- Agrochemicals

- Organic Fertilizer Market

Organic Fertilizer Market Size, Share, and Growth Forecast 2026 - 2033

Organic Fertilizer Market by Product Source (Animal-Based, Plant-Based, Mineral-Based), Product Form (Granules, Powder, Liquid), Crop Type (Cereals and Grains, Fruits and Vegetables, Oilseeds and Pulses, Turf and Ornamentals, Miscellaneous), End User (Farmers/Growers, Horticulture, Landscaping and Golf Courses, Home Gardening), by Regional Analysis, 2026 - 2033

Organic Fertilizer Market Size and Trend Analysis

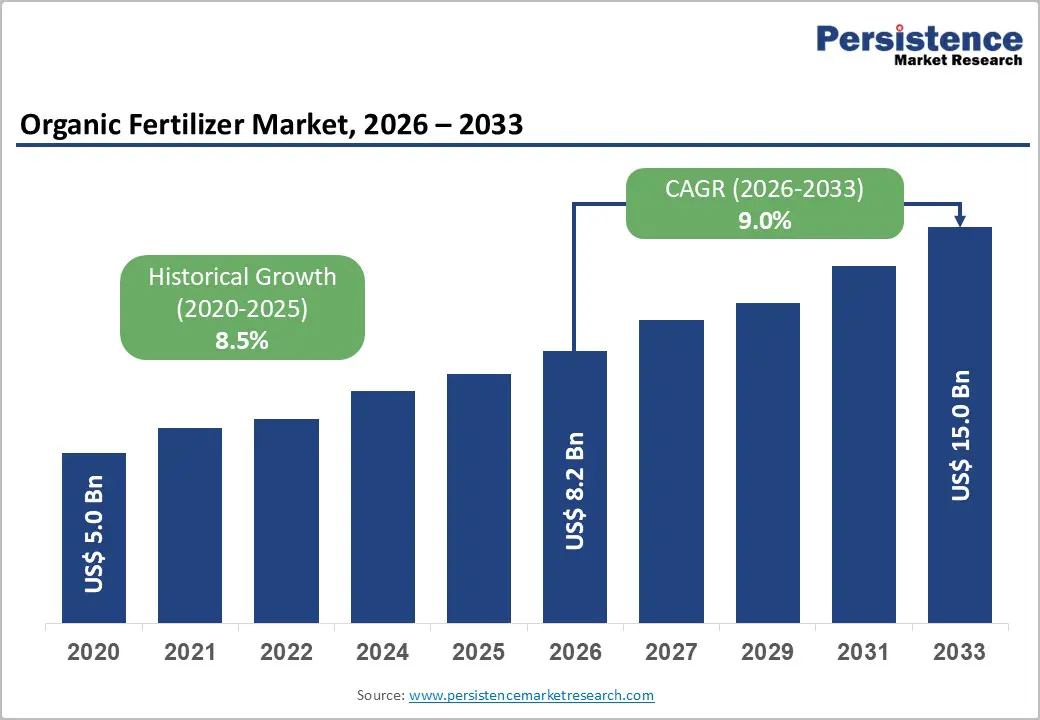

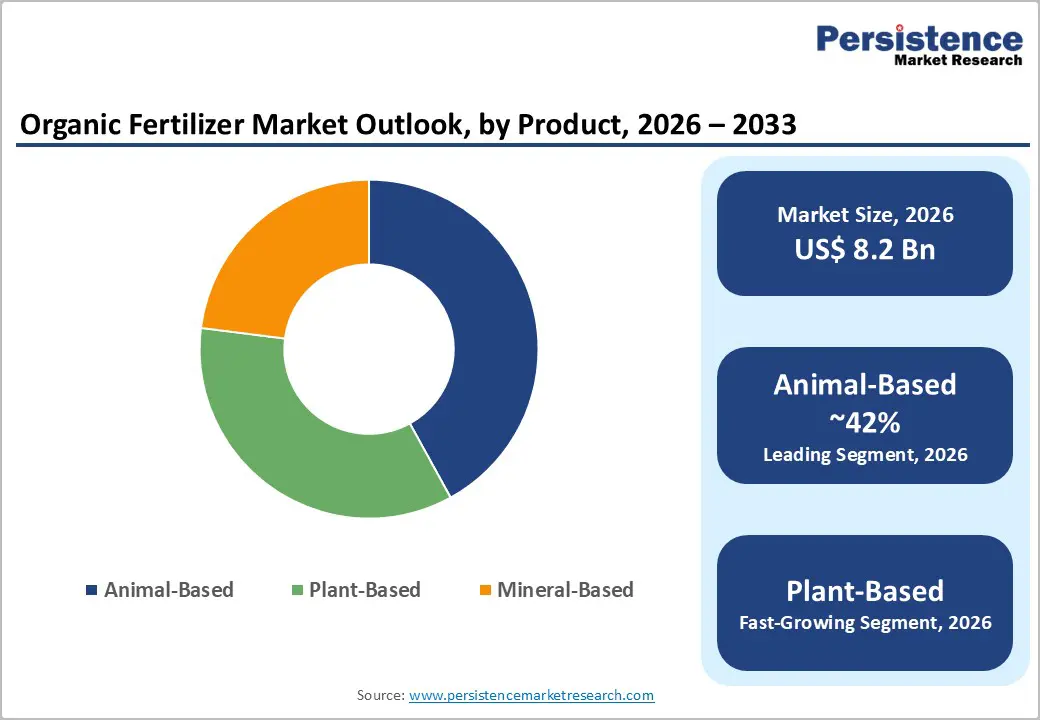

The global organic fertilizer market size is expected to be valued at US$ 8.2 billion in 2026 and projected to reach US$ 15.0 billion by 2033, growing at a CAGR of 9.0% between 2026 and 2033. This robust growth is primarily fueled by accelerating global adoption of sustainable agricultural practices, stringent government regulations on synthetic fertilizer use, and heightened consumer demand for organically produced food.

The market is further accelerated by expanding organic farmland, growing food safety awareness, and supportive policy frameworks across major agricultural economies.

Key Industry Highlights

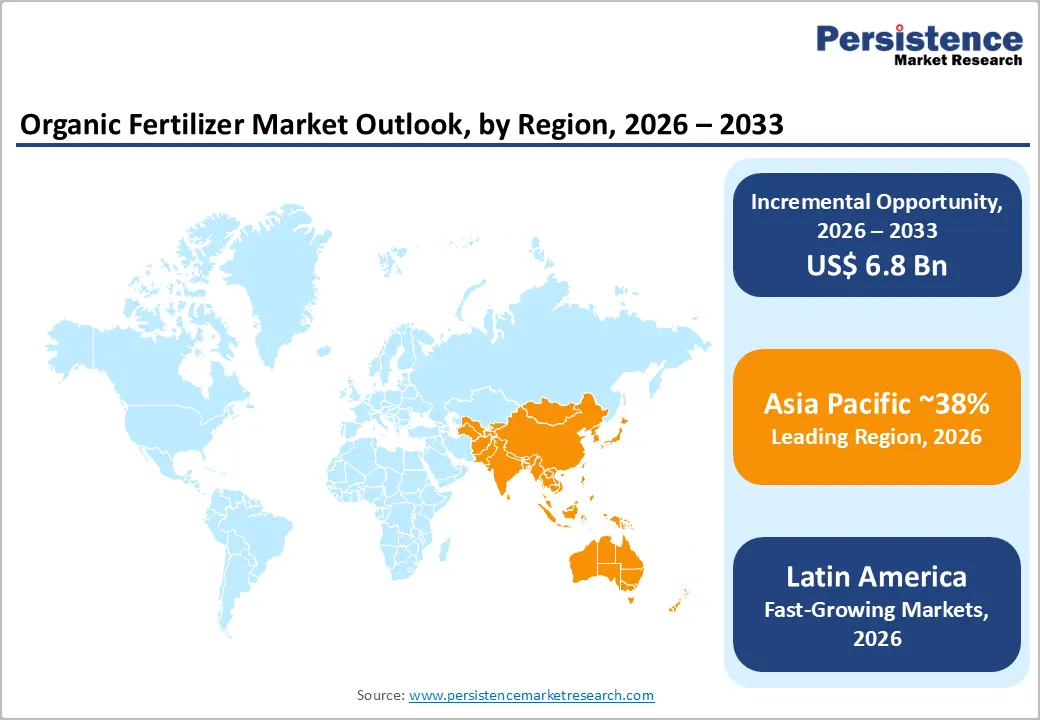

- Leading Region: Asia Pacific: Asia Pacific dominates the global organic fertilizer market with approximately 38% market share in 2026, driven by large-scale organic farming initiatives in China and India, government subsidies, and abundant raw material availability.

- Fastest Growing Region: Latin America is projected to be the fastest growing region at a CAGR of 11.2%, propelled by rising organic export certifications in Brazil and Argentina and expanding agroecological farming policies.

- Dominant Segment: Animal-Based (Product Source): Animal-based organic fertilizers lead with 42% share in 2026, benefiting from high nutrient content, abundant livestock byproduct availability, and strong adoption in commercial horticulture and intensive cropping systems.

- Fastest Growing Segment: Liquid Form (Product Form): Liquid organic fertilizers represent the fastest growing form segment, driven by precision fertigation systems, urban agriculture adoption, and high compatibility with greenhouse and vertical farming operations.

- Key Market Opportunity: Urban Agriculture & Biofortification: Integration of microbial inoculants and biostimulants with organic fertilizers, alongside the expansion of urban and controlled-environment agriculture, presents the highest-growth commercial opportunity for market participants through 2033.

DRO Analysis

Market Growth Drivers

Rising Global Adoption of Organic Farming Practices

The surge in organic farming worldwide is one of the most prominent catalysts driving demand for organic fertilizers. According to the Research Institute of Organic Agriculture (FiBL) and IFOAM, Organics International, the global organic agricultural land reached approximately 76.4 million hectares in recent reporting years, with over 3.7 million organic producers operating globally.

The European Union's Farm to Fork Strategy targets 25% of farmland under organic management by 2030, while India's Paramparagat Krishi Vikas Yojana (PKVY) has incentivized organic conversion across millions of smallholder farms. Such large-scale shifts from conventional to organic cultivation directly expand the addressable market for organic fertilizers, creating consistent, long-term demand for products derived from animal, plant, and mineral sources.

Stringent Regulations on Synthetic Fertilizers and Growing Food Safety Awareness

Regulatory pressure on synthetic chemical fertilizers continues to intensify globally, directly benefiting the organic fertilizer segment. The European Green Deal and its associated Farm to Fork Strategy mandate a 20% reduction in fertilizer use and a 50% reduction in the use of more hazardous pesticides by 2030.

In parallel, the U.S. Environmental Protection Agency (EPA) continues to tighten nutrient management guidelines to address nitrate runoff and soil degradation. Consumer awareness of pesticide residues in food, combined with the rapid growth of certified organic food retail, valued at over US$ 130 billion globally per Organic Trade Association data, is compelling food producers to shift toward compliant, organic input solutions.

Market Restraints

High Cost of Organic Fertilizers Relative to Synthetic Alternatives

One of the primary restraints limiting broader market penetration is the significantly higher cost of organic fertilizers compared to synthetic counterparts. Organic fertilizers typically command a price premium of 30-50% over conventional chemical fertilizers due to complex sourcing, processing, and quality certification requirements.

For smallholder farmers in developing nations, who represent the majority of global agricultural producers, this price differential can be prohibitive. Limited availability of raw materials such as quality bone meal, blood meal, and composted organic matter further tightens supply chains and elevates production costs, restricting adoption in price-sensitive markets across Sub-Saharan Africa and parts of Southeast Asia.

Lower Nutrient Concentration and Slower Release Rates

Organic fertilizers generally offer lower nutrient density (N-P-K values) compared to synthetic alternatives, which means farmers must apply substantially larger volumes per hectare to achieve comparable crop yield outcomes. For instance, while urea delivers roughly 46% nitrogen by weight, most organic nitrogen sources provide only 5-12% nitrogen. This necessitates higher transportation, storage, and application costs per unit nutrient delivered.

The slower nutrient release mechanism, while beneficial for soil health over the long term, can result in sub-optimal performance during critical crop growth phases, discouraging use among commercially driven large-scale farming operations focused on maximizing short-term productivity.

Market Opportunities

Integration of Biofortification and Precision Organic Nutrition Technologies

The convergence of biotechnology with organic fertilizer formulation presents a significant commercial opportunity for market participants. Innovations such as microbial inoculants, biostimulants, and nano-encapsulated organic nutrient delivery systems are enabling organic fertilizers to overcome traditional limitations of slow nutrient release and low concentration. The global biostimulants market is witnessing double-digit growth, with biostimulant-enriched organic fertilizers gaining regulatory approval across the EU, U.S., and India.

Companies integrating nitrogen-fixing bacteria (Rhizobium, Azospirillum) and phosphate-solubilizing microorganisms into organic fertilizer matrices are achieving demonstrably superior crop response rates, opening new premium product categories. Investment in fermentation-derived organic nutrients and seaweed-based liquid formulations further broadens the technology opportunity landscape for early movers.

Expansion into High-Value Horticulture and Urban Agriculture Segments

Rising urbanization and the rapid expansion of vertical farms, rooftop gardens, and controlled-environment agriculture (CEA) globally offer organic fertilizer manufacturers a lucrative, high-margin growth avenue. The Food and Agriculture Organization (FAO) projects that by 2050, nearly 68% of the world's population will reside in urban areas, intensifying interest in urban food production systems.

High-value horticulture crops, including berries, leafy greens, herbs, and specialty vegetables, command retail premiums that make the cost of organic inputs economically viable for producers. Government initiatives such as the EU's Urban Agriculture Promotion Policy and India's National Horticulture Mission are channeling funding toward organic horticultural inputs, offering organic fertilizer companies a structurally growing, policy-supported demand pocket with strong volume and margin potential through 2033.

Category-wise Analysis

Product Source Insights

Animal-based organic fertilizers represent the leading segment within the Product Source category, commanding approximately 42% market share in 2026. This dominance is attributable to the widespread availability and established efficacy of animal-derived inputs such as bone meal, blood meals, fish emulsion, poultry manure, and feather meals. These materials offer relatively higher nitrogen and phosphorus content compared to many plant-based alternatives, making them a preferred choice for commercial horticulture and intensive cropping systems.

The global livestock industry generates vast quantities of manure annually, the FAO estimates livestock waste production exceeding 130 billion tons per year globally, providing a cost-effective and abundant raw material. Additionally, the growing role of Darling Ingredients and similar companies in converting rendering byproducts into nutrient-rich organic fertilizers underscores the segment's supply chain maturity and scalability.

Product Form Insights

Granules dominate the Product Form category with an estimated market share of approximately 48% in 2026. Granular organic fertilizers are widely preferred across large-scale farming operations owing to their ease of application, extended shelf life, resistance to caking and moisture absorption, and compatibility with mechanized spreading equipment. Their slow, steady nutrient release profile aligns well with crop nutritional cycles, reducing application frequency and labor costs.

Major manufacturers including Yara, ICL, and IFFCO maintain extensive granular product portfolios targeting both row crops and specialty horticulture. According to U.S. Department of Agriculture (USDA) data, granular formulations dominate fertilizer distribution channels in North America, reinforcing the segment's commercial advantage in the largest developed organic agriculture market.

Crop Type Insights

Fruits and Vegetables represent the leading segment within Crop Type, holding an estimated 35% market share in 2026. This segment's dominance is driven by the strong premium pricing associated with certified organic produce, which makes organic fertilizer adoption economically compelling for fruit and vegetable growers. According to the Organic Trade Association, fresh produce accounted for the largest share of organic food sales, with organic fruits and vegetables representing over 36% of all organic food purchases in the U.S. alone.

The high nutrient sensitivity of horticultural crops, combined with strict residue standards for export markets, particularly within the European Union's Regulation (EC) No 834/2007, necessitates the use of certified organic inputs, underpinning consistent and growing demand from commercial fruit and vegetable producers globally.

End User Insights

Farmers and Growers constitute the dominant end-user segment, accounting for approximately 55% of the organic fertilizer market share in 2026. This primacy reflects the scale of global agricultural production and the ongoing transition toward organic and regenerative farming practices driven by regulatory mandates and market demand for organic food. Supportive government subsidy programs, such as India's National Programme for Organic Production (NPOP) and the EU's agri-environment-climate measures under the Common Agricultural Policy (CAP), directly incentivize farm-level adoption of organic inputs.

The growing network of organic farmer cooperatives and certified organic supply chains in regions such as Europe, South Asia, and Latin America further reinforces farmer/grower demand, as supply chain certifications increasingly mandate compliance with organic input standards across entire production systems.

Regional Analysis

Asia Pacific holds the leading position in the global organic fertilizer market, capturing approximately 38% market share in 2026, while Latin America is identified as the fastest growing region with an estimated CAGR of 11.2% over the 2026 - 2033 forecast period.

North America Organic Fertilizer Market Trends and Insights

North America represents a mature, innovation-driven market for organic fertilizers, supported by strong consumer demand for organic food products and established regulatory frameworks. The USDA National Organic Program (NOP) and voluntary certification pathways incentivize widespread use of compliant organic inputs. The region benefits from advanced product development ecosystems and significant retail infrastructure for organic produce, sustaining steady market growth.

U.S. Organic Fertilizer Market Size

The United States accounts for the majority of North American organic fertilizer consumption, representing nearly 78% of the regional market in 2026. With certified organic cropland exceeding 5.5 million acres per USDA data, and organic food retail sales surpassing US$ 61 billion annually, the U.S. market reflects strong structural demand for organic agricultural inputs across both commercial farming and home gardening segments.

Europe Organic Fertilizer Market Trends and Insights

Europe is the second-largest organic fertilizer market globally, characterized by proactive regulatory support through the EU Farm to Fork Strategy and the European Green Deal. With organic farmland covering approximately 15.9 million hectares as per Eurostat data, and ambitious targets for 25% organic land coverage by 2030, the region exhibits structurally driven demand growth across multiple crop and fertilizer categories.

Germany Organic Fertilizer Market Size

Germany represents the largest organic fertilizer market in Europe, contributing approximately 22% of the European market share in 2026. With over 1.8 million hectares of certified organic farmland and a national target of 30% organic land coverage by 2030, Germany is a strategic market for organic input suppliers. Leading players such as K+S Aktiengesellschaft have strengthened their organic and specialty fertilizer portfolios to serve this demand.

U.K. Organic Fertilizer Market Size

The United Kingdom holds approximately 10% of the European organic fertilizer market in 2026. Post-Brexit agricultural policy updates, including the Environmental Land Management (ELM) scheme, are redirecting agricultural payments toward sustainable farming practices. The Soil Association reports on continued growth in UK organic land and the number of certified organic operators, supporting sustained demand for compliant organic fertilizer products.

France Organic Fertilizer Market Size

France contributes approximately 14% of the European organic fertilizer market in 2026, benefiting from strong state support under the 'Ambition Bio 2022' plan targeting 15% organic farmland coverage. France's advanced viticulture and specialty horticulture sectors, both of which are major consumers of organic fertilizers, provide a diversified demand base, with the country's organic food market among the largest in continental Europe.

Asia Pacific Organic Fertilizer Market Trends and Insights

Asia Pacific leads the global organic fertilizer market by volume, driven by the sheer scale of agricultural operations across China, India, Japan, and Southeast Asia. China has committed to significantly reducing chemical fertilizer application as part of its 'Zero Growth in Chemical Fertilizer Use' action plan, generating substantial replacement demand for organic alternatives. The region benefits from abundant raw material supply chains and rapidly growing domestic organic food consumption.

India Organic Fertilizer Market Size

India accounts for roughly 25% of the Asia Pacific organic fertilizer market share in 2026. Government programs including the National Mission for Sustainable Agriculture (NMSA), PKVY, and state-level organic farming subsidies are driving rapidly adoption. India's organic certified area has grown steadily, with the country being one of the world's largest organic producers by number of farmers, per APEDA data.

Japan Organic Fertilizer Market Size

Japan represents approximately 12% of the Asia Pacific organic fertilizer market in 2026. Japan's 'Green Food System Strategy' targets 25% of farmland under organic management by 2050, supporting long-term structural demand growth. Japan's advanced horticultural sector and premium positioning of organic produce in domestic retail drive consistent demand for high-quality granular and liquid organic fertilizer formulations.

Southeast Asia Organic Fertilizer Market Size

Southeast Asia collectively accounts for approximately 18% of the Asia Pacific organic fertilizer market in 2026. Countries such as Thailand, Vietnam, and Indonesia are experiencing rapid growth in organic agricultural exports, particularly tropical fruits and spices, driving demand for certified organic inputs. Regional agricultural development programs supported by the ASEAN Centre for Biodiversity and bilateral trade agreements with the EU and U.S. are increasingly mandating organic certification compliance.

Competitive Landscape

The global organic fertilizer market exhibits a moderately fragmented competitive structure, with multinational corporations coexisting alongside a large base of regional and local producers. Leading companies such as Yara International, ICL, and IFFCO are leveraging their distribution networks and R&D capabilities to develop high-performance blended organic-mineral fertilizer products.

Key competitive differentiators include product certification, raw material traceability, and nutrient efficacy data. Emerging business models integrating digital soil health platforms with fertilizer advisory services, and circular economy approaches converting food and agricultural waste into premium organic inputs, are reshaping competitive dynamics. Strategic acquisitions and capacity expansions in high-growth Asia Pacific and Latin American markets are accelerating among top-tier players.

Key Developments

- In January 2025, Yara International announced the expansion of its organic and low-carbon fertilizer product line, committing to scaling production of organic nitrogen solutions across European markets as part of its sustainability roadmap.

- In March 2024 , Darling Ingredients completed the acquisition of additional rendering and organic nutrient processing capacity, strengthening its position as a leading producer of animal-based organic fertilizer ingredients across North America and Europe.

- In November 2023, Coromandel International Limited launched a new range of customized organic fertilizer blends targeting high-value horticulture crops in India, leveraging its extensive agronomic service network to drive adoption among commercial fruit and vegetable growers.

Organic Fertilizer Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.0 Billion |

| Current Market Value (2026) | US$ 8.2 Billion |

| Projected Market Value (2033) | US$ 15.0 Billion |

| CAGR (2026 - 2033) | 9.0% |

| Leading Region | Asia Pacific, 38% market share (2025) |

| Dominant Category - Product Source | Animal-Based, 42% market share (2025) |

| Top-Ranking Category - Product Form | Granules, 48% market share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 6.8 Billion |

Companies Covered in Organic Fertilizer Market

- IFFCO

- Yara

- The Scotts Company LLC

- Southern Petrochemical Industries Corporation Ltd (SPIC)

- Multiplex Group Of Companies

- uståne Natural Fertilizer, Inc.

- ICL

- Coromandel International Limited

- T.Stanes and Company Limited

- TerraLink Horticulture Inc.

- Queensland Organics

- K+S Aktiengesellschaft

- Darling Ingredients

- Fertoz

- Midwestern Bio Ag Holdings, LLC

Frequently Asked Questions

The global organic fertilizer market is expected to reach a value of US$ 8.2 billion in 2026 and is projected to grow at a CAGR of 9.0% to reach US$ 15.0 billion by 2033.

Primary demand drivers include the rapid expansion of global organic farmland, stringent regulatory frameworks such as the EU Farm to Fork Strategy mandating fertilizer use reductions, and rising consumer preference for certified organic food products.

Asia Pacific is the leading region in the global organic fertilizer market, holding approximately 38% market share in 2026, supported by the massive scale of agricultural operations in China and India, favorable government policies, and abundant availability of organic raw materials.

Key opportunities include the rapid expansion of urban agriculture, vertical farms, and controlled-environment horticulture, supported by the FAO's projection of 68% urban population by 2050, presents a high-value, high-growth end-market for specialized organic fertilizer products through 2033.

Leading companies operating in the global organic fertilizer market include IFFCO, Yara International, The Scotts Company LLC, ICL Group, Coromandel International Limited, Darling Ingredients, K+S Aktiengesellschaft, T. Stanes and Company Limited, Fertoz, Midwestern BioAg Holdings LLC, and Sustane Natural Fertilizer Inc., among others.