- Oil & Gas

- North America Oil Storage Market

North America Oil Storage Market Size, Share, and Growth Forecast 2026 – 2033

North America Oil Storage Market by Tank Type (Fixed Roof, Floating Roof, Underground), Product (Crude Oil, Gasoline, Middle Distillates, Aviation Fuel), Industry (Refining, Petrochemical, Transportation, Other), and Regional Analysis for 2026–2033

North America Oil Storage Market Size and Trend Analysis

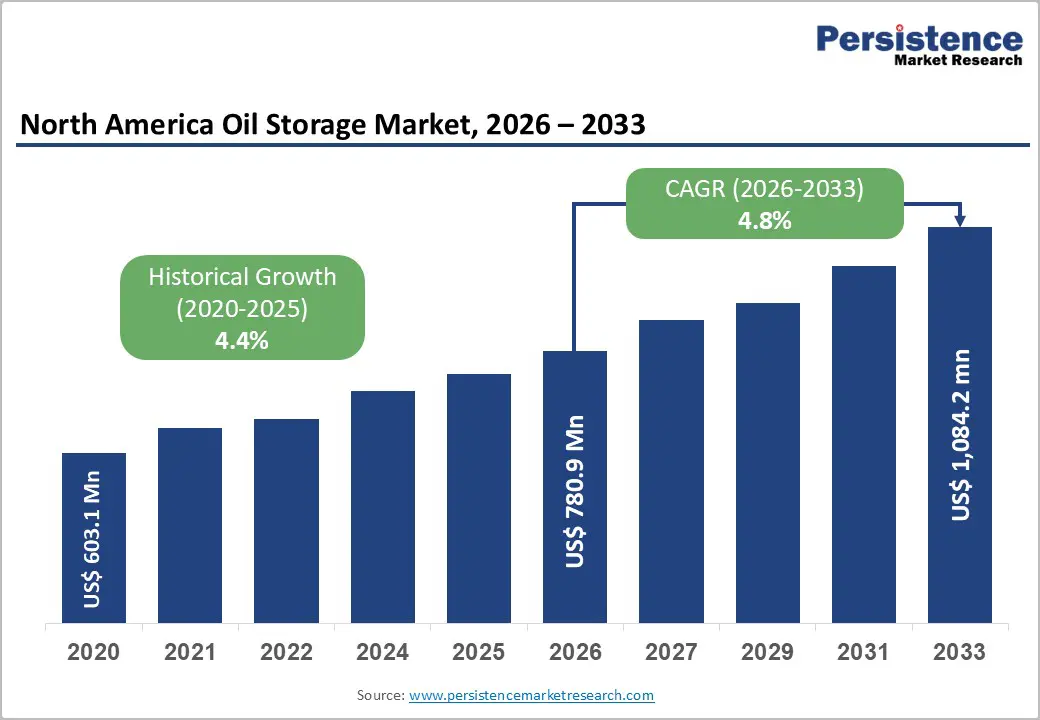

The North America oil storage market is valued at US$ 780.6 million in 2026 and is projected to reach US$ 1,084.2 million by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

The market's robust expansion is primarily driven by record-breaking U.S. crude oil production and a strategic imperative to fortify energy security reserves. According to the U.S. Energy Information Administration (EIA), domestic crude output reached an annual record of 13.6 million barrels per day (bpd) in 2025, creating substantial and sustained demand for interim and buffer storage. Concurrently, the U.S. Department of Energy (DOE) has pursued aggressive Strategic Petroleum Reserve (SPR) replenishment programs, procuring over 200 million barrels of crude oil since 2022, reinforcing infrastructure investment across the region.

Key Industry Highlights:

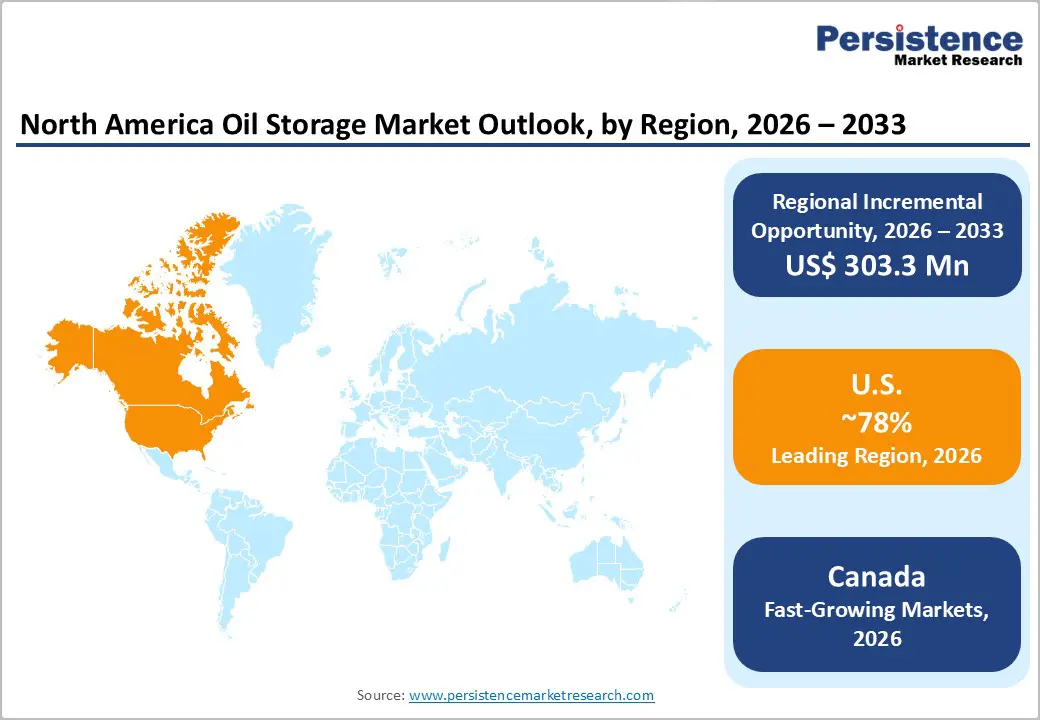

- Leading Country: The United States leads the North America oil storage market, with more than 78% share in 2026, driven by record crude output of 13.6 million bpd in 2025, a 714-million-barrel SPR authorized capacity, and the world's most extensive commercial terminal network.

- Fast-Growing Market: Canada is the fast-growing market supported by oil sands expansion, Trans Mountain Pipeline commissioning, and growing Asia Pacific export ambitions.

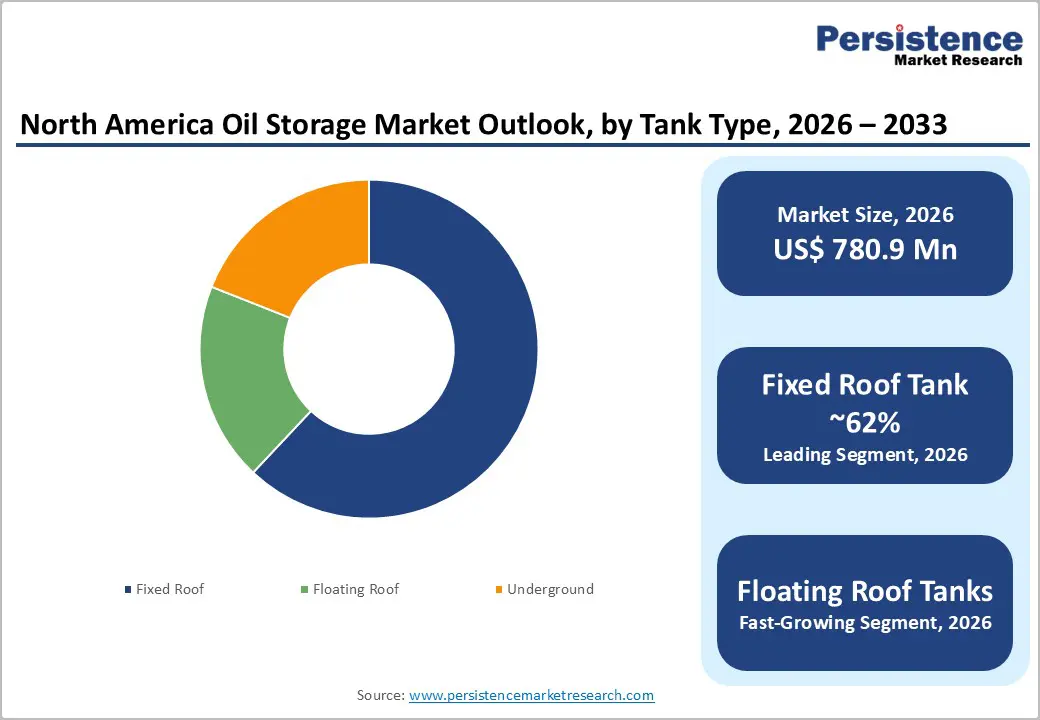

- Dominant Tank Type Segment: Fixed roof tanks dominate the tank type category with approximately 62% market share, favored for cost-effectiveness and compatibility with crude oil and low-volatility refined product storage at inland and refinery-adjacent terminals.

- Fastest Growing Segment: Floating roof tanks represent the fast-growing tank type propelled by EPA emission compliance mandates and expanding crude oil export terminal infrastructure along the U.S. Gulf Coast.

- Key Opportunity: The proliferation of IoT and AI-powered automated inventory management systems offers high-value differentiation for storage operators, enabling premium pricing, improved ESG credentials, and superior feedstock optimization for refinery and petrochemical clients.

DRO Analysis

Drivers - Surging Domestic Crude Oil Production Amplifying Storage Demand

Record-high U.S. crude oil production has emerged as the primary driver of storage demand in North America. According to the EIA's Short-Term Energy Outlook, U.S. crude output averaged 13.6 million barrels per day (bpd) in 2025, marking the highest annual figure ever recorded. Within this context, the Permian Basin alone contributed an average of 6.6 million bpd in 2025. Such production levels consistently exceed real-time refining and consumption rates, necessitating the leasing or expansion of tank capacity by producers and midstream operators.

The Port of Corpus Christi also reported remarkable crude oil exports, exceeding 2.3 million bpd in the first quarter of 2025. In response to this increased demand, private operators have added over 10 million barrels of new near-dock terminal capacity since early 2024. Furthermore, pipeline bottlenecks have intensified this situation, as localized storage hubs in West Texas experienced nearly 90% utilization in early 2025 due to infrastructure constraints.

Government-Led Strategic Reserve Policies Stimulating Infrastructure Investment

Active federal policy serves as a significant secondary growth driver for the North America Oil Storage Market. The U.S. Department of Energy has secured contracts for the acquisition of over 200 million barrels of crude oil to replenish the Strategic Petroleum Reserve (SPR) following emergency drawdowns that occurred between 2022 and 2023. The SPR has an authorized storage capacity of 714 million barrels, which is stored in underground salt caverns located in Texas and Louisiana. According to the Congressional Research Service (CRS), the Secretary of Energy has pursued funding of approximately $20 billion to further refill the reserve, thereby sustaining a multi-year procurement and storage infrastructure initiative.

The Canadian Association of Petroleum Producers (CAPP) has projected that national crude oil output will approach 5.5 million barrels per day by 2025. This anticipated increase underscores the necessity for additional commercial storage capacity throughout Alberta and its export corridors.

Restraints - Volatile Oil Prices Constraining Capital Expenditure for Storage Expansion

Fluctuating crude oil prices represent a persistent headwind for long-term storage investment decisions. West Texas Intermediate (WTI) prices averaged US$ 77/barrel in 2024 before declining to approximately US$ 65/barrel in 2025, according to EIA data. Lower price environments reduce the contango incentive that encourages merchants and producers to build or lease storage. When forward prices fail to cover storage costs plus financing, operators scale back expansion plans. The reduction in active drilling rigs, 5% fewer rigs in 2025 versus 2024 per EIA, reflects this dampening effect, directly constraining throughput volumes and weakening near-term utilization rates at commercial terminals.

Stringent Environmental Regulations and High Compliance Costs

Escalating regulatory requirements from the U.S. Environmental Protection Agency (EPA) and equivalent bodies under Canada's Impact Assessment Act impose significant compliance expenditures on storage operators. Volatile Organic Compound (VOC) emission standards, secondary containment mandates, and spill-prevention plans require continuous upgrades to aging tank infrastructure. These obligations particularly affect operators of older fixed-roof tank fleets, which constitute a substantial portion of existing capacity. Compliance retrofitting can add 15–25% to project capital costs for brownfield expansions, reducing return on investment. Small and mid-size operators face disproportionate cost burdens, leading to market exits or asset divestiture to larger players, thereby moderating the pace of overall capacity expansion.

Opportunities – Adoption of Floating Roof Tank Driven by Emission Reduction Mandates

The transition from fixed-roof to floating-roof tank systems represents a significant commercial opportunity for tank manufacturers, engineering firms, and operators. Floating roof tanks minimize evaporative losses by maintaining a roof that rests directly on the stored liquid surface, substantially reducing VOC emissions and fire risk. Advancements in seal technologies and high-performance materials have further improved operational efficiency and regulatory compliance. Tightening EPA emission thresholds for storage facilities is expected to accelerate retrofits and new installations, creating a sustained procurement cycle for floating roof solutions across the U.S. Gulf Coast and inland terminal hubs.

Digital Technologies and Automated Inventory Management: Modernizing Storage Operations

The integration of Internet of Things (IoT)-enabled sensors, Artificial Intelligence (AI)-driven inventory management, and automated tank gauging systems presents a high-value opportunity for technology providers and storage operators alike. Digital monitoring reduces overfill incidents, optimizes throughput scheduling, and lowers labor costs. Major producers in the Permian Basin have already deployed AI and electronic hydraulic fracturing technology, with direct downstream benefits for linked storage facilities per EIA analysis.

Companies that invest in real-time inventory optimization platforms can offer differentiated, premium-priced services, particularly to refinery and petrochemical customers who require precise just-in-time feedstock logistics. As North American midstream operators face increasing pressure to demonstrate ESG compliance, digitally monitored, low-emission storage infrastructure is positioned to attract both commercial clients and institutional capital.

Category-wise Analysis

Tank Type Insights

Fixed roof tanks constitute the dominant segment within the Tank Type category, accounting for approximately 62% of the North America oil storage market in 2026. Their leadership is underpinned by cost-effectiveness, structural durability, and compatibility with a wide range of products, including crude oil, heavy fuel oil, and refined distillates.

The U.S. alone hosts over 18,000 fixed-roof tanks with a combined capacity exceeding 420 million barrels. These tanks are particularly prevalent at inland terminals and refinery gate facilities where low-volatility products are stored, and operational simplicity is prioritized. Fixed roof tanks remain integral to SPR infrastructure, which holds ~394 million barrels in underground salt caverns and above-ground configurations.

Product Insights

Crude oil is the leading product segment, accounting for approximately 35% of the North America Oil Storage Market share, and serves as the primary driver for the entire storage ecosystem. The combined U.S. and Canadian production of over 18 million bpd of crude oil, greater than any other country globally per EIA, necessitates extensive buffer storage at wellhead, pipeline hub, and export terminal levels.

Seasonal refinery maintenance windows and periodic outages spike utilization: during Gulf Coast refinery outages in March 2025, regional storage utilization surged approximately 11% within two weeks, per EIA data. Crude's dominance also reflects the strategic stockpiling function of the SPR, which exclusively stores crude oil.

Industry Insights

The refining segment holds the leading share within the Industry category, accounting for approximately 40% of the North America oil storage market. Refineries require continuous upstream crude feedstock storage to buffer against supply interruptions and maintain stable distillation unit operations at optimal utilization rates. The U.S.A. is home to some of the world's largest refining complexes, particularly along the Gulf Coast and in Texas, where refinery utilization surged to over 93% ahead of the summer driving season in 2025, per EIA data.

Storage tanks at and adjacent to refineries serve as both receiving and finished-product dispatch points, making them integral to refinery supply chain continuity. Petrochemical end-use is emerging as the fastest-growing sub-segment, driven by expanding feedstock demand.

Regional Analysis

U.S. (United States) Market Trends & Analysis

The United States dominates the North America oil storage market, accounting for more than 78% of the regional capacity and revenue. Underpinned by record crude output averaging 13.6 million bpd in 2025 per EIA, the country's storage infrastructure spans onshore tank farms, underground salt cavern reserves, and coastal export terminals. The SPR, the world's largest emergency crude reserve, holds approximately 394 million barrels as of end-2024 in caverns across Texas and Louisiana per CRS analysis. The Cushing, Oklahoma hub, the WTI futures delivery point, fell below 20 million barrels in early 2025, creating structural tightness and price sensitivity in benchmark crude markets.

Recent geopolitical developments have amplified U.S. storage dynamics. Escalating U.S.-Iran tensions and Middle East supply disruptions, which the EIA's May 2026 STEO estimates caused collective shut-ins of approximately 9.1 million bpd from Iraq, Saudi Arabia, Kuwait, UAE, Qatar, and Bahrain in April 2026, have elevated Brent crude prices toward US$ 115/barrel in Q2 2026. This spike has incentivized commercial operators to maximize U.S. storage utilization for contango plays and energy security buffering, supporting near-term demand.

The Trump administration's broad tariff regime has simultaneously created supply chain uncertainty in petroleum equipment imports, modestly increasing capital costs for new tank construction, particularly for large-diameter steel tanks.

Canada Market Trends, Drivers & Insights

Canada represents the fastest-growing country segment within the North America Oil Storage Market, registering an estimated CAGR of 6.3% during the forecast period. The country's oil production, predominantly oil sands and conventional crude from Alberta, was projected to approach 5.5 million bpd by 2025 per CAPP. The commissioning of the Trans Mountain Pipeline Expansion (TMX) in May 2024 marked a pivotal infrastructure development, tripling export capacity from 300,000 to 890,000 bpd toward British Columbia coastal terminals and new Asia Pacific export markets, creating incremental demand for upstream buffer storage in Alberta.

Despite progress, Canada faces pipeline bottleneck challenges, with Alberta production periodically exceeding takeaway capacity. U.S. tariffs on Canadian crude, periodically imposed or threatened under the Trump administration's trade policy, have added price risk for cross-border crude flows, occasionally incentivizing producers to stockpile domestically rather than export at unfavorable netbacks. This has created episodic demand surges for Alberta storage capacity. Total Canadian petroleum stocks were approximately 190.9 million barrels at the end of 2024, reflecting steady drawdown trends amid rising exports.

Competitive Landscape

The North America oil storage market is moderately consolidated, with a handful of large-scale midstream and terminal operators, including Kinder Morgan, Royal Vopak, Magellan Midstream Partners, and NuStar Energy, commanding significant market share through extensive terminal networks and long-term take-or-pay contracts. The market is also witnessing consolidation, with larger players acquiring regional operators to expand reach. Emerging business model trends include fee-based revenue contracts, renewable feedstock co-location, and digital terminal management platforms that optimize throughput and reduce operating expenditure.

Key Developments

- January 2026: CST Industries announced that DXP Enterprises, Inc. has acquired Mid Atlantic Storage Systems, Inc. (MASSI), a key dealer and provider of liquid storage tank solutions, strengthening capabilities in the oil storage and broader fluid handling market.

- March 2026: Phillips 66 and Kinder Morgan announced the extension of the second open season for their proposed Western Gateway Pipeline, aimed at securing remaining transportation capacity commitments.

- September 2023: ONEOK, Inc. announced the completion of the acquisition of Magellan Midstream Partners, L.P. (Magellan), creating a more diversified North American midstream infrastructure company focused on delivering essential energy products and services to its customers and continuing strong returns to investors.

Top Companies in North America Oil Storage Market

Kinder Morgan, Inc. (Houston, U.S.) is the largest independent terminal operator in North America, operating approximately 139 terminals with a combined liquids storage capacity of approximately 141 million barrels. The company transports about 40% of U.S.-consumed natural gas and moves approximately 2.4 million barrels per day of petroleum products. For full-year 2025, Kinder Morgan projected Adjusted EBITDA of US$ 8.3 billion, a 4% increase from 2024, underpinned by fee-based terminal and pipeline revenues.

Royal Vopak N.V. (Rotterdam, Netherlands) is the world's largest independent liquid bulk storage service provider, operating over 85 terminals with combined capacity exceeding 30 million cubic meters (190 million barrels) globally. In North America, the company operates strategic terminals including its Galena Park and Deer Park facilities along the Houston Ship Channel. Its €2 billion terminal investment program and dedicated energy transition fund position it as a premium storage partner for both conventional hydrocarbons and emerging low-carbon fuels.

Magellan Midstream Partners, L.P. (Tulsa, U.S.) owns the longest refined petroleum products pipeline system in the United States, with access to over 40% of the nation's refining capacity. The company can store over 80 million barrels (13 million cubic meters) of petroleum products spanning gasoline, diesel, and crude oil. Its deep integration with pipeline networks and refinery gate terminals across the Gulf Coast and Midwest provides a structural advantage in throughput capture and long-term customer retention.

Global North America Oil Storage Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 603.1 Mn |

|

Current Market Value (2026) |

US$ 780.6 Mn |

|

Projected Market Value (2033) |

US$ 1,084.2 Mn |

|

CAGR (2026–2033) |

4.8% |

|

Leading Region |

United States, ~78% share |

|

Dominant Segment |

Fixed Roof (Tank Type), ~62% share |

|

Top-ranking Segment |

Crude Oil (Product), ~35% share |

|

Incremental Opportunity |

US$ 303.6 Mn (2026–2033) |

Companies Covered in North America Oil Storage Market

- CST Industries

- Kinder Morgan

- Magellan Midstream Partners

- Fisher Tank

- NOV

- ZCL Composites

- Royal Vopak

- Superior Tank

- NuStar Energy

- Shawcor Ltd.

Frequently Asked Questions

The North America Oil Storage Market is valued at US$ 780.6 Mn in 2026 and is projected to reach US$ 1,084.2 Mn by 2033, growing at a CAGR of 4.8% during 2026–2033, driven by record U.S. crude oil production and sustained government strategic reserve programs.

The market is primarily driven by record-high U.S. crude oil production of 13.6 million bpd in 2025 per EIA data, increasing crude export volumes through Gulf Coast terminals, active U.S. DOE Strategic Petroleum Reserve replenishment exceeding 200 million barrels, and growing Canadian oil sands output approaching 5.5 million bpd.

Fixed Roof Tanks lead the Tank Type category with approximately 62% market share, owing to their structural durability, cost-effectiveness, and versatility for storing crude oil and low-volatility refined products. The U.S. alone operates over 18,000 fixed-roof tanks with a capacity exceeding 420 million barrels, making them the backbone of national petroleum storage infrastructure.

The United States is the leading region, accounting for approximately 78% of the North America Oil Storage Market. Its dominance reflects the world's largest crude oil production volumes, the SPR with 714 million barrels of authorized capacity, and a vast network of pipeline-connected commercial terminals concentrated along the Gulf Coast and in Cushing, Oklahoma.

The fastest-growing opportunity lies in Floating Roof Tank adoption, expanding at a CAGR of 7.6%, driven by tightening EPA VOC emission regulations and demand for environmentally compliant storage solutions. The parallel adoption of IoT and AI-powered automated inventory management systems offers operators the ability to monetize premium digital services while improving ESG credentials and feedstock optimization efficiency.

The key players include Kinder Morgan, Inc., Royal Vopak N.V., Magellan Midstream Partners, L.P., NuStar Energy L.P., CST Industries, Inc., Fisher Tank Company, NOV Inc., ZCL Composites, Superior Tank Co., Inc., and Shawcor Ltd.