- Healthcare Services

- North America Ambulance Service Market

North America Ambulance Service Market Size, Share, Trends, Growth, and Regional Forecast, 2026 to 2033

North America Ambulance Service Market by Transport (Ground Ambulance Services, Air Ambulance Services), Service Type (Emergency Services, Non-Emergency Services), Equipment, and Regional Analysis from 2026 to 2033

North America Ambulance Service Market Share and Trends Analysis

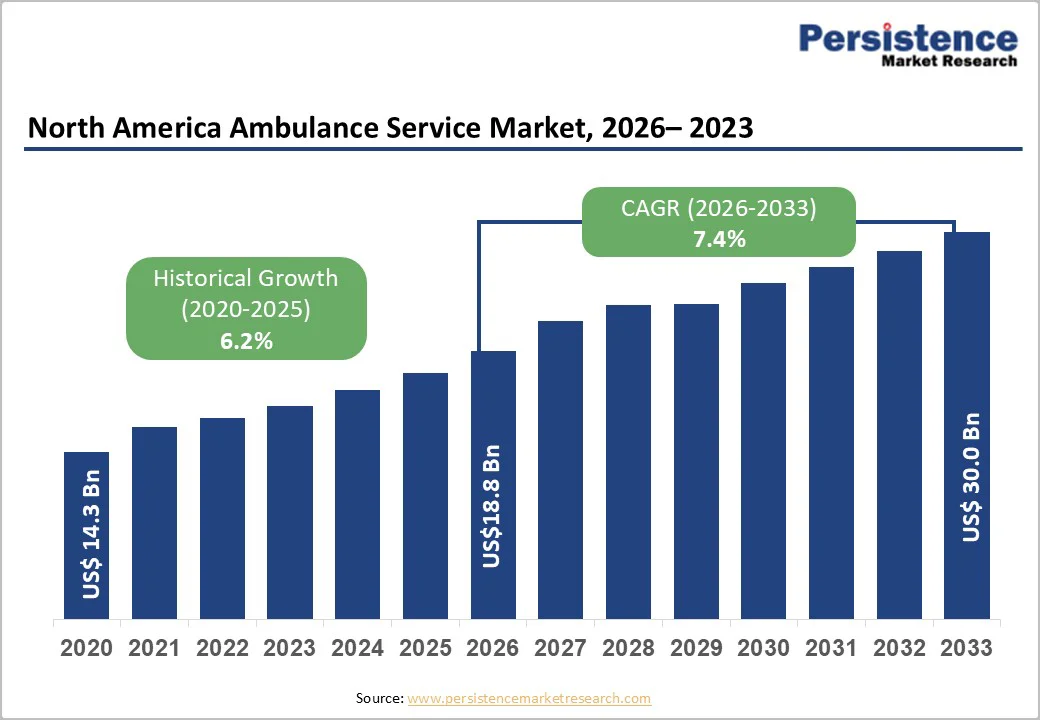

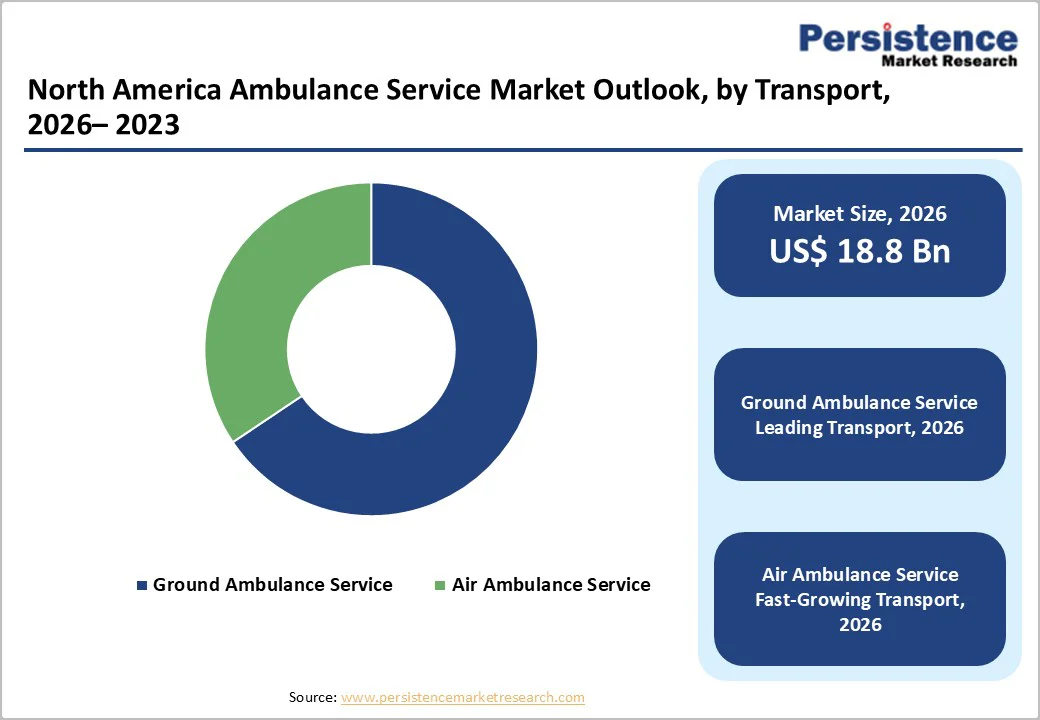

The North America ambulance service market size is estimated to grow from US$ 18.80 billion in 2026 and projected to reach US$ 30.03 billion by 2033, growing at a CAGR of 7.4% during the forecast period from 2026 to 2033.

The North America ambulance service market is driven by a rise in demand for emergency care, prevalence of chronic diseases, and investments in technologically advanced EMS vehicles and equipment. Growth is further supported by federal and state funding programs, followed by the adoption of telemedicine-enabled ambulances that improve patient monitoring and response times.

Key Industry Highlights

- Leading Transport: Ground ambulances dominate due to extensive network coverage, allowing rapid access across both urban and rural regions. Their lower operational cost and widespread availability make them the primary mode for most emergency and non-emergency transports.

- Fastest-growing Transport: Air ambulances are expanding quickly due to their ability to reach remote or geographically isolated areas where ground access is limited. Increasing adoption of advanced life-support systems and faster critical-care transport drives their growth.

- Leading Service Type: Emergency services lead the market due to rising trauma cases, cardiac emergencies, strokes, and accident rates requiring immediate intervention. Strong government support and investments in EMS infrastructure further accelerate utilization

- Fastest-growing Service Type: Growth is driven by increasing patient transfers for dialysis, rehabilitation, chemotherapy, and long-term care. The rise in chronic disease patients and medical tourism increases demand for scheduled and interfacility transportation.

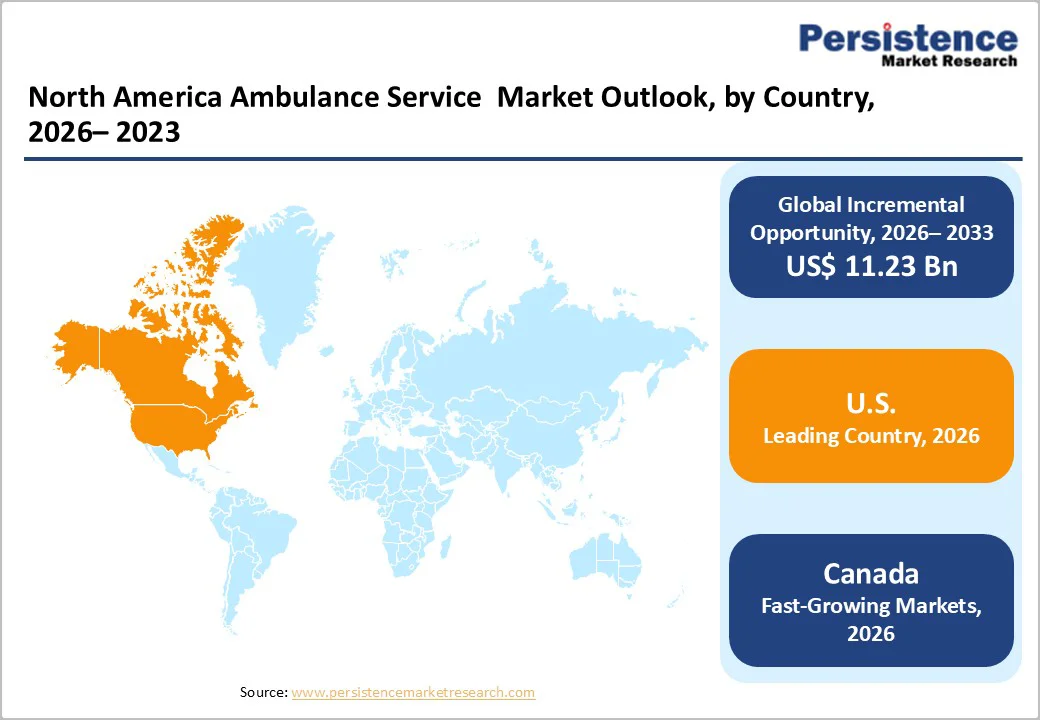

- Leading Country: The U.S. leads due to high healthcare spending, advanced EMS service models, and strong reimbursement and insurance structures. A large population base and high emergency caseload sustain dominant market demand.

- Fastest-growing Country: Canada is expanding rapidly due to investments in rural EMS accessibility, air-medical networks, and federal healthcare support programs. Rising chronic illness incidence and large geographic coverage needs boost ambulance service growth.

| Key Insights | Details |

|---|---|

| North America Ambulance Service Market Size (2026E) | US$ 18.80 Bn |

| Market Value Forecast (2033F) | US$ 30.03 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.2% |

Market Dynamics

Driver - Rising Trauma Burden & Technology-Enabled Emergency Response

Higher accident and trauma volumes driven by growing urbanization are significantly increasing ambulance utilization across North America. For instance, according to the U.S. Department of Transportation, an estimated 2.44 million people were injured in roadway incidents in 2023, up from 2.38 million in 2022, reflecting a 2.5% increase.

Although the rise was not statistically significant and the injury rate per 100 million vehicle miles traveled remained stable at 75, the absolute growth in trauma cases highlights the demand for emergency response. This continuing burden of road injuries directly contributes to increased call volumes, ambulance dispatch frequency, and greater operational requirements for EMS providers across North America.

Rapid population concentration in metropolitan regions, heavier traffic congestion, and rising road injury rates are escalating emergency call frequencies and critical-care transport demand. This trend is pushing healthcare systems and municipal agencies to expand emergency medical service (EMS) fleets and improve response infrastructure to reduce mortality risks and pre-hospital delays.

Moreover, the integration of advanced technology, such as on-board diagnostic monitoring, tele-EMS connectivity, GPS-optimised dispatch, and electronic patient records, is transforming the quality and pace of pre-hospital care delivery.

Real-time communication between paramedics and emergency departments enables faster medical decision-making, more accurate triage, and better outcomes during transport. These advancements increase the value proposition of ambulance services and support the transition toward data-driven, outcomes-based emergency care.

Restraints - Escalating Cost Pressures & Regulatory Complexity Impacting EMS Operations

Rising operating expenses across fuel, vehicle procurement, maintenance, and advanced medical equipment are intensifying financial pressure on ambulance service providers in North America.

For instance, in November 2026, ambulance transport costs in Spokane County, Washington, saw a sharp increase, reflecting rising operational pressures across North America. American Medical Response (AMR), which handles about 95% of local transports, announced that ambulance rides will exceed $5,000 next year up dramatically from $975 in 2021.

Persistent inflation, higher fleet modernization costs, and increased spending for safety and monitoring technologies continue to elevate per-call operating economics. As margins tighten, many private and municipal EMS organizations face growing challenges in sustaining service coverage, upgrading fleets, and investing in workforce capacity without raising service fees or relying on subsidies.

Furthermore, regulatory fragmentation across U.S. states and Canadian provinces adds significant compliance and administrative burdens. Variability in licensing standards, reimbursement policies, certification mandates, and operational protocols makes cross-regional scaling difficult and resource-intensive.

EMS providers must navigate complex multi-jurisdictional frameworks, prolonging approval timelines and increasing legal and administrative costs. These structural hurdles limit operational expansion, delay fleet and technology deployment, and constrain industry consolidation efforts.

Opportunity - Expansion of Outsourced EMS Models & High-Acuity Transport Capabilities

The growing adoption of public-private partnerships (PPPs) and outsourced emergency medical services is creating opportunities across North America. Municipalities and healthcare networks increasingly contract private EMS operators to enhance service coverage, reduce response times, and access specialized capabilities such as neonatal, bariatric, and inter-facility transport.

For instance, in November?2026, Lincoln Memorial University (LMU) and Covenant Health announced a strategic EMS partnership: Covenant will begin running its ambulance services from an LMU-leased facility in Cumberland Gap starting December 1, improving response times across Tennessee and into Virginia and Kentucky.

This shift enables scalability, operational efficiency, and improved capital allocation, allowing private providers to extend geographic reach and invest in advanced fleet infrastructure while supporting government agencies facing budget and resource constraints.

Moreover, the demand for specialized air and critical-care transport is growing due to high volumes of time-sensitive, high-acuity cases requiring rapid stabilization and transfer to tertiary care centers.

Helicopter EMS (HEMS) and fixed-wing medical aircraft equipped with ICU-grade technology are becoming essential for trauma, stroke, cardiac, and organ-transport services. As healthcare systems emphasize faster door-to-treatment pathways, the expansion of air ambulance networks and critical-care transport fleets presents strong long-term growth potential for market participants.

Category-wise Analysis

By Transport Insights

Ground ambulance service leads the market with approximately 65.6% share in 2026. The ground ambulance service segment dominates the North America ambulance service market due to its extensive utilization in emergency response, higher call volumes, broader geographic accessibility, and critical role in inter-facility transfers.

Ground units remain the primary mode of rapid medical transport for trauma, cardiac emergencies, stroke, respiratory distress, and community medical support, supported by continuous investments in fleet expansion, digital dispatch systems, and integration of advanced onboard monitoring equipment.

Additionally, the scalability of ground ambulance networks across both urban and rural regions, compared with the limited coverage and higher operational cost of air ambulance services, further strengthens market growth.

Increasing public-private partnerships, upgraded training programs for paramedics and EMTs, and adoption of computer-aided dispatch (CAD), GPS-based navigation, and tele-EMS communication platforms are enhancing response efficiency and patient outcomes.

By Service Type Insights

Emergency services dominate the North America ambulance service market with a value share of 68.9% due to their critical role in responding to life-threatening conditions, high trauma incidence, and increasing complexity of acute medical cases.

Emergency ambulance services are essential for rapid intervention in events such as cardiac arrest, stroke, severe injuries, respiratory failure, sepsis, and mass-casualty situations, where every minute significantly impacts patient outcomes.

The growing number of emergency callouts driven by rising road accidents, workplace injuries, and chronic disease complications continues to elevate demand for high-acuity transport. Expanding advanced life support (ALS) capabilities, including paramedic-led units equipped with ventilators, ECG monitors, defibrillators, infusion pumps, and real-time tele-EMS communication systems, further strengthens service efficiency and clinical readiness during transit.

By Equipment Insights

Advanced Life Support (ALS) dominates the North America ambulance service market with a value share of 55.6% due to its ability to deliver comprehensive pre-hospital critical care supported by highly trained paramedics and advanced medical equipment.

ALS units are equipped with cardiac monitoring, defibrillators, ventilators, IV drug administration systems, and real-time telemedicine connectivity, enabling rapid stabilization of patients experiencing cardiac arrest, major trauma, stroke, respiratory failure, and other complex emergencies.

The growing burden of chronic and acute diseases, rising emergency call volumes, and increasing adoption of clinical protocols that require advanced intervention during transport continue to boost market growth in the region.

Competitive Landscape

The North America ambulance service market is competitive, led by players such as American Air Ambulance, Babcock International Group, Air Methods., Acadian Ambulance Service, Aero Med Express, and Falck A/S. These providers are focused on expanding fleet capabilities, enhancing emergency response infrastructure, and integrating advanced tele-EMS and real-time monitoring technologies to improve patient outcomes.

Market leaders actively pursue mergers & acquisitions, public-private partnerships, and geographic network expansions to strengthen their operational presence. Additionally, investment in digital dispatch automation, GPS fleet optimization, and advanced life support (ALS) training supports improved clinical efficiency and accelerates adoption of data-driven emergency care models across the region.

Key Industry Developments:

- In November 2025, Pittsford Volunteer Ambulance (PVA) added a 2024 Crestline ambulance to its fleet, replacing a 2016 Road Rescue with nearly 150,000 miles. The purchase was largely funded by Jamison Schriber of Goldman Sachs. PVA, an independent not-for-profit in North America.

- In November 2025, Central Aroostook Ambulance Service in Aroostook County enhanced its care capabilities with a new ambulance, costing over $450,000 and funded through a federal grant. Serving Mars Hill, Blaine, and Bridgewater, the larger, more spacious vehicle joined the fleet in late summer, providing additional equipment and improved services for the growing ambulance service.

- In June 2025, Falck USA launched ambulance operations in the Dallas/Fort Worth Metroplex, expanding its presence into the Southwest and bringing its globally recognized emergency care standards to one of the fastest-growing U.S. regions.

Companies Covered in North America Ambulance Service Market

- Babcock International Group

- Air Methods.

- Acadian Ambulance Service

- Aero Med Express

- Falck A/S

- Global Medical Response

- PHI Air Medical

- MetroAtlanta Ambulance Service

- Superior Air-Ground Ambulance Service, Inc.

- AmeriPro Health

- FirstMed Ambulance Services, Inc.

- Others

Frequently Asked Questions

The North America ambulance service market is projected to be valued at US$ 18.80 Bn in 2026.

Rising emergency call volumes, increasing trauma and chronic disease cases, and expanding demand for rapid, advanced pre-hospital medical intervention are driving market growth.

The North America ambulance service market is poised to witness a CAGR of 7.4% between 2026 and 2033.

Expansion of public-private EMS partnerships and growth of non-emergency medical transport are creating significant opportunities in the market.

Major players in the North America ambulance service market are American Air Ambulance, Babcock International Group, Air Methods., Acadian Ambulance Service, Aero Med Express, and Falck A/S.