- Processed Food

- North America Healthy Snack Chips Market

North America Healthy Snack Chips Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

North America Healthy Snack Chips Market by Sales Channel (Retail Stores, Online Retail, Convenience Stores, Supermarkets, Others), Product (Tortilla Chips, Pop Chips, Potato Chips, Tapioca Chips, Others), and by Regional Analysis, 2026-2033

Market Size and Share Analysis

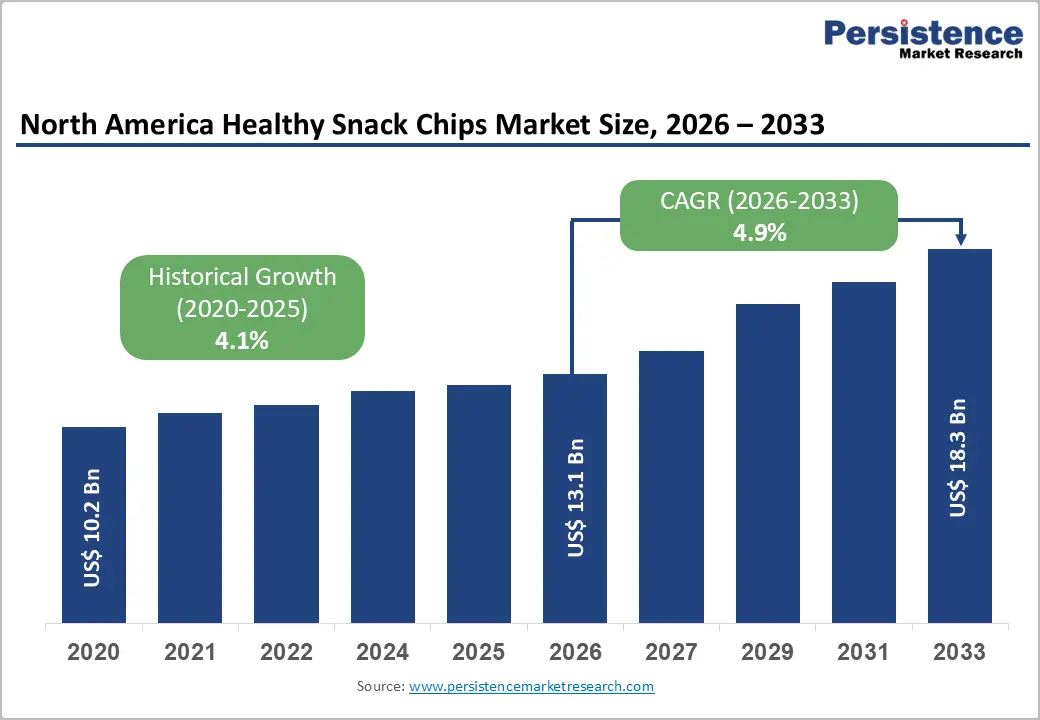

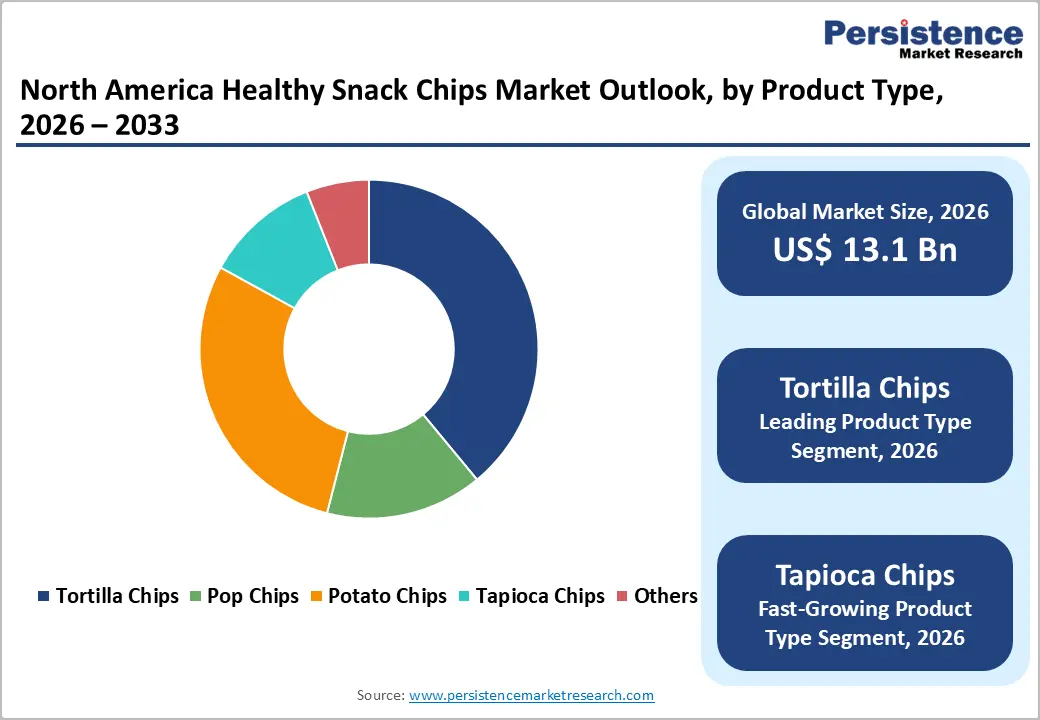

The North America Healthy Snack Chips Market size is expected to be valued at US$ 13.1 billion in 2026 and projected to reach US$ 18.3 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033

Clean eating has moved beyond labels into everyday snacking behavior, reshaping how chips are formulated, positioned, and sold across North America. Innovation now sits at the intersection of transparency, lifestyle alignment, and retail execution, with the U.S. and Canada evolving at different but complementary speeds.

Key Industry Highlights

- Leading Country: United States, accounting for approximately 79% market share, driven by strong demand for baked and air-popped chips, bold flavor experimentation, clean oil usage, and widespread supermarket penetration supporting better-for-you snacking.

- Fastest-Growing Product Type Segment: Tapioca Chips, fueled by gluten-free positioning, cassava-based sourcing, premium texture appeal, and compatibility with clean oils and innovative seasoning blends.

- Market Drivers: Rising consumer preference for clean-label and minimally processed snacks is accelerating reformulation toward short ingredient lists, natural seasonings, and transparent sourcing, strengthening trust and repeat purchases.

- Market Opportunities: Co-branding with fitness and lifestyle platforms enables brands to embed healthy snack chips into active routines through protein-enhanced variants, limited editions, and experiential sampling strategies.

- Key Developments: In October 2025, Utz Brands showcased new flavor innovations at the NACS Show; in August 2025, Nature’s Path expanded Que Pasa Rolled Chips; in July 2025, Decadent Crunch debuted at the Summer Fancy Food Show.

| Key Insights | Details |

|---|---|

| North America Healthy Snack Chips Market Size (2026E) | US$ 13.1 Bn |

| Market Value Forecast (2033F) | US$ 18.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Rising consumer preference for clean-label and minimally processed snack options

Ingredient scrutiny has moved from niche behavior to mainstream habit, reshaping how snack chips are evaluated across North America. Shoppers increasingly associate short ingredient lists with transparency, safety, and nutritional integrity. Healthy snack chips made with recognizable grains, simple oils, and natural seasonings are perceived as smarter everyday choices, especially among urban professionals and young families. This mindset encourages brands to reformulate away from artificial flavors, preservatives, and synthetic colorants, accelerating demand for baked, air-popped, and minimally processed chips.

In the U.S., brands such as Que Pasa and Jackson’s have gained traction by highlighting clean sourcing, avocado oil usage, and grain authenticity on front-of-pack labels. Retailers actively support these products through clean-label merchandising sections. As consumer trust becomes a decisive purchase factor, clean-label positioning strengthens brand loyalty and repeat purchases, making it a powerful growth driver for the healthy snack chips market.

Restraints – Retail shelf space competition with legacy snack brands

Shelf space remains one of the toughest barriers for emerging healthy snack chip brands. Large legacy snack companies dominate prime retail placements through long-standing retailer relationships, high promotional budgets, and strong volume guarantees. Their ability to fund discounts, end-cap displays, and multi-SKU assortments often limits visibility for newer, health-focused entrants trying to gain consumer attention.

Even when healthy chips secure placement, they frequently occupy secondary shelves with lower foot traffic. Retailers remain cautious about allocating premium space to brands with shorter sales histories or higher price points. Slotting fees and performance thresholds further strain smaller players. As a result, many health-oriented brands rely heavily on regional rollouts or online channels before achieving national presence. This competitive imbalance slows scale expansion and delays profitability, restricting broader market penetration despite growing consumer demand.

Opportunity – Collaboration with fitness and lifestyle brands for co-branded healthy snack offerings

The convergence of fitness culture and everyday snacking presents a strong collaboration opportunity for healthy chip brands. Consumers increasingly align food choices with active lifestyles, seeking snacks that complement workouts, recovery routines, and wellness goals. Co-branding with gyms, sports clubs, yoga studios, or digital fitness platforms enhances credibility while expanding reach beyond traditional grocery channels.

Startups gain instant trust through association with established fitness communities, while larger brands benefit from deeper lifestyle integration. Limited-edition flavors, protein-enhanced chips, or functional positioning linked to endurance and energy resonate with performance-focused consumers. Sampling at fitness events and bundled offerings with training subscriptions strengthen engagement. These partnerships reduce customer acquisition costs while creating differentiated brand narratives. For both new entrants and established players, fitness-led collaborations transform healthy snack chips from occasional treats into routine lifestyle products, unlocking sustained growth potential across North America.

Category-wise Analysis

By Product Type, Tapioca Chips expected to show promising growth

Tapioca Chips are expected to show promising growth in forecast period as consumers explore grain-free and allergen-friendly snack alternatives. Derived from cassava, tapioca chips offer a neutral flavor base, light texture, and natural gluten-free appeal. Their compatibility with clean oils and seasoning innovation positions them well among health-conscious and digestive-sensitive consumers.

Tortilla chips continue to benefit from cultural familiarity and plant-based positioning, especially when paired with ancient grains. Pop chips attract calorie-aware consumers through air-popped formats. Potato chips retain mass appeal but face reformulation pressure to stay relevant. Tapioca chips stand out by addressing gluten avoidance, flavor versatility, and premium texture preferences simultaneously. This unique alignment with evolving dietary habits supports faster adoption and shelf expansion, reinforcing tapioca chips as a high-potential growth segment.

By Sales Channel, Supermarkets/Hypermarkets hold the leading position

Supermarkets/Hypermarkets hold approx. 47% market share as of 2025, driven by broad product assortments, high foot traffic, and strong impulse purchase behavior. These outlets enable side-by-side comparison of healthy and conventional chips, encouraging trial through visibility and promotional pricing. Private label healthy chips further strengthen category presence within large retail formats.

Convenience stores focus on single-serve packs targeting on-the-go consumption. Specialty stores emphasize premium, organic, and functional positioning with curated assortments. Online retail supports discovery, subscription models, and direct brand engagement. Despite digital growth, supermarkets remain central to volume sales due to scale, accessibility, and consumer trust. Their ability to support nationwide distribution and frequent promotions solidifies leadership within the North America healthy snack chips market.

Region-wise Insights

U.S. Healthy Snack Chips Market Trends and Insights

U.S. holds approximately 79% market share in the North America Healthy Snack Chips Market, reflecting strong demand for better-for-you snacking across demographics. Consumers increasingly favor baked, air-popped, and plant-based chips aligned with wellness routines. Flavor innovation has shifted toward bold spices, regional seasonings, and globally inspired profiles that enhance indulgence without compromising health cues.

Brands are investing in functional positioning, emphasizing protein, fiber, and clean oils. Retailers actively expand healthy snack aisles while foodservice venues incorporate better-for-you chips into combo meals. Sustainability messaging around responsible sourcing and recyclable packaging further influences purchasing decisions. As snacking replaces traditional meals, the U.S. market continues to drive innovation, scale, and premiumization within the healthy snack chips segment.

Canada Healthy Snack Chips Market Trends and Insights

Canada Healthy Snack Chips Market is expected to grow at a CAGR of 7.8% as consumers prioritize nutrition transparency and balanced snacking. Demand is rising for organic, non-GMO, and allergen-friendly chips, supported by strong regulatory awareness and label literacy. Canadian shoppers favor baked formats and simple seasoning blends that emphasize natural taste.

Local brands leverage domestic sourcing, and sustainability claims to build trust. Retailers promote healthier snacks through wellness sections and private-label innovation. Urban centers show growing interest in globally inspired flavors and portion-controlled packaging. E-commerce and specialty grocers play an increasing role in product discovery. Canada’s steady shift toward mindful eating and responsible consumption strengthens long-term demand for healthy snack chips across mainstream and premium channels.

Market Competitive Landscape

The North America healthy snack chips market remains moderately fragmented, with established snack companies competing alongside agile health-focused brands. Leading players invest in clean-label sourcing, non-GMO certifications, and transparent ingredient communication to build consumer trust. Product innovation centers on alternative bases, clean oils, and bold seasoning profiles aligned with wellness trends.

Sustainability initiatives include recyclable packaging and responsible agricultural sourcing. Companies closely monitor food labeling regulations and sodium guidelines to ensure compliance. B2C strategies dominate, supported by digital engagement, influencer marketing, and lifestyle positioning. Flavor experimentation and limited editions sustain consumer interest. While large players leverage scale and distribution, emerging brands compete through authenticity, functional claims, and targeted niche appeal, shaping a dynamic competitive environment.

Key Developments:

- In October 2025, Utz Brands, Inc. unveiled its latest flavor innovations and product extensions at the 2025 NACS Show, highlighting its focus on convenience-led snacking trends.

- In August 2025, Nature’s Path expanded its Que Pasa portfolio with the launch of Rolled Chips in Chile & Lime and Spicy Queso flavors.

- In July 2025, Decadent Crunch®, El Capitan Foods’ premium tortilla chip brand, debuted at the 2025 Summer Fancy Food Show.

Companies Covered in North America Healthy Snack Chips Market

- General Mills, Inc.

- BFY Brands

- Campbell Soup Company

- PepsiCo Inc.

- Utz Brands Inc.

- Hain Celestial Group Inc.

- El Capitan Foods

- Shearer's Foods

- Herr's Food, Inc.

- Snyder's-Lance, Inc.

- Others

Frequently Asked Questions

What is the expected North America Healthy Snack Chips Market size in 2026?

Rising consumer preference for clean-label and minimally processed snack drives the demand for North America Healthy Snack Chips Market.

The North America Healthy Snack Chips market is poised to witness a CAGR of 4.9% between 2026 and 2033

Collaboration with fitness and lifestyle brands for co-branded healthy snacks is the key market opportunity

Major players in the North America Healthy Snack Chips Market include General Mills, Inc., BFY Brands, Campbell Soup Company, PepsiCo Inc., Utz Brands Inc., Hain Celestial Group Inc., and others