- Specialty & Fine Chemicals

- Aviation Fuel Additives Market

Aviation Fuel Additives Market Size, Share, and Growth Forecast, 2025 - 2032

Aviation Fuel Additives Market By Additive Type (Static Dissipator, Antioxidants, Others), Fuel Type (Gasoline, Others), End-user (Cargo aircraft, Passenger Aircraft, Others), and Regional Analysis for 2025 - 2032

Aviation Fuel Additives Market Size and Trends Analysis

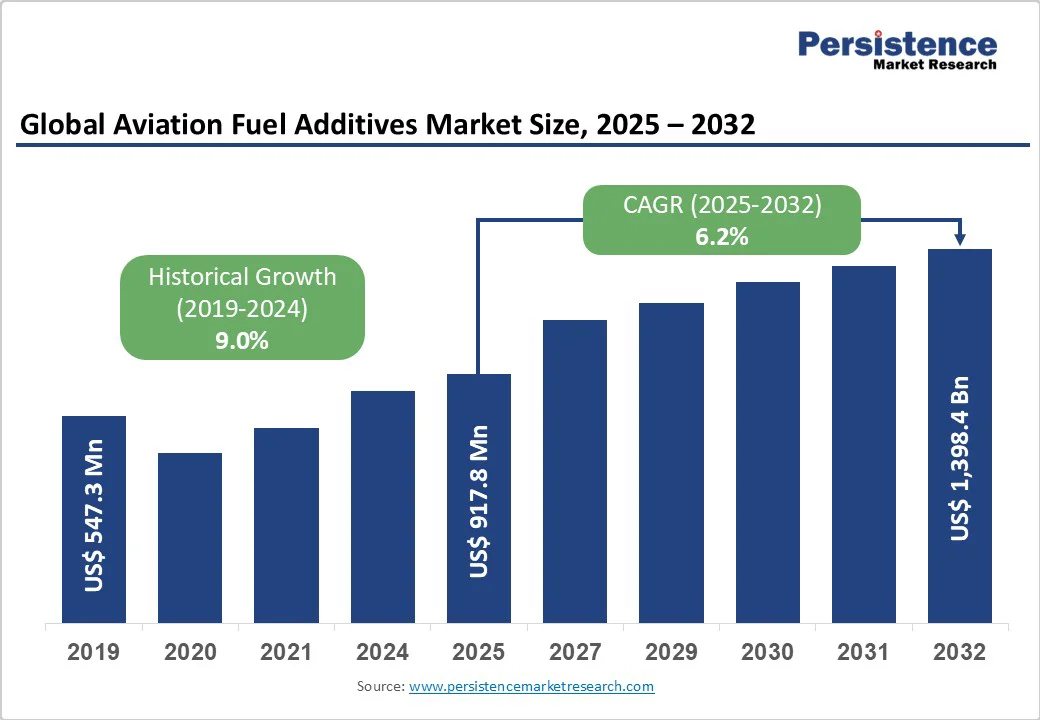

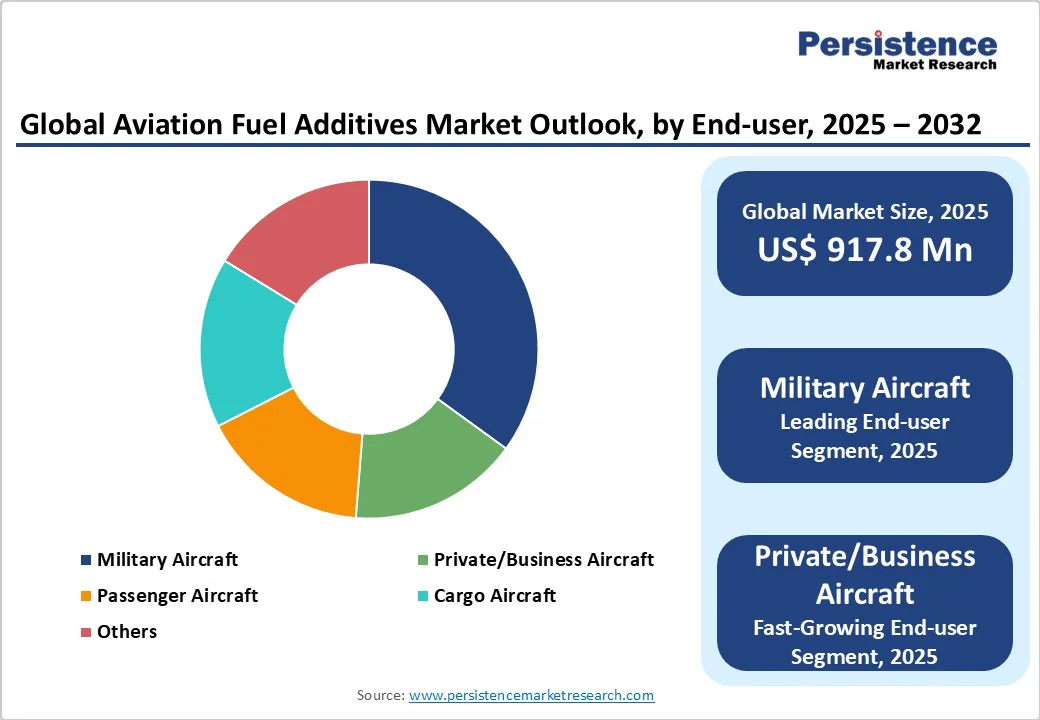

The global aviation fuel additives market size is likely to be valued at US$917.8 Million in 2025 and is expected to reach US$1,398.4 Million by 2032, growing at a CAGR of 6.2% during the forecast period from 2025 to 2032, driven by the increasing global air traffic, stringent environmental regulations, and the growing adoption of sustainable aviation fuels (SAF) requiring specialized additive packages.

The rising demand for fuel efficiency improvements and enhanced operational reliability across commercial, military, and general aviation sectors further accelerates market growth.

Key Industry Highlights

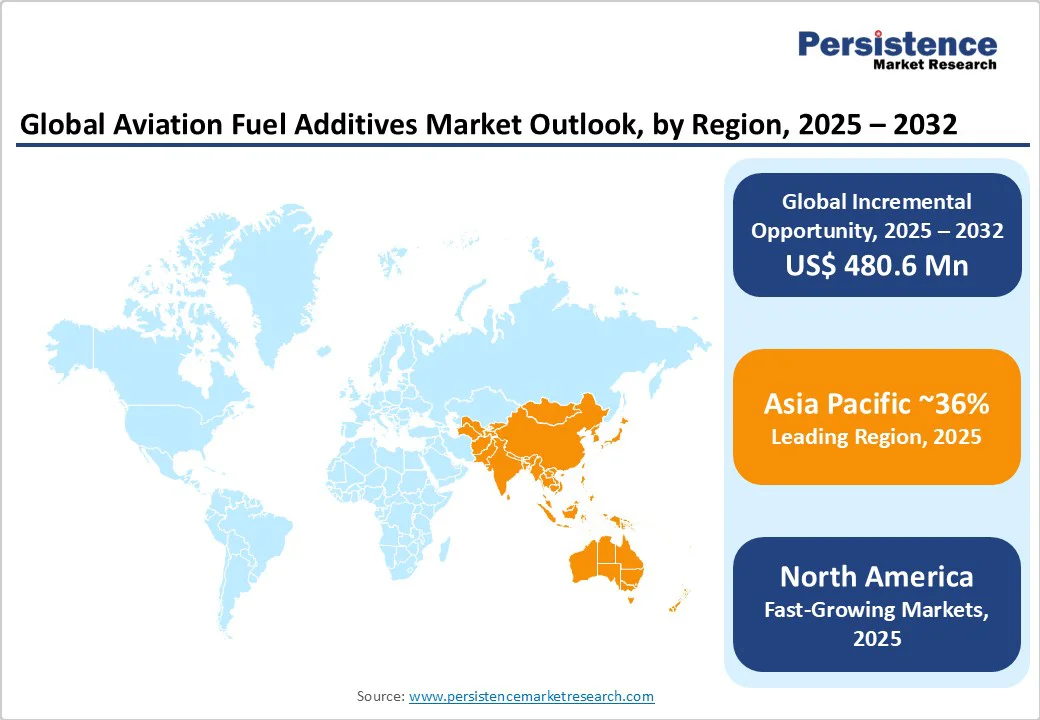

- Leading Region: Asia Pacific leads globally with 36% market share in 2025, driven by rapid aviation expansion across China, Japan, India, and ASEAN nations requiring substantial fuel additive volumes for commercial and military applications.

- Fastest Growing Region: North America emerges as the fastest-growing region with an 8.2% CAGR between 2025 and 2032, supported by fleet modernization programs, SAF mandates, and advanced regulatory frameworks driving premium additive adoption rates.

- Dominant Additive Type: Corrosion Inhibitors dominate with 48% value share, serving critical dual functions as lubricity improvers while protecting fuel system components across diverse operational environments and aircraft applications.

- Leading End-user: The military aircraft segment expands rapidly at 35% market share, requiring specialized additive packages for extreme operating conditions, enhanced thermal stability, and extended deployment cycle reliability requirements.

- Key Opportunity: Sustainable aviation fuel integration presents a key growth opportunity as SAF production scales from 600 million liters in 2023 to the projected 1.3 billion liters in 2024, requiring specialized bio-compatible additive development.

| Key Insights | Details |

|---|---|

| Aviation Fuel Additives Market Size (2025E) | US$917.8 Million |

| Market Value Forecast (2032F) | US$1,398.4 Million |

| Projected Growth CAGR (2025-2032) | 6.2% |

| Historical Market Growth (2019-2024) | 9.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expanding Military Aviation Operations and Fleet Modernization

The military aviation sector represents a significant growth driver for aviation fuel additives, with military aircraft applications commanding approximately 35% market share in 2025. Military jets require specialized fuel formulations capable of withstanding extreme operating conditions, including high-altitude operations, extended deployment cycles, and severe weather scenarios. JP-8 and JP-5 military fuel specifications mandate the inclusion of anti-icing additives, corrosion inhibitors, and static dissipator additives to ensure operational reliability.

The U.S. Air Force completed its conversion from JP-4 to JP-8 by 1995, while installations in Alaska continue utilizing JP-8 due to superior cold-weather performance characteristics. Enhanced thermal stability additives such as Spec-Aid 8Q462 increase JP-8’s thermal stability by 100°F, enabling improved engine performance in high-performance military aircraft without compromising fuel system integrity.

Sustainable Aviation Fuel Integration Requirements

The accelerating transition toward sustainable aviation fuels creates substantial demand for advanced additive packages designed specifically for bio-based and synthetic fuel formulations. SAF production reached 600 million liters in 2023, representing 0.2% of global jet fuel consumption, with projections indicating growth to 1.3 billion liters by 2024.

The U.K. Government’s SAF Mandate, effective January 1, 2025, requires 2% SAF blending initially, increasing to 10% by 2030 and 22% by 2040. These mandates necessitate specialized additive formulations addressing the distinct thermal and chemical properties of renewable feedstocks, including Hydro-processed Esters and Fatty Acids (HEFA), Fischer-Tropsch (FT) synthetic fuels, and alcohol-to-jet (ATJ) processes. Advanced additive packages ensure compatibility with existing engine systems while maintaining performance standards equivalent to conventional jet fuel.

Barrier Analysis - Volatile Crude Oil Price Fluctuations

Fluctuating crude oil prices create significant cost pressures affecting aviation fuel additive adoption rates across the industry. During periods of elevated oil prices, airlines implement aggressive cost-reduction strategies, including potential cutbacks on premium fuel additive usage to manage operational expenses.

This volatility disrupts demand predictability for additive manufacturers, making accurate production planning and inventory management challenging. The unpredictable nature of oil price movements, ranging from US$40 to US$120 per barrel over recent years, creates cyclical demand patterns that directly impact market stability and long-term investment decisions in additive technology development.

Stringent Regulatory Approval Processes

The aviation industry’s rigorous safety standards necessitate extensive testing and certification procedures for new fuel additive formulations, creating substantial barriers to market entry and innovation. FAA, EASA, and other international aviation authorities require comprehensive documentation demonstrating additive safety, performance characteristics, and compatibility with existing aircraft systems before approval.

These certification processes can extend two to five years and require significant financial investments exceeding US$10 Million for complex additive systems. The regulatory complexity increases for novel bio-based additives and advanced nanotechnology formulations, potentially delaying market introduction of innovative solutions addressing emerging industry needs.

Opportunity Analysis - Advanced Nanotechnology-Based Additive Development

The integration of nanotechnology presents transformative opportunities for developing next-generation aviation fuel additives with enhanced performance characteristics. Nanocatalyst technologies demonstrate superior thermal stability, improved combustion efficiency, and extended engine component protection compared to conventional additive formulations.

Recent research literatures indicate that nanotechnology-based additives can achieve 10-15% improvements in fuel efficiency while simultaneously reducing particulate emissions by 50-70%. Digital integration opportunities through IoT-enabled additive monitoring systems enable real-time dosing optimization and predictive maintenance strategies, creating value-added services for aviation customers. The growing adoption of digital fleet management systems provides platforms for integrating advanced additive monitoring capabilities, enabling airlines to optimize fuel performance while reducing the total cost of ownership.

Emerging Market Aviation Infrastructure Expansion

Rapid aviation sector growth in Asia Pacific and Latin American markets creates substantial opportunities for aviation fuel additive suppliers. China requires approximately 7,600 new commercial aircraft valued at US$1.2 Trillion over the next two decades, according to Boeing forecasts. The Asia-Pacific region maintains the largest market share at approximately 36% in 2025, with countries including India, Japan, and ASEAN nations demonstrating robust aviation growth rates.

North America emerges as the fastest-growing region with an 8.2% CAGR between 2025 and 2032, driven by fleet modernization initiatives and increasing focus on operational efficiency. The expansion of low-cost carrier operations and growing middle-class populations in emerging markets create sustained demand for cost-effective fuel additive solutions that enhance operational reliability while meeting international safety standards.

Category-wise Analysis

Additive Type Insights

Corrosion Inhibitors dominate the aviation fuel additives market with approximately 48% value share in 2025, establishing themselves as the leading segment due to their critical role in protecting fuel system components from degradation. These additives serve dual functions as Corrosion Inhibitor/Lubricity Improvers (CI/LI), enhancing fuel lubricity while preventing metal component corrosion throughout the fuel distribution system.

DCI-4A and DCI-6A represent industry-standard formulations approved for both civilian and military aviation applications, with DCI-6A preferred for pipeline applications due to superior corrosion protection at lower treatment rates ranging from 3-9 mg/l.

The extensive heritage and proven performance of corrosion inhibitors across diverse operating conditions, from sea-level operations to high-altitude military missions, solidifies their market leadership position within the aviation chemicals market ecosystem.

Fuel Type Insights

Jet Fuel maintains overwhelming market dominance with approximately 96% market share in 2025, reflecting its universal application across commercial, military, and general aviation sectors. Jet A-1 specification fuels power the majority of global commercial aircraft operations, requiring standardized additive packages including antioxidants, anti-icing agents, and static dissipator additives.

Military applications utilize enhanced formulations such as JP-8 containing mandatory corrosion inhibitors and Fuel System Icing Inhibitor (FSII) additives at concentrations of 0.10-0.15% by volume according to MIL-DTL-83133 specifications.

The segment’s dominance stems from jet fuel’s superior energy density 43.1 MJ/kg, operational safety characteristics, and compatibility with existing aircraft infrastructure compared to Aviation Gasoline alternatives primarily used in smaller piston-engine aircraft applications within the broader Sustainable Aviation Fuel Market transition.

End-user Insights

Military Aircraft applications represent the fastest-expanding segment with approximately 35% market share in 2025, driven by increasing defense expenditures and fleet modernization programs worldwide. Military aviation requires specialized additive packages addressing extreme operational requirements, including high-altitude performance, extended storage capabilities, and compatibility with combat environment conditions.

JP-8+100 formulations containing Spec-Aid 8Q462 additive improve thermal stability by 100°F compared to standard JP-8, enabling enhanced performance in high-performance fighter aircraft and tactical operations.

The segment benefits from predictable government procurement cycles, premium pricing acceptance for performance-critical applications, and continuous technology advancement requirements supporting next-generation military aircraft development programs requiring advanced fuel system protection within the expanding Expired Aviation Chemicals Market management protocols.

Regional Insights

North America Aviation Fuel Additives Trends

North America emerges as the fastest-growing regional market with an 8.2% CAGR between 2025 and 2032, driven by robust fleet modernization initiatives and stringent environmental compliance requirements. The U.S. maintains global leadership in aviation fuel additive innovation through advanced research and development programs conducted by the FAA and industry collaborations. Regulatory frameworks, including ASTM D1655 specifications for civilian jet fuels and MIL-DTL-83133 for military applications, establish comprehensive standards ensuring safety and performance consistency across diverse operational environments.

The region’s innovation ecosystem benefits from strong partnerships between additive manufacturers, aircraft OEMs, and research institutions developing next-generation formulations. Sustainable Aviation Fuel mandates implemented across major U.S. airports create substantial demand for bio-compatible additive packages supporting SAF integration requirements. The U.S. Department of Energy projects SAF production capacity reaching 3 billion gallons annually by 2030, necessitating specialized additive development for renewable feedstock compatibility and performance optimization.

Europe Aviation Fuel Additives Trends

European markets demonstrate strong regulatory harmonization through EASA certification requirements and European Union environmental mandates, driving advanced additive adoption. Germany, the U.K., France, and Spain lead regional demand through established aerospace manufacturing capabilities and comprehensive military aviation programs. DEF STAN 91-91 specifications for Jet A-1 and DEF STAN 91-87 for military fuels establish stringent quality standards requiring advanced additive formulations meeting performance and safety criteria.

The U.K.’s SAF Mandate, effective January 2025, requires 2% sustainable fuel blending, increasing to 22% by 2040, creating substantial market opportunities for bio-compatible additive systems. European aerospace manufacturers, including Airbus, collaborate with additive suppliers developing formulations optimized for next-generation engine technologies and alternative fuel integration. Regional initiatives supporting carbon-neutral aviation by 2050 accelerate investment in advanced additive technologies, reducing emissions while maintaining operational safety standards across commercial and military applications.

Asia Pacific Aviation Fuel Additives Trends

Asia Pacific maintains the largest regional market share at approximately 36% in 2025, supported by rapid aviation sector expansion across China, Japan, India, and ASEAN nations. China represents the largest fuel consumer in the region and second globally after the U.S., with Boeing projecting requirements for 7,600 new commercial aircraft valued at US$1.2 Trillion over the next two decades. The region’s manufacturing advantages and growing middle-class population drive sustained aviation growth, creating substantial additive demand.

The Japanese aerospace industry emphasizes technological innovation and quality standards requiring premium additive formulations for domestic and export applications. Indian aviation expansion, driven by economic growth and urbanization, creates emerging opportunities for cost-effective additive solutions meeting international safety standards. ASEAN nations, including Thailand, Singapore, and Malaysia, develop regional aviation hubs necessitating standardized fuel quality management systems incorporating advanced additive technologies supporting diverse aircraft operations and maintenance requirements.

Competitive Landscape

The aviation fuel additives market demonstrates moderate consolidation with established global players maintaining significant market share through technological expertise, regulatory approvals, and distribution capabilities. Market leaders, including BASF SE, Afton Chemical Corporation, and Innospec Chemical Company, leverage extensive product portfolios, research and development investments, and strategic partnerships with aircraft manufacturers and fuel suppliers.

Key differentiators include proprietary additive formulations, comprehensive regulatory approvals across multiple jurisdictions, and technical service capabilities supporting customer application requirements. Emerging business models focus on digital integration opportunities, including IoT-enabled monitoring systems and predictive analytics, enhancing additive performance optimization and customer value proposition development.

Key Industry Developments

- In March 2022, Afton Chemical expanded its Singapore facility with new Gasoline Performance Additives blending capabilities, the first in Asia Pacific, boosting its global network and supporting regional growth.

- In January 2025, the University of Illinois developed a sustainable aviation fuel additive, ethylbenzene, from recycled polystyrene. It lubricates fuel systems and seals, preventing leaks, offering a renewable aromatic source to boost sustainable aviation fuel use in commercial aircraft.

- In September 2025, BASF announced its next-generation Keropur Gasoline Performance Additive Series with Keropur AP 225-20. This new formulation meets the updated U.S. TOP TIER+™ standard, EPA’s Lowest Additive Concentration (LAC) requirements, and is seeking CARB approval. It will be available well before the mandatory January 2027 deadline.

Companies Covered in Aviation Fuel Additives Market

- BASF SE

- Dorf-Ketal Chemicals India Pvt. Ltd.

- Afton Chemical Corporation

- Shell Chemicals LP

- Hammonds Fuel Additives Inc.

- Innospec Chemical Company

- Prist Aerospace

- Meridian Fuels

- A S Harrison & Co Pty Limited

- TDS CHEMICAL CORP. LIMITED

- The Dow Chemical Company

- Nexeo Solutions

- Total S.A.

- BP Plc

Frequently Asked Questions

The global aviation fuel additives market is expected to grow from US$917.8 Million in 2025 to US$1,398.4 Million by 2032, with a compound annual growth rate (CAGR) of 6.2% during the forecast period.

Key demand drivers are rising global air traffic, strict environmental regulations, growing use of sustainable aviation fuels with specialized additives, military fleet upgrades, and the need for improved fuel efficiency and reliability in commercial and defense aviation.

Corrosion Inhibitors lead the market with approximately 48% value share in 2025, serving critical dual functions as lubricity improvers while protecting fuel system components from degradation across diverse operational environments and aircraft applications.

Asia Pacific holds the largest regional market share at around 36% in 2025, fueled by rapid aviation growth in China, Japan, India, and ASEAN, supported by rising middle-class populations and major infrastructure projects.

SAF integration offers the biggest growth potential, with production rising from 600 million liters in 2023 to 1.3 billion liters in 2024, driving demand for specialized bio-compatible additives to ensure renewable feedstock compatibility and optimal performance.

Major market players include BASF SE, Afton Chemical Corporation, Innospec Chemical Company, Shell Chemicals LP, Dorf-Ketal Chemicals India Pvt. Ltd., Prist Aerospace, Hammonds Fuel Additives Inc., and The Dow Chemical Company.