- Medical Devices

- Digital Intraoral Sensors and Consumables Market

Digital Intraoral Sensors and Consumables Market Size, Share, and Growth Forecast 2026 - 2033

Digital Intraoral Sensors and Consumables Market by Product (Dental Digital Intraoral Sensors and Consumables), by Application (Restorative Dentistry, Orthodontics, Implantology, and Others), End-user and Regional Analysis from 2026 - 2033

Digital Intraoral Sensors and Consumables Market Share and Trends Analysis

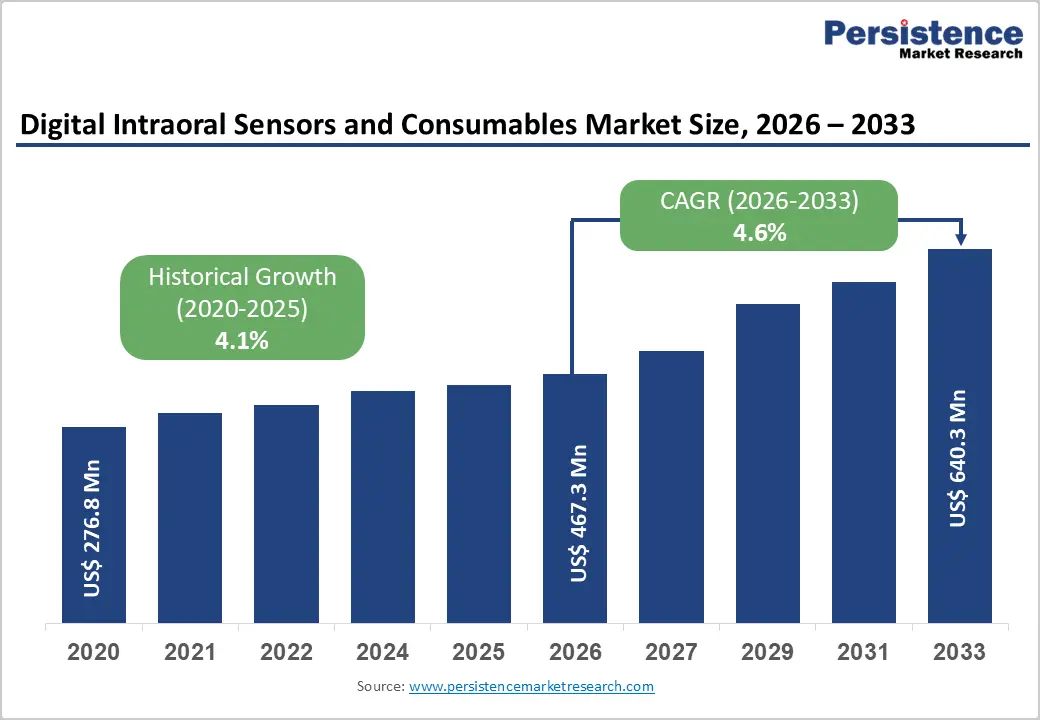

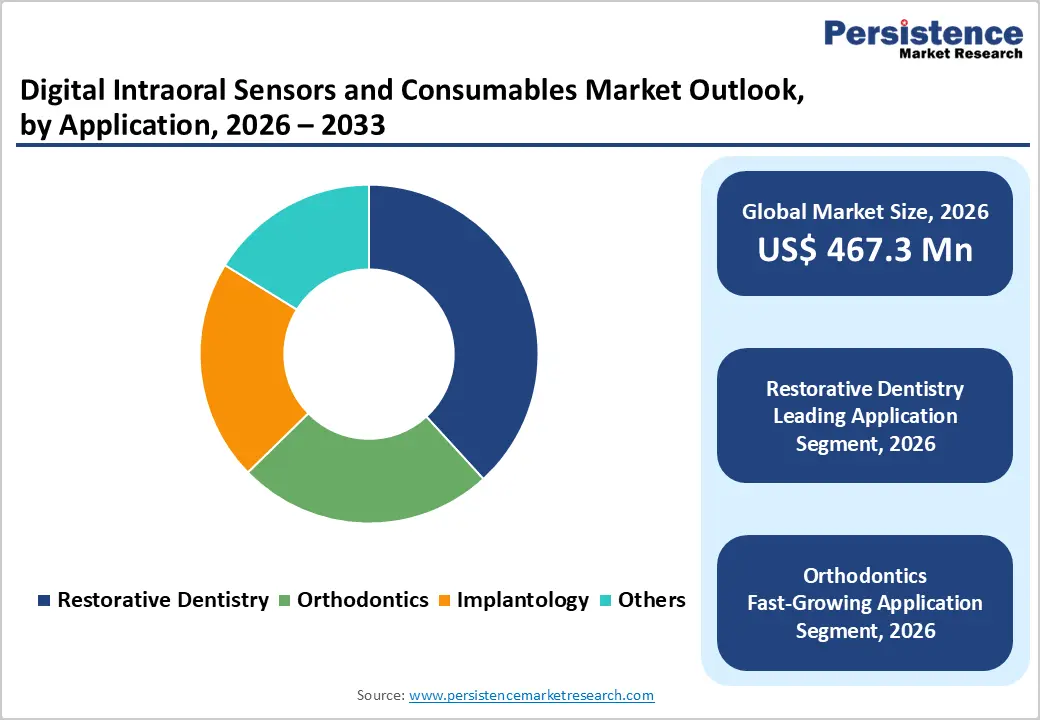

The global digital intraoral sensors and consumables market size is expected to be valued at US$ 467.3 million in 2026 and projected to reach US$ 640.3 million by 2033, growing at a CAGR of 4.6% between 2026 and 2033.

Global demand for digital intraoral sensors and consumables is rising steadily, driven by increasing volumes of restorative, cosmetic, and diagnostic dental procedures, along with the rapid shift toward digital dentistry workflows. Dental clinics and hospitals are increasingly adopting digital intraoral sensors, phosphor storage plates, intraoral cameras, and image plate scanners to support accurate diagnosis, treatment planning, and chairside decision-making.

Growing investments in dental infrastructure, expansion of organized dental chains, and wider availability of cost-effective digital imaging solutions are accelerating adoption across both developed and emerging markets. Continuous advancements in sensor resolution, wireless connectivity, image-processing algorithms, and software integration are improving diagnostic accuracy, workflow efficiency, and clinical turnaround times. In addition, rising clinician awareness, expanding training programs, and strong clinical evidence supporting digital intraoral imaging are further supporting sustained global market growth.

Key Market highlights

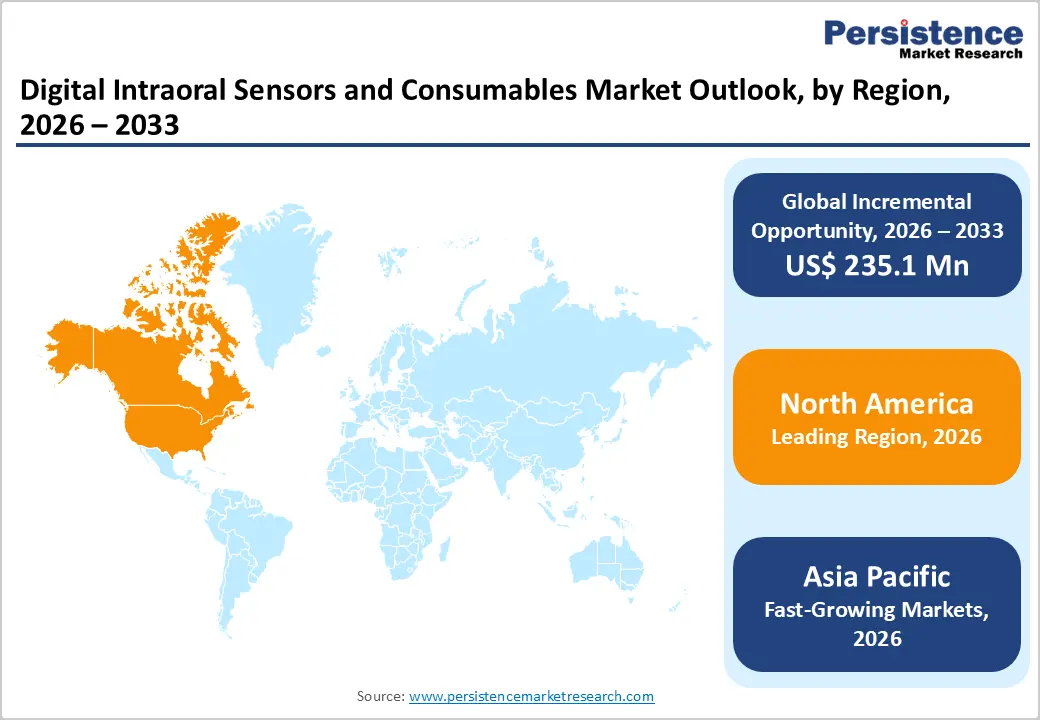

- Leading Region: North America holds the largest share at 44%, supported by advanced dental care infrastructure, high penetration of digital imaging technologies, strong healthcare expenditure, and early access to FDA-approved digital intraoral sensors and consumables.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace, driven by a large and underserved patient population, rapid modernization of dental clinics and hospitals, growing medical tourism, and increasing investments in digital dental imaging infrastructure.

- Leading Product Segment: Dental digital intraoral sensors dominate the market due to their widespread use in routine diagnostics, restorative dentistry, implant planning, and follow-up imaging, offering high resolution, low radiation exposure, and reliable clinical performance.

- Fastest-Growing Product Segment: Consumables are witnessing rapid growth as replacement demand for phosphor storage plates, increased use of intraoral cameras, and higher imaging frequency in chairside workflows support recurring revenue generation.

- Leading Component Segment: Restorative dentistry remains the leading application, driven by high imaging requirements for caries detection, crown and bridge procedures, root canal treatments, and post-restorative evaluations.

- Fastest-Growing Component Segment: Orthodontics is growing rapidly due to increasing reliance on digital imaging for treatment planning, progress monitoring, and integration with digital orthodontic workflows across clinics and specialty practices.

| Report Attribute | Details |

|---|---|

|

Digital Intraoral Sensors and Consumables Size (2026E) |

US$ 467.3 million |

|

Market Value Forecast (2033F) |

US$ 640.3 million |

|

Projected Growth CAGR (2026-2033) |

4.6% |

|

Historical Market Growth (2020-2025) |

4.1% |

Market Dynamics

Driver- Growing Adoption of Digital Intraoral Imaging in Dental Practices

The rapid shift toward digital dentistry workflows in clinics and hospitals is driving significant adoption of intraoral sensors and related imaging consumables. As dental practices modernize, these technologies streamline patient management, reduce procedural times, and facilitate seamless integration with computer-aided treatment planning and CAD/CAM systems. Hospitals and multi-specialty dental centers are increasingly investing in digital imaging infrastructure to enhance operational efficiency, improve patient experience, and support advanced treatment modalities such as orthodontics, implantology, and restorative procedures. The availability of both wired and wireless intraoral sensors further enables flexible implementation across diverse clinical settings, meeting the growing demand for precision dentistry.

Digital intraoral imaging offers clear advantages over conventional film-based systems, which is a key factor in accelerating market adoption. Low radiation exposure ensures enhanced patient safety, while instant image acquisition allows clinicians to make faster and more informed diagnostic decisions. High-resolution imaging improves detection of dental caries, periodontal disease, and structural abnormalities, thereby increasing diagnostic accuracy and treatment outcomes. These benefits, combined with the ease of storing and sharing digital images across clinical networks, position intraoral sensors and imaging consumables as indispensable tools in modern dentistry. Consequently, digital imaging is increasingly replacing traditional film systems, reinforcing its status as the preferred solution in contemporary dental practice.

Restraint- High-Cost Barriers and Limited Accessibility Constraining Market Adoption

The High upfront costs for advanced intraoral sensors and imaging systems remain a significant barrier, as smaller clinics often face budget constraints and may be unable to justify large capital investments. Additionally, limited reimbursement coverage for advanced dental imaging procedures in multiple countries restricts the financial incentives for adopting these technologies. In markets where insurance and public health schemes provide minimal support for high-end imaging, dental practices may be reluctant to transition from conventional film-based systems. These economic considerations significantly influence market penetration, slowing adoption in price-sensitive regions.

Moreover, technical and operational challenges also affect long-term utilization of digital intraoral imaging systems. Issues such as sensor durability, cable damage, and limited compatibility across different imaging software platforms can lead to operational disruptions and increased maintenance costs. Clinics may encounter difficulties integrating new systems with existing workflows, which can reduce overall efficiency and staff adoption. Addressing these restraints requires continued innovation in hardware resilience, software standardization, and cost-effective solutions, which are essential for enabling broader adoption across diverse dental practices.

Opportunity- Technological Innovation and Regional Expansion Fuelling Market Opportunities

The digital intraoral imaging market presents several growth opportunities driven by technological innovation and evolving dental practice needs. The rising demand for wireless and AI-enabled intraoral sensors allows manufacturers to differentiate their products and target premium segments, offering enhanced diagnostic capabilities, ease of use, and streamlined clinical workflows. Additionally, replacement demand from aging film-based and early-generation digital systems provides a steady upgrade market, as clinics and hospitals increasingly adopt advanced imaging solutions to improve accuracy, efficiency, and patient experience. These factors collectively create opportunities for both product innovation and revenue growth in established and emerging markets.

Furthermore, the regional expansion creates significant opportunities in the market due to rapid growth of dental infrastructure and private dental clinics in Asia Pacific, Latin America, and the Middle East is creating new avenues for market penetration. Moreover, increasing integration of intraoral imaging with cloud-based software, tele-dentistry platforms, and comprehensive digital treatment planning tools supports long-term adoption by enabling remote consultations, data-driven decision-making, and seamless workflow management. Together, technological advancements, replacement demand, and regional expansion are expected to drive sustained growth and create a favorable environment for manufacturers and service providers in the digital intraoral imaging sector.

Category-wise Insights

Product Type Analysis

Digital intraoral sensors are projected to account for approximately 63% of the global Digital Intraoral Sensors and Consumables market in 2026, reflecting their central role in modern dental diagnostics. Their dominance is driven by widespread adoption across routine dental examinations, restorative procedures, endodontics, and implant planning. Compared to traditional film and phosphor plates, digital sensors provide instant image acquisition, superior image resolution, and reduced radiation exposure, significantly improving diagnostic accuracy and clinical efficiency.

The growing preference for chairside digital workflows further strengthens demand for intraoral sensors, as they integrate seamlessly with practice management software and digital treatment planning systems. High utilization rates, frequent imaging per patient, and the need for reliable, repeatable results make sensors a critical investment for dental clinics and hospitals. Additionally, ongoing technological advancements such as improved sensor durability, ergonomic designs, and enhanced imaging software are supporting replacement demand and upgrades. As dental practices continue transitioning toward fully digital ecosystems, digital intraoral sensors are expected to retain their leading share within the product type segment through 2026.

Component Analysis

The Restorative dentistry segment is projected to dominate the global digital intraoral sensors and consumables market in 2026, accounting for a significant revenue share of 38.2%. This is attributed to the high capital cost and essential role of core equipment such as milling machines, intraoral scanners, laboratory scanners, and dental 3D printers. Dental laboratories and clinics rely heavily on these systems for routine restorative, implant, and prosthetic workflows. Continuous equipment upgrades, growing adoption of multi-axis milling machines, and expanding use of 3D printing for models and surgical guides contribute to sustained demand. High utilization rates and long replacement cycles further support the hardware segment’s strong market position.

End Use Analysis

The Dental Clinics segment is expected to dominate the global Digital Intraoral Sensors and Consumables market in 2026, capturing a revenue share of 46.8%. Dental clinics serve as the primary point of care for routine diagnostics, restorative procedures, and preventive dental services, consistent driving utilization of intraoral sensors, phosphor storage plates, and intraoral cameras. Increasing adoption of chairside digital imaging, emphasis on faster diagnosis, and improved patient communication are accelerating uptake. Additionally, the expansion of group dental practices and dental service organizations (DSOs), coupled with declining equipment costs and simplified workflows, continues to reinforce dental clinics as the leading end-user segment globally.

Regional Insights

North America Digital Intraoral Sensors and Consumables Market Trends and Insights

North America is expected to maintain global dominance in the digital intraoral sensors and consumables market, accounting for an estimated 44% market share, supported by advanced dental care infrastructure, high penetration of digital imaging technologies, and early adoption of sensor-based diagnostics. The U.S. leads the region due to widespread deployment of digital intraoral X-ray sensors, strong replacement demand for legacy film-based systems, and high utilization of consumables such as phosphor storage plates and intraoral cameras. Strong investment in cosmetic, restorative, and implant dentistry further accelerates imaging demand.

The regional market benefits from favorable reimbursement structures for dental procedures, high clinician familiarity with digital workflows, and increasing integration of cloud-based imaging software and AI-assisted diagnostics. Ongoing investments in practice modernization, expansion of group dental practices, and emphasis on chairside efficiency continue to reinforce North America’s long-term leadership in the global Digital Intraoral Sensors and Consumables market.

Europe Digital Intraoral Sensors and Consumables Market Trends and Insights

Europe exhibits steady and mature adoption of digital intraoral sensors and consumables market, supported by well-established dental healthcare systems, strong regulatory frameworks, and a dense network of private clinics and dental laboratories across Germany, the U.K., France, Italy, Switzerland, and the Nordic countries. Consistent demand for high-quality diagnostics in restorative dentistry, orthodontics, and implantology drives sustained utilization of digital sensors, PSP plates, and imaging accessories.

The region emphasizes clinical accuracy, radiation safety, and workflow standardization, supporting regular upgrades from wired to wireless sensor systems. Increasing focus on efficiency, cost control, and cross-border dental services, particularly in Central and Eastern Europe continues to support gradual market expansion, despite pricing pressures and reimbursement constraints in some countries.

Asia Pacific Digital Intraoral Sensors and Consumables Market Trends and Insights

Asia Pacific is projected to be the fastest-growing region in the digital intraoral sensors and consumables market, registering a CAGR of approximately 5.9%, driven by rapid expansion of dental care infrastructure, rising oral health awareness, and accelerating digital transformation of dental practices. Key markets including China, India, Japan, South Korea, and Southeast Asia are witnessing increased adoption of digital intraoral sensors and consumables across both urban clinics and emerging mid-tier practices.

Government initiatives supporting healthcare digitization, the growth of private dental chains, and rising medical tourism are improving access to advanced imaging technologies. Additionally, the availability of cost-effective sensors and consumables, along with the growing demand for aesthetic dentistry, orthodontics, and implant procedures, continues to fuel strong growth momentum, positioning Asia Pacific as a critical expansion region for global digital intraoral sensors and consumables manufacturers.

Competitive Landscape

Market Structure Analysis

The global digital intraoral sensors and consumables market is moderately to highly competitive, with prominent players such as Dentsply Sirona, Envista, Planmeca Oy, Carestream Dental, LLC, and Danaher Corporation. These companies leverage broad dental imaging portfolios, advanced sensor technologies (CMOS/CCD), proprietary imaging software, and well-established global distribution networks to strengthen their presence across dental clinics, hospitals, and academic dental institutions. Manufacturers are increasingly focused on improving diagnostic accuracy and workflow efficiency through the development of wireless intraoral sensors, enhanced image-processing algorithms, and seamless integration with practice management and digital dentistry ecosystems. Strategic priorities include continuous product innovation, expansion into emerging markets, partnerships with dental service organizations and group practices, and adherence to evolving regulatory standards to support wider adoption of digital intraoral imaging solutions and sustain long-term market growth.?

Key Market Developments

- In March 2025, OMNIVISION partnered with Biotech Dental to integrate its medical-grade CameraCubeChip® modules into Biotech’s Scan4All 3D intraoral scanners Iris by Starck. The modules enhance precision and reliability for dental applications. The collaboration and technology were showcased at the International Dental Show (IDS) 2025 in Cologne, Germany.

- In September 2024, Dentsply Sirona introduced Primescan 2, a next-generation intraoral scanner designed to advance digital patient care. Cloud-native, wireless, and highly versatile, Primescan 2 builds on the proven scanning technology of its predecessor while enabling scanning directly to the cloud on any internet-connected device.

- In September 2024, DEXIS introduced DEXIS™ Connect Pro, a proactive service platform designed to monitor the health of CBCT and intraoral sensor devices. Leveraging IoT technology, the platform automatically tracks device performance and arranges support or equipment replacements as needed. According to Brian Gooch, Global Product Manager and VP of Marketing at DEXIS, this solution helps dental practices save time and enhance productivity by ensuring seamless device maintenance and support.

Companies Covered in Digital Intraoral Sensors and Consumables Market

- Dentsply Sirona

- Envista

- Planmeca Oy

- Carestream Dental, LLC

- Danaher Corporation

- FONA Dental

- Suni Medical Imaging, Inc.

- DÜRR DENTAL SE

- Midmark Corporation

- Acteon Group

- Ray Medical

- Others

Frequently Asked Questions

The global digital intraoral sensors and consumables market reaches US$ 467.3 million in 2026.

Rising dental disease burden, rapid adoption of digital dentistry workflows, demand for low-radiation and high-resolution imaging, and increasing penetration of dental clinics in emerging markets are driving growth of the global digital intraoral sensors and consumables market.

North America leads with 39% share in 2025.

Strong opportunities exist in wireless and AI-enabled intraoral sensors, replacement demand for PSP plates and legacy systems, expanding private dental chains in Asia-Pacific, and integration of imaging with CAD/CAM and practice management platforms.

Dentsply Sirona, Envista, Planmeca Oy, Carestream Dental, LLC, and Danaher Corporation.