- Food Ingredients & Additives

- U.S. Potato Flour Market

U.S. Potato Flour Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Potato Flour Market by Nature (Organic, Conventional), by Processing Method (Drum-Dried, Air-Dried, Freeze-Dried), by End Use (Bakery & Baking Mixes, Snacks & Extruded Foods, Soups, Sauces & Gravies, Meat Processing & Breading, Gluten-Free & Clean-Label Foods, Others), and by Regional Analysis, 2026-2033

U.S. Potato Flour Market Size and Share Analysis

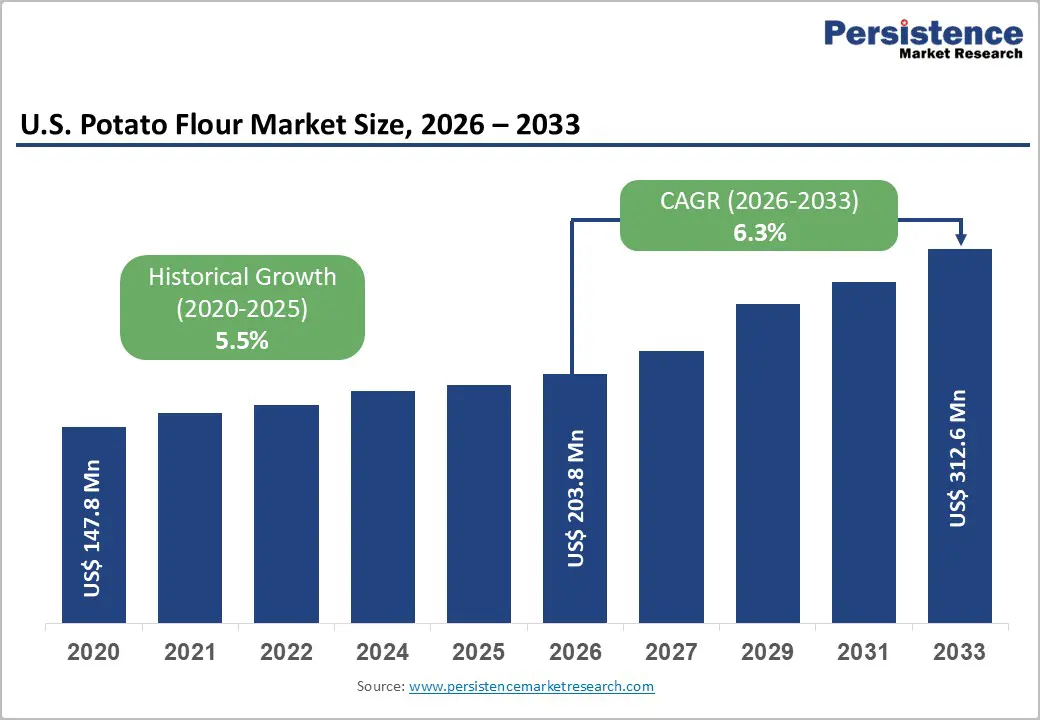

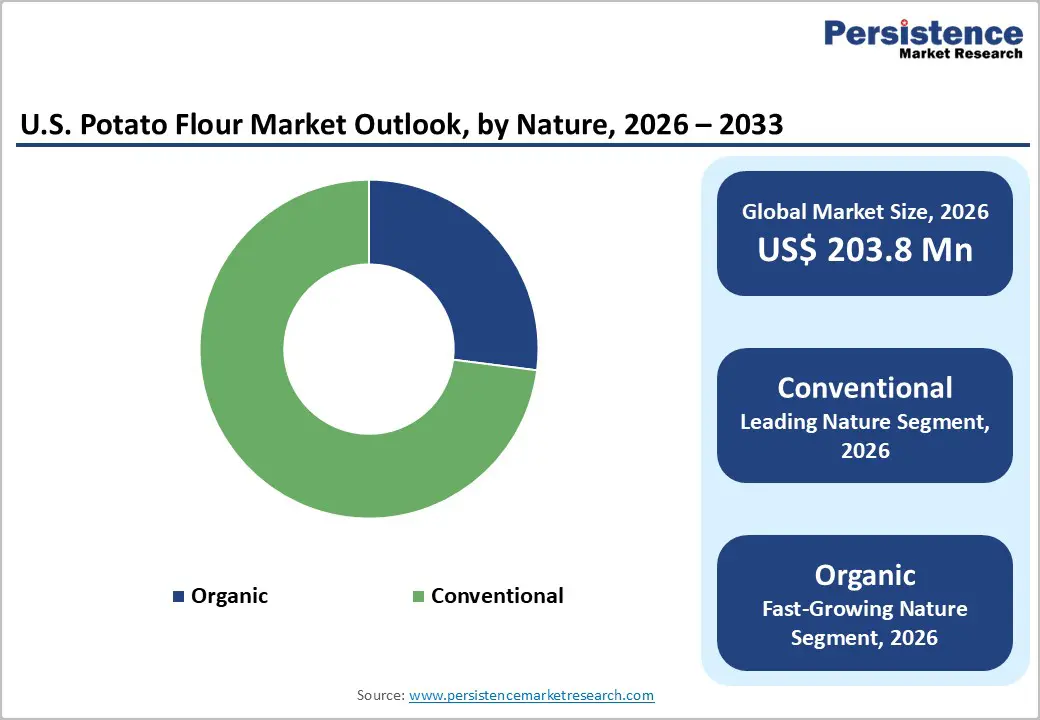

The U.S. potato flour market size is expected to be valued at US$ 203.8 million in 2026 and projected to reach US$ 312.6 million by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The U.S. potato flour market is moving from a commodity ingredient to a strategic functional solution, driven by gluten-free demand, clean-label reformulation, and expanding use in next-generation foods. Its role is deepening across bakery, snacks, and plant-based innovation, not just as a filler but as a performance ingredient.

Key Industry Highlights

- Fastest-Growing Application Area: Plant-Based Meat & Functional Foods, fueled by potato flour’s superior binding, moisture retention, and texture-enhancing properties in vegan and high-protein formulations.

- Dominant Product Segment: Conventional Potato Flour, holding around 73% share due to cost efficiency, scalability, and widespread adoption by industrial bakery, snack, and foodservice manufacturers.

- Fastest-Growing Product Segment: Organic Potato Flour, supported by rising consumer willingness to pay premiums for non-GMO, chemical-free, and sustainably sourced ingredients.

- Market Drivers: Rising demand for gluten-free, allergen-friendly, and clean-label foods is pushing manufacturers to replace wheat and chemically modified starches with naturally processed potato flour.

- Opportunities: Expanding use in plant-based meats, high-fiber bakery blends, and functional food formulations positions potato flour as a critical ingredient for future food innovation.

- Key Developments: In November 2025, SolEdits and Lyckeby announced plans to launch CRISPR-edited potatoes designed to deliver chemical-free, storage-stable starch, signaling a technological shift in potato-based ingredient performance and supply stability.

| Report Attribute | Details |

|---|---|

|

Global Potato Flour Market Size (2026E) |

US$ 203.8 Mn |

|

Market Value Forecast (2033F) |

US$ 312.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

Market Dynamics

Driver

Rising Demand for Gluten-Free and Clean-Label Food Products

The primary driver of the U.S. Potato Flour Market is the accelerating consumer shift toward gluten-free and allergen-friendly dietary patterns. As of 2024, approximately 34% of global consumers reported a preference for food products labeled as gluten-free, a trend that is particularly pronounced in North America. In the United States, industrial food producers utilized over 64,000 metric tons of potato flour in gluten-free bakery and snack production in the previous year alone. Organizations like the U.S. Food and Drug Administration (FDA) and the United States Department of Agriculture (USDA) have observed a steady rise in the consumption of processed potato products as manufacturers seek ingredients that satisfy "clean-label" requirements. Potato flour, being a naturally processed and chemical-free ingredient, perfectly aligns with these expectations, leading to its inclusion in over 51% of new bakery product launches in 2024.

Expanding Applications in the Bakery and Snack Industries

The multi-functional nature of potato flour as a binding and texturizing agent significantly bolsters its adoption across the industrial food sector. More than 40% of all potato flour produced in the United States is currently utilized as a critical ingredient in the bakery sector, where it helps retain moisture and provides a soft, consistent texture to bread and pastries. The snacks and extruded foods segment is also a major contributor, as the flour serves as a superior thickener and flavor enhancer. The American food processing industry, supported by technological advancements in dehydration techniques, has enhanced the quality and consistency of potato-based ingredients, making them attractive to large-scale manufacturers like Idaho Pacific Holdings and Basic American Foods. This industrial demand is further propelled by the growth of the quick-service restaurant sector, which requires stable, easily prepared ingredients for high-volume operations

Restraints

Fluctuation in Raw Material Prices and Production Complexity

The production of potato flour is a more labor-intensive and complex process compared to other flour types, involving multiple stages of dehydration and milling. Furthermore, the market is highly vulnerable to the volatility of farm-gate potato prices, which are influenced by climate variability and weather shocks. Irregular rainfall and shifting temperature patterns in key potato-growing regions, such as the Pacific Northwest, can disrupt yields and lead to unstable supply conditions. These supply chain challenges, often exacerbated by rising transportation and energy costs, force manufacturers to navigate a volatile cost environment. High production and procurement costs can compress profit margins for millers and may lead to higher retail prices, potentially suppressing demand among price-sensitive consumers.

Opportunity

Growing Potential in Plant-Based Meat and Functional Food Sectors

The rapid expansion of the plant-based meat industry presents a lucrative opportunity for potato flour manufacturers due to its exceptional moisture-retention and binding properties. In 2023, over 145 registered plant-based meat products utilized potato flour as a key binding agent to improve texture and succulence. As consumers increasingly perceive plant-based products as safer and healthier, demand for functional ingredients like potato flour is expected to surge. Companies such as King Arthur Baking Company and Bob’s Red Mill Natural Foods are well-positioned to capitalize on this trend by developing specialized formulations that cater to vegan and vegetarian demographics. Additionally, the integration of potato flour in high-protein and fiber-rich specialty blends aligns with the wellness-oriented preferences of modern consumers.

Category-wise Analysis

Nature Analysis

The Conventional segment holds the leading position in the U.S. Potato Flour Market, capturing a dominant 73% market share in 2025. This market leadership is primarily attributed to its cost-efficiency, broad commercial availability, and wide adoption across industrial food processing applications. Conventional potato flour is the preferred choice for large-scale manufacturers of bakery products, snacks, and convenience foods who require consistent functional performance at an affordable price point. However, the Organic segment is recognized as the fastest-growing category, projected to expand at a significant CAGR between 2025 and 2033. This growth is fueled by an escalating consumer preference for chemical-free, non-GMO, and sustainably sourced ingredients. Rising awareness of health and environmental issues has led many households to pay a premium for organic variants, encouraging companies like Carrington Farms and Authentic Foods to expand their organic product portfolios.

End Use Analysis

The Food Industry, particularly the Bakery & Baking Mixes and Snacks & Extruded Foods segments, accounts for the largest revenue stream in the potato flour market. In the United States, the food industry held a major value share of 64.1% in recent years, with the Bakery sector alone accounting for more than 40% of total consumption. Potato flour is prized in these applications for its ability to improve the crumb structure of bread and the crunch of extruded snacks. The Gluten-Free & Clean-Label Foods segment is the fastest-growing end-use category, driven by the increasing diagnosis of celiac disease and gluten intolerance, which affects approximately 7.1% of the global population. Additionally, the Foodservice sector is witnessing steady growth, as restaurants and quick-service establishments utilize potato flour for breading, thickening soups and sauces, and enhancing the flavor profile of various menu items.

Market Competitive Landscape

The U.S. Potato Flour Market is characterized by a moderate level of concentration, with a small number of large multinational corporations and specialized regional players dominating the production landscape. Top-tier producers and leaders maintain their market positions through strategic investments in high-capacity milling facilities, robust distribution networks, and continuous R&D in functional flour innovations. Strategies such as mergers, acquisitions, and partnerships are frequently employed to consolidate market share and enter emerging markets. Meanwhile, smaller, specialty-focused companies like Bob’s Red Mill Natural Foods and Authentic Foods differentiate themselves through product premiumization, organic certifications, and a focus on the retail and gluten-free consumer segments.

Key Developments:

- In November 2025, SolEdits and Lyckeby announced they are poised to launch CRISPR-edited potatoes designed to produce chemical-free, storage-stable starch, representing a significant innovation in crop biotechnology and ingredient performance.

- In October 2024, EarthFresh acquired Mountain King Potatoes, significantly widening its U.S. retail distribution and strengthening its supply chain for potato-based products.

Companies Covered in U.S. Potato Flour Market

- Bob’s Red Mill Natural Foods

- Idaho Pacific Holdings

- King Arthur Baking Company

- Emsland Group

- AGRANA Beteiligungs‑AG

- Basic American Foods

- American Key Food Products

- Authentic Foods

- Carrington Farms

- Oregon Potato Company

- Others

Frequently Asked Questions

The U.S. potato flour market is currently valued at US$ 106.8 Mn.

Increasing demand from the food industry, rising demand for natural food products that provide multiple health benefits, strong preference for gluten-free products, and increasing consumption of potato flour in retail/household are factors driving market expansion.

From 2017 to 2021, demand for potato flour in the U.S. increased at a CAGR of 5.9%.

Sales of potato flour in the U.S. are projected to increase at 6.4% CAGR and reach US$ 198.1 Mn by the end of 2032.

Bob’s Red Mill Natural Foods, Idaho Pacific Holdings, Edward & Sons Trading Co., Kipuka Mills, Authentic Foods, and King Arthur Baking Company are prominent potato flour producers in the U.S.