- Food Ingredients & Additives

- North America Spices Market

North America Spices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

North America Spices Market by Product Type (Pepper, Cinnamon, Ginger, Cumin, Bay Leaves, Dried Chilies, Cardamom, Turmeric, Cloves, Others), by Nature (Organic, Conventional), by Form (Whole, Powder, Oil, Other), Application (Processed Food, Nutraceuticals, Cosmetics & Personal Care, Beverages, Other), Distribution Channel (B2B, B2C) and Regional Analysis from 2026 to 2033

North America Spices Market Size and Share Analysis

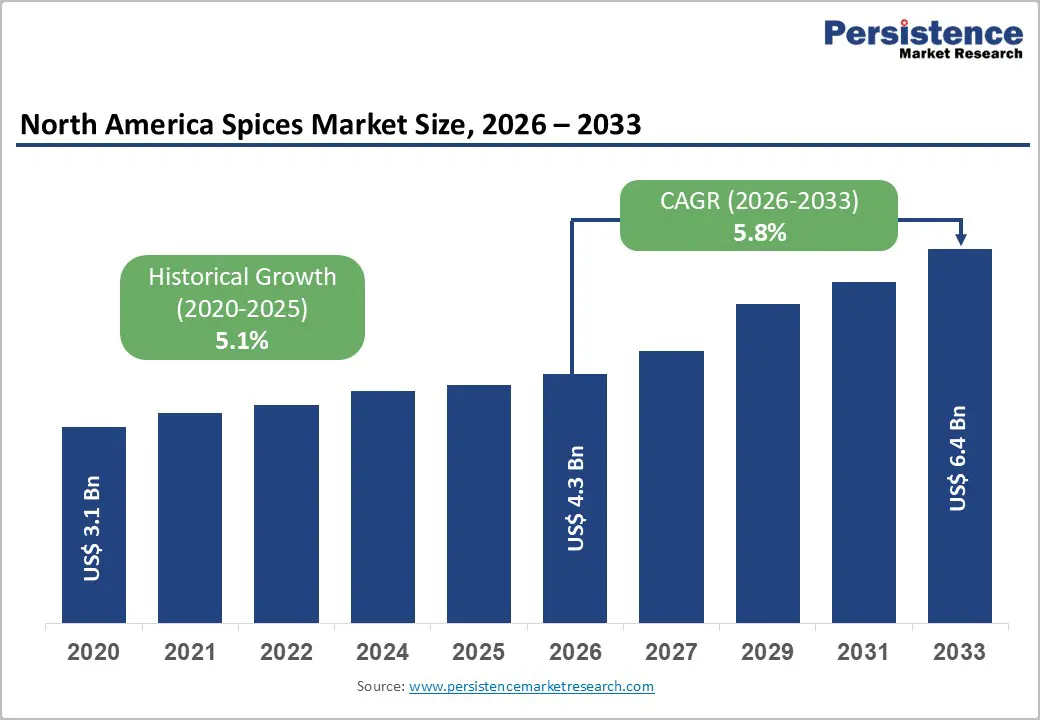

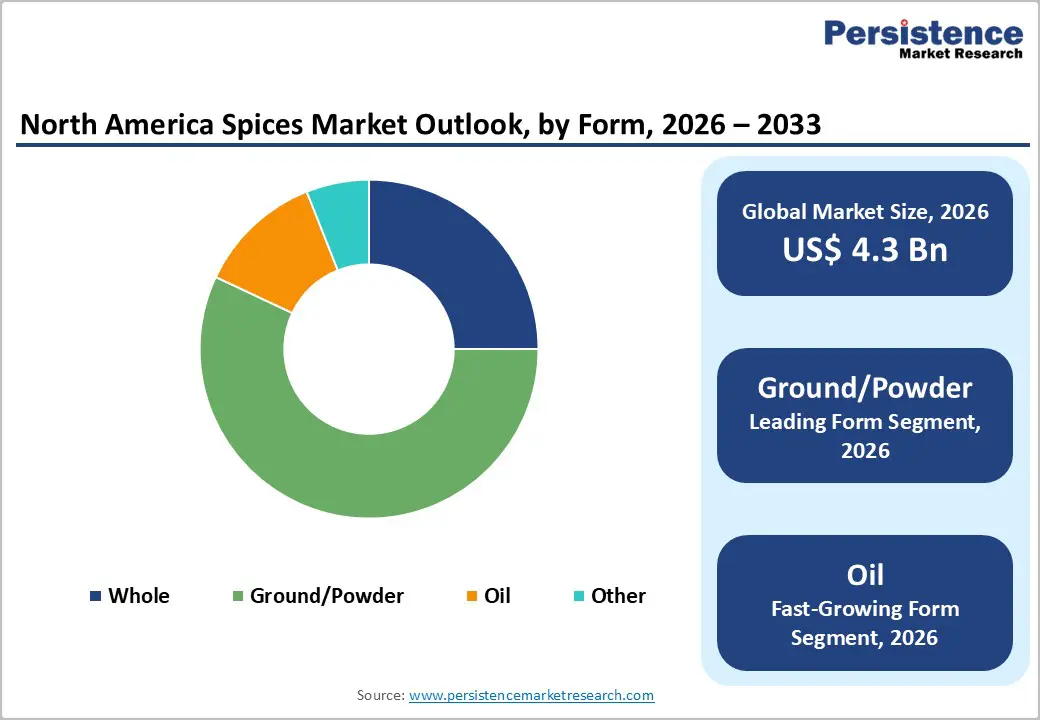

The North America Spices Market size is expected to be valued at US$ 4.3 billion in 2026 and projected to reach US$ 6.4 billion by 2033, growing at a CAGR of 5.8% between 2026 and 2033

The North America spices market is evolving from a pantry staple category into a value-added flavor solutions space, shaped by convenience cooking, clean-label expectations, and foodservice collaboration. Innovation across blends, formats, sourcing, and packaging is redefining how spices are consumed, positioned, and monetized across the U.S. and Canada.

Key Industry Highlights

- Leading Country: United States, holding approximately 81% market share, supported by a large consumer base, diverse ethnic cuisines, strong retail penetration, and rapid adoption of blended and functional seasonings for home and foodservice use.

- Fastest-Growing Form Segment: Ground/Powder spices, holding around 56% market share as of 2025, fueled by convenience cooking, compatibility with processed foods, and widespread use in sauces, marinades, and ready-to-cook applications.

- Market Drivers: Rising demand for quick, flavorful homemade meals is accelerating spice blend consumption, as consumers seek restaurant-style taste, consistency, and ease of use aligned with hybrid work lifestyles and modern cooking appliances.

- Opportunities: Co-creating custom seasoning blends with national QSR and restaurant chains for exclusive menu items offers long-term volume contracts, brand visibility, and innovation-led growth opportunities for both established players and new entrants.

- Key Developments: In November 2025, McCormick® refreshed the McCormick Gourmet Collection with premium, display-forward packaging emphasizing quality and global sourcing. In August 2025, Felton’s EM² Seasonings partnered with Savoy Restaurant in Detroit to strengthen foodservice collaboration and brand presence.

| Key Insights | Details |

|---|---|

| North America Spices Market Size (2026E) | US$ 4.3 Bn |

| Market Value Forecast (2033F) | US$ 6.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Dynamics

Driver – Rising demand for quick, flavorful homemade meals boosts spice blend consumption

Weeknight cooking has become a balancing act between speed and satisfaction, pushing spices into a starring role. North American consumers increasingly rely on ready spice blends to recreate restaurant-style flavors without lengthy preparation. Blends simplify cooking decisions, reduce ingredient clutter, and deliver consistent taste outcomes, making them ideal for time-pressed households. As hybrid work lifestyles persist, home kitchens are being treated as everyday dining spaces rather than occasional use areas. This shift has elevated demand for all-purpose seasonings, global cuisine blends, and recipe-specific mixes that shorten preparation time while enhancing sensory appeal.

In the U.S., McCormick has expanded its Grill Mates and Flavor Maker ranges to support fast, customizable home cooking occasions. These blends align with air fryers, sheet-pan meals, and one-pot recipes popularized through digital cooking content. Retailers are responding by increasing shelf space for blended spices over single-origin products. This behavioral shift directly supports higher repeat purchases, premium pricing, and innovation-led growth across the North America spices market.

Restraints – Climate impacts and crop yield variability in origin countries squeeze margins and availability

Spice supply chains begin thousands of miles away, where weather volatility increasingly dictates availability and cost. Irregular rainfall, prolonged droughts, and shifting monsoon patterns in key producing regions disrupt harvest cycles for pepper, cinnamon, turmeric, and chilies. These disruptions reduce yields, create quality inconsistencies, and compress export volumes, tightening supply into North America. Importers face rising procurement costs alongside longer lead times, complicating inventory planning for processors and retailers.

Margin pressure intensifies when climate-driven shortages coincide with strong downstream demand. Brands must absorb higher raw material costs or risk consumer pushback through price increases. Smaller spice companies feel this impact more acutely due to limited sourcing diversification. In response, buyers are restructuring contracts, building buffer inventories, and exploring alternative origins. Climate variability is no longer a seasonal risk; it has become a structural restraint shaping sourcing strategies across the North America spices market.

Opportunity – Co-create custom seasoning formats with national QSR and restaurant chains for exclusive menu items

Menu differentiation has become a competitive weapon for quick-service and casual dining chains, opening space for spice innovation partnerships. Co-developed seasoning blends allow restaurants to deliver proprietary flavors while spice suppliers gain stable, high-volume demand. These collaborations move beyond basic salt-pepper formulations toward signature rubs, finishing seasonings, and region-inspired blends designed for specific proteins or cooking equipment.

For key players and startups alike, this model offers predictable offtake, faster commercialization, and brand visibility through menu mentions. U.S. restaurant chains increasingly seek clean-label, allergen-controlled seasonings that perform consistently at scale. New entrants can position themselves as agile formulation partners, while established suppliers can leverage manufacturing scale and quality systems. Exclusive QSR blends create long-term contracts, reduce retail dependence, and embed spice suppliers directly into foodservice innovation pipelines.

Category-wise Analysis

By Form, Ground/Powder dominate the global spices market

Ground/Powder hold approx. 56% market share as of 2025, reflecting their convenience, versatility, and compatibility with modern cooking habits. Powdered spices integrate easily into sauces, marinades, snacks, and packaged foods, making them the preferred format for both households and industrial users. Their uniform dispersion and longer perceived usability support higher repeat consumption compared to whole formats.

Whole spices maintain relevance in premium culinary applications and ethnic cooking traditions where freshness perception matters. Oils and oleoresins are gaining traction in food manufacturing due to consistent potency and shelf stability. Despite these niches, ground spices continue to dominate as they align seamlessly with fast cooking, processed foods, and scalable flavor formulation needs.

By Nature, organic spices are expected to show lucrative growth during forecast period

Organic spices are expected to grow at CAGR of 7.6%, driven by rising consumer scrutiny around farming practices, residue levels, and ingredient transparency. Shoppers increasingly associate organic certification with safer consumption and environmental responsibility, particularly in products used daily. Food brands are reformulating sauces, snacks, and ready meals with organic seasonings to support clean-label claims. Retailers are reinforcing this shift through premium shelf placement and private-label organic spice lines.

Conventional spices continue to dominate volume sales due to lower pricing and wider availability. They remain essential for foodservice operators and value-focused consumers. However, growth momentum is gradually shifting as organic supply chains mature, certification costs stabilize, and sustainability narratives influence purchasing behavior across North America.

Region-wise Insights

U.S. Spices Market Trends and Insights

U.S. holds approximately 81% market share in the North America Spices Market, anchored by a large consumer base, diverse culinary influences, and strong retail infrastructure. Demand is shifting toward globally inspired flavors, functional spice blends, and clean-label formulations that support health-driven positioning. Digital recipe platforms and social media continue shaping spice discovery and trial.

Manufacturers are investing in recyclable packaging, traceable sourcing, and AI-driven flavor development. Growth in D2C spice brands and private labels reflects evolving buying behavior. Foodservice innovation, ethnic cuisine expansion, and premiumization trends position the U.S. as the primary driver of regional spice market evolution.

Canada Spices Market Trends and Insights

Canada Spices Market is expected to grow at a CAGR of 6.6%, supported by rising multicultural populations and increasing interest in international home cooking. Consumers are experimenting with Middle Eastern, South Asian, and Caribbean flavors, boosting demand for authentic spice profiles. Health-focused buying patterns are strengthening interest in turmeric, ginger, and functional blends.

Retailers emphasize organic certification, ethical sourcing, and bilingual packaging to align with regulatory and consumer expectations. Smaller batch brands and specialty spice companies are gaining traction through farmers’ markets and online platforms. Canada’s market favors premium quality, transparency, and culinary storytelling, creating distinct growth dynamics from the U.S. landscape.

Market Competitive Landscape

The North America spices market is moderately fragmented, with global leaders coexisting alongside strong regional and niche players. Leading companies focus on clean-label sourcing, third-party certifications, and sustainability-linked supplier programs to strengthen brand trust. Packaging innovation, including recyclable jars and freshness-preserving designs, is becoming a competitive differentiator.

Regulatory compliance around food safety, labeling, and organic claims shapes market entry strategies. Companies are expanding D2C channels, developing custom blends, and introducing globally inspired flavor portfolios. Strategic partnerships with foodservice operators and private labels help balance retail competition while supporting scalable growth across diverse consumer segments.

Key Developments:

- In November 2025, McCormick® announced a refreshed visual identity for its McCormick Gourmet Collection, introducing premium, display-forward packaging that highlights craftsmanship, quality cues, and the brand’s global sourcing of high-grade herbs and spices.

- In August 2025, Felton’s EM² Seasonings (Felton’s Spice) announced a strategic partnership with Savoy Restaurant in Detroit, Michigan, aimed at expanding brand visibility and strengthening its presence within the foodservice and culinary collaboration space.

- In February 2025, Newman’s Own expanded its portfolio with the launch of Newman’s Own Organic Seasonings, a certified organic line developed through a licensing agreement with Harris Spice Co., a California-based spice and seasoning manufacturer, reinforcing the brand’s commitment to organic sourcing and clean-label offerings.

Companies Covered in North America Spices Market

- McCormick & Company, Inc.

- Olam International Limited

- Badia Spices, Inc.

- Sleaford Quality Foods Ltd.

- Prymat sp. z o. o.

- Worlée NaturProdukte GmbH

- Kräuter Mix GmbH

- El Clarín Spices S.L

- Elite Spice

- Ramón Sabater, S.A.U.

- DF World of Spices GmbH

- Felton’s EM²

- Others

Frequently Asked Questions

The North America Spices market is projected to be valued at US$ 4.3 Bn in 2026.

Rising demand for quick, flavorful homemade meals boosts spice blend consumption drives the demand for North America Spices Market.

The North America Spices market is poised to witness a CAGR of 5.8% between 2026 and 2033

Co-creating custom seasoning formats with national QSR and restaurant chains for exclusive menu items is the key market opportunity

Major players in the North America Spices Market include McCormick & Company, Inc., Olam International Limited, Badia Spices, Inc., Sleaford Quality Foods Ltd.,and others