- Automotive Components & Materials

- Gasoline Particulate Filter Market

Gasoline Particulate Filter Market Size, Share, and Growth Forecast 2026 - 2033

Gasoline Particulate Filter Market by Filter Type (Ceramic, Cordierite, Silicon Carbide), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles), Sales Channel (OEM, Aftermarket), and Regional Analysis, 2026 - 2033

Gasoline Particulate Filter Market Size and Trend Analysis

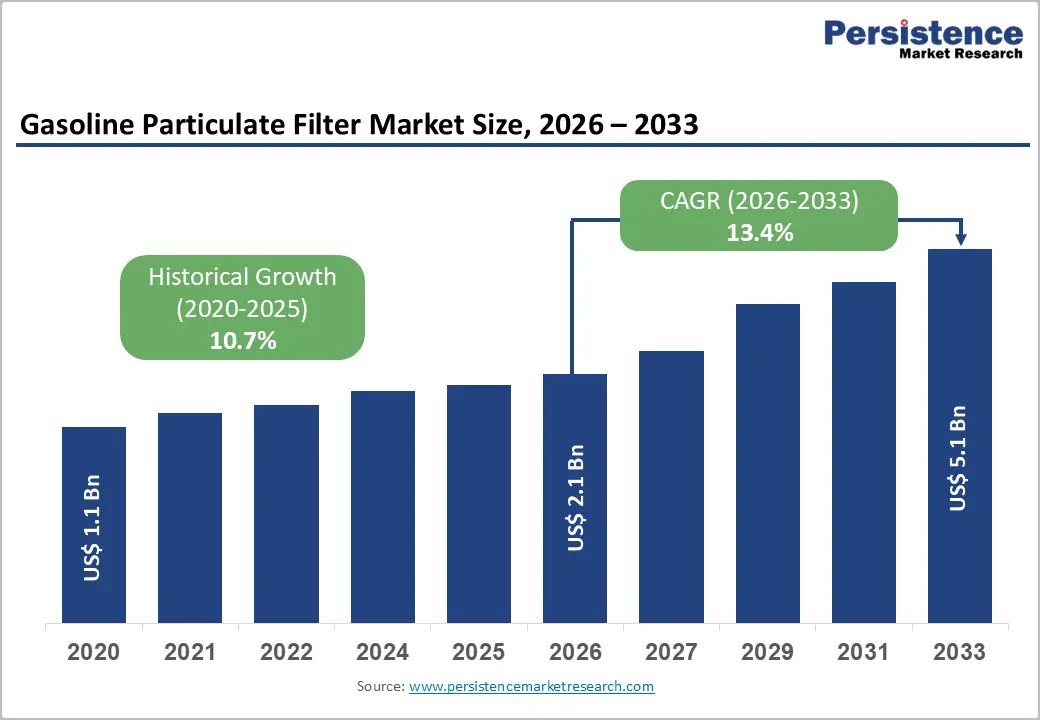

The global gasoline particulate filter market is expected to be valued at US$ 2.1 billion in 2026 and to reach US$ 5.1 billion by 2033, growing at a CAGR of 13.4% over 2026 - 2033. Strong regulatory pressure on particulate number (PN) emissions from gasoline direct-injection (GDI) engines in Europe, China, India, and North America is making gasoline particulate filters (GPFs) a standard exhaust aftertreatment component in new light-duty vehicles.

This growth is further supported by the rising share of GDI and hybrid gasoline vehicles, which produce higher fine particulate emissions than port-fuel-injected engines and therefore require efficient filtration to meet Euro 6/6d, emerging Euro 7, China 6/7, and future BS7 norms. In parallel, leading suppliers such as Corning, NGK Insulators, Tenneco, Faurecia (FORVIA), and Johnson Matthey continue to invest in high-porosity ceramic substrates and advanced catalyst coatings, improving filtration efficiency and pressure-drop performance and reinforcing long-term adoption of GPF technology.

Key Industry Highlights

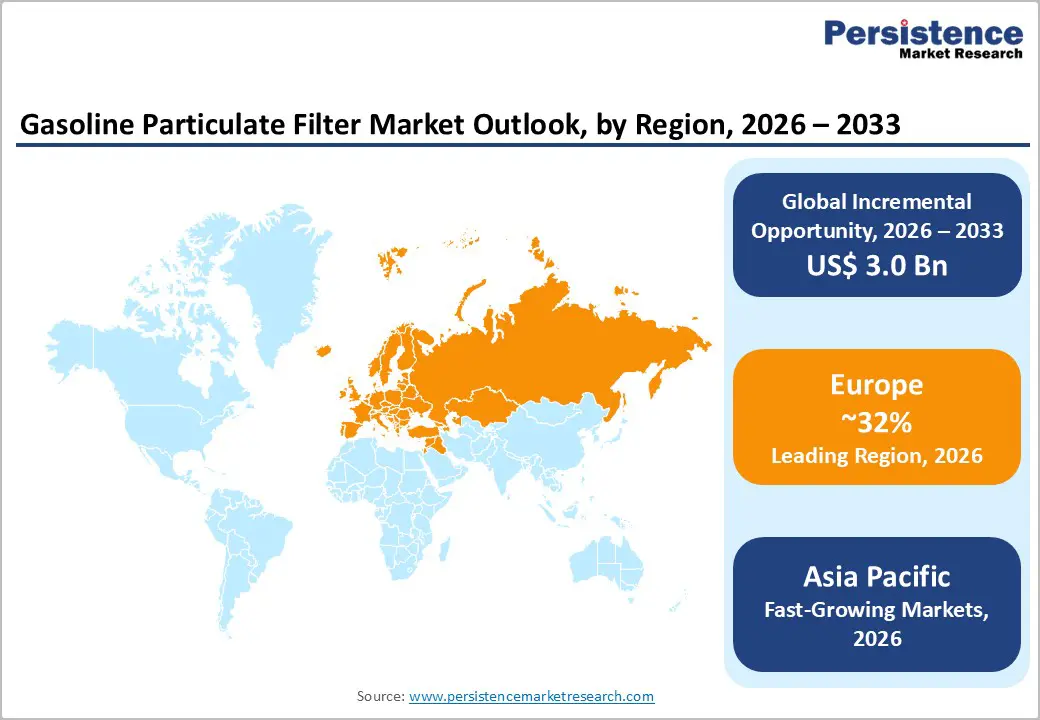

- Leading region: Europe remains the leading gasoline particulate filter market, supported by early adoption of PN-based limits, comprehensive Euro 6/6d and forthcoming Euro 7 regulations, and a dense concentration of global OEMs and Tier-1 exhaust system suppliers.

- Fastest-growing region: Asia Pacific is projected to record the fastest growth through 2033, driven by China 6, BS VI, and future Indian standards, expanding hybrid and GDI penetration, and strong local manufacturing ecosystems in China, India, Japan, and ASEAN economies.

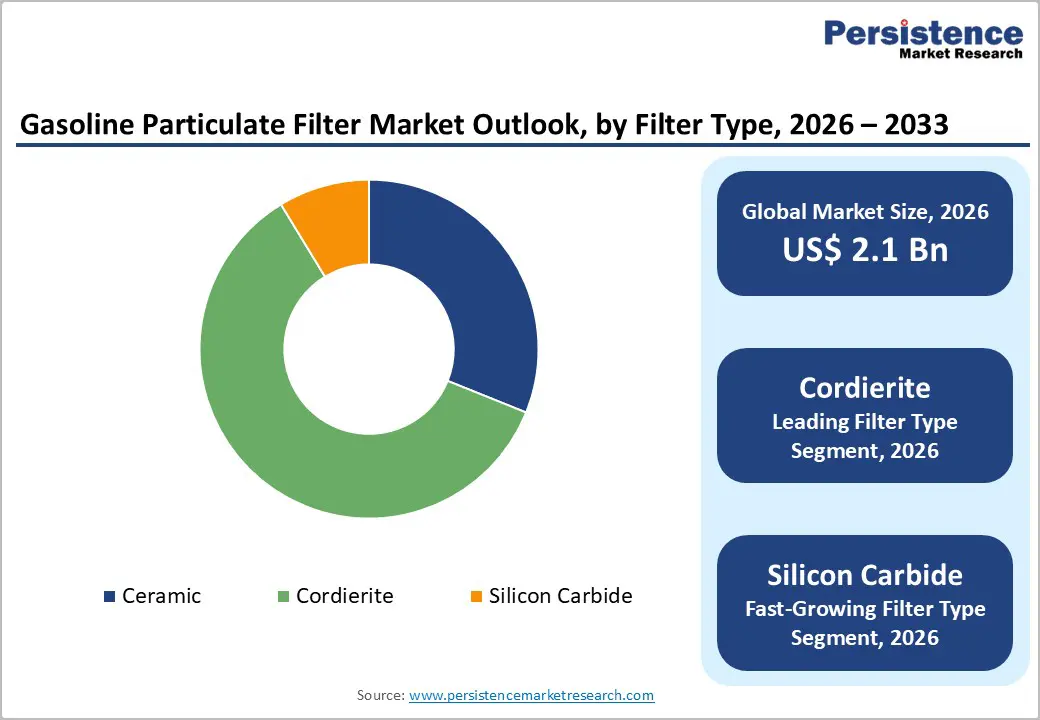

- Dominant segment: Cordierite ceramic gasoline particulate filters hold the dominant share of installations due to their cost-effectiveness, proven durability, and high porosity, making them the preferred choice for mass-market passenger car platforms worldwide.

- Fastest-growing segment: Silicon carbide-based GPFs and technologically advanced high-porosity catalyzed filters are expected to grow fastest, as OEMs seek robust thermal resistance and low pressure drop for high-performance, hybrid, and demanding real-driving-emissions applications.

- Key market opportunity: The combination of tightening Euro 7/CN7/BS7-style norms, expansion of low-emission zones, and the aging of the first GPF-equipped vehicle cohorts creates attractive opportunities in premium OEM systems, aftermarket replacement, and remanufactured gasoline particulate filters.

| Key Insights | Details |

|---|---|

| Gasoline Particulate Filter Market Size (2026E) | US$ 2.1 billion |

| Market Value Forecast (2033F) | US$ 5.1 billion |

| Projected Growth CAGR (2026 - 2033) | 13.4% |

| Historical Market Growth (2020 - 2025) | 10.7% |

Market Dynamics

Drivers - Stringent global particulate number regulations for gasoline engines

The most powerful demand driver for gasoline particulate filters is the tightening of particulate number (PN) standards applied to gasoline direct-injection vehicles across major automotive markets. Under Euro 6 and Euro 6d regulations, the European Union introduced a PN limit of 6×10¹¹ particles per kilometer for light-duty vehicles, which has effectively required OEMs to adopt GPFs on most new GDI platforms to comply with real-driving emissions (RDE) and WLTP testing. Similar PN-based standards in China (China 6) and more recent adoption in India under BS VI, along with the anticipated shifts toward Euro 7, CN7, and BS7, further reinforce the need for more efficient filtration down to particle sizes near 10 nanometers. As regulators continue to extend durability requirements and tighten limits over wider operating conditions, automakers increasingly rely on high-performance GPF systems, structurally locking in long-term demand growth for GPF substrates, coatings, and integrated exhaust modules.

Rising penetration of GDI and hybrid gasoline powertrains

A second key driver is the rapid shift in powertrain mix from diesel to gasoline and gasoline-hybrid vehicles, particularly in Europe, China, and other urbanized markets. Over the last decade, many OEMs have replaced small diesel engines with turbocharged gasoline direct-injection units to deliver comparable torque and fuel economy with lower nitrogen-oxide emissions, but this has significantly increased particulate emissions, necessitating GPFs to keep PN within legal thresholds. At the same time, HEV and plug-in hybrid platforms frequently operate their gasoline engines at transient conditions and cold starts, both of which can worsen particulate formation and require robust filtration to maintain compliance over full useful life. As hybrid and advanced gasoline powertrains expand their share of global light-duty vehicle sales, exhaust aftertreatment architectures are being standardized around GPF-plus-three-way-catalyst layouts, structurally expanding the addressable base of the gasoline particulate filter market.

Restraints - Higher system cost and engineering complexity

The addition of a gasoline particulate filter increases exhaust system cost and complexity, which acts as a restraint, particularly in price-sensitive vehicle segments and emerging markets. Ceramic filter substrates, canning, temperature and pressure sensors, and control strategy calibration all add to the bill-of-materials and development expenses, while tighter backpressure constraints require careful optimization to avoid fuel-consumption penalties. For small and entry-level vehicles, these incremental costs can weigh heavily on OEM margins and consumer affordability, creating resistance to rapid GPF penetration when regulatory enforcement is weaker. In addition, in regions where low-sulfur fuels and robust inspection-and-maintenance regimes are not yet universal, OEMs may be cautious about deploying sophisticated GPF systems due to durability and warranty concerns, slowing adoption relative to more developed markets.

Long-term demand risk from electrification

A structural headwind for the gasoline particulate filter market is the accelerating shift toward battery electric vehicles (BEVs), which do not require exhaust aftertreatment systems. Many governments, especially in Europe and parts of Asia, have announced timelines for phasing out new internal-combustion-engine (ICE) passenger cars or tightening fleet average CO2 targets, encouraging OEMs to redirect investment from ICE optimization to electrified platforms. As BEV and fuel-cell electric vehicle volumes grow, the long-term pool of gasoline vehicles that can be equipped with GPFs will eventually plateau and decline, particularly in wealthier urban markets with strong charging infrastructure. While this effect is gradual and offset in the medium term by continued growth in hybrid and plug-in hybrid gasoline vehicles, it does cap the ultimate market size and creates strategic uncertainty for GPF suppliers beyond the 2030s.

Opportunity - Next-generation high-porosity and catalyzed GPF technologies

There is a sizable opportunity in next-generation GPF substrates and coatings that can meet future Euro 7, CN7, and BS7 standards while reducing pressure drop and improving durability. Recent technical work presented in SAE papers demonstrates high-porosity cordierite-based filters and advanced microstructures, such as Corning® DuraTrap® GC HP with proprietary hierarchical pore designs, delivering very high filtration efficiency for catalyzed GPFs without excessive backpressure. Such designs allow engineers to count particles down to around 10 nanometers, expand operating windows, and maintain performance over longer mileage and harsher real-world driving cycles. As regulators require extended useful life compliance, including on-board monitoring of PN emissions, OEMs will prioritize suppliers offering robust, low-pressure-drop substrates and integrated catalyst solutions, creating premium pricing opportunities for technology leaders like Corning, NGK Insulators, Johnson Matthey, and Umicore.

Aftermarket and replacement demand for aging GPF fleets

A second major opportunity lies in the aftermarket and replacement segment as the first generations of GPF-equipped vehicles age and begin to require filter renewal, cleaning, or replacement. Corning has already highlighted cumulative shipments of more than 50 million gasoline particulate filters worldwide, reflecting a large installed base in Europe and China that will progressively move into high-mileage and second-hand ownership phases. Experience from diesel particulate filters shows that frequent short-trip urban driving and poor maintenance can accelerate soot and ash accumulation, pushing consumers toward replacement or remanufactured units as vehicles age. As regulatory inspections become stricter and roadside checks expand, especially in low-emission zones, maintaining functional GPFs will be critical to keeping vehicles legal, supporting a growing business for aftermarket suppliers, remanufacturers, and service networks offering validated GPF cleaning and replacement solutions.

Category-wise Analysis

Filter Type Insights

Within filter types, cordierite-based ceramic GPFs are expected to account for the largest share of the gasoline particulate filter market by 2025, with an estimated share of around 60% of total installations. This dominance reflects cordierite’s favorable cost-to-performance balance, low thermal expansion, and well-understood manufacturability, building on decades of use in diesel particulate filters and three-way-catalyst substrates. Suppliers such as Corning have commercialized patented cordierite compositions optimized for GPF duty, combining high porosity and engineered microstructures that provide efficient filtration of fine particulates while maintaining acceptable exhaust backpressure. Although silicon carbide (SiC) offers superior high-temperature resistance and regeneration robustness, its higher material and processing costs limit its use primarily to premium or severe-duty applications, leaving cost-effective cordierite as the default choice for mass-market passenger cars and many light commercial vehicles.

Vehicle Type Analysis

By vehicle type, passenger cars are expected to remain the leading segment in the gasoline particulate filter market, contributing an estimated around 70-75% of GPF demand in 2025. Light-duty passenger cars represent the bulk of global gasoline vehicle production, and the rapid adoption of turbocharged gasoline direct-injection engines in compact and mid-size segments has necessitated widespread GPF integration to meet PN standards. In Europe, passenger cars make up roughly three-quarters of overall vehicle production, and gasoline plus hybrid powertrains account for the majority of new registrations, reinforcing the central role of GPFs on these platforms. Passenger cars are also the primary focus of low-emission zones and city-level air-quality policies, which increasingly target ultrafine particulates, pushing OEMs to apply the most sophisticated filtration and calibration strategies on high-volume passenger models first, ahead of heavier commercial segments.

Sales Channel Insights

Across sales channels, the OEM segment accounts for the overwhelming majority of gasoline particulate filter volumes, with an estimated share of approximately 85-90% of the market in 2025. GPFs are typically integrated into the original exhaust aftertreatment system-often in close-coupled positions combined with three-way catalysts-requiring tight engineering collaboration between OEMs and Tier-1 suppliers such as Tenneco, Faurecia (FORVIA), Katcon, and Bekaert. Because GPFs directly affect combustion calibration, cold-start performance, and on-board diagnostics, retrofitting them in the aftermarket is technically complex and less common, which keeps the center of gravity on factory-installed systems. However, as fleets age and regulatory checks intensify, the aftermarket segment is projected to grow faster than OEM installations from 2026 onward, driven by replacement, cleaning, and remanufacturing opportunities similar to the trajectory observed in diesel particulate filters.

Regional Insights

North America Gasoline Particulate Filter Market Trends and Insights

In North America, the gasoline particulate filter market is underpinned by the United States Environmental Protection Agency (EPA) Tier 3 standards and aligned state-level programs such as California Air Resources Board (CARB) LEV III, which impose tight fleet average limits on both particulate mass and number for light-duty gasoline vehicles. As the share of gasoline direct-injection engines in new U.S. vehicles has risen sharply over the last decade, OEMs have increasingly turned to GPFs to ensure compliance under stringent certification and in-use testing regimes, especially for turbocharged and high-output models. North America is thus expected to account for a significant minority share of global GPF demand by the mid-2020s, supported by a large installed base of gasoline and hybrid vehicles and strong enforcement capacity.

In addition, the region’s robust innovation ecosystem-anchored by research collaborations involving SAE International, leading universities, and major suppliers such as Corning, Tenneco, and Johnson Matthey-is accelerating the development of advanced high-porosity substrates and catalyzed GPF solutions tailored to U.S. drive cycles and durability expectations. As federal and state authorities continue to tighten greenhouse-gas and criteria-pollutant standards for light-duty vehicles, including extended useful life and on-board monitoring provisions, the reliance on efficient GPF systems is expected to deepen, particularly on gasoline-hybrid SUVs and crossovers that dominate new vehicle sales in the region.

Europe Gasoline Particulate Filter Market Trends and Insights

Europe currently represents the leading regional market for gasoline particulate filters, supported by early and aggressive implementation of PN-based emission limits and the widespread adoption of WLTP and RDE testing for light-duty vehicles. Under Euro 6 and Euro 6d, both diesel and gasoline engines are subject to a PN limit of 6×10¹¹ particles per kilometer, and this requirement, combined with real-world conformity factors, has effectively made GPFs standard on most new gasoline direct-injection cars sold across the European Union. Europe accounted for slightly above 30% of global gasoline particulate filter revenues in 2024, reflecting the region’s high regulatory stringency and concentration of leading OEMs and Tier-1 exhaust suppliers.

Looking ahead, the proposed Euro 7 framework is expected to tighten PN limits further, extend them over broader temperature ranges, and include smaller particle sizes and longer durability requirements, reinforcing the critical role of high-performance GPFs in future European powertrain strategies. Suppliers like Corning have already celebrated milestones such as the sale of more than 50 million gasoline particulate filters globally, much of which is linked to European deployments, while FORVIA Faurecia is actively promoting ultra-low-emission exhaust architectures that integrate GPFs with advanced catalysts and electrically heated components for cold-start control. These trends position Europe as both the largest and one of the most technologically advanced regional markets for gasoline particulate filters over the forecast horizon.

Asia Pacific Gasoline Particulate Filter Market Trends and Insights

The Asia Pacific gasoline particulate filter market is expected to be the fastest-growing region between 2026 and 2033, driven primarily by regulatory tightening and surging vehicle production in China, India, Japan, and key ASEAN economies. China 6 emission standards, rolled out in two stages (China 6a and 6b), include stringent PN caps for gasoline vehicles similar to Euro 6, which has spurred rapid deployment of GPFs on domestic and joint-venture passenger car platforms. In India, the introduction of BS VI norms in 2020 and planned progression toward more advanced standards (often aligned conceptually with Euro 7-type limits) are pushing OEMs and suppliers to prepare GPF-equipped gasoline vehicles, especially in urban and premium segments where GDI engines are gaining traction.

Manufacturing advantages also play a central role in regional growth. Asia Pacific hosts major GPF substrate and canning facilities for companies such as Corning, which has expanded its production sites in Shanghai (China) to serve rising local and export demand, and other global players that operate large exhaust component plants across China, India, and South Korea. As vehicle ownership continues to climb and megacities struggle with particulate pollution, policymakers are increasingly prioritizing ultrafine particle control, creating fertile ground for accelerated GPF penetration not only in passenger cars but also in light commercial fleets serving e-commerce and urban logistics. These dynamics position Asia Pacific as the key volume growth engine for the gasoline particulate filter market over the forecast period.

Competitive Landscape

The gasoline particulate filter market is moderately consolidated, dominated by a group of global Tier 1 exhaust system integrators and ceramic substrate specialists, supported by regional coating, canning, and aftermarket participants. High entry barriers stem from stringent emission regulations, OEM qualification requirements, and the need for advanced materials engineering capabilities. Competitive differentiation is largely technology-driven, focusing on substrate innovation, optimized catalyst washcoat formulations, and reduced backpressure designs that maintain engine performance while meeting tightening particulate number limits.

Business strategies emphasize vertical integration across substrate production, coating, and full exhaust module assembly to enhance value capture and ensure compliance with OEM packaging constraints. Capacity expansion in Europe and Asia remains a priority to align with vehicle production hubs and regulatory enforcement timelines. Companies are also investing in next-generation high-porosity, thermally durable filters and expanding aftermarket offerings, including replacement and remanufactured units, to capitalize on the growing installed base of gasoline particulate filter-equipped vehicles worldwide.

Key Developments:

- September, 2024: Cambustion launched an updated particulate filter test system designed for heavy-duty and industrial engines, enabling enhanced quality assurance and performance evaluation of diesel and gasoline particulate filters under full-scale conditions.

Companies Covered in Gasoline Particulate Filter Market

- Tenneco

- Faurecia (FORVIA)

- Bekaert

- Katcon

- Corning

- NGK Insulators

- Alantum Corporation

- CDTi Advanced Materials Inc.

- Johnson Matthey Plc

- Umicore

- Bosal

- Eberspächer

- Denso Corporation

- Marelli

- Faurecia Service

Frequently Asked Questions

The gasoline particulate filter market is expected to reach around US$ 2.1 billion in 2026, supported by tightening PN-based emission regulations and growing penetration of gasoline direct-injection and hybrid powertrains in major automotive markets.

The main demand driver is the global tightening of particulate number limits under frameworks such as Euro 6/6d, emerging Euro 7, China 6/7, and future BS7, which effectively mandate GPF adoption of new gasoline direct-injection vehicles to control ultrafine particle emissions over real-world driving conditions.

Europe currently leads the gasoline particulate filter market, accounting for slightly above 40% of global revenues in 2024, driven by early implementation of PN standards, comprehensive WLTP/RDE testing, and a high concentration of leading OEMs and exhaust aftertreatment suppliers.

A key opportunity lies in advanced high-porosity and catalyzed GPF technologies and in the aftermarket replacement segment, as next-generation regulations and aging GPF-equipped fleets create demand for premium low-pressure-drop substrates, integrated exhaust modules, and remanufactured filters.

Major players include Tenneco, Faurecia (FORVIA), Bekaert, Katcon, Corning, NGK Insulators, Johnson Matthey Plc, Umicore, Alantum Corporation, CDTi Advanced Materials Inc., Bosal, Eberspächer, Denso, and Marelli, alongside specialized aftermarket providers such as Faurecia Service.