- Healthcare Services

- North America Toxicology Laboratories Market

North America Toxicology Laboratories Market Size, Share, and Growth Forecast, 2025 - 2032

North America Toxicology Laboratories Market By Specimen Type (Urine, Blood, Others), Analytical Method (Immunoassay-Based Testing, GC-MS, Others), Application (Clinical Toxicology, Forensic Toxicology, Workplace Drug Testing, Sports Drug Testing, Others), and Regional Analysis for 2025 - 2032

North America Toxicology Laboratories Market Share and Trends Analysis

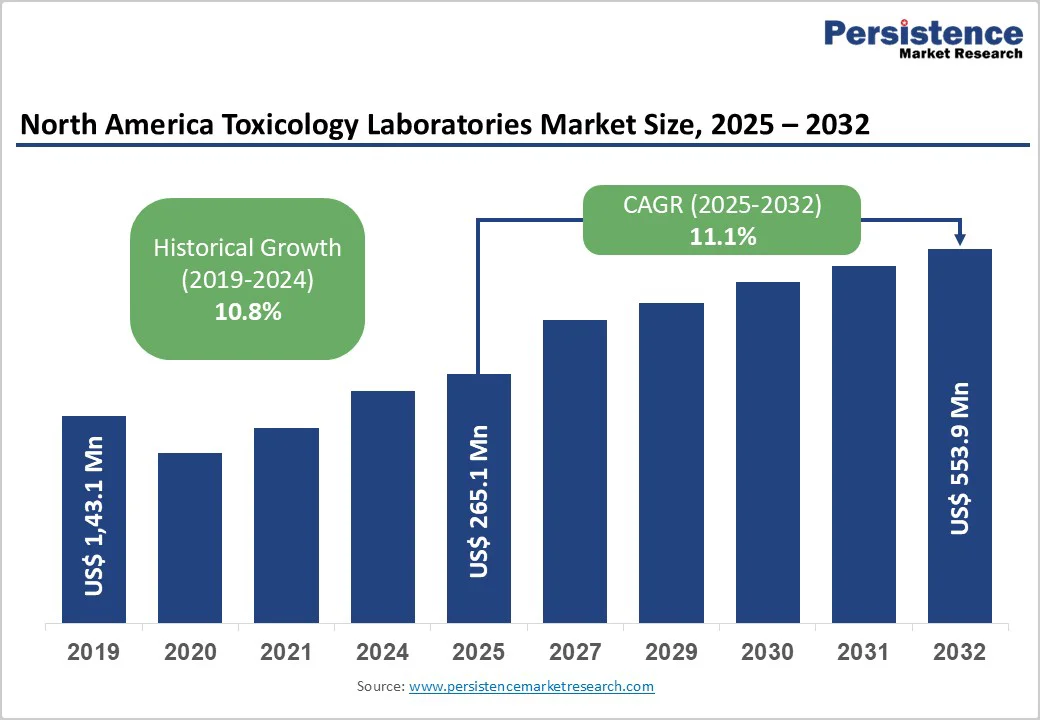

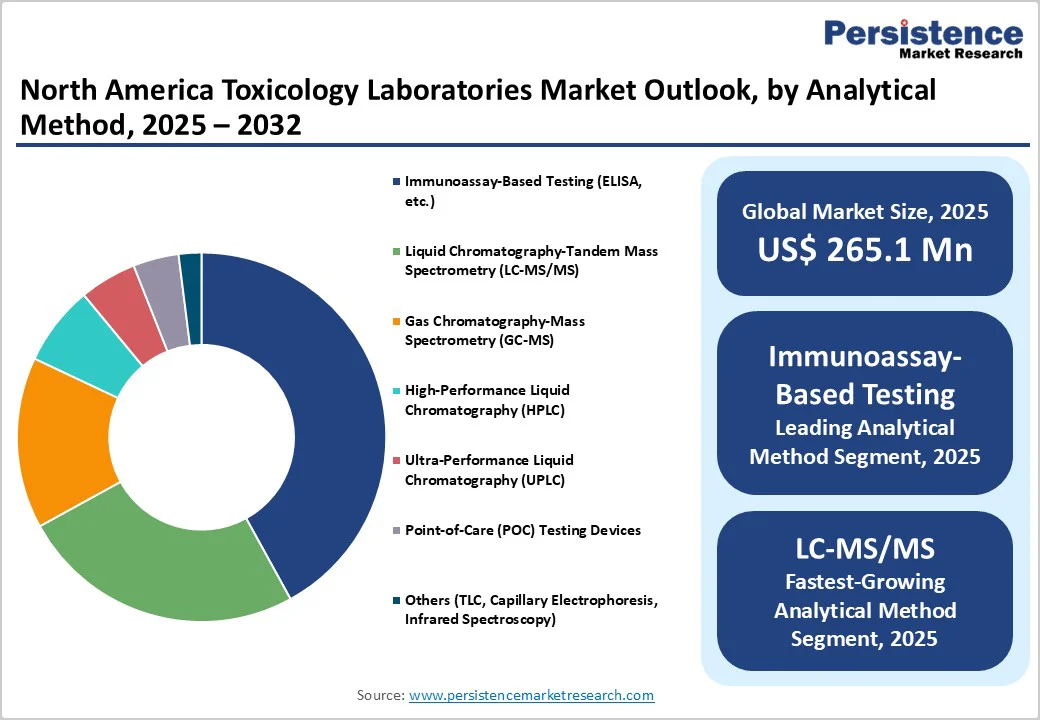

The North America toxicology laboratories market size is likely to be valued at US$265.1 Million in 2025, and is estimated to reach US$553.9 Million by 2032, growing at a CAGR of 11.1% during the forecast period 2025−2032, driven by the escalating demand for toxicology testing solutions across clinical, forensic, and workplace settings.

This growth is further driven by rising substance abuse rates, stricter regulatory requirements, advancements in analytical technologies, and the expanding use of personalized medicine, with increasing investments in opioid monitoring, precision toxicology, and emerging neonatal testing, broadening the market scope.

Key Industry Highlights

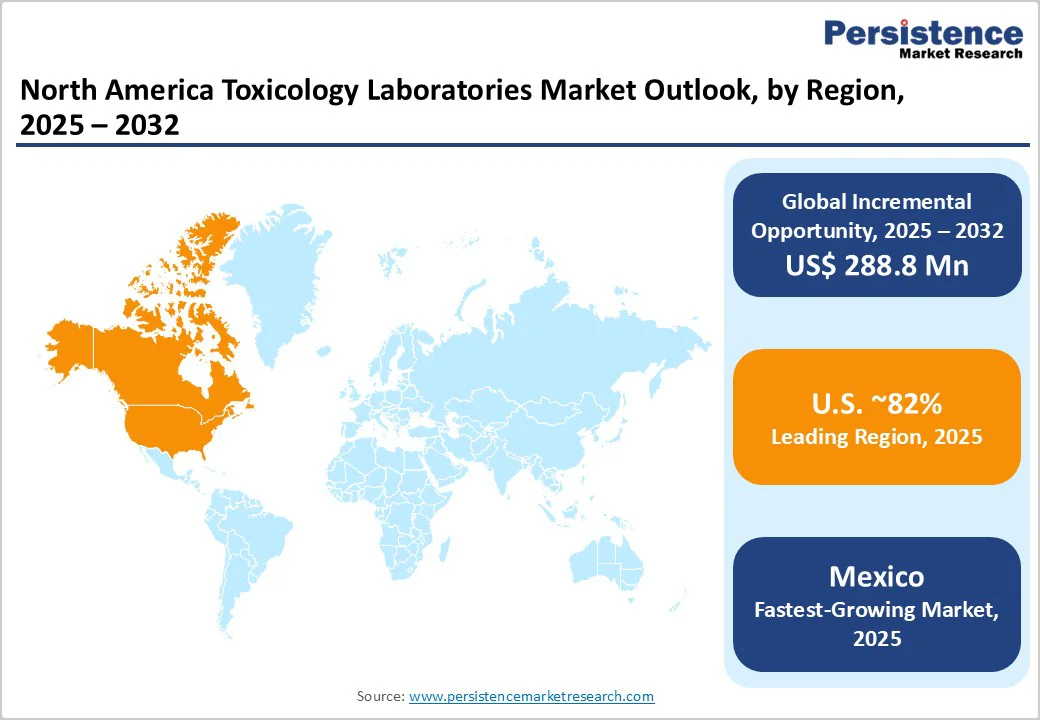

- Country-level Dynamics: The U.S. commands 82% market share in 2025, propelled by regulatory rigor and public health initiatives, while the Canadian toxicology laboratories market benefits from harmonized regulations and infrastructure investments.

- Fastest-growing Market: The market in Mexico is projected to display the highest 2025-2032 CAGR of 13.8%, driven by industrial growth, healthcare expansion, and cost advantages.

- Dominant Specimen Types: Urine specimen testing dominates the market with a 48% share in 2025, whereas oral fluid testing is the fastest-growing segment through 2032.

- Leading Analytical Methods: Immunoassay, especially ELISA, leads in 2025 with a 42% share, with LC-MS/MS techniques soaring at the highest CAGR between 2025 and 2032.

- Application Leadership: Workplace drug testing accounts for 40% of market applications in 2025, while neonatal and maternal toxicology is the highest growth application segment for 2025-2032.

- Player Strategies: Strategic moves by key players include LC-MS/MS platform launches, acquisition of neonatal laboratories, and partnerships for point-of-care (POC) toxicology technologies, pioneering innovation, and market consolidation.

- April 2025: Premier Biotech expanded its oral fluid toxicology testing leadership by acquiring OraSure Technologies' substance abuse testing business and Green Earth Biomedical’s Mexican subsidiary, enhancing its product offerings and accelerating international growth in challenging markets.

| Key Insights | Details |

|---|---|

|

North America Toxicology Laboratories Market Size (2025E) |

US$265.1 Mn |

|

Market Value Forecast (2032F) |

US$553.9 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

11.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Opioid Crisis and Advanced Therapeutic Drug Monitoring

The ongoing opioid crisis remains a critical driver for the North America toxicology laboratories market growth. In 2023, approximately 105,000 people died from drug overdoses in the U.S., and nearly 80,000 of those deaths involved opioids, according to data from the Centers for Disease Control and Prevention (CDC). Therapeutic drug monitoring (TDM) for opioids and other controlled substances has become essential to optimize dosing, mitigate abuse risk, and improve patient outcomes.

Sophisticated mass spectrometry technologies, such as liquid chromatography-tandem mass spectrometry LC-MS/MS, enable highly sensitive and specific quantification of opioids and metabolites in biological specimens. The U.S. federal regulatory landscape, including the Substance Abuse and Mental Health Services Administration (SAMHSA) and DEA guidelines, mandates stringent drug screening and monitoring protocols, catalyzing demand for toxicology services in hospitals, pain clinics, and forensic labs.

High Analytical Instrumentation Costs and Regulatory Complexity

The market faces structural roadblocks stemming principally from the high capital expenditure associated with the acquisition and maintenance of advanced analytical instrumentation, notably LC-MS/MS and gas chromatography-mass spectrometry (GC-MS) systems. These instruments often require initial investments exceeding US$500,000, with ongoing operational and regulatory compliance costs intensifying financial pressure, especially for smaller laboratories.

The complex regulatory environment, including CLIA certification, CAP accreditation, and evolving federal and state mandates, can also impose barriers to market entry and expansion. Supply chain disruptions for specialized reagents and consumables have occasionally impeded continuous testing workflows, leading to potential revenue volatility and delayed turnaround times.

Growth of Neonatal and Maternal Toxicology Screening

Emerging public health initiatives are driving substantial opportunities in neonatal and maternal toxicology screening. Rising awareness of prenatal substance exposure implications is fueling demand for in-depth toxicology testing of meconium, umbilical cord tissue, and maternal biological samples. The growth of neonatal toxicology is being propelled by enhanced screening programs supported by healthcare payers and government funding, coupled with technological advancements enabling earlier and more accurate exposure detection.

The early identification of substance exposure reduces neonatal abstinence syndrome (NAS) incidence and associated healthcare costs, incentivizing hospital systems to integrate comprehensive toxicology panels. Market estimates value the neonatal toxicology opportunity at US$80 Million by 2032 within North America, marking it as a strategically lucrative area for testing service providers and diagnostic reagent manufacturers.

Category-wise Analysis

Specimen Type Insights

Urine specimen testing is set to hold a commanding position in 2025, estimated at approximately 48% of the North America toxicology laboratories market revenue share. Its dominance stems primarily from its established use in workplace drug testing programs, clinical toxicology, and forensic settings, due to the non-invasive nature of collection, cost efficiency, and wide acceptance by regulatory authorities such as SAMHSA and the Department of Transportation. Urine testing protocols cover most substances of abuse, including opioids, cannabinoids, amphetamines, and benzodiazepines, offering detection windows suitable for recent substance use monitoring. Urine testing infrastructure gains additional benefits from mature supply chains and analytical workflows, supporting high-volume screening and confirmatory testing.

Oral fluid testing is growing at the fastest rate between 2025 and 2032. The growth is driven by increasing adoption in roadside drug screening, workplace testing requiring non-invasive and on-site methods, and clinical settings emphasizing reduced sample adulteration. Advances in portable collection devices and improved analytical sensitivity using LC-MS/MS enable rapid and reliable detection of recent drug use. Regulatory bodies are increasingly accepting oral fluid for various testing indications owing to its ease of administration compared to urine and blood.

Analytical Method Insights

Immunoassay testing, particularly enzyme-linked immunosorbent assay (ELISA), accounts for around 42% of the market share in 2025. Its widespread adoption is due to rapid throughput, cost-effectiveness, and suitability for initial drug screening. ELISA assays provide sensitive detection of a wide range of analytes and are configured for both qualitative and quantitative applications. In workplace testing environments and hospital toxicology laboratories, ELISA remains the backbone of preliminary testing, with results informing confirmatory procedures. Integrated automated immunoassay analyzers enable laboratory workflows to efficiently manage high specimen volumes, maintaining the market lead of ELISA.

LC-MS/MS is identified as the fastest-growing technology during 2025–2032. This growth is attributed to the superior specificity and multiplexing capabilities of LC-MS/MS, allowing simultaneous detection of multiple drugs and metabolites, including emerging substances of abuse and novel psychoactive compounds. Laboratories are transitioning from GC-MS to LC-MS/MS due to reduced sample preparation times and enhanced analytical sensitivity. Regulatory emphasis on confirmatory testing and personalized medicine applications further drives LC-MS/MS adoption. Innovations in miniaturized and portable LC-MS/MS instruments portend broader accessibility and cost reductions, fueling growth.

Application Insights

Workplace drug testing dominates the application landscape with a 40% revenue share in 2025. Its leadership is anchored in U.S. federal and state regulatory mandates requiring pre-employment, random, post-accident, reasonable suspicion, and return-to-duty drug testing protocols. The expansion of industries implementing stringent drug-free workplace policies, combined with heightened employer awareness of productivity and safety benefits, sustains the market primacy of this segment. The segment’s high testing volume and recurring nature have also created stable revenue bases for laboratories.

Neonatal and maternal toxicology represent the fastest-expanding application through 2032. Public health initiatives targeting early detection of prenatal and neonatal drug exposure underpin this growth. Comprehensive toxicology panels on meconium, umbilical cord tissue, and maternal biological samples enable healthcare providers to mitigate neonatal abstinence syndrome risks. Reimbursement support and increasing screening mandates across states contribute to escalating adoption. Growth in this segment offers laboratories a lucrative expansion avenue aligned with evolving maternal and neonatal care standards.

Country Insights

U.S. Toxicology Laboratories Market Trends

The U.S. holds an estimated 82% of the North America toxicology laboratories market share in 2025, and is forecast to sustain a high CAGR through 2032. This market dominance is supported by comprehensive regulatory frameworks, including CLIA certification requirements, SAMHSA drug testing guidelines, and DEA-mandated monitoring programs for controlled substances. The U.S. innovation ecosystem fosters rapid adoption of advanced analytical technologies such as LC-MS/MS, alongside investments in point-of-care testing and pharmacogenomics integration.

The opioid epidemic continues to catalyze the demand for sophisticated toxicology services in pain management clinics, forensic labs, and hospitals in the country. Competitive intensity remains high among established laboratory networks such as Laboratory Corporation of America Holdings (LabCorp) and Quest Diagnostics, leading technology adoption cycles and forming strategic partnerships to expand neonatal toxicology and forensic testing capabilities. Expansion opportunities stem from increasing telehealth integration, fostering decentralized sample collection, and remote testing models.

Canada Toxicology Laboratories Market Trends

Canada comprises about 12% of the regional market from 2025 to 2032. This accelerated growth aligns with federal and provincial initiatives, emphasizing workplace safety, forensic case backlog reduction, and harmonization with U.S. regulatory standards. Centralized laboratory systems throughout provinces foster efficiency and standardized quality, improving testing accessibility.

Investments are also being directed towards enhancing forensic toxicology infrastructure and augmenting neonatal screening programs. The competitive landscape features both established national chains and innovative startups focusing on pharmacogenomic testing and rapid immunoassay platforms. Opportunities exist in expanding rural access through mobile laboratory services and leveraging government funding for public health toxicology initiatives.

Mexico Toxicology Laboratories Market Trends

Mexico is the smallest but fastest-growing market within North America during 2025-2032, driven by economic expansion, healthcare infrastructure development, and industrial sector demands for comprehensive workplace drug testing. Regulatory improvements aligning Mexican standards with international best practices, coupled with cost advantages in manufacturing reagents and consumables, attract foreign investment and partnerships.

Emerging contract research organizations (CROs) augment pharmacovigilance and clinical trial toxicology testing. The market remains fragmented, offering significant opportunities for new entrants providing tailored toxicology panels and cost-effective analytical solutions targeted towards Mexico's expanding pharmaceutical and manufacturing sectors.

Competitive Landscape

The North America toxicology laboratories market structure exhibits moderate consolidation, with a few leading entities controlling approximately 60% of the market share. The key players, such as LabCorp, Quest Diagnostics, Eurofins Scientific, and Sonic Healthcare, leverage extensive geographic coverage, integrated service portfolios, and significant investments in state-of-the-art analytical platforms. Smaller laboratories and specialized CROs occupy niche segments including forensic toxicology, neonatal testing, and personalized medicine.

The market fosters competition through innovation, scale economies, and diversified test menus, while regulatory adherence and accreditation status significantly influence client trust and contract acquisition. Emerging boutique laboratories focus on technological agility and specialized testing panels, adding complexity but enhancing market dynamism.

Key Industry Developments

- In September 2025, Guardant Health and Quest Diagnostics partnered to expand access to Shield™, the first FDA-approved blood-based colorectal cancer screening test for average-risk adults 45+. Leveraging Quest’s nationwide network for ordering and blood draws, the collaboration aims to boost screening compliance among over 50 million eligible adults. Shield is covered by Medicare and Veterans Affairs, supporting broader adoption.

- In July 2025, RetinalGenix Technologies partnered with LabCorp to advance its DNA/RNA/GPS Pharmaco-Genetic Mapping platform, integrating genetic testing with high-resolution retinal imaging for early detection of ocular and systemic diseases. Patients can anonymously submit samples at LabCorp sites, supporting privacy and accessibility. The collaboration seeks CPT codes and plans expanded imaging services to enhance screening efficiency and coverage.

- In January 2025, United States Drug Testing Laboratories Inc. (USDTL) was acquired by Northlane Capital Partners to strengthen its advanced forensic toxicology capabilities and expand its customer base. Based in Des Plaines, Illinois, USDTL serves over 1,000 healthcare, court, and employer clients with 160+ employees, supporting continued growth and innovation.

Companies Covered in North America Toxicology Laboratories Market

- Laboratory Corporation of America Holdings (LabCorp)

- Quest Diagnostics Incorporated

- Eurofins Scientific SE

- Sonic Healthcare Limited

- Thermo Fisher Scientific Inc.

- Abbott Laboratories

- Alere Inc. (Now part of Abbott)

- Charles River Laboratories International, Inc.

- Bio-Techne Corporation

- Hologic, Inc.

- SGS SA

- PPD, Inc.

- ICON plc

- Syneos Health, Inc.

- Siemens Healthineers AG

Frequently Asked Questions

The North America toxicology laboratories market is projected to reach US$265.1 Million in 2025.

Widespread prevalence of substance abuse, stringent regulatory mandates, and advances in analytical technologies in the region are driving the market.

The North America toxicology laboratories market is poised to witness a CAGR of 11.1% from 2025 to 2032.

Growing adoption of personalized medicine and increased investments in opioid monitoring, precision toxicology, and emerging neonatal testing technologies are key market opportunities.

Laboratory Corporation of America Holdings (LabCorp), Quest Diagnostics Incorporated, and Eurofins Scientific SE are some of the key players in the market.