- Healthcare Services

- North America Mobile Health Market

North America Mobile Health Market Size, Share, and Growth Forecast, 2026 – 2033

North America Mobile Health Market by Service Type (Treatment Services, Diagnostic Services, Others), Device (Blood Glucose Monitors, Cardiac Monitors, Hemodynamic Monitors, Others), and Country Analysis for 2026 – 2033

North America Mobile Health Market Size and Trends Analysis

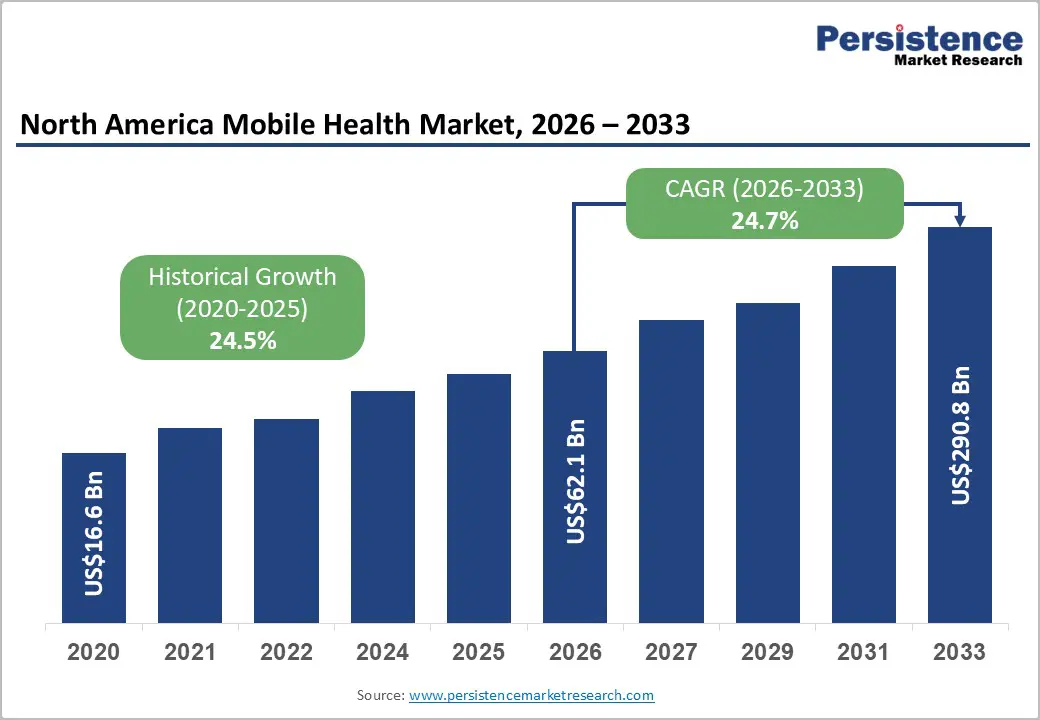

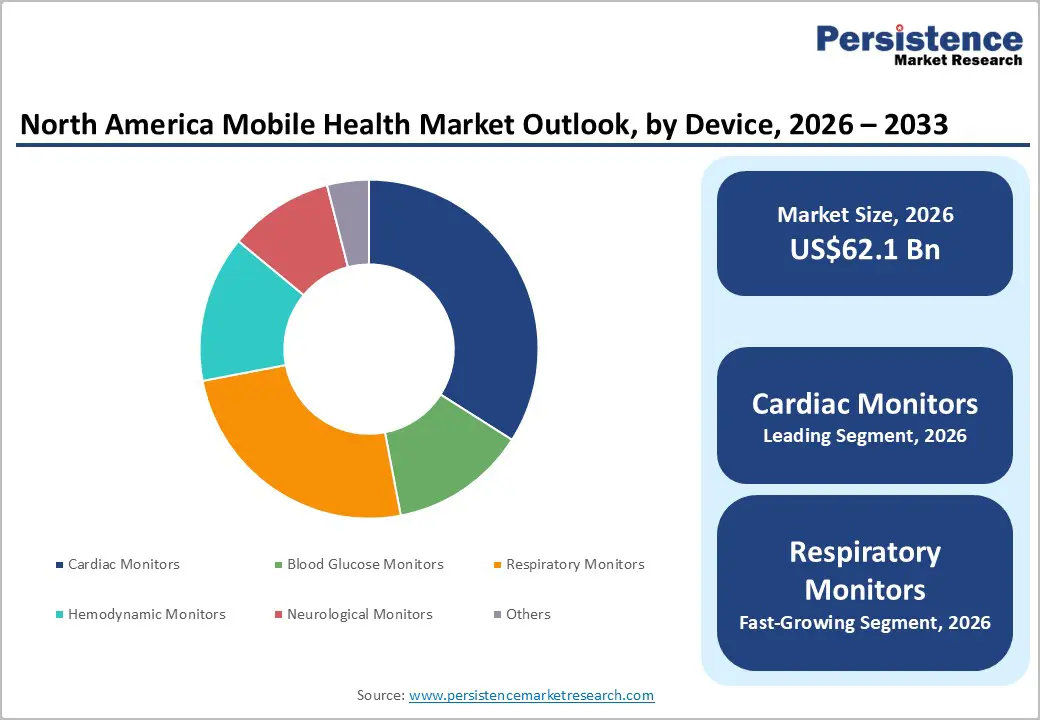

The North America mobile health market size is likely to be valued at US$62.1 billion in 2026 and is expected to reach US$290.8 billion by 2033, growing at a CAGR of 24.7% during the forecast period from 2026 to 2033, driven by increasing digital transformation of healthcare systems and the widespread adoption of connected health technologies.

The growing burden of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions has significantly increased the demand for remote monitoring and continuous patient engagement solutions. Mobile health platforms enable healthcare providers to deliver real-time care, improve patient adherence to treatment, and enhance disease management outside traditional clinical settings. The strong penetration of smartphones, wearable devices, and mobile applications has accelerated the integration of digital health tools into everyday healthcare practices. Advancements in wireless connectivity, cloud computing, artificial intelligence, and data analytics are enabling seamless transmission and interpretation of health data, supporting more personalized and proactive healthcare delivery.

Key Industry Highlights:

- Leading Region: The U.S. is anticipated to be the leading region, accounting for a market share of 85% in 2026, driven by high adoption of telehealth platforms, advanced digital health infrastructure, strong presence of leading technology companies, and widespread use of smartphones and wearable health devices.

- Fastest-growing Region: Canada is likely to be the fastest-growing region in the North America mobile health in 2026, supported by growing digital health adoption, government-backed telehealth initiatives, and increasing use of mobile healthcare applications and remote monitoring solutions.

- Leading Service Type: Monitoring services are projected to represent the leading service type in 2026, accounting for 68% of the revenue share, driven by strong adoption of remote patient monitoring for chronic disease management.

- Leading Device Type: Cardiac monitors are anticipated to be the leading device type, accounting for over 30% of the revenue share in 2026, supported by rising cardiovascular disease prevalence and increasing adoption of remote cardiac monitoring devices.

| Key Insights | Details |

|---|---|

| North America Mobile Health Market Size (2026E) | US$62.1 Bn |

| Market Value Forecast (2033F) | US$290.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 24.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 24.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Increasing Prevalence of Chronic Diseases and Aging Population

The growing prevalence of chronic diseases such as diabetes, cardiovascular disorders, respiratory illnesses, and hypertension is significantly driving the adoption of mobile health solutions across North America. Healthcare providers increasingly rely on mobile health applications and connected monitoring devices to track patient health data in real time and improve disease management outside traditional clinical settings. Remote patient monitoring tools enable continuous observation of vital parameters, helping physicians detect early warning signs and intervene promptly. As healthcare systems shift toward value-based care models, mHealth platforms support better patient engagement, medication adherence, and long-term disease management while reducing hospital readmissions and healthcare costs.

The expanding aging population in North America is accelerating demand for accessible and home-based healthcare solutions. Older adults often require continuous health monitoring and frequent medical consultations, which mobile health technologies can efficiently provide through wearable devices, digital monitoring tools, and telehealth platforms. These solutions allow seniors to manage chronic conditions independently while maintaining regular communication with healthcare providers. Governments and healthcare organizations are also encouraging remote care initiatives to reduce pressure on hospitals and long-term care facilities.

Technological Advancements in Wearables and AI Integration

Modern wearables such as smartwatches, fitness trackers, and connected biosensors can continuously measure vital parameters, including heart rate, oxygen saturation, physical activity, and sleep patterns. These devices synchronize with mobile health applications, allowing healthcare professionals to access real-time patient data and make informed treatment decisions. Continuous innovation in sensor technologies, miniaturization, and battery efficiency has improved the accuracy and usability of wearable health devices, making them increasingly popular among both healthcare providers and consumers.

Artificial intelligence integration enhances the capabilities of mobile health platforms by enabling predictive analytics, automated diagnostics, and personalized health insights. AI-driven algorithms analyze large volumes of patient data collected from wearables and mobile applications to detect early health risks and recommend preventive measures. This helps clinicians deliver more precise and proactive care while improving patient outcomes. AI supports virtual health assistants, symptom-checking tools, and digital coaching programs that guide users in managing their health conditions.

Barrier Analysis - Data Privacy and Cybersecurity Vulnerabilities

Despite strong growth prospects, concerns related to data privacy and cybersecurity remain significant challenges for the mobile health market. mHealth (mobile health) platforms collect and store large volumes of sensitive patient information, including medical histories, diagnostic data, and personal health records. The transmission of this information across mobile devices, cloud systems, and digital networks increases the risk of unauthorized access, data breaches, and cyberattacks. Healthcare organizations must therefore implement strict security protocols to ensure patient confidentiality and protect digital health infrastructure from evolving cyber threats.

Regulatory frameworks such as healthcare data protection laws impose strict compliance requirements for companies operating in the mobile health ecosystem. While these regulations aim to safeguard patient information, they also increase operational complexity for technology developers and healthcare providers. Ensuring secure data storage, encryption, and secure communication channels requires continuous investment in cybersecurity technologies. Privacy concerns may reduce patient trust in digital healthcare platforms, slowing adoption in certain populations. Addressing these security challenges through advanced encryption, regulatory compliance, and secure data management systems is essential for sustaining long-term market growth.

Limited Reimbursement and Economic Sustainability

In many healthcare systems, reimbursement structures have traditionally focused on in-person medical consultations and hospital-based treatments. Healthcare providers may face uncertainty when adopting mobile health technologies that are not fully covered under existing insurance policies. This lack of standardized reimbursement frameworks can discourage hospitals, clinics, and physicians from investing in mHealth platforms and remote monitoring solutions. Inconsistent insurance coverage for digital health services limits the large-scale implementation of mobile health platforms across healthcare facilities.

Economic sustainability also remains a concern for digital health startups and service providers. Developing advanced mobile health applications, integrating them with healthcare systems, and maintaining regulatory compliance requires significant financial resources. Smaller companies often struggle to scale their technologies without consistent reimbursement support or long-term healthcare partnerships. Healthcare providers must balance the costs of implementing digital health solutions with the expected improvements in patient outcomes and operational efficiency. Until reimbursement systems fully adapt to digital healthcare delivery models, the adoption of mobile health technologies may face certain financial limitations.

Opportunity Analysis - Rise of Preventive Wellness Solutions for Mental Health

Growing awareness of mental health and preventive wellness is generating strong opportunities for mobile health applications in North America. Increasing levels of stress, anxiety, and lifestyle-related health issues have encouraged individuals to seek digital solutions that support mental well-being and daily health management. Mobile health platforms now offer a wide range of wellness tools, including meditation programs, stress management applications, sleep monitoring, and virtual counseling services. These digital solutions allow users to track emotional health, receive personalized wellness recommendations, and access mental health support from the convenience of their smartphones.

Employers and healthcare organizations are also promoting digital wellness programs to improve workforce health and productivity. Mobile health applications are increasingly integrated into corporate wellness initiatives that encourage healthy habits, mental resilience, and preventive care. Advances in wearable devices enhance these programs by tracking stress levels, physical activity, and sleep quality to provide actionable wellness insights. Many mobile health platforms now integrate AI-based mental health assessments and digital therapy tools to support early detection of psychological conditions.

Expansion into Personalized Medicine via AI and Genomics Convergence

The convergence of artificial intelligence, genomics, and mobile health technologies is creating new opportunities for personalized medicine. Mobile health platforms can integrate patient genetic data, lifestyle information, and real-time health metrics to generate personalized treatment recommendations. This approach enables healthcare providers to design targeted therapies based on an individual’s genetic profile, improving treatment effectiveness and reducing adverse drug reactions. As precision medicine continues to advance, mobile health applications are becoming valuable tools for collecting and analyzing patient-specific data in real time.

AI-driven analytics enhance personalized healthcare by identifying patterns within genetic and physiological data collected through connected devices. Mobile platforms can provide customized health insights, preventive recommendations, and early disease detection based on individual risk factors. Pharmaceutical companies, healthcare providers, and digital health developers are increasingly collaborating to integrate genomic data into mobile health ecosystems. This integration supports more accurate diagnostics, individualized treatment planning, and long-term disease prevention strategies. As personalized healthcare gains importance, the combination of AI, genomics, and mobile health technologies will open significant growth opportunities within the digital health landscape.

Category-wise Analysis

Service Type Insights

Monitoring services are expected to lead the North America mobile health market, accounting for approximately 68% of revenue in 2026, driven by the growing demand for continuous patient monitoring and remote disease management. Mobile health platforms integrated with wearable devices and connected sensors allow healthcare providers to track vital health parameters such as heart rate, blood pressure, oxygen saturation, and glucose levels in real time. These solutions are particularly valuable for managing chronic diseases, including cardiovascular conditions, diabetes, and respiratory disorders.

For example, Philips Healthcare offers remote monitoring platforms that allow healthcare providers to track patient health data through connected mobile applications and wearable devices, supporting continuous patient care outside hospital environments.

Wellness and fitness solutions are likely to represent the fastest-growing segment, supported by the rising focus on preventive healthcare and lifestyle management. Consumers are increasingly using mobile health applications to monitor daily activities, maintain fitness routines, track sleep patterns, and manage stress levels. These digital wellness platforms encourage individuals to adopt healthier lifestyles by providing personalized insights, activity tracking, and health coaching features.

The popularity of smartphones and wearable fitness devices has significantly expanded the reach of wellness applications among younger populations and health-conscious consumers. For example, Headspace provides meditation, mindfulness, and stress management programs through mobile platforms, demonstrating how wellness-focused applications are becoming an important component of the mobile health ecosystem.

Device Type Insights

Cardiac monitors are projected to lead the market, capturing around 30% of the revenue share in 2026, supported by the increasing prevalence of cardiovascular diseases and the growing demand for continuous cardiac monitoring. Mobile-connected cardiac monitoring devices allow patients and healthcare providers to track heart activity in real time using wearable sensors and smartphone applications. These devices support early detection of irregular heart rhythms, enabling physicians to provide timely medical intervention and prevent severe cardiac complications.

For example, the Apple Watch includes electrocardiogram and heart rhythm monitoring features that allow users to track heart health and share data with healthcare professionals through connected mobile applications.

Respiratory monitors are likely to be the fastest-growing device type, driven by the increasing prevalence of respiratory conditions and the growing need for continuous respiratory health monitoring. Mobile-connected respiratory monitoring devices enable patients to track breathing patterns, oxygen saturation levels, and lung function through portable sensors and smartphone applications. Advancements in sensor technology and wireless connectivity are improving the accuracy and usability of these devices, enabling patients to monitor respiratory health more effectively.

For example, Medtronic plc offers connected respiratory monitoring technologies that integrate with mobile health platforms, allowing healthcare providers to track patient respiratory conditions remotely and deliver timely clinical support.

Country Insights

U.S. Mobile Health Market Trends

The U.S. is anticipated to be the leading region, accounting for a market share of 85% in 2026, driven by the widespread adoption of telehealth services, wearable devices, and digital health applications. Healthcare providers are increasingly integrating mobile platforms with electronic health records and remote patient monitoring systems to enhance patient engagement and improve care delivery. A large proportion of consumers now use mobile health tools to track fitness, manage chronic conditions, and communicate with healthcare professionals remotely. Telehealth has become a major component of healthcare delivery, with many physicians regularly using virtual consultations and mobile platforms to provide follow-up care and chronic disease management.

Another major trend is the increasing integration of artificial intelligence, predictive analytics, and cloud-based healthcare platforms. AI-powered mobile health applications analyze patient-generated data from wearable devices and mobile apps to support early diagnosis, personalized treatment recommendations, and preventive healthcare strategies. Healthcare organizations are also investing in remote patient monitoring programs to reduce hospital visits and improve long-term disease management.

For example, Dexcom provides continuous glucose monitoring systems that connect with mobile applications, allowing patients with diabetes to track glucose levels in real time and share data with healthcare providers for better treatment management.

Canada Mobile Health Market Trends

Canada is likely to be the fastest-growing region, driven by the increasing adoption of telehealth services, expanding digital health infrastructure, and the rising use of mobile health applications and wearable monitoring technologies. Many healthcare institutions are integrating mobile platforms with electronic health records and telehealth systems to improve care coordination and enable continuous monitoring of chronic conditions. Virtual care delivered through mobile applications is particularly important for rural and remote populations where access to healthcare facilities can be limited.

The rising adoption of wearable devices such as smartwatches and fitness trackers is enabling individuals to track vital health indicators, including physical activity, sleep patterns, and heart rate, through connected mobile applications.

Another key trend shaping Canada’s mobile health market is the increasing use of artificial intelligence and data analytics within digital health platforms. AI-enabled mobile health applications analyze patient-generated health data to provide predictive insights, symptom monitoring, and personalized treatment recommendations. Healthcare providers are also expanding remote patient monitoring programs to manage chronic diseases and support home-based care. For example, TELUS Health has developed digital health platforms that connect patients with healthcare professionals through mobile applications, enabling virtual consultations, prescription services, and secure access to medical records.

Competitive Landscape

The North America mobile health market exhibits a moderately fragmented structure, driven by the presence of both technology companies and specialized digital health providers offering mobile applications, connected medical devices, and remote patient monitoring platforms. The competitive environment is characterized by rapid technological innovation, increasing investments in digital healthcare, and strong collaboration between healthcare providers, telecom operators, and software developers. Companies in the market are focusing on expanding their digital health ecosystems, improving interoperability with electronic health records, and strengthening partnerships with hospitals and healthcare institutions.

With key leaders including Apple Inc., Medtronic plc, Koninklijke Philips N.V., Boston Scientific Corporation, AT&T Inc., and Veradigm, the market demonstrates strong competition between consumer technology firms and medical device manufacturers. These players compete through continuous product innovation, integration of artificial intelligence and wearable technologies, strategic acquisitions, and expansion of remote monitoring solutions that improve patient engagement and chronic disease management. Many companies are also investing heavily in research and development to introduce advanced mobile health platforms capable of delivering personalized healthcare services.

Key Industry Developments:

- In February 2026, Former Fitbit co-founders James Park and Eric Friedman introduced Luffu, an AI-powered family health monitoring app that aggregates medical and wellness data from connected devices and platforms to provide personalized insights, medication reminders, and alerts about potential health changes.

- In November 2025, Apple Inc. is reportedly preparing to launch Health+, an AI-powered enhancement to its Health app that will provide personalized wellness coaching, nutrition tracking, and tailored health insights by analyzing user data from connected Apple devices.

Companies Covered in North America Mobile Health Market

- Veradigm (Allscripts Healthcare, LLC)

- Apple Inc.

- AT&T Inc.

- Oracle (Cerner Corporation)

- Boston Scientific Corporation

- Cisco Systems Inc.

- Koninklijke Philips N.V.

- Medtronic plc

- MobileSmith

- Samsung Healthcare Solutions

- eClinicalWorks

- Care Innovations, LLC

- Telus Health

Frequently Asked Questions

The North America mobile health market is projected to reach US$62.1 billion in 2026.

The North America mobile health market is driven by the rising prevalence of chronic diseases, increasing adoption of smartphones and wearable health devices, and the growing demand for telehealth and remote patient monitoring solutions.

The North America mobile health market is expected to grow at a CAGR of 24.7% from 2026 to 2033.

Key market opportunities include the expansion of AI-powered personalized healthcare, growing adoption of preventive wellness and mental health apps, and increasing integration of mobile health platforms with wearable and remote monitoring technologies.

Veradigm (Allscripts Healthcare, LLC), Apple Inc., AT&T Inc., and Oracle (Cerner Corporation) are the leading players.