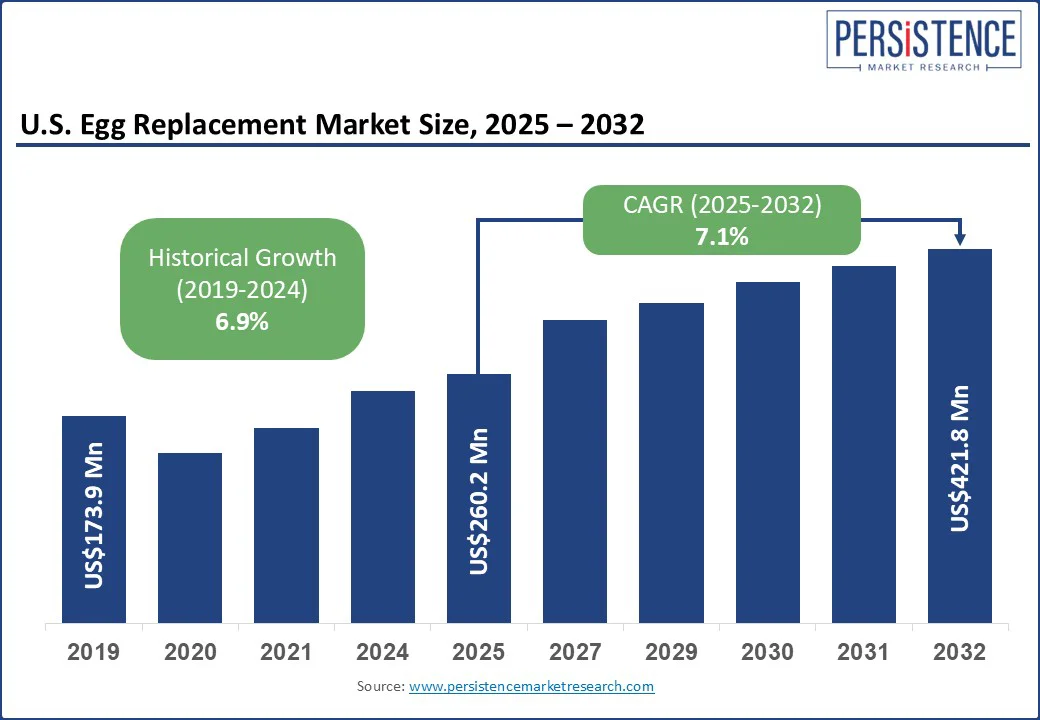

The U.S. egg replacement market size is projected to rise from US$260.2 Mn in 2025 to US$421.8 Mn by 2032. It is anticipated to witness a CAGR of 7.1% during the forecast period from 2025 to 2032.

The U.S. egg replacement industry growth is driven by increasing demand from vegans and allergy-sensitive consumers. Rising egg prices following avian flu outbreaks, as well as increasing scrutiny over cholesterol and animal welfare, have further spurred demand across bakery, convenience food, and foodservice segments.

Key Industry Highlights

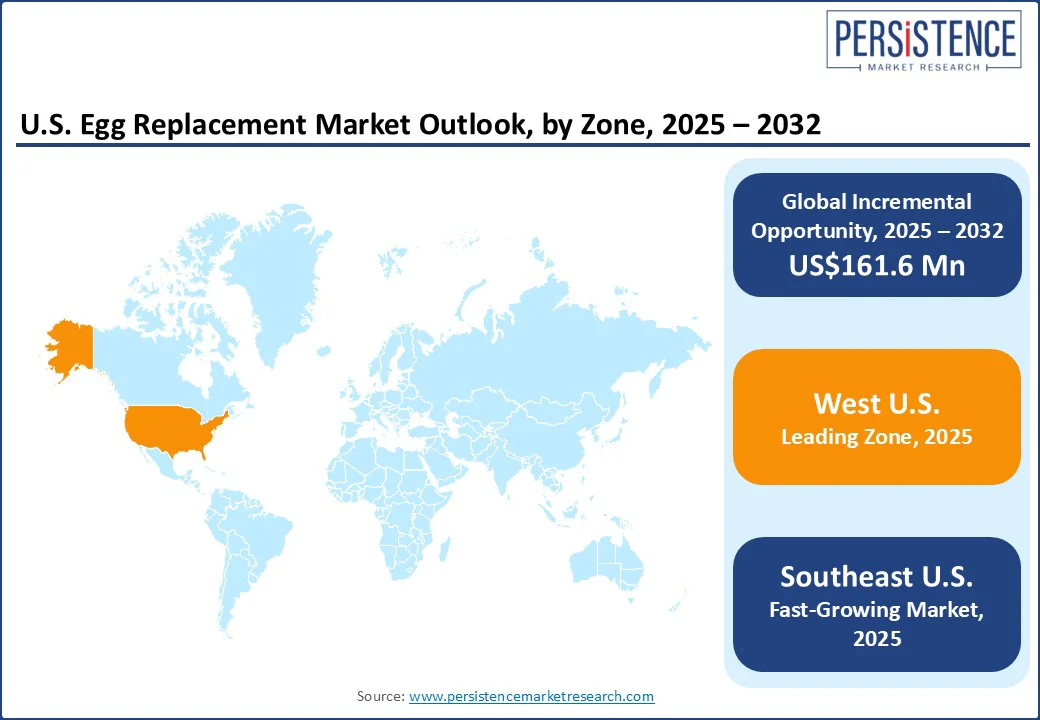

- Leading Zone: West U.S. to remain at the forefront owing to the high concentration of plant-based start-ups in California.

- Fastest-growing Zone: The Southeast U.S. is expected to achieve the fastest growth, driven by the increasing adoption of replacers to stabilize production among cost-sensitive bakeries and frozen food producers.

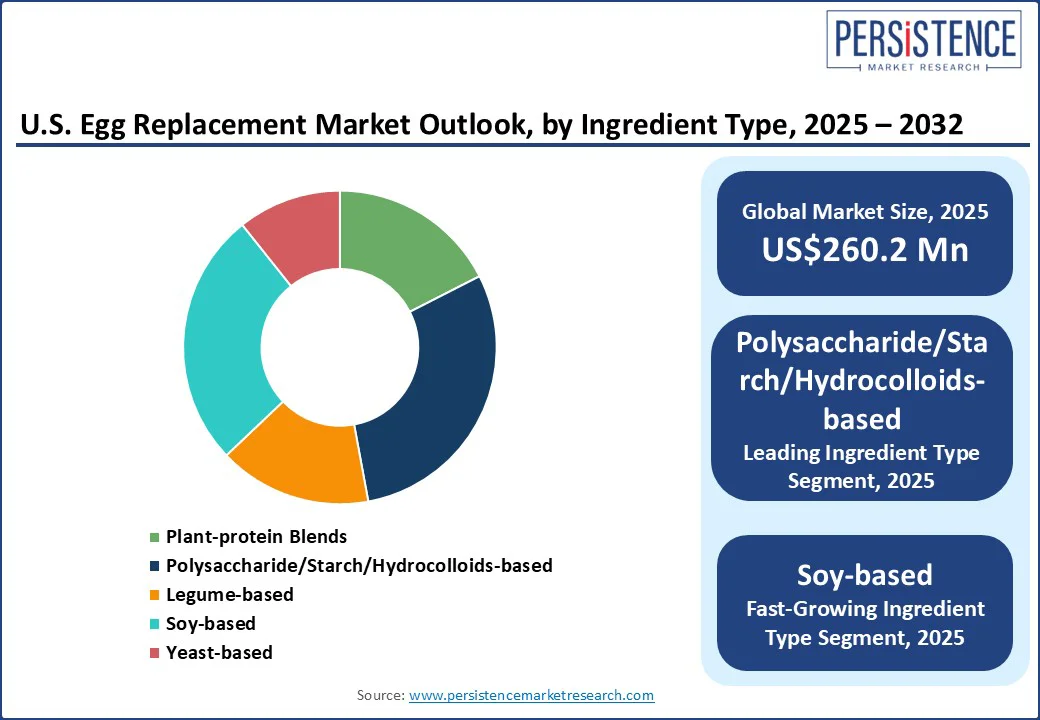

- Dominant Ingredient Type: Polysaccharide/starch/hydrocolloids-based egg replacers are projected to hold approximately 29.6% of the market share in 2025, augmented by the emergence of legume-based replacers that provide protein functionality closer to real eggs.

- Leading Application: Bakery and confectionery projected to account for nearly 27.2% market share in 2025, due to egg price volatility, which has made bakery producers the first to adopt stable alternatives.

- New Product Launch: Crespel & Deiters Food USA developed a plant-based egg replacement option called Lory Stab for baked goods in April 2025. The replacer is a compound of technically treated raw materials that help maintain dough stability.

|

Global Market Attribute |

Key Insights |

|

U.S. Egg Replacement Market Size (2025E) |

US$260.2 Mn |

|

Market Value Forecast (2032F) |

US$421.8 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.9% |

Market Dynamics

Driver - Health Risks of Cholesterol in Eggs Propel Demand

Rising concerns about obesity and cardiovascular diseases linked to animal-based products are spurring the shift toward egg replacements in the U.S. Consumers and health organizations have become more aware of the ill effects of eggs after scrutinizing the cholesterol and saturated fat content of eggs.

A single chicken egg contains about 186 mg of cholesterol, concentrated in the yolk, which has long been associated with high LDL cholesterol levels. For populations already struggling with obesity, healthcare professionals are recommending plant-based alternatives that mimic eggs’ functionality without the cholesterol burden.

The trend is augmented by consumer demand for heart-healthy convenience foods. U.S.-based brands are responding by explicitly marketing egg-free products as cholesterol-free and lower in calories, targeting weight-conscious buyers.

For example, in 2024, JUST Egg highlighted clinical findings in its campaigns, positioning its mung bean-based scramble as cholesterol-free. Similarly, Follow Your Heart promoted its vegan egg replacer as part of a lifestyle choice for consumers managing hypertension or high cholesterol. These marketing strategies align with the rising popularity of plant-based diets recommended by cardiology associations.

Restraint - Sensory Limitations Restrict Adoption in Baking and Confectionery Applications

Nutritional differences remain a key barrier to adoption in the U.S., as many consumers still see eggs as a compact source of complete protein, vitamins A, D, and B12, and essential minerals such as selenium. While some replacements provide protein through soy or mung bean isolates, they rarely match the amino acid completeness of eggs without fortification. This creates skepticism among health-conscious buyers who want functional plant-based choices but are unwilling to compromise on nutrient density.

Sensory challenges also slow wide adoption, specifically in segments where eggs are used for aeration and mouthfeel. Functional limitations are evident in professional baking and confectionery. Current replacers often have to be used in combination to achieve functional properties, adding complexity and cost for manufacturers. This inconsistency discourages small firms lacking dedicated R&D from adopting egg replacement ingredients.

Opportunity - Lightweight and Stable Formats Cater to Large-scale Food Manufacturing

The rise of powdered egg replacements is creating new opportunities in the U.S. by addressing shelf-life, storage, and formulation challenges that liquid or fresh alternatives cannot easily solve. Powdered forms are lightweight, stable at room temperature, and easy to transport. This makes egg replacements ideal for large bakeries, food manufacturers, and humanitarian supply chains, where refrigeration is limited. These are also expanding into the meal-kit and home-baking segments, where convenience and portion control are highly valued.

Unlike liquid alternatives, which must be consumed shortly after opening, powdered versions offer greater convenience and shelf stability. The increasing popularity of DIY meal kits further creates avenues for powdered replacers to be included as pre-measured sachets, reducing the complexity of recipes while ensuring a consistent outcome for consumers.

These replacers allow smooth incorporation of added nutrients such as omega-3s and vitamin B12, making them more nutritionally competitive with conventional eggs.

Category-wise Analysis

Ingredient Type Insights

Based on ingredient type, the market is divided into plant-protein blends, polysaccharide/starch/hydrocolloids-based, legume-based, soy-based, and yeast-based. Among these, the polysaccharide/starch/hydrocolloids-based egg replacers are predicted to account for nearly 29.6% of the market share in 2025, due to their functional versatility in food applications. These ingredients often mimic the textural, binding, and emulsifying properties of eggs without relying on animal sources. It makes them ideal for vegan, vegetarian, and egg-allergic consumers.

Soy-based egg replacements are gaining impetus as they provide a protein profile and functional performance that closely resembles real eggs. It makes them attractive for food manufacturers and consumers seeking plant-based options.

Soy proteins also deliver foaming, emulsification, and gelling, which are essential for products such as meringues, mousses, and bakery items where aeration is important. This versatility gives soy a competitive advantage in applications that require eggs, not just for structure but also for their protein-backed chemical interactions during cooking.

Application Insights

By application, the market is segregated into bakery and confectionery, convenience foods, sauces and salad dressings, dairy and frozen desserts, and other processed foods. Out of these, bakery and confectionery will likely hold around 27.2% of the U.S. egg replacement market share in 2025, as eggs perform multiple roles simultaneously, including binding, leavening, emulsification, moisture retention, and aeration, which are important in baked goods and sweets.

Cakes, cookies, and pastries collapse or lose volume without proper leavening, while confectionery items rely on foam stability that egg whites traditionally provide. Egg replacements made for this industry replicate these functions, often blending starches, proteins, and hydrocolloids in custom blends to deliver the required lift.

Convenience foods are a key application area as this segment demands ingredients that are consistent, cost-effective, and safe across large-scale processing and long distribution chains. Ready-to-eat meals, frozen snacks, and instant mixes often rely on eggs for binding, texture, and color.

However, liquid or powdered egg ingredients tend to pose storage and contamination risks. Plant-based or starch-hydrocolloid products are easy to transport, have longer shelf lives, and reduce the requirement for strict cold-chain logistics. For manufacturers producing frozen burritos or instant baking mixes, this stability translates into low overhead costs.

Zone Insights

West U.S. Egg Replacement Market Trends - California Emerges as a Hub for Alternative Protein Development

In the West, egg replacements are moving from niche vegan products into mainstream food manufacturing as consumer demand and supply chain risks converge. The zone saw egg price volatility from 2022 to 2023 due to avian flu outbreaks, which compelled large bakeries, confectioners, and ready-meal producers to adopt alternatives. This shift was not temporary, but once manufacturers tested starch, soy, and pea protein solutions, many retained them as permanent partial replacements to hedge against future volatility.

California has become a testing ground for alternative proteins. Start-ups and food-tech accelerators in San Francisco and Los Angeles are piloting egg-free solutions across retail and foodservice channels.

Brands, including San Francisco-based JUST Egg, have used the West Coast as their launchpad, first supplying local restaurants and grocers before expanding nationwide. The zone’s dense population of flexitarians and higher-than-average vegan adoption rates also provide an immediate consumer base that is receptive to egg substitutes in everyday foods.

Southeast U.S. Egg Replacement Market Trends - B2B Ingredient Suppliers Lead Expansion into Frozen Meals and Baked Goods

In the Southeast U.S., the market is boosted by affordability, allergy concerns, and resilience against egg supply volatility. Georgia, North Carolina, and Arkansas have a heavy reliance on poultry farming. The recurring impacts of avian flu outbreaks have made foodservice operators and regional packaged food brands more open to experimenting with egg alternatives to stabilize procurement. Momentum in the Southeast U.S. is B2B-led, with domestic ingredient suppliers and co-packers pushing egg replacement blends into frozen meals, dough mixes, and private-label baked goods.

The zone is also witnessing a gradual uptake in school and institutional food programs, where allergy management and nutrition guidelines play a key role. The Southeast further reports higher childhood egg allergies compared to the national average. Hence, schools in Florida and South Carolina have begun testing starch-protein replacers in pancakes, muffins, and sauces to reduce allergen risks while maintaining student acceptance.

Northeast U.S. Egg Replacement Market Trends - Universities Pioneer Plant-based Egg Use through Dining Hall Programs

In the Northeast U.S., the market is being propelled by the zone’s rising concentration of health-conscious consumers, dense urban populations, and a well-established specialty food culture. New York, Boston, and Philadelphia are at the forefront with cafés, bakeries, and restaurant groups actively experimenting with plant-based formulations to meet the expectations of younger demographics. Several New York-based bagel shops have started using starch- and soy-based replacers in their breakfast sandwiches to capture flexitarian customers without alienating traditional eaters.

The Northeast also leads in university-driven adoption. Large institutions, including Harvard, NYU, and Cornell, have added plant-based egg alternatives to their dining halls. These are often sourced from regional start-ups or suppliers piloting new blends. Another unique driver is regulatory and consumer pressure around sustainability and welfare. States such as Massachusetts have enacted stringent cage-free and animal welfare legislation, pushing food manufacturers and retailers to diversify beyond conventional eggs.

Competitive Landscape

The U.S. egg replacement market consists of retail scramble brands, baking-mix pantry replacers, B2B ingredient suppliers, and precision-fermentation start-ups. Retail brands anchor the consumer segment, while classic pantry replacers dominate the home-baking. Ingredient suppliers are influencing commercial reformulations.

A new competitive pressure comes from precision fermentation, which aims to provide egg proteins without hens and with fewer formulation trade-offs. Market power is concentrated in two areas: consumer brands that drive demand at retail, and ingredient suppliers that support reformulation at the manufacturing level.

Key Industry Developments

- In August 2025, U.K.-based plant-based egg brand Crackd, maker of The No-Egg Egg, successfully secured distribution in its first group of U.S. grocery stores. Crackd is now available in Chicago at Jewel-Osco markets, as well as in Dallas, Houston, Austin, and other key cities across Texas.

- In March 2025, BreadPartners, Inc., based in Cinnaminson, introduced a new complete egg substitute in all yeast-raised doughs called Naturell Soleil. It is non-GMO, free from common allergens, and helps maintain essential properties such as emulsification and color.

Companies Covered in U.S. Egg Replacement Market

- Puratos

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Fiberstar, Inc.

- All American Foods, Inc.

- Natural Products, Inc.

- Manildra Group USA

- Devansoy Inc.

- J&K Ingredients, Inc.

- Ingredion Inc.

Frequently Asked Questions

The U.S. egg replacement market is projected to reach US$ 260.2 Mn in 2025.

Rising egg prices due to avian flu outbreaks and expanding flexitarian populations are the key market drivers.

The U.S. egg replacement market is poised to witness a CAGR of 7.1% from 2025 to 2032.

Private-label expansion in major retailers such as Wegmans and the launch of fortified powdered blends with added vitamins are the key market opportunities.

Puratos, Cargill, Incorporated, and Archer Daniels Midland Company (ADM) are a few key market players.