- Agrochemicals

- Catechol Market

Catechol Market Size, Share, and Growth Forecast 2026 - 2033

Catechol Market by Form (Flakes (Solid Form), Molten (Liquid Form)), Application (Intermediates, Chelating Agents, Processing Aids, Photographic Chemicals, Others), End-user Industry (Agrochemicals, Food and Fragrances, Polymers, Photography, Pharmaceuticals, Others), and Regional Analysis, 2026 - 2033

Catechol Market Size and Trend Analysis

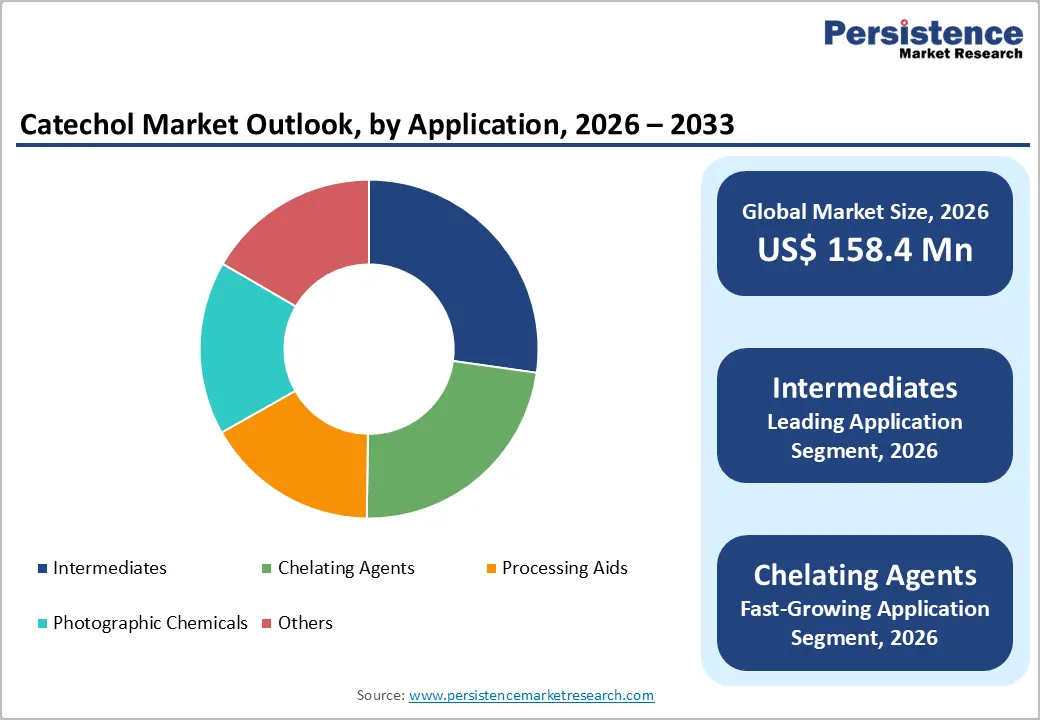

The global catechol market size is expected to be valued at US$ 158.4 million in 2026 and projected to reach US$ 211.3 million by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

Demand growth is primarily driven by expanding applications in polymers, pharmaceuticals, and agrochemicals, where catechol functions as a vital intermediate. Rising polyurethane resin production and increasing use in chelating agents further support consumption. Growth in global chemical manufacturing, with output rising 3.5% in 2024 according to UNIDO, strengthens intermediate demand. Additionally, tightening environmental regulations are encouraging bio-based production routes, supporting sustainable and specialty chemical applications.

Key Industry Highlights:

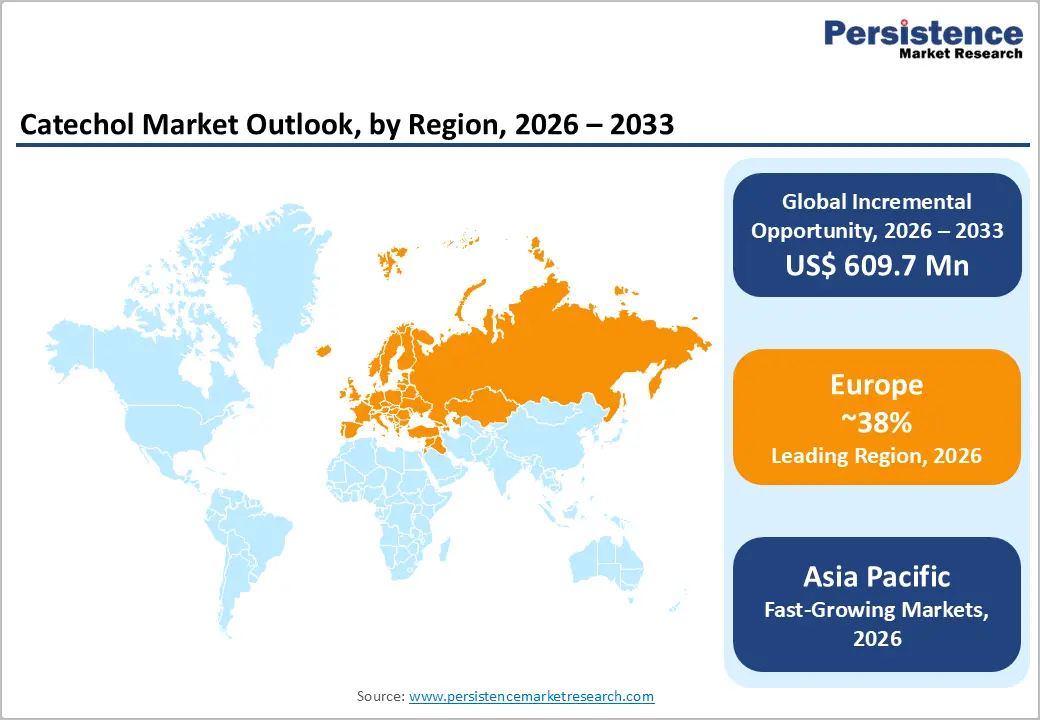

- Leading Region Category: Europe leads the catechol market with 38% share in 2025, supported by regulatory harmonization and strong polymer demand.

- Fastest-Growing Region Category: Asia Pacific is the fastest-growing region with 32% share in 2025 and a 5.2% CAGR (2025–2032), driven by manufacturing expansion in China and India.

- Leading Form Category: Flakes (solid form) dominate the market with 65% share in 2025, preferred for safe logistics and precise dosing in polymers and pharmaceuticals.

- Fastest-Growing End-Use Category: Polymers are the fastest-growing end-use, holding 38% share in 2025, fueled by rising demand in construction and automotive resin applications.

- Key Market Opportunity: Bio-based catechol production offers a significant opportunity, reducing emissions by 70% and aligning with global green policies and sustainable manufacturing trends.

| Key Insights | Details |

|---|---|

|

Catechol Size (2026E) |

US$ 158.4 Million |

|

Market Value Forecast (2033F) |

US$ 211.3 Million |

|

Projected Growth CAGR (2026-2033) |

4.2% |

|

Historical Market Growth (2020-2025) |

4.8% |

Market Dynamics

Drivers - Expanding Pharmaceutical and Polymer Applications

The surge in pharmaceutical formulations and polymer production remains a major driver for the catechol market. Catechol is a key intermediate in synthesizing L-DOPA for Parkinson’s treatment and antioxidants such as butylated hydroxyanisole (BHA). According to the International Council of Chemical Associations (ICCA), global pharmaceutical chemical output grew 5.2% annually between 2020 and 2024, strengthening intermediate demand.

In polymers, catechol supports the production of polyester resins and epoxy hardeners used in coatings and engineering materials. The European Chemical Industry Council (CEFIC) reported 4.1% growth in specialty polymers in 2024, reflecting expanding industrial and construction activities. This sustained demand from healthcare and advanced materials ensures steady consumption growth for catechol manufacturers.

Rising Demand from Agrochemicals Sector

Growing agrochemical innovation significantly supports catechol demand, particularly as a precursor in pesticide and herbicide manufacturing. Catechol derivatives improve crop protection performance and formulation stability, aligning with global food security objectives. The Food and Agriculture Organization (FAO) reports pesticide consumption increased by 2.8% annually from 2021 to 2025, reflecting intensifying agricultural activity worldwide.

Emerging agricultural economies such as India and Brazil recorded around 6% growth in agrochemical consumption in 2024, according to FAO data. Rising population pressure, shrinking arable land, and climate variability are encouraging higher input usage. This environment sustains demand for catechol-based intermediates as formulators prioritize efficiency, durability, and cost-effective crop protection solutions.

Restraints - Stringent Environmental Compliance Requirements

Tightening environmental regulations act as a significant restraint on the catechol market, as the compound is classified as hazardous in several jurisdictions. The U.S. Environmental Protection Agency (EPA) includes catechol under the Toxic Release Inventory (TRI), requiring strict emission monitoring and reporting. EPA 2024 data indicates compliance costs can increase operational expenses by 15–20% for chemical manufacturers.

In Europe, REACH regulations mandate comprehensive toxicity testing and registration procedures before commercialization. These requirements raise approval timelines and capital expenditure, particularly for new entrants. As a result, investment in additional production facilities slows, especially in cost-sensitive developing regions, constraining supply-side expansion and limiting overall market scalability.

High Production Costs and Feedstock Volatility

High raw material and energy costs present another major challenge for catechol producers. Catechol is primarily derived from phenol or benzene, both of which experienced price increases of approximately 12% in 2024, according to the American Chemistry Council (ACC). Such volatility directly compresses manufacturer margins and complicates long-term pricing strategies.

Additionally, catechol production involves energy-intensive processing steps. The International Energy Agency (IEA) projects chemical sector energy costs to rise by nearly 5% through 2030. Smaller and mid-sized manufacturers are particularly vulnerable to these fluctuations, potentially reducing competitive intensity and limiting innovation within the global catechol market.

Opportunity - Advancements in Bio-Based Production Technologies

The transition toward sustainable, bio-based catechol production presents a strong growth opportunity, particularly among environmentally conscious pharmaceutical and food manufacturers. A 2024 Nature Biotechnology study led by U.S. Department of Energy (DOE) researchers demonstrated that enzymatic production from glucose using engineered microbes can reduce carbon emissions by nearly 70% compared to conventional routes.

Supportive policy frameworks further accelerate commercialization. The EU Green Deal has allocated nearly €1 billion for bio-chemical innovation through 2030, encouraging industrial-scale adoption. Additionally, the polymers segment, projected to grow at 5.1% CAGR (2025–2032), benefits from bio-catechol integration into bioplastics, with Japan’s METI reporting pilot-scale production advancements in 2025.

Expanding Demand Across Emerging Economies

Rapid industrialization in Asia Pacific creates substantial demand opportunities for catechol across agrochemicals and specialty chemical applications. The region represents the fastest-growing end-use market, expanding at a projected 4.8% CAGR (2026–2033). China’s 14th Five-Year Plan prioritizes chemical self-sufficiency, encouraging domestic intermediate production, as outlined by the National Development and Reform Commission (NDRC).

India also presents strong growth potential, with pharmaceutical exports reaching US$ 27 billion in 2024, according to the Pharmaceuticals Export Promotion Council of India. Rising output increases demand for intermediates and chelating agents. Manufacturers can leverage this momentum through strategic capacity expansions, joint ventures, and technology transfers in high-growth regional markets.

Category-wise Analysis

Form Insights

Flakes (solid form) lead the catechol market, holding a 65% share in 2025 due to advantages in handling, storage, and transportation. Solid flakes reduce leakage risks compared to liquid forms and comply with International Maritime Dangerous Goods (IMDG) standards for safer shipping. CEFIC data indicates that around 70% of industrial chemicals are transported as solids to enhance stability and cut costs by 10–15%. In pharmaceutical and polymer applications, flakes allow precise dosing, with ICCA surveys showing 80% of formulators prefer them, reinforcing their market dominance.

Meanwhile, liquid catechol is emerging as the fastest-growing form segment, driven by ease of use in automated processes and inline reactors. Its adoption is rising in continuous manufacturing and specialty chemical production, where rapid solubility and seamless integration into formulations improve operational efficiency and reduce handling time.

Application Insights

Intermediates dominate the catechol market, capturing 32% share in 2025, largely due to their extensive use in pharmaceuticals and agrochemical synthesis. Catechol is converted into compounds such as guaiacol and veratrole, essential for antibiotics and herbicides. U.S. International Trade Commission (USITC) reports that intermediates accounted for 45% of fine chemical output in 2024, highlighting their significance in high-volume chemical manufacturing. Its chemical stability provides an advantage over alternative intermediates, maintaining leadership in polymer and agrochemical applications.

Specialty chemicals represent the fastest-growing application segment, fueled by rising demand in flavors, fragrances, antioxidants, and chelating agents. Increasing interest in high-purity and bio-based formulations, particularly for pharmaceutical and food-grade products, drives this segment’s rapid adoption across emerging and developed markets.

Industry Insights

Polymers are the leading end-use sector for catechol, accounting for 38% of the market in 2025. Catechol is critical in polyurethane and resin production, improving flexibility, adhesion, and durability in coatings and composites. According to ACC, U.S. polymer production grew 4.5% in 2024, with automotive and construction sectors consuming 60% of output per ISO standards. Recycling initiatives further strengthen Catechol’s position in polymer applications.

Agrochemicals are the fastest-growing industry, supported by the rising need for pesticides, herbicides, and crop protection solutions. Expanding agricultural activities in Asia Pacific, coupled with innovations in eco-friendly and high-performance agrochemical formulations, are driving demand for catechol intermediates in this sector.

Regional Insights

North America Catechol Market Trends and Insights

North America, led by the U.S., benefits from a strong innovation ecosystem and strict regulatory standards. The EPA’s TSCA framework ensures a high-purity catechol supply for pharmaceutical applications, accelerating L-DOPA and antioxidant production. DOE-funded bio-catechol initiatives in 2024 reduced imports by 8%, supporting local manufacturing. NIST reports a 15% rise in R&D investment in fine chemicals, while pharmaceutical employment grew 3.2% in 2025, sustaining industrial demand.

The region is projected to grow at a CAGR of 4.0% from 2025 to 2032, driven by continued investments in sustainable processes, high-value pharmaceutical intermediates, and advanced polymer production. Innovation partnerships, bio-based adoption, and regulatory compliance collectively strengthen North America’s position in the global catechol market.

Europe Catechol Market Trends and Insights

Europe leads the global catechol market with a 38% share in 2025, driven by harmonized regulations under REACH and ECHA. Germany’s chemical output grew 2.9% in 2024, supported by polymer exports, while the U.K.’s Chemicals Strategy emphasizes sustainable sourcing. France maintains leadership in fragrance applications, and Spain’s agrochemical sector expanded 4% per Eurostat, benefiting from regulatory alignment and eased cross-border trade.

Regulatory stability and advanced industrial infrastructure foster high-quality catechol production, particularly for pharmaceuticals, polymers, and specialty chemicals. Ongoing investments in green chemistry and sustainable intermediates further enhance Europe’s market dominance, while strong intra-regional trade ensures continued volume growth across key industries.

Asia Pacific Catechol Market Trends and Insights

Asia Pacific holds a 32% share of the global catechol market in 2025 and is the fastest-growing region, expanding at a CAGR of 5.2% (2025–2032). Growth is fueled by rapid industrialization and the rise of chemical manufacturing hubs in China, Japan, India, and ASEAN countries. China added 6% chemical production capacity in 2025, leveraging low-cost intermediates for domestic and export markets.

Japan advances bio-based catechol production through METI-led initiatives, while India’s pharmaceutical exports reached US$ 28 billion in 2025, driving higher intermediate demand. ASEAN countries benefit from increased foreign direct investment, supporting a 5.3% market growth. Strong expansion in agrochemicals, polymers, and specialty chemicals underpins sustained regional adoption of catechol.

Competitive Landscape

The global catechol market is highly consolidated, with leading players dominating through integrated supply chains and robust production capabilities. Companies focus on enhancing product differentiation by offering high-purity catechol (>99%) and meeting sustainability certifications, catering to pharmaceutical, polymer, and specialty chemical applications. Strategic investments in research and development drive innovation, particularly in bio-based production routes, enabling firms to reduce environmental impact and appeal to eco-conscious end-users.

Emerging business models emphasize circular economy initiatives, such as recycling phenol and other chemical waste streams to produce catechol efficiently. Partnerships, technology collaborations, and sustainable production practices are increasingly shaping competitive dynamics, allowing manufacturers to maintain cost advantages while supporting regulatory compliance and long-term market growth.

Key Developments:

- In March 2024, Ineos Phenol expanded catechol production capacity in Germany by 20% to address growing demand from the polymer sector, enhancing supply reliability and supporting regional industrial growth.

- In July 2025, Mitsui Chemicals launched a bio-catechol pilot using sugarcane as feedstock, targeting compliance with EU green standards and promoting sustainable production for pharmaceutical and polymer applications.

- In November 2024, Ube Industries partnered with an Indian firm to supply catechol intermediates for agrochemical formulations, strengthening regional market presence and supporting increasing demand in crop protection and specialty chemical segments.

Companies Covered in Catechol Market

- Solvay S.A.

- UBE Industries Ltd.

- Camlin Fine Sciences Ltd.

- Jiangsu Sanjili Chemical Co., Ltd.

- Tokyo Chemical Industry Co., Ltd. (TCI)

- Merck KGaA (Sigma-Aldrich)

- Thermo Fisher Scientific (Alfa Aesar)

- Biosynth Carbosynth

- Loba Chemie Pvt. Ltd.

- Sisco Research Laboratories Pvt. Ltd.

- Central Drug House (P) Ltd.

- Haihang Industry Co., Ltd.

- Sinochem Nanjing Corporation

- Muby Chemicals

- Zhejiang Glary Chemicals Co., Ltd.

Frequently Asked Questions

The global Catechol market is expected to reach US$ 158.4 million in 2026, growing from historical levels due to polymer and pharmaceutical demand.

Expanding polymers and pharmaceuticals applications drive demand, with ICCA reporting 5.2% annual growth in pharmaceutical chemicals.

Europe leads with 38% share in 2025, backed by REACH regulations and strong chemical infrastructure in Germany, France, and the U.K.

Bio-based production innovations offer potential, reducing emissions by 70% and aligning with EU Green Deal funding for sustainable chemicals.

Leading players include Ineos Phenol, Mitsui Chemicals, Ube Industries, and BASF SE, focusing on capacity expansions and bio-routes.