- Pharmaceuticals

- Oral Anticoagulant Market

Oral Anticoagulant Market Size, Share, and Growth Forecast, 2026 – 2033

Oral Anticoagulant Market by Product Type (Warfarin, Novel Oral Anticoagulants), Disease Indication (Pulmonary Embolism (PE), Deep Vein Thrombosis (DVT), Heart Attacks, Atrial Fibrillation (AF)), Distribution Channel (Retail Pharmacies, Online Pharmacies, Hospital Pharmacies), and Regional Analysis for 2026-2033

Oral Anticoagulant Market Share and Trends Analysis

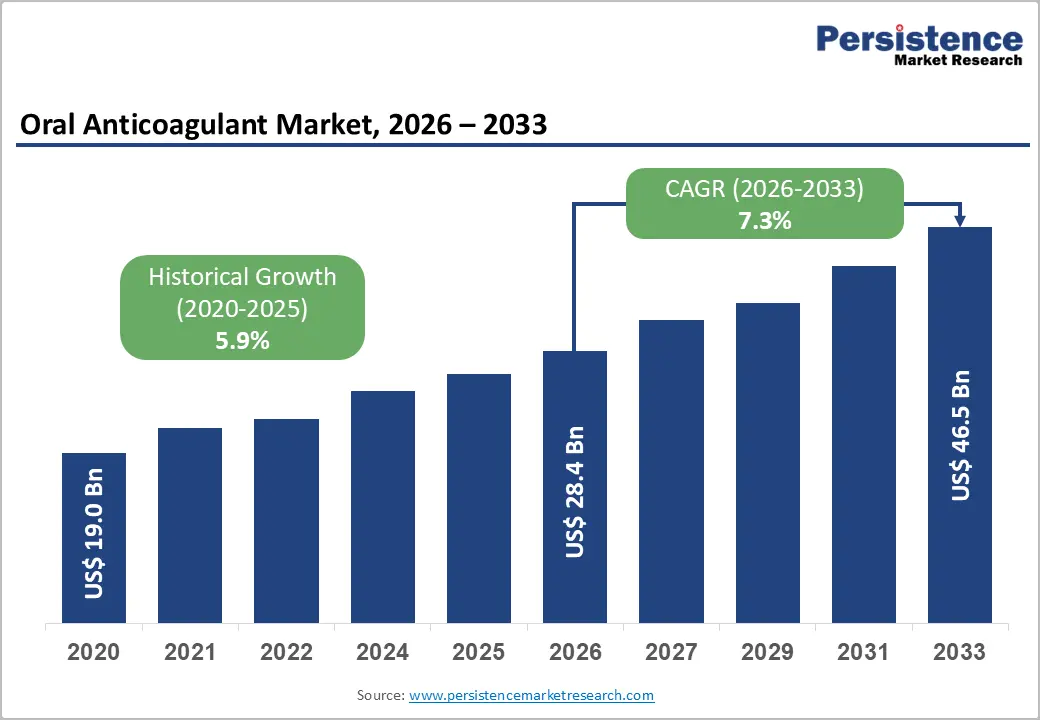

The global oral anticoagulant market size is likely to be valued at US$ 28.4 billion in 2026, and is projected to reach US$ 46.5 billion by 2033, growing at a CAGR of 7.3% during the forecast period 2026-2033.

The market is poised for sustained growth primarily due to rising prevalence of cardiovascular disorders (CVDs) and thromboembolic conditions across aging populations. Expanding clinical awareness among healthcare providers and patients is accelerating early adoption of anticoagulant therapies. Integration of digital health tools, such as remote patient monitoring and adherence-tracking applications, is enhancing treatment management and reducing adverse events, thereby supporting broader acceptance. Strengthening healthcare infrastructure, particularly in emerging economies, facilitates improved accessibility to prescription medications and specialist care, enabling higher treatment penetration. Regulatory encouragement of evidence-based treatment protocols and guideline updates is reinforcing confidence in oral anticoagulant therapies among practitioners.

Key Industry Highlights

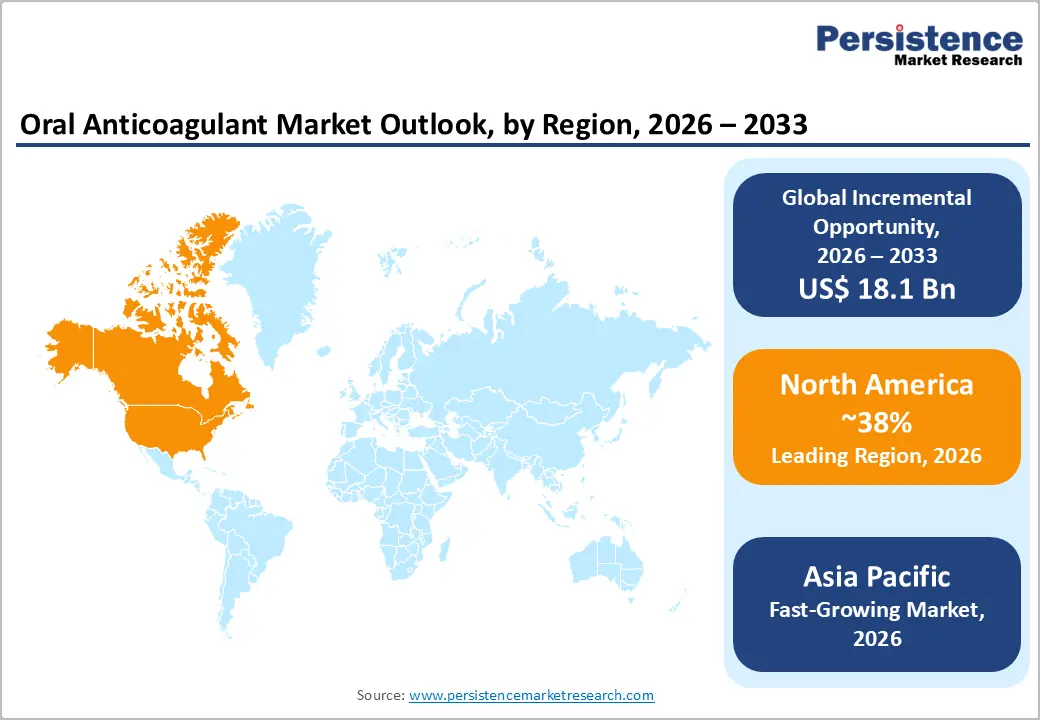

- Dominant Region: North America is projected to hold about 38% market share in 2026, driven by cardiovascular disease and wide adoption of non–vitamin K antagonist oral anticoagulants (NOAC).

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by rising CVD prevalence.

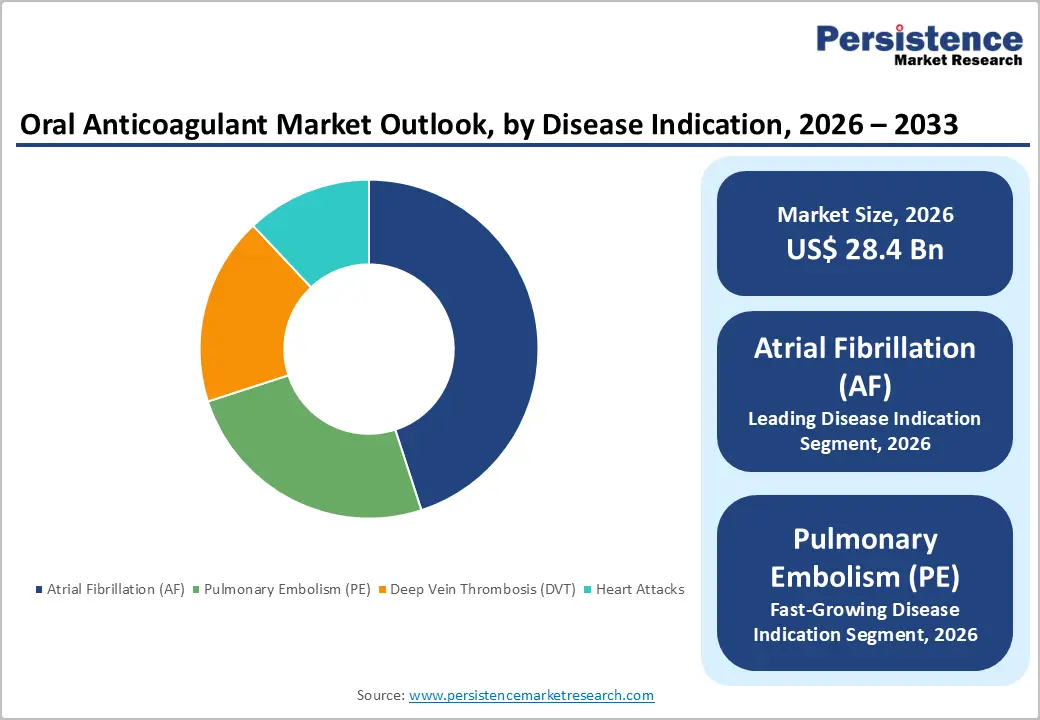

- Leading Disease Indication: Atrial fibrillation (AF) is expected to hold an estimated 45% revenue share in 2026, propelled by high prevalence and stroke risk.

- Fastest-growing Disease Indication: Pulmonary embolism is poised to grow the fastest from 2026 to 2033, owing to early diagnosis and treatment.

| Key Insights | Details |

|---|---|

|

Oral Anticoagulant Market Size (2026E) |

US$ 28.4 Bn |

|

Market Value Forecast (2033F) |

US$ 46.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Incidence of Cardiovascular and Thromboembolic Conditions

Sustained growth in cardiovascular and thromboembolic conditions is shaping demand due to fundamental shifts in public health drivers. Government data from the U.S. Centers for Disease Control and Prevention (CDC) shows that up to 900,000 Americans are affected by venous thromboembolism (VTE) each year, with an estimated 60,000–100,000 deaths annually from these blood clot events. VTE, which includes deep vein thrombosis and pulmonary embolism, coexists with cardiovascular risk profiles and frequently occurs in conjunction with hospitalizations, cancer treatment, and other comorbidities.

Parallel to thromboembolic trends, cardiovascular disease remains a pervasive burden on public health systems, with CDC figures indicating that heart disease accounts for hundreds of thousands of deaths annually, translating to someone dying of cardiovascular disease every 34 seconds in the United States. These trends are intimately linked to rising prevalence of core risk factors such as high blood pressure, diabetes, and obesity, which increase the likelihood of clinical events requiring long-term management. The aggregation of these conditions in aging and at-risk populations elevates clinical complexity, prolongs treatment cycles, and increases utilization of preventive therapies.

Expansion of Healthcare Infrastructure and Clinical Awareness

Improved access to hospitals, clinics and diagnostic services expands opportunities for early detection and management of conditions that require anticoagulation therapy. When primary care and specialty cardiology services are more readily available, clinicians can diagnose arrhythmias, deep vein thrombosis and other thromboembolic disorders sooner and initiate appropriate treatment protocols. Public health surveillance systems and electronic health records that support clinical decision-making contribute to more consistent prescribing practices and adherence to evidence-based guidelines.

Increased clinical awareness among healthcare professionals and patients drives demand for appropriate therapeutic interventions and reinforces preventive healthcare orientation. Educational initiatives, clinical practice guidelines and decision support tools improve clinicians’ confidence in prescribing newer oral agents with favorable safety profiles, while patient outreach programs enhance understanding of stroke risk and therapy benefits. Public health campaigns and continuing professional development initiatives align provider competencies with evolving standards of care and encourage uptake of recommended therapies.

Bleeding Risk and Clinical Safety Concerns

Oral anticoagulants function by inhibiting blood clot formation, which is essential in preventing conditions such as stroke, deep vein thrombosis, and pulmonary embolism. The therapeutic mechanism that reduces clotting simultaneously increases the likelihood of uncontrolled bleeding events, ranging from minor bruising to life-threatening hemorrhages. Clinical studies and real-world data indicate that patients receiving oral anticoagulants require careful monitoring and dose adjustments, especially those with advanced age, renal impairment, or concomitant use of other medications that influence hemostasis. Healthcare providers demonstrate caution in prescribing oral anticoagulants for high-risk populations due to potential adverse outcomes, which limits widespread adoption in certain segments.

Regulatory authorities impose strict labeling and risk management guidelines to mitigate severe bleeding events, creating barriers for market expansion and new product introductions. The demand for safer, more predictable anticoagulation alternatives drives investment in clinical research and novel drug development, but existing safety concerns slow the uptake of traditional therapies. Payers and healthcare systems incorporate safety-related monitoring costs into treatment considerations, influencing formulary placement and reimbursement policies.

High Therapy Costs and Access Barriers

The oral anticoagulant market experiences significant restraints due to the elevated cost of therapy and restricted patient access. Innovative anticoagulants involve extensive research, clinical trials, and regulatory compliance, which drives pricing structures upward. Payers and healthcare systems frequently impose reimbursement limitations, impacting affordability for patients in both emerging and developed markets. Chronic conditions requiring long-term anticoagulation intensify financial burden on individuals and institutions, limiting adoption rates of novel therapies. Cost-sensitive regions tend to rely on traditional vitamin K antagonists despite clinical advantages of direct oral anticoagulants, slowing overall market penetration and revenue growth.

Access barriers also arise from complex prescription protocols, specialist dependency, and regional disparities in healthcare infrastructure. Patient education, monitoring requirements, and logistical challenges in rural or underserved areas reduce therapy initiation and adherence. Regulatory frameworks in certain countries restrict availability to specific indications or patient populations, creating uneven market distribution. Limited insurance coverage and high out-of-pocket expenses further impede patient uptake, particularly among older adults and individuals with comorbidities.

Penetration in Emerging and Under-Served Markets

Oral anticoagulant demand in emerging and under-served markets is driven by increasing prevalence of cardiovascular disorders and rising awareness of thromboembolic conditions. Healthcare infrastructure expansion, growing insurance coverage, and government-led chronic disease management programs are creating access to prescription therapies. Cost-effective oral anticoagulants provide an alternative to traditional injectable treatments, making them more attractive in regions with limited healthcare resources. Shifts in patient demographics, including aging populations and higher incidence of atrial fibrillation, amplify the need for accessible anticoagulation therapy.

Increasing physician education and adherence to international treatment guidelines enhance prescription rates, while patient education initiatives improve therapy compliance. Affordability strategies, including tiered pricing and generic alternatives, expand reach to wider populations. Emerging markets also present opportunities to integrate digital health solutions for monitoring therapy adherence, reducing adverse events, and enhancing outcomes. Investment in supply chain optimization and community-based programs strengthens brand presence and fosters long-term patient engagement, creating sustainable revenue streams in under-served territories.

Innovation in Drug Formulations and Combination Therapies

The market is experiencing a strong shift toward advanced drug formulations and combination therapies driven by rising demand for safer, more effective treatment options. Novel formulations focus on enhancing bioavailability, reducing dosing frequency, and improving patient adherence, addressing critical challenges in anticoagulation therapy. Extended-release and targeted delivery mechanisms optimize therapeutic outcomes while minimizing bleeding risks and other adverse events. Pharmaceutical companies actively invest in formulation research to differentiate products in a highly competitive landscape, offering tailored solutions for diverse patient populations with complex comorbidities.

Combination therapies integrating anticoagulants with complementary agents aim to streamline treatment regimens for patients with multiple cardiovascular conditions. These therapies facilitate simultaneous management of thrombosis, atrial fibrillation, and other cardiovascular disorders, reducing the need for polypharmacy and improving overall treatment efficiency. Clinical data supporting synergistic effects and favorable safety profiles strengthen market adoption and create opportunities for premium pricing models.

Category-wise Analysis

Disease Indication Insights

AF is poised to lead with a forecasted 45% of the oral anticoagulant market revenue share in 2026, on account of high prevalence among aging populations and significant risk of stroke if untreated. Healthcare providers prioritize anticoagulation in AF patients to prevent thromboembolic complications, establishing a stable patient base for long-term therapy. The chronic nature of AF and associated comorbidities such as hypertension and heart failure necessitate sustained treatment, supporting consistent revenue streams.

Clinical guidelines from organizations such as the American Heart Association (AHA) and European Society of Cardiology (ESC) reinforce anticoagulation as a standard of care, strengthening adoption. Patient education campaigns on stroke prevention enhance adherence and trust in prescribed therapy.

Pulmonary embolism is anticipated to be the fastest-growing segment between 2026 and 2033, driven by increased diagnostic detection and early intervention strategies. Advances in imaging modalities and clinical risk scoring enable timely identification of PE cases, expanding the treatable population. Early anticoagulant initiation improves clinical outcomes and reduces hospitalizations, creating measurable demand for oral therapies in both inpatient and post-discharge care. The convenience of novel oral anticoagulants, such as NOACs, for outpatient continuation post-hospitalization promotes faster adoption and improves patient adherence.

Distribution Channel Insights

Hospital pharmacies are positioned as the leading segment with nearly 50% market share in 2026, supported by high clinical credibility, provider referrals, and integration with inpatient anticoagulation protocols. Hospitals serve as primary sites for initiation of anticoagulant therapy, especially for acute cases such as DVT and PE. Institutional formularies, clinical monitoring capabilities, and patient education programs ensure safe and effective treatment administration. Hospital pharmacies facilitate early therapy adoption and provide continuity of care through discharge planning and outpatient prescription coordination.

Online pharmacies are expected to emerge as the fastest-growing segment between 2026 and 2033, driven by digitalization, convenience, and cost-efficiency. Increasing consumer acceptance of e-pharmacy platforms allows patients to refill prescriptions remotely, supporting continuity of therapy and improved adherence. Telemedicine integration and digital prescription services reduce barriers for patients in rural or underserved regions, expanding market reach. E-commerce platforms provide subscription models, home delivery, and automated reminders, enabling consistent therapy maintenance. Regulatory frameworks increasingly recognize licensed online pharmacy operations, providing legal clarity for digital dispensing.

Regional Insights

North America Oral Anticoagulant Market Trends

North America is expected to lead with an estimated 38% of the oral anticoagulant market share in 2026, supported by high prevalence of atrial fibrillation, venous thromboembolism, and related cardiovascular conditions in the United States and Canada. Widespread integration of advanced diagnostic tools, including high-resolution imaging and risk stratification algorithms, enables early detection and timely initiation of therapy, expanding the treatable patient pool. Established pharmaceutical companies with robust pipelines for novel oral anticoagulants (NOACs) and combination therapies drive continuous product innovation and strengthen market penetration across diverse care settings.

Leadership is further reinforced by sophisticated healthcare financing structures in the United States and Canada that facilitate coverage of premium therapies. Health systems emphasize outcomes-driven treatment models, encouraging prescription of therapies with proven efficacy and safety profiles. Clinical awareness of bleeding risk management and patient adherence strategies improves long-term therapy retention. Extensive real-world evidence from ongoing clinical trials highlights superior pharmacokinetics and reduced monitoring requirements of advanced formulations. Emphasis on post-discharge anticoagulation management and integration with outpatient care pathways accelerates adoption rates.

Europe Oral Anticoagulant Market Trends

Europe maintains a significant position in the oral anticoagulant market, supported by a high prevalence of atrial fibrillation, venous thromboembolism, and other cardiovascular disorders across Germany, France, the United Kingdom, and Italy. Widespread implementation of advanced diagnostic technologies, including high-resolution imaging and clinical risk scoring tools, enables timely identification of treatable patients. Healthcare systems emphasize evidence-based therapy selection, promoting the use of NOACs and other novel oral anticoagulants and combination therapies with improved safety profiles. Strong clinical research networks facilitate real-world evidence generation, supporting prescriber confidence and enhancing long-term therapy adherence.

Market growth is reinforced by structured reimbursement frameworks that support premium therapy adoption and outcomes-driven care models. Emphasis on post-discharge continuity of therapy and outpatient anticoagulation programs reduces hospitalization rates and improves clinical efficiency. Healthcare providers focus on personalized treatment regimens, integrating patient risk assessment and bleeding management strategies to optimize outcomes. Ongoing clinical trials and regulatory support for next-generation formulations accelerate introduction of advanced oral anticoagulants. Patient education initiatives and professional training programs strengthen therapy adherence and awareness of anticoagulation benefits.

Asia Pacific Oral Anticoagulant Market Trends

Asia Pacific is forecasted to be the fastest-growing market for oral anticoagulants between 2026 and 2033, stimulated by increasing prevalence of atrial fibrillation, venous thromboembolism, and other cardiovascular disorders in China, India, and Australia. Expanding access to advanced healthcare infrastructure and improved diagnostic capabilities enables earlier detection and timely treatment initiation, broadening the treatable patient population. Rising adoption of novel oral anticoagulants (NOACs) supported by clinical evidence on safety and efficacy drives market expansion. Growing awareness among healthcare providers regarding risk stratification, bleeding management, and therapy adherence enhances prescription confidence and long-term patient retention.

Market acceleration is also supported by increasing outpatient care adoption and structured post-discharge anticoagulation programs, facilitating continuity of therapy and reducing hospitalization burden. Government-led initiatives and healthcare policy reforms aimed at cardiovascular disease management strengthen demand for innovative oral anticoagulant formulations. Rapid urbanization, rising income levels, and increased insurance coverage contribute to higher treatment accessibility. Clinical trials conducted locally provide region-specific evidence, reinforcing adoption of advanced formulations and combination therapies.

Competitive Landscape

The global oral anticoagulant market demonstrates a moderately consolidated structure, with a limited number of major pharmaceutical companies capturing the largest revenue share while smaller regional firms focus on specilized segments. Key players such as Johnson & Johnson Services Inc, Pfizer, GlaxoSmithKline Plc, Abbott Laboratories, and Boehringer Ingelheim GmbH are estimated to collectively represent approximately 60–65% of the global market in 2026. These companies maintain competitive advantage through extensive clinical trial portfolios, established brand recognition, and well-developed relationships with payers and healthcare providers.

Market dynamics are shaped by significant barriers to entry, including stringent regulatory requirements, substantial research and development costs, and the necessity of robust distribution networks capable of supporting both inpatient and outpatient care. Investment in clinical development and post-marketing surveillance remains critical for gaining prescriber confidence and achieving market acceptance. Geographic expansion strategies, particularly in high-growth regions, further strengthen market position and sustain revenue streams. Strategic collaborations, licensing agreements, and portfolio diversification enable leading companies to respond to evolving patient needs and regulatory expectations.

Key Industry Developments

- In September 2025, biotech company VarmX received Fast Track designation from the U.S. Food and Drug Administration (FDA) for its lead asset VMX-C001, a novel therapy designed to restore coagulation in patients on factor Xa direct oral anticoagulants who require urgent surgery or face severe bleeding, aiming to accelerate development and potential market access.

- In July 2025, Bristol-Myers Squibb and Pfizer launched a direct-to-patient option for Eliquis (apixaban) through the Eliquis-360 Support program, allowing eligible patients in the United States to purchase the oral anticoagulant at more than 40% below list price with direct shipping nationwide.

- In March 2025, Triastek’s 3D-printed gastric retention NOAC, T20G, received Investigational New Drug (IND) clearance from the U.S. FDA, allowing the company to initiate clinical trials. The anticoagulant therapy uses a proprietary 3D microstructure platform to enable once-daily dosing with sustained drug release.

Companies Covered in Oral Anticoagulant Market

- Johnson & Johnson Services Inc

- Pfizer

- GlaxoSmithKline Plc

- Abbott Laboratories

- Boehringer Ingelheim GmbH

- AstraZeneca Plc

- Daiichi Sankyo Company Ltd

- Portola Pharmaceuticals Inc

- Eli Lilly & Company

- Medicure

Frequently Asked Questions

The global oral anticoagulant market is projected to reach US$ 28.4 billion in 2026.

Rising prevalence of cardiovascular disorders, increasing adoption of novel oral anticoagulants such as NOACs, and demand for safer, convenient, and effective anticoagulation therapies are driving the market.

The market is poised to witness a CAGR of 7.3% from 2026 to 2033.

Development of advanced drug formulations, combination therapies, and expansion into high-growth emerging markets represent key opportunities in the market.

Some of the key market players include Johnson & Johnson Services Inc, Pfizer, GlaxoSmithKline Plc, Abbott Laboratories, and Boehringer Ingelheim GmbH.