- Pharmaceuticals

- Oral Transmucosal Drugs Market

Oral Transmucosal Drugs Market Size, Share, and Growth Forecast 2026 - 2033

Oral Transmucosal Drugs Market by Product Type (Tablets, Films, Lozenges & Troches, Oral Sprays, Others), Drug Type (Buprenorphine, Fentanyl, Nitroglycerin, Midazolam, Others), Therapeutic Area (Opioid Dependence, Breakthrough Cancer Pain, Seizure Clusters and Epilepsy, Angina Pectoris, Others), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Pharmacies), and Regional Analysis, 2026 - 2033

Oral Transmucosal Drugs Market Size and Trend Analysis

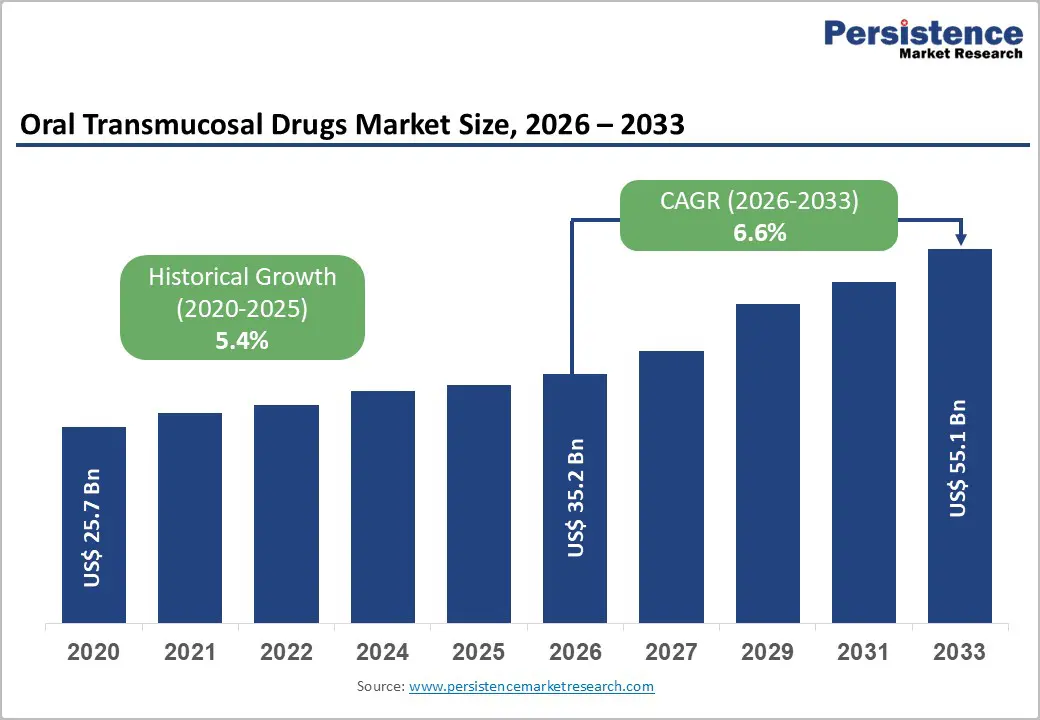

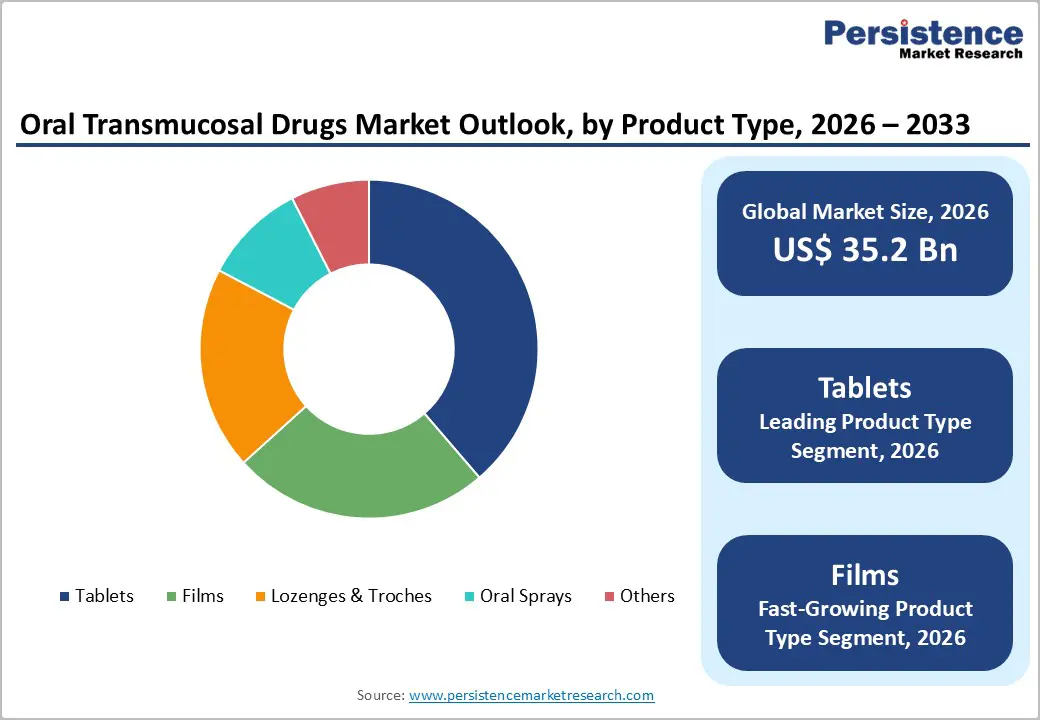

The global oral transmucosal drugs market size is expected to be valued at US$ 35.2 billion in 2026 and projected to reach US$ 55.1 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

The growth is underpinned by the accelerating adoption of transmucosal drug delivery as a clinically preferred alternative to oral and injectable routes offering rapid systemic absorption, bypassing first-pass hepatic metabolism, and enhancing patient compliance.

The growing global burden of opioid dependence, breakthrough cancer pain, and epilepsy is driving prescribing volumes for proven transmucosal agents such as buprenorphine sublingual films, fentanyl buccal tablets, and midazolam nasal-to-buccal formulations. Simultaneously, ongoing innovation in oral film and spray technologies, supported by robust regulatory activity at the U.S. FDA and EMA, is expanding the addressable therapeutic applications.

Key Industry Highlights

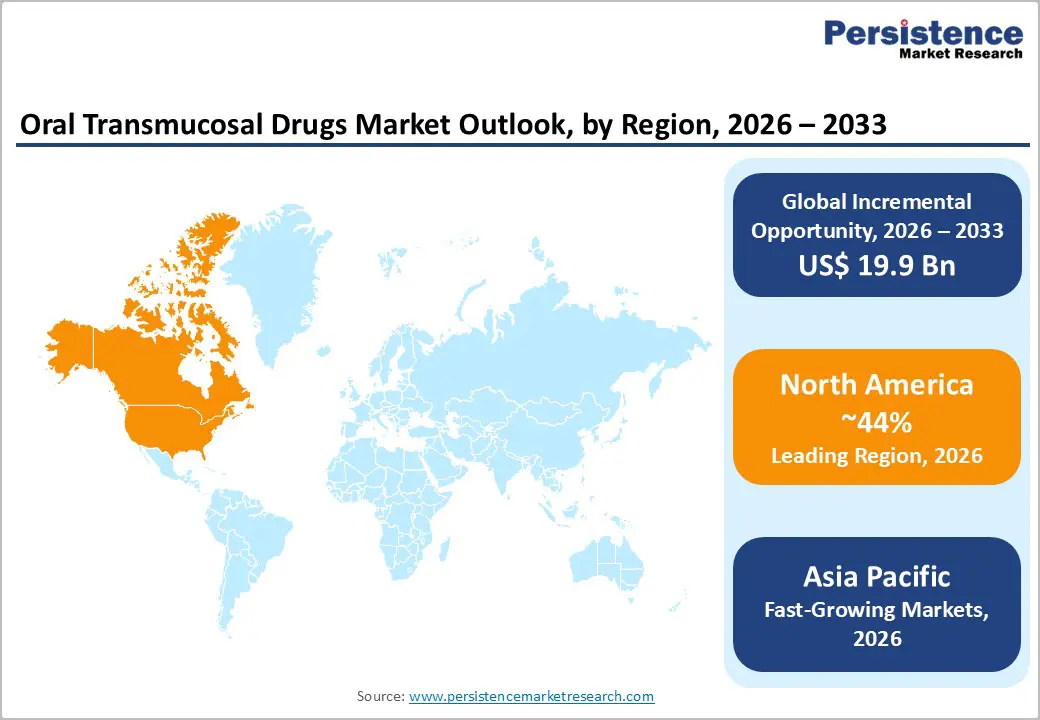

- Leading Region – North America: North America leads the global oral transmucosal drugs market with approximately 44% revenue share in 2026, anchored by the U.S. opioid dependence treatment market, broad FDA approvals, elimination of the DEA X-waiver, and robust specialty pharmacy infrastructure.

- Fastest Growing Region – Asia Pacific: Asia Pacific is the fastest-growing regional market, driven by the expanding OUD treatment programs in China and India, growing oncology palliative care demand in Japan, and India's competitive oral thin film contract manufacturing capabilities.

- Dominant Segment – Tablets: Tablets hold approximately 39% of product type revenues in 2026, underpinned by high-volume sublingual nitroglycerin and buprenorphine prescriptions, broad generic availability, and the longest clinical track record among all oral transmucosal dosage forms.

- Fastest Growing Segment – Oral Films: Oral thin films are the fast-growing product type, driven by lifecycle management strategies converting established molecules (buprenorphine, asenapine) to film formats, superior patient compliance attributes, and strong FDA receptivity to NDA submissions for innovative OTF platforms.

- Key Opportunity – Pediatric & Geriatric Transmucosal Formulations: The rise in global population aged 60+ and mandatory pediatric formulation requirements under the FDA PREA create a substantial market opportunity for age-appropriate transmucosal dosage forms in neurology, cardiology, and pain management.

Market Dynamics

Drivers - Rising Prevalence of Opioid Dependence Fueling Demand for Buprenorphine Transmucosal Formulations

The escalating global opioid crisis remains the most powerful demand driver for oral transmucosal drugs, particularly sublingual and buccal buprenorphine formulations used in medication-assisted treatment (MAT). The United Nations Office on Drugs and Crime (UNODC) estimates that approximately 60 million people globally suffer from opioid use disorder (OUD).

In the United States, the Substance Abuse and Mental Health Services Administration (SAMHSA) reported over 6.1 million Americans aged 12 and older with OUD in 2021. Transmucosal buprenorphine marketed as Suboxone (Indivior) and generic equivalents, has become the standard of care for OUD management, with prescriptions growing consistently year-on-year. Regulatory backing through the U.S. Mainstreaming Addiction Treatment (MAT) Act of 2023 has removed prescribing restrictions for buprenorphine, further accelerating patient access and treatment volumes.

Technological Superiority of the Transmucosal Route Driving Clinical and Patient Preference

Oral transmucosal drug delivery offers distinct pharmacokinetic advantages that are driving its adoption across multiple therapeutic areas. Drug absorption through the buccal, sublingual, or gingival mucosa provides rapid onset of action typically within 5–15 minutes by directly entering systemic circulation, bypassing the gastrointestinal tract and first-pass hepatic metabolism. This is critical for acute-indication therapies such as breakthrough cancer pain (fentanyl buccal tablets) and acute seizure management (midazolam buccal solution). According to a 2022 review in the Journal of Controlled Release, transmucosal bioavailability of select drugs is up to 3–5 times higher than equivalent oral formulations. Patient preference surveys consistently cite ease of administration, no-water-required convenience, and rapid symptom relief as key adherence drivers, broadening the appeal of transmucosal formats across chronic and acute care settings.

Restraints - Stringent Controlled Substance Regulations Creating Market Access Barriers

A significant proportion of oral transmucosal drugs, including buprenorphine, fentanyl, and midazolam, are classified as controlled substances under the U.S. Controlled Substances Act (CSA) and analogous frameworks of the International Narcotics Control Board (INCB). These classifications impose restrictive prescribing, dispensing, storage, and record-keeping requirements that constrain prescriber participation and patient access. In many low- and middle-income countries (LMICs), over-regulation of opioid formulations results in chronic under-treatment of pain, artificially limiting the addressable commercial market for transmucosal analgesics globally.

Mucosal Irritation, Variable Absorption, and Formulation Stability Challenges

Oral transmucosal drug delivery faces inherent biopharmaceutical limitations that can hinder clinical uptake and product development efficiency. Chronic administration of transmucosal formulations, particularly adhesive buccal tablets and films can cause mucosal irritation, ulceration, or taste aversion, reducing patient tolerability. Variable salivary flow, food intake, and mucosal thickness across patient populations introduce pharmacokinetic inconsistency. Additionally, the instability of active pharmaceutical ingredients in humid oral environments presents formulation challenges for manufacturers, requiring specialized excipients and packaging, increasing development complexity and cost, and potentially limiting the range of molecules suitable for this delivery route.

Opportunities - Oral Dissolving Films: The Fastest-Growing Format Unlocking New Molecule Opportunities

Oral thin films (OTFs) are the fastest-growing product type in the oral transmucosal drugs market, representing a compelling opportunity for both branded and generic pharmaceutical companies. Unlike conventional tablets, OTFs dissolve within seconds on the oral mucosa without requiring water, offering superior compliance, tamper-resistance, and precise dosing.

The FDA has been increasingly receptive to OTF formulations, with approvals spanning opioid dependence (Suboxone Film), acute agitation (Secuado), and migraine. Aquestive Therapeutics and IntelGenx Technologies are among the specialist players advancing proprietary OTF platforms. Per PharmTech industry analysis, the oral thin film segment is projected to grow at a significantly faster pace than tablets or lozenges through 2030, driven by lifecycle management strategies of major pharmaceutical companies converting existing molecules to OTF formats, representing a differentiated pipeline opportunity.

Expanding Therapeutic Applications in Pediatric and Geriatric Populations

Oral transmucosal drug delivery offers a significant untapped opportunity in pediatric and geriatric patient segments, where swallowing conventional tablets or capsules presents a safety or compliance challenge. The WHO estimates that globally, over 1 billion people are aged 60 or older, a population growing rapidly and disproportionately affected by dysphagia and polypharmacy challenges. The FDA's Pediatric Research Equity Act (PREA) mandates pediatric formulation development for many approved drugs, creating a regulatory pathway incentive. Transmucosal midazolam for seizure cluster management in pediatric patients, approved as Nayzilam (UCB) and Seizalam, exemplifies this trend. Companies investing in age-appropriate transmucosal formulations for cardiovascular, neurological, and pain indications are positioned to access a large, underserved patient population with premium pricing potential.

Category-wise Analysis

Product Type Insights

Tablets constitute the leading product type in the oral transmucosal drugs market, capturing approximately 39% of total revenues in 2026. Sublingual and buccal tablets have the longest clinical track record across key transmucosal therapeutic areas, including nitroglycerin sublingual tablets for acute angina, one of the oldest and most prescribed transmucosal therapies globally, and fentanyl buccal tablets (Fentora, Teva Pharmaceuticals) for breakthrough cancer pain. The established manufacturing infrastructure, pharmacist familiarity, and extensive generic competition in the sublingual nitroglycerin category have sustained high prescription volumes. According to IQVIA dispensing data, buprenorphine sublingual tablets and nitroglycerin sublingual formulations collectively account for the highest prescription volumes among all transmucosal dosage forms, cementing the tablet segment's revenue leadership through the forecast period.

Drug Type Insights

Buprenorphine is the leading drug type in the oral transmucosal drugs market, accounting for approximately 38% of segment revenues in 2026. This dominance reflects the massive and growing OUD treatment population, the maturity of the buprenorphine transmucosal franchise, and strong generic penetration following the expiry of Suboxone Film exclusivity. The SAMHSA National Survey on Drug Use and Health (NSDUH) 2022 data indicate that buprenorphine is the most prescribed MAT medication in the United States, with annual prescriptions exceeding 10 million. The U.S. MAT Act of 2023 eliminated the DEA X-waiver requirement, substantially broadening the prescriber base for buprenorphine and sustaining long-term volume growth across sublingual tablet and film formulations.

Therapeutic Area Insights

Opioid Dependence is the leading therapeutic area in the oral transmucosal drugs market, commanding approximately 36% of global revenues in 2026. This dominance is directly tied to the scale of the global OUD epidemic and the central role of sublingual and buccal buprenorphine/naloxone formulations in evidence-based treatment protocols. The WHO includes buprenorphine on its Essential Medicines List as a cornerstone of OUD management, underscoring its global clinical importance. Driven by the U.S. opioid crisis, prescriptions for transmucosal buprenorphine formulations have grown consistently at over 5% annually in recent years. Furthermore, expanding OUD treatment infrastructure in Europe and Australia is broadening the geographic revenue base for this segment.

Distribution Channel Insights

Specialty Pharmacies represent the leading distribution channel for oral transmucosal drugs, capturing approximately 40% of revenues in 2026. This reflects the controlled substance status and clinical complexity of most transmucosal drugs, which require specialized dispensing, patient counseling, prior authorization management, and risk evaluation and mitigation strategy (REMS) compliance. The FDA mandates REMS programs for high-risk opioids, including transmucosal immediate-release fentanyl (TIRF REMS Access) and buprenorphine, directing distribution through credentialed specialty pharmacy networks. According to the National Association of Specialty Pharmacy (NASP), specialty pharmacy now represents over 50% of total U.S. drug spend, reflecting the broader shift toward high-acuity, managed-access dispensing models that are particularly aligned with the oral transmucosal drug category.

Regional Insights

North America Oral Transmucosal Drugs Market Trends and Insights

North America accounted for approximately 44.2% of the global oral transmucosal drugs market in 2026. Regional growth is driven by high diagnosis and treatment rates for opioid use disorder, extensive adoption of buprenorphine sublingual films, and favorable reimbursement for rapid-onset pain and seizure therapies. The region also benefits from the most mature regulatory framework for transmucosal formulations, strong generic penetration, and highly developed specialty pharmacy and REMS distribution systems. Continued expansion of addiction treatment access and broader physician prescribing are expected to sustain long-term market leadership.

U.S. Oral Transmucosal Drugs Market Trends and Insights

The U.S. represented nearly 85.6% of the North American market in 2025. Demand is led by widespread use of buprenorphine/naloxone films for opioid use disorder, fentanyl buccal products for breakthrough cancer pain, and midazolam formulations for seizure rescue. The country has the largest number of FDA-approved oral transmucosal products globally, supported by strong commercial insurance and Medicaid reimbursement. Growing generic competition and expanded office-based addiction treatment continue to improve affordability and treatment penetration.

Canada Oral Transmucosal Drugs Market Trends and Insights

Canada accounted for an estimated 9.8% of regional revenue in 2026 and is projected to reach a positive CAGR in the coming years. Publicly funded opioid response programs and provincial reimbursement for buprenorphine are driving broad adoption across addiction treatment centers. Rising use of transmucosal analgesics in oncology and palliative care further supports market expansion. Increased emphasis on harm reduction and rapid access to substitution therapy is expected to sustain steady demand growth.

Europe Oral Transmucosal Drugs Market Trends and Insights

Europe is likely to capture around 28.7% of global oral transmucosal drug revenues in 2026. The market is supported by widespread opioid substitution therapy, established use of sublingual nitroglycerin, and streamlined approvals through the European Medicines Agency. Strong reimbursement frameworks and physician familiarity with transmucosal delivery contribute to stable uptake across major markets. Innovation in oral thin films and buccal formulations for CNS and oncology applications is expected to accelerate future growth.

Germany Oral Transmucosal Drugs Market Trends and Insights

Germany is poised for 24.8% of the European market in 2026. Extensive addiction treatment infrastructure, broad statutory insurance coverage, and high prescribing rates for buprenorphine-based therapies support market leadership. The country also maintains strong oncology and palliative care services, sustaining demand for fentanyl buccal formulations. Continued adoption of advanced oral film technologies is reinforcing Germany’s role as the region’s largest market.

UK Oral Transmucosal Drugs Market Trends and Insights

UK is likely to account for 18.9% of Europe’s market and is forecast to achieve a positive CAGR in the forecast years. NHS-supported addiction services and favorable reimbursement for opioid substitution treatments drive high utilization of sublingual buprenorphine. Growth is also supported by increasing adoption of transmucosal products for neurological and emergency care applications. Ongoing innovation in specialty oral formulations is expected to strengthen demand over the forecast period.

Asia Pacific Oral Transmucosal Drugs Market Trends and Insights

Asia Pacific is poised for a leading share of the global market in 2026 and is projected to register the fast CAGR. Growth is fueled by increasing awareness of opioid dependence treatment, rising cancer prevalence, and expanding domestic pharmaceutical manufacturing. Government-supported addiction programs and greater availability of cost-effective oral films and tablets are accelerating adoption across both developed and emerging healthcare systems.

Japan Oral Transmucosal Drugs Market Trends and Insights

Japan accounted for approximately 31.4% of the Asia Pacific market in 2025. Advanced healthcare infrastructure, strong regulatory oversight, and high standards in oncology and palliative care support broad use of transmucosal therapies. The country has a well-established market for sublingual and buccal products in addiction treatment and pain management. Continued uptake of innovative formulations is expected to maintain Japan’s regional leadership.

India Oral Transmucosal Drugs Market Trends and Insights

India’s substantial contribution is likely to fuel growth and is expected to reach a CAGR of 10.6%. Expansion of the National Drug Dependence Treatment Programme and increasing access to buprenorphine are driving domestic demand. India is also a major manufacturing hub for oral thin films and sublingual tablets, supporting both local consumption and exports. Cost-efficient production capabilities and growing healthcare investment position the country for rapid expansion.

Competitive Landscape

The global oral transmucosal drugs market is moderately fragmented, with a mix of large multinational pharmaceutical companies, including Teva Pharmaceuticals, Pfizer, Sanofi, and AbbVie, and specialized drug delivery companies such as Aquestive Therapeutics and IntelGenx Technologies. Large players leverage brand equity, established distribution networks, and REMS infrastructure, while specialists differentiate through proprietary drug delivery platform technologies (e.g., oral thin films, sublingual sprays). Generic competition is intense in mature segments (nitroglycerin, buprenorphine), while branded innovation in films, sprays, and novel molecules for pediatric and geriatric indications represents the key competitive frontier. Licensing and co-development partnerships are a dominant business model for delivery technology specialists.

Key Developments:

- In April 2026, Tivic Health Systems, Inc., a clinical-stage immunotherapeutics company, announced that it had been invited to present at the U.S. Department of War Tech Watch Program on May 7, 2026. The Tech Watch initiative evaluates emerging technologies with significant defense and dual-use potential.

- In May 2025, Aspire Biopharma Holdings, Inc. announced that the first participant was dosed in a U.S.-based Phase I single-center clinical trial evaluating the safety, pharmacokinetics, and pharmacodynamics of its lead candidate, a patent-pending oral transmucosal formulation of fast-acting high-dose aspirin.

Companies Covered in Oral Transmucosal Drugs Market

- GSK plc

- Hikma Pharmaceuticals PLC

- Bristol-Myers Squibb Company

- Teva Pharmaceutical Industries Ltd.

- Novartis AG

- Sanofi

- AbbVie Inc.

- Eli Lilly and Company

- Boehringer Ingelheim

- Pfizer Inc.

- Aquestive Therapeutics, Inc.

- Jazz Pharmaceuticals, Inc.

- ZIM Laboratories Limited

- IntelGenx Technologies Corp.

- Otsuka Pharmaceutical Co., Ltd.

- Others

Frequently Asked Questions

The global oral transmucosal drugs market is projected to be valued at US$ 35.2 billion in 2026, supported by high and growing prescription volumes for buprenorphine sublingual films and tablets in opioid dependence treatment, buccal fentanyl in breakthrough cancer pain, and midazolam transmucosal formulations for seizure management all benefiting from favorable FDA and EMA regulatory environments.

Primary demand drivers include rising prevalence of opioid dependence, breakthrough cancer pain and seizure disorders, along with growing preference for rapid-onset, non-invasive drug delivery systems with improved bioavailability.

North America leads the global oral transmucosal drugs market with approximately 44% revenue share in 2025. The United States is the dominant country market, underpinned by the highest global burden of diagnosed opioid use disorder, the broadest portfolio of FDA-approved transmucosal formulations, expanded buprenorphine prescribing access post DEA X-waiver elimination, and a mature specialty pharmacy distribution infrastructure.

Key market opportunities lie in expanding transmucosal formulations for CNS disorders, emergency rescue therapies, pediatric applications, and adoption of advanced mucoadhesive films and sprays in emerging markets.

Leading companies include Teva Pharmaceutical Industries (fentanyl buccal tablets), Indivior PLC (Suboxone film), Aquestive Therapeutics (OTF platforms), Jazz Pharmaceuticals, GSK plc, Pfizer Inc., AbbVie Inc., ZIM Laboratories, IntelGenx Technologies, and UCB S.A., among others advancing innovation across sublingual, buccal, and oral film delivery platforms.