- Retail

- Floral Nectar Market

Floral Nectar Market Size, Share, and Growth Forecast, 2026 – 2033

Floral Nectar Market by Flower Source (Clover, Lavender, Wildflower, Others), Sales Channel (Supermarkets/Hypermarket, Online Retail), Application (Food & Beverages, Cosmetics & Personal Care, Others), and Regional Analysis 2026 – 2033

Floral Nectar Market Size and Trends Analysis

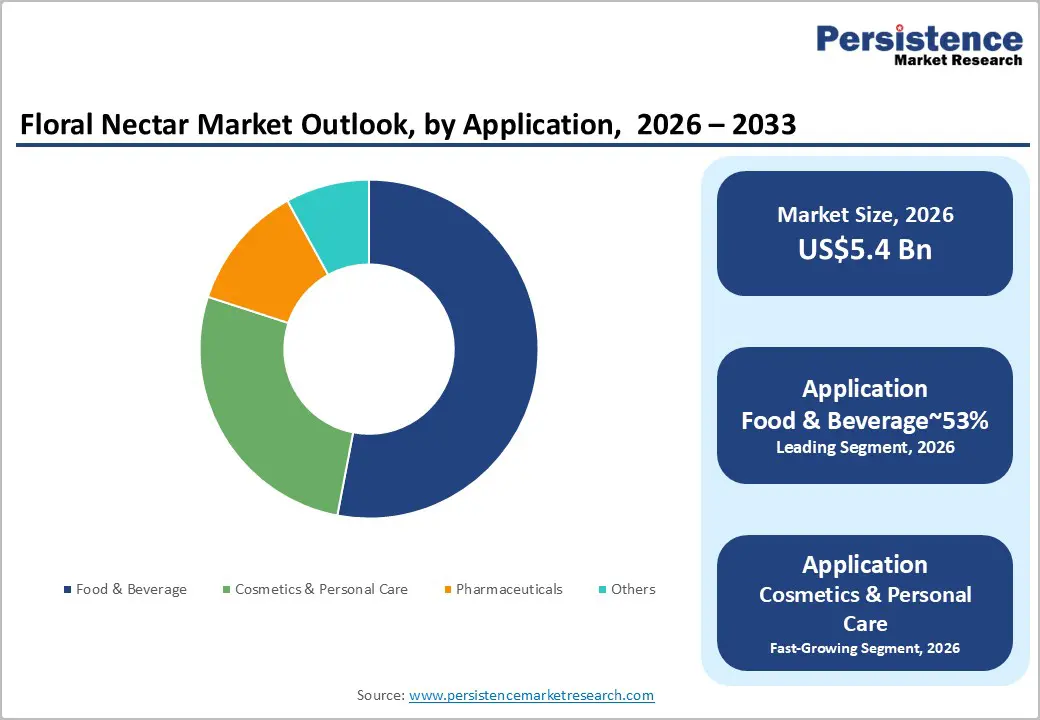

The global floral nectar market size is likely to be valued at US$5.4 billion in 2026 and is expected to reach US$7.8 billion by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033, driven by the rising prevalence of lifestyle-related health conditions, which have catalyzed the demand for low-glycemic and nutrient-rich sugar alternatives. Rising demand for natural sweeteners amid health consciousness drives this expansion. Additionally, the integration of floral nectars into the cosmetics and pharmaceutical sectors has diversified revenue streams beyond traditional food and beverage applications. Increased transparency in supply chains and the adoption of sustainable beekeeping practices have further solidified consumer trust, ensuring steady market progression. Clean-label trends and applications in food, cosmetics, and pharmaceuticals bolster market growth.

Key Industry Highlights:

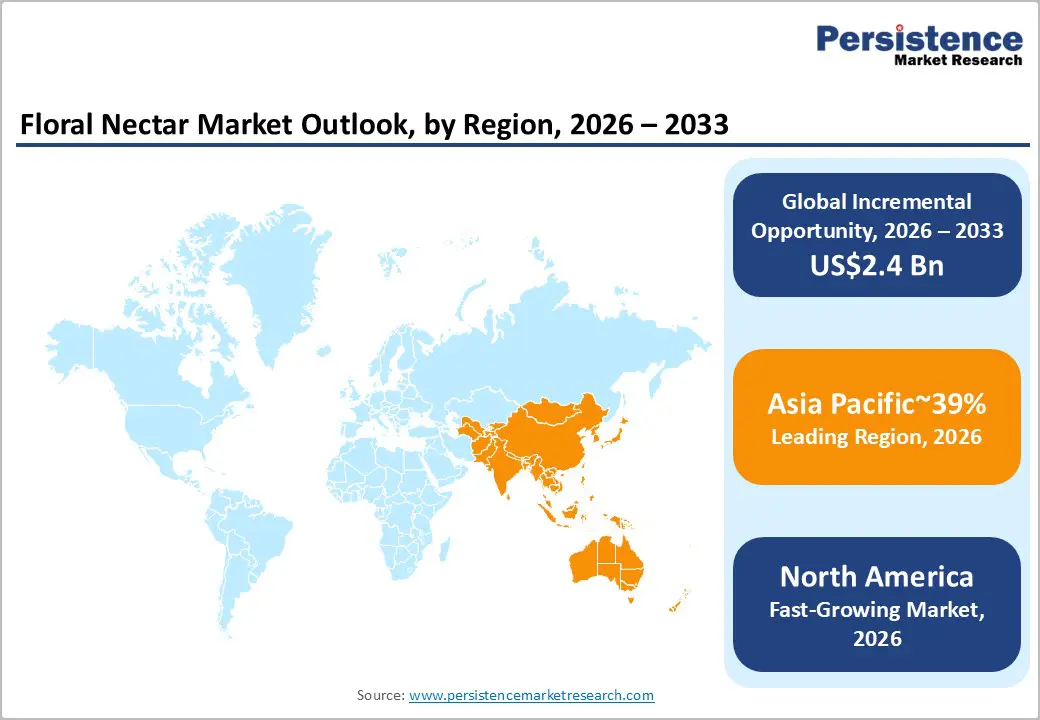

- Leading Region: Asia Pacific is projected to lead due to extensive floral biodiversity and expanding wellness consumption, accounting for approximately 39% share in 2026, supported by evolving extraction technologies, large-scale agricultural processing capacity, and a strong ecosystem of regional suppliers.

- Fastest-growing Region: North America is anticipated to grow fastest due to expanding natural sweetener adoption, regulatory emphasis on sugar transparency, and increasing integration of botanical nectars across functional foods, beverages, and nutraceutical formulations supported by innovation ecosystems.

- Leading Flower Source: Clover is expected to lead, accounting for approximately 34% share in 2026, propelled by its extensive cultivation as a nitrogen-fixing cover crop and its high nectar yield.

- Leading Application: Food & Beverages is projected to dominate for ingredient simplicity, formulation flexibility, cost alignment with natural sweeteners, and functional use across bakery, dairy, confectionery, and beverage manufacturing, holding approximately 53% share in 2026, supported by formulation expansion across major beverage and flavor ecosystems.

| Key Insights | Details |

|---|---|

|

Floral Nectar Market Size (2026E) |

US$5.4 Bn |

|

Market Value Forecast (2033F) |

US$7.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Rising Consumer Preference for Clean Label and Naturally Derived Sweeteners

Consumer dietary priorities are increasingly shifting toward ingredient transparency and minimally processed sweetening solutions. Heightened awareness regarding potential health concerns linked with synthetic sweeteners and refined sugar substitutes is reshaping purchasing behavior across global food categories. Consumers increasingly evaluate product formulations through label scrutiny, prioritizing ingredients recognized for natural origin and minimal chemical processing. Floral nectars derived from botanical sources align with this evolving preference framework, reinforcing their positioning within clean-label product portfolios. Food and beverage manufacturers are responding by integrating plant-derived nectar sweeteners into reformulated products targeting health-conscious consumer segments. Regulatory emphasis on ingredient transparency and traceability further strengthens demand for naturally sourced sweetening alternatives.

The shift toward ethical consumption patterns further amplifies demand within plant-based, organic, and specialty dietary product categories. Floral nectars derived directly from botanical sources are increasingly incorporated into vegan and organic formulations seeking ingredient authenticity. This trend influences upstream sourcing strategies, encouraging closer integration between agricultural producers, ingredient processors, and consumer goods manufacturers. Advances in filtration, enzymatic stabilization, and quality verification technologies enhance nectar consistency while preserving natural product attributes. These technological improvements support broader industrial adoption across packaged foods, beverages, and health-oriented formulations. Consequently, clean label consumer expectations are emerging as a foundational demand driver shaping long-term market expansion.

Expanding Functional Nutrition and Preventive Health Positioning of Floral Nectar

The market is increasingly supported by rising consumer alignment with functional nutrition and preventive health priorities. Floral nectars possess bioactive compounds associated with antioxidant, antimicrobial, and anti-inflammatory properties valued in wellness-oriented consumption patterns. These functional attributes position floral nectar as more than a conventional sweetening ingredient within modern dietary frameworks. Growing public health discourse surrounding sugar reduction encourages substitution toward naturally derived sweeteners with comparatively balanced metabolic profiles. Botanical nectars are therefore increasingly integrated into formulations addressing nutritional balance and metabolic health concerns. Regulatory discourse across health institutions emphasizing reduced refined sugar intake indirectly strengthens the positioning of botanical nectar alternatives.

Beyond traditional food applications, the functional composition of premium floral nectars enables entry into specialized nutraceutical and pharmaceutical adjacent product categories. Certain botanical nectar varieties demonstrate antimicrobial and immune supportive attributes that attract formulation interest within wellness supplements. These properties support inclusion in lozenges, immunity formulations, and health tonics positioned around preventive healthcare narratives. Pharmaceutical ingredient developers are also evaluating botanical nectar derivatives for excipient and therapeutic support roles within natural health products. This convergence between nutrition science, wellness branding, and preventive health consumption expands the value proposition of floral nectars.

Barrier Analysis – Pollinator Decline and Environmental Instability Affecting Floral Nectar Supply

The floral nectar market faces structural supply instability driven by ecological pressures affecting pollinator populations and flowering ecosystems. Honeybees and other pollinating insects play a fundamental role in the pollination of flowers, which affects nectar production, but for direct floral nectar harvesting, the plants themselves are the source. Declining pollinator populations linked to climate variability, pesticide exposure, and habitat fragmentation have disrupted nectar production cycles. These environmental pressures create fluctuations in raw material availability across key nectar-producing regions. Agricultural yield variability consequently affects the stability of nectar harvesting and processing operations throughout the supply chain. Ingredient processors experience procurement uncertainty when seasonal flowering patterns become less predictable under changing climatic conditions.

Raw material unpredictability translates into unstable input pricing and margin compression across nectar-dependent product categories. Food and beverage manufacturers operating at an industrial scale require dependable ingredient sourcing to sustain large volume production cycles. When nectar supply tightens due to ecological disruptions, processors face procurement delays and rising acquisition costs. These pressures occasionally encourage substitution toward more stable sweetening agents that offer predictable supply continuity. Environmental risks, therefore, introduce structural uncertainty into the floral nectar value chain, affecting long-term sourcing strategies. The situation also increases reliance on geographically diversified nectar procurement networks to mitigate regional production disruptions.

Cost Premium and Price Volatility Limiting Competitive Penetration

The market faces structural cost pressures arising from comparatively complex extraction, purification, and stabilization processes. Floral nectar processing requires specialized filtration, concentration, and preservation techniques that elevate operational expenditure relative to conventional sugar refinement. Raw material procurement further contributes to cost instability because nectar availability is influenced by seasonal flowering cycles and agricultural variability. These supply-side fluctuations introduce procurement uncertainty for ingredient processors and packaged food manufacturers relying on consistent input sourcing. Elevated production costs translate into higher final product pricing across retail and industrial ingredient channels. As a result, floral nectar ingredients often occupy premium product segments rather than mainstream sweetener categories. This pricing dynamic constrains large-scale substitution of refined sugars within cost-sensitive food manufacturing environments.

Price volatility across nectar inputs also introduces margin management challenges throughout the value chain. Manufacturers operating within highly competitive food and beverage categories prioritize ingredient stability to maintain predictable production economics. Lower-priced sweetening alternatives such as glucose syrups and refined sugar continue to dominate formulations targeting price-sensitive consumer markets. These substitutes provide cost efficiency and dependable supply continuity that many mass market producers require. Consequently, floral nectar ingredients face structural penetration limits within high-volume packaged food segments. Retail price sensitivity further restricts adoption in emerging economies where affordability remains a primary purchasing criterion. This cost differential, therefore, remains a persistent barrier affecting broader market expansion across global floral nectar applications.

Opportunity Analysis – Expansion of Direct-to-Consumer and Digital Retail Ecosystems

The floral nectar market is gaining strategic opportunities from the accelerating digital transformation of specialty food retail channels. Online commerce platforms enable nectar producers to directly engage consumers without relying exclusively on traditional wholesale distribution structures. This shift improves margin realization by reducing intermediary layers across the retail value chain. Digital storefronts allow brands to communicate detailed product narratives centered on botanical origin, floral diversity, and functional attributes. Consumers increasingly value transparency regarding ingredient provenance, which online retail environments effectively facilitate through detailed product storytelling. Social commerce platforms and digital marketplaces further expand visibility for niche and artisanal nectar varieties. These mechanisms collectively strengthen market access for producers offering differentiated botanical nectar products.

The growth of direct consumer engagement also supports innovative commercial models within the premium sweetener segment. Subscription-based purchasing systems enable recurring sales while strengthening long-term consumer relationships for specialty nectar products. Digital channels provide access to geographically diverse nectar varieties that may not be widely distributed through conventional retail networks. Producers can showcase distinct floral sources such as lavender, acacia, and other regionally unique botanical nectars. This variety-driven positioning enhances consumer exploration within natural sweetener categories and supports product differentiation. Digital retail analytics additionally provide producers with granular insights into consumer preference patterns.

Functional Food Innovation and Digital Channel Expansion

The floral nectar market is gaining momentum from increasing innovation within functional foods and health-oriented beverage formulations. Floral nectars possess antioxidant compounds and bioactive constituents that align with evolving consumer interest in wellness-supportive ingredients. Product developers are incorporating botanical nectar varieties into teas, herbal beverages, and dietary supplements positioned around natural health benefits. These formulations emphasize naturally derived sweetening combined with perceived nutritional advantages compared with conventional refined sugar alternatives. Consumer awareness regarding immune support and metabolic balance is reinforcing demand for ingredients associated with natural antioxidant profiles. As health-oriented product development accelerates, floral nectars are increasingly positioned as multifunctional ingredients across nutraceutical and beverage innovation pipelines. This convergence between flavor enhancement and functional nutrition strengthens the strategic relevance of botanical nectar inputs.

Parallel expansion of digital retail infrastructure further amplifies this opportunity by improving market accessibility for specialized nectar products. E-commerce platforms enable producers to reach health-conscious consumers seeking differentiated functional sweeteners. Direct-to-consumer engagement supports educational marketing around botanical sources and associated wellness attributes. Online retail ecosystems also facilitate cross-border availability of premium nectar varieties that remain limited in traditional retail environments. Emerging Asian markets are demonstrating heightened receptivity to functional beverage formats integrating natural botanical sweeteners. Increasing digital penetration across these regions supports wider product visibility and consumer experimentation. The intersection of functional food innovation and digital commerce expansion is creating a structurally favorable opportunity environment for the market.

Category–wise Analysis

Flower Source Insights

Clover is projected to lead the market, accounting for approximately 34% share in 2026, supported by its entrenched agricultural footprint and high nectar productivity across temperate farming systems. Adoption remains anchored by Clover's neutral sensory profile and reliable supply economics, making it the industrial standard for bulk sweetening bases and cosmetic formulations. Extensive cultivation as a nitrogen-fixing cover crop within regenerative agriculture programs expands acreage and ensures abundant raw material for nectar extraction. Advances in bloom forecasting and crop optimization, including initiatives by Syngenta and enhanced seed varieties from BASF, are improving harvest predictability and nectar yields. Market incumbents such as Givaudan, Symrise, and Robertet leverage large-scale processing ecosystems and traceable supply chains to anchor enterprise procurement. This combination of global cultivation scale, ecosystem lock-in, and cost-efficient sourcing sustains clover's dominance within structured food and cosmetic ingredient supply models.

Lavender is anticipated to be the fastest-growing segment, propelled by expanding demand for bioactive botanical ingredients across wellness, premium beverages, and neuro-cosmetic formulations. Growth momentum is reinforced by lavender nectar’s high terpene and linalool content, enabling functional positioning in stress-relief skincare, sleep-support drinks, and aromatherapeutic confectionery. Technology inflection points such as supercritical CO extraction and cold-pressed preservation methods are materially enhancing purity and bioactive retention, elevating lavender from a fragrance input to a performance ingredient. Ingredient houses, including Givaudan and Symrise, are introducing advanced nectar-actives, while vertically integrated brands such as L’Oréal en Provence expand pesticide-free lavender ecosystems. As validation across cosmetic science, functional beverage R&D, and wellness markets deepens, lavender nectar is positioned to outpace broader market expansion through innovation-driven adoption.

Application Insights

The food & beverage segment is expected to lead, accounting for approximately 53% share in 2026, underpinned by its entrenched role as the primary industrial consumption channel across bakery, confectionery, dairy, and functional beverage manufacturing. Adoption remains anchored by nectar’s dual functionality as both a natural sweetener and a botanical flavor enhancer, enabling manufacturers to reformulate products while maintaining taste complexity and clean-label positioning. Global beverage and food companies are prioritizing ingredient substitution strategies that replace refined sugar and high-fructose syrups sugar and high-fructose syrups with floral nectars to align with evolving consumer expectations for natural sugars. Industry participants, including Monin Inc., Tate & Lyle, and The Coca-Cola Company, continue expanding nectar-based formulations supported by flavor stabilization technologies developed by Kerry Group, reinforcing the segment’s structural dominance.

The cosmetics & personal care segment is expected to be the fastest-growing segment, driven by expanding demand for botanical active ingredients within skincare and haircare formulations. Growth is being catalyzed by ingredient innovation that positions floral nectars as multifunctional components delivering antioxidant protection, humectant hydration, and micronutrient enrichment within premium beauty products. Cosmetic manufacturers are increasingly integrating nectar-derived extracts into serums, creams, and hair treatments as consumers gravitate toward clean beauty formulations emphasizing natural efficacy and ingredient transparency. Companies including L'Oréal, Givaudan, and SILAB are developing specialized nectar platforms and cosmetic actives, while luxury brands such as Estée Lauder and Dior incorporate rare botanical nectars into high-value skincare ecosystems to capture early innovation demand.

Regional Insights

Asia Pacific Floral Nectar Market Trends

Asia Pacific is expected to remain the leading regional market, accounting for approximately 39% in 2026, as the integrated agriculture supply chain, extensive floral biodiversity, and expanding wellness consumption reinforce structural dominance. The region is projected to sustain leadership through large-scale agricultural output, cost-efficient processing infrastructure, and strong alignment between traditional medicine systems and modern functional food applications. Growing use of nectar-based ingredients in herbal beverages, nutraceutical formulations, and natural sweeteners is anticipated to strengthen regional industrial demand. Vendor ecosystems led by Givaudan, Symrise, and Robertet are expected to expand product portfolios while scaling advanced nectar extraction and purification technologies to meet international quality standards.

China is expected to serve as the regional anchor shaping Asia Pacific’s long-term market trajectory through its vast agricultural base and technologically evolving extraction sector. and the technologically evolving honey processing sector. Regulatory alignment with international food safety standards is expected to accelerate cross-border trade while reinforcing consumer trust in premium floral extracts and specialty nectar formulations. Domestic beverage and functional food producers are anticipated to integrate specialty floral nectars into wellness formulations, supporting demand across nutraceutical and herbal drink segments. Industry participants, including Yili Group and Comvita, are projected to strengthen premium nectar positioning through product innovation, origin-certified sourcing, and expanding e-commerce distribution channels.

North America Floral Nectar Market Trends

North America is expected to register the fastest growth trajectory, as natural sweetener substitution and clean-label nutrition trends accelerate consumer adoption. The region is projected to expand rapidly through strong health-driven purchasing behavior, advanced food innovation ecosystems, and regulatory frameworks encouraging reduced refined sugar consumption. Expanding demand for functional beverages, nutraceutical blends, and premium floral nectars is anticipated to strengthen commercial integration across food processing and wellness product categories. Industry participants, including Givaudan, Symrise, and Mane, are expected to expand clean-label nectar portfolios while strengthening fair-trade sourcing, organic certification, and sustainable supply chain practices.

The U.S. is expected to function as the regional anchor shaping North America's expansion through its mature retail ecosystem and rapidly evolving functional food sector. Regulatory transparency around sugar labeling and ingredient disclosure is anticipated to reinforce demand for plant-derived natural sweeteners across packaged foods and beverages. Vendor strategies are projected to increasingly emphasize traceability, digital retail expansion, and direct-to-consumer platforms led by companies such as Specialty Nectar Brands and Botanical Extract Suppliers, strengthening premium nectar positioning in health-oriented consumer segments.

Europe Floral Nectar Market Trends

Europe is expected to remain a structurally mature and premium-oriented floral nectar market, supported by strong regulatory harmonization and consumer preference for traceable natural ingredients. The region is projected to maintain steady market stability through strict quality enforcement under EU food safety regulations and broader clean-label food policies encouraging natural sweetener adoption. Demand is anticipated to remain concentrated in monofloral and organic nectar varieties as European consumers increasingly prioritize biodiversity preservation, ethical sourcing, and residue-free agricultural production. Market structure is expected to remain moderately consolidated with established processors such as Givaudan, Symrise, and Robertet strengthening premium positioning through sustainable sourcing and product authenticity verification.

Germany is projected to act as the regional anchor shaping Europe's market momentum through its advanced botanical extraction infrastructure and strong cross-border trade networks. Regulatory compliance, strict residue monitoring, and growing demand for specialty nectar ingredients are expected to drive innovation across beverage, gourmet food, and functional nutrition applications. Industry participants, including Symrise and other local extractors, are anticipated to expand value-added nectar formulations targeting premium culinary and craft beverage segments, reinforcing Europe's long-term premiumization trajectory.

Competitive Landscape

The floral nectar market is moderately fragmented, with leadership concentrated among global ingredient and botanical extract suppliers such as Givaudan, International Flavors & Fragrances, Symrise, and Firmenich. These organizations exert functional influence through their extensive natural extract portfolios, advanced formulation capabilities, and established procurement relationships with food, beverage, fragrance, and personal care manufacturers. Their technological footprint across botanical sourcing, extraction, and ingredient standardization shapes quality benchmarks and supply chain practices across the industry. Additional participants, including Takasago International Corporation, Kerry Group, and Sensient Technologies, further reinforce market stability through integrated taste, fragrance, and nutrition platforms that support industrial-scale product development.

Competitive positioning across the market reflects a clear bifurcation between vertically integrated botanical extract specialists and diversified flavor and fragrance conglomerates. Companies such as Robertet Group and Mane Group emphasize natural raw-material sourcing and artisanal extraction expertise, while broader ingredient platforms such as COFCO Corporation and Kerry Group leverage global agricultural supply networks and formulation ecosystems. Regional specialists, including Comvita, Guanshengyuan Group, Beijing Baihua Bee Industry, Herbarom, Jiangxi Wang's Bee Garden, and Sioux Honey Association, contribute differentiated capabilities in monofloral sourcing, apiculture integration, and premium botanical ingredients. Industry behavior increasingly reflects ecosystem integration across sustainable sourcing initiatives, digital traceability systems, and closer collaboration between agricultural producers, ingredient processors, and consumer goods manufacturers, gradually reinforcing supplier credibility.

Key Industry Developments:

- In March 2026, Symrise AG reported a record 2.8% organic sales growth in 2025, driven by high demand for its Maison Lautier natural flower extracts. This development reinforces the premiumization of floral nectars in fine fragrances and personal care, ensuring stable long-term revenue for high-end extract producers.

- In February 2026, LMR (Laboratoire Monique Rémy by IFF) unveiled Tonka Bean CO Absolute, utilizing planet-friendly CO extraction. This development offers a high-purity, sustainable alternative to traditional solvent-based extracts, meeting the surging demand for clean-label "gourmand" fragrance profiles.

Companies Covered in Floral Nectar Market

- Givaudan

- International Flavors & Fragrances

- Symrise

- Firmenich

- Takasago International Corporation

- Kerry Group

- Sensient Technologies

- Robertet Group

- Mane Group

- COFCO Corporation

- Comvita

- Guanshengyuan Group

- Beijing Baihua Bee Industry

- Herbarom

- Jiangxi Wang's Bee Garden

- Sioux Honey Association

Frequently Asked Questions

The global floral nectar market is projected to be valued at US$5.4 billion in 2026 and is expected to reach US$7.8 billion by 2033, supported by rising consumer preference for natural sweeteners and clean-label ingredients across food, wellness, and cosmetic applications.

Growing health awareness and increasing scrutiny of ingredient labels are encouraging consumers to shift away from refined sugars and synthetic sweeteners. Floral nectars such as clover, lavender, and wildflower nectars provide natural origin, functional nutrients, and perceived health benefits, making them attractive for food manufacturers reformulating products around clean-label and plant-derived ingredient strategies.

The floral nectar market is forecast to grow at a CAGR of 5.4% from 2026 to 2033, reflecting expanding applications across functional foods, nutraceutical products, and natural personal care formulations.

Asia Pacific is the leading regional market, accounting for approximately 39% share in 2026, supported by strong apiculture infrastructure, extensive floral biodiversity, and growing demand for natural sweeteners in functional foods, herbal beverages, and traditional wellness products.

The market is moderately fragmented, with key players including Dabur India Ltd., Apis India Ltd., Comvita Limited, Capilano Honey Ltd., and Wholesome Sweeteners Inc. These companies compete through diversified nectar portfolios, vertically integrated sourcing networks, and expanding distribution across food, wellness, and specialty retail channels.