- Nutraceuticals & Functional Foods

- North America and Europe Table Eggs Market

North America and Europe Table Eggs Market Size, Share, and Growth Forecast 2026 – 2033

North America and Europe Table Eggs Market by Product Type (Regular Eggs, Specialty Eggs), by Packaging Type (Cartons, Transparent Containers, Trays, Bulk Packaging, Organic Packaging), by Distribution Channel (Supermarkets/Hypermarkets, Grocery Stores, Others), Application (Households, Foodservice Industry, Food Manufacturers, Bakery and Confectionery, Catering Services), and Regional Analysis, 2026–2033

North America and Europe Table Eggs Market Size and Trend Analysis

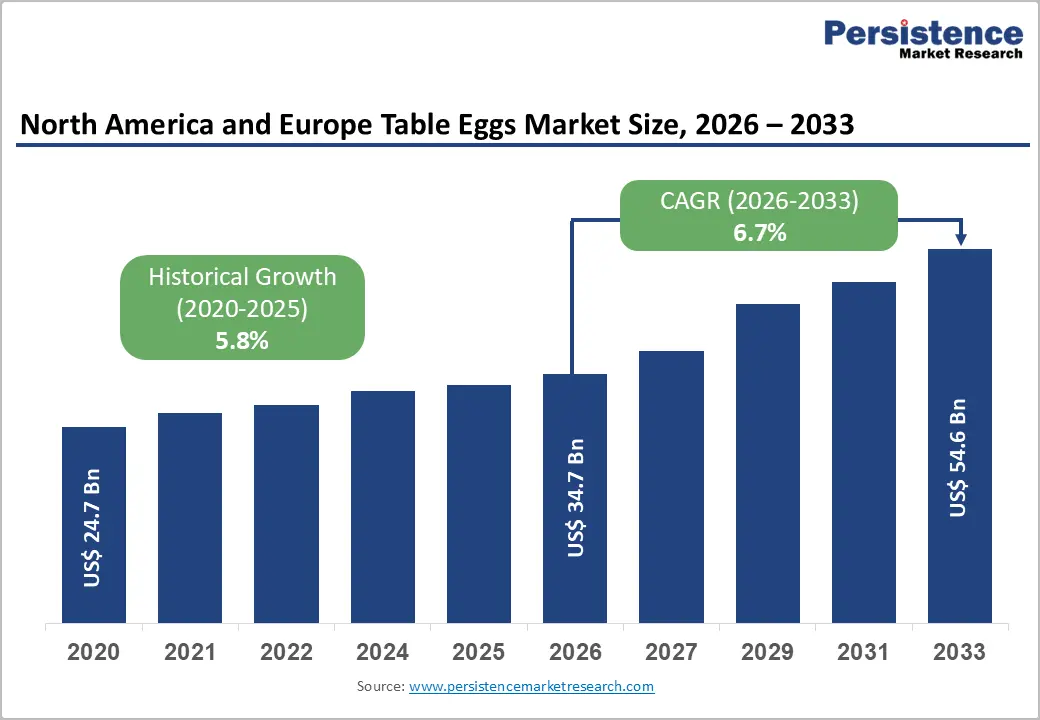

The table eggs market size is expected to be valued at US$ 34.7 billion in 2026 and projected to reach US$ 54.6 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

The North America and Europe table eggs market is experiencing robust growth, propelled by converging forces of nutritional awareness, animal welfare policy evolution, and the premiumization of egg products. Eggs are universally recognized as one of the most affordable and nutritionally complete protein sources available to consumers, a positioning reinforced by the U.S. Department of Agriculture (USDA) and European Food Safety Authority (EFSA), both of which include eggs as a key dietary protein recommendation. The accelerating structural shift from conventional cage-based to free-range, organic, and pasture-raised production, driven by landmark EU animal welfare directives and U.S. retailer cage-free pledges, is simultaneously expanding the specialty eggs category and elevating average selling prices, supporting strong value-based market growth through 2033.

Key Market Highlights

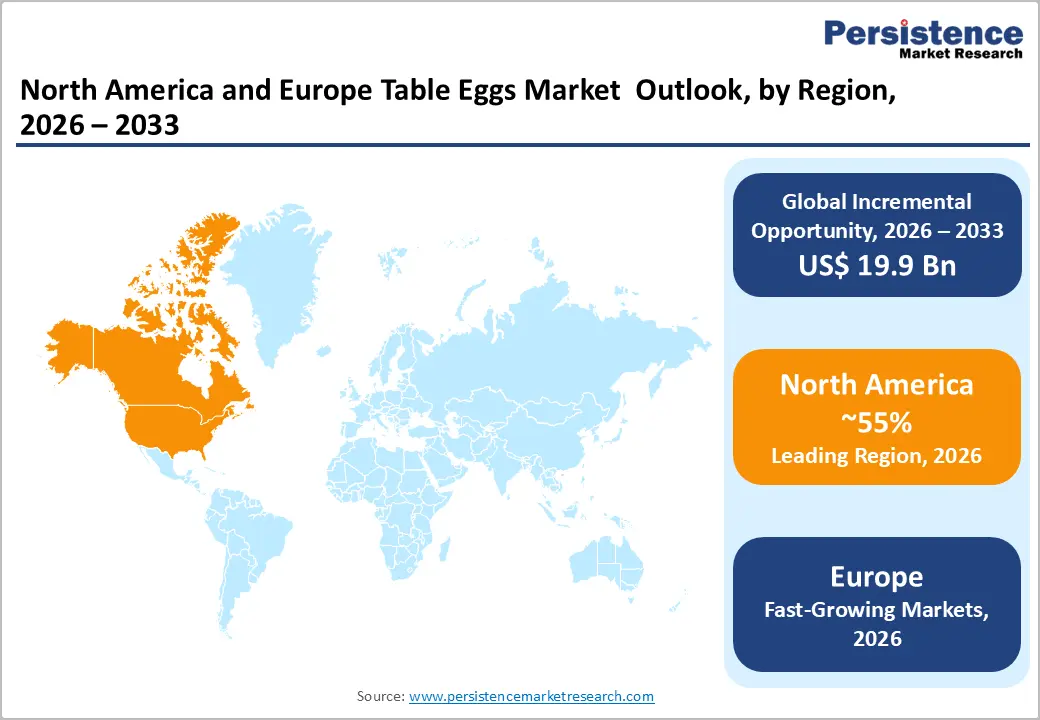

- Regional Leadership: North America leads the table eggs market with approximately 55% of market share in 2025, driven by the U.S.'s large-scale production infrastructure, ongoing cage-free transition mandated by California's Proposition 12, and strong specialty egg retail demand.

- Fast-Growing Market: Europe is the fastest growing regional market over 2026–2033, powered by the EU Farm to Fork Strategy, proposed strengthening of animal welfare legislation, and rapidly growing consumer demand for organic, free-range, and pasture-raised specialty egg formats across major markets.

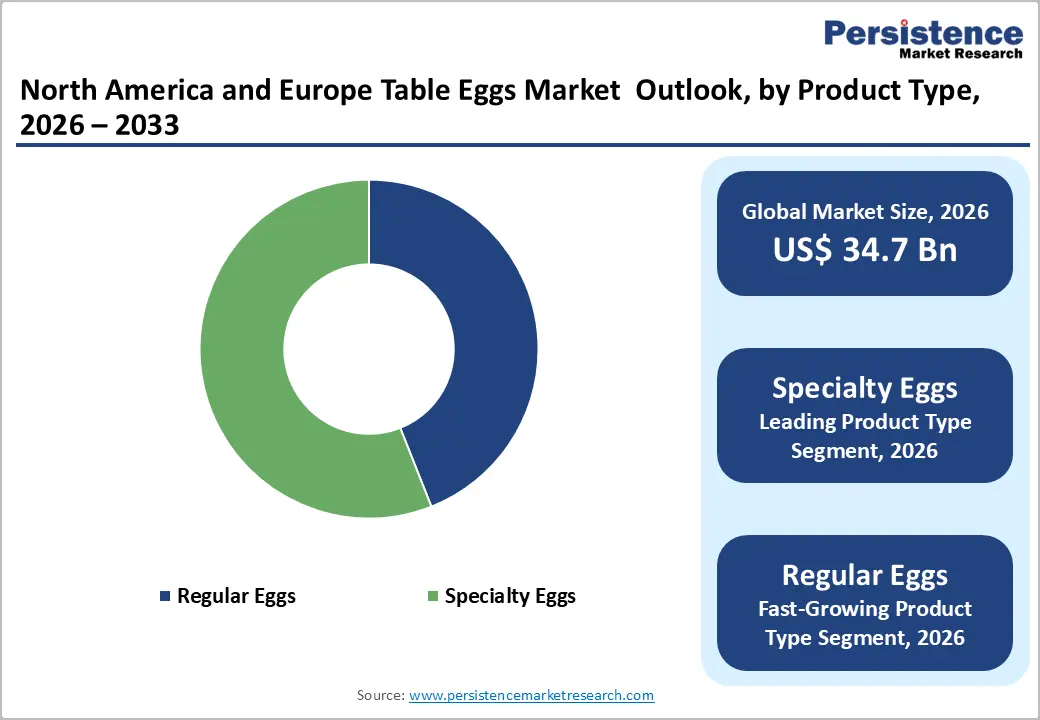

- Dominant Product: Specialty eggs lead the product type category with approximately 56% market share in 2025, underpinned by the EU battery cage ban, U.S. cage-free retailer commitments, and sustained consumer premiumization driving free-range, organic, and pasture-raised egg adoption.

- Fastest Growing Product: The foodservice industry is the fastest growing end-use application over 2026–2033, driven by post-pandemic recovery in restaurant and hospitality sector egg procurement and expanding breakfast-centric foodservice menus across North America and Europe.

- Opportunity: Expanding certified specialty egg portfolios including pasture-raised, omega-3 enriched, and RSPCA Assured or American Humane Certified variants offers producers premium pricing opportunities of 30–70% above conventional egg pricing in mainstream retail channels.

Market Dynamics

Drivers - Transition to Cage-Free and Specialty Egg Production Elevating Market Value

One of the most consequential structural shifts reshaping the North America and Europe table eggs market is the large-scale, policy-mandated, and retailer-driven transition away from conventional battery cage production toward cage-free, free-range, and organic systems. In the European Union, the ban on conventional battery cages has been in force since January 2012 under EU Council Directive 1999/74/EC, fundamentally restructuring European egg production economics and elevating the baseline quality standard.

In the United States, over 200 major food retailers and foodservice operators including McDonald's, Walmart, and Costco, have made binding cage-free sourcing commitments, compelling producers to invest in welfare-compliant housing. According to the United Egg Producers (UEP), the U.S. cage-free flock share has increased substantially year-over-year, with cage-free eggs commanding significant retail price premiums over conventional counterparts, materially elevating overall market value.

Restraints - Highly Pathogenic Avian Influenza (HPAI) Outbreaks Disrupting Supply and Inflating Prices

Avian influenza outbreaks represent the single most acute and unpredictable supply-side risk for the table eggs market in both North America and Europe. The 2022–2023 HPAI outbreak in the United States, the largest in U.S. history per the U.S. Centers for Disease Control and Prevention (CDC) and USDA APHIS, resulted in the culling of over 58 million birds, causing severe supply shortages and retail egg price spikes exceeding 60% year-over-year. Similar HPAI waves across France, the Netherlands, and the United Kingdom have imposed comparable disruptions on European egg supply chains, creating sustained consumer price volatility and undermining purchasing power-driven demand among price-sensitive household segments.

Opportunities - Expanding Specialty Eggs Portfolio to Capture Premium Consumer Segments

Specialty eggs encompassing free-range, pasture-raised, organic, omega-3 enriched, and heritage breed variants represent the dominant and fastest-innovating segment within the table eggs category, offering producers a compelling premium pricing opportunity. According to the Organic Trade Association (OTA), U.S. organic egg sales grew by over 10% in 2022, significantly outpacing conventional egg category growth.

In Europe, pasture-raised eggs are increasingly sought by premium retail buyers and sustainability-conscious consumers aligned with EU Farm to Fork Strategy objectives promoting higher animal welfare standards. Producers investing in certified welfare and sustainability labeling such as RSPCA Assured in the U.K. or American Humane Certified in the U.S. can build strong brand equity, command retail price premiums of 30–70% over conventional eggs, and access exclusive distribution agreements with premium grocery chains.

Category-wise Analysis

Product Type Insights

Specialty eggs hold the leading position in the North America and Europe table eggs market by product type, accounting for approximately 56% of total share in 2025. The segment's dominance reflects the accelerating transition of consumer preference toward eggs produced that is directed at better welfare, sustainability and nutritionally enhanced conditions. The implementation of the EU battery cage ban and widespread U.S. retailer cage-free commitments have embedded specialty egg consumption at a mainstream retail level, removing the "niche premium" barrier that historically constrained the segment's volume.

The United Egg Producers (UEP) projects that cage-free eggs will represent the majority of U.S. production by the late 2020s. Regular conventional eggs, while declining in share, remain important in price-sensitive distribution channels and bulk institutional procurement, and are identified as the fast-growing segment in absolute volume terms in emerging export markets.

Packaging Type Insights

Cartons are the dominant packaging format in the North America and Europe table eggs market, accounting for approximately 52% of total packaging share in 2025. Carton packaging available in molded pulp (recycled paper), plastic, and foam variants offers superior egg protection during retail handling, clear branding space for premium specialty egg labeling, and strong consumer familiarity across supermarket and grocery channels. The rapid growth of sustainability-focused purchasing behavior has significantly boosted demand for recycled molded pulp cartons in particular, as producers align packaging formats with broader environmental commitments. The Sustainable Packaging Coalition (SPC) notes that fiber-based egg cartons are among the most widely recycled packaging formats in North American retail. Organic packaging is emerging as the fastest growing sub-segment, driven by premium organic and pasture-raised egg producers seeking packaging that communicates product provenance and environmental credentials to premium consumers.

Regional Insights

U.S. Table Eggs Market Trends and Insights

The U.S. dominates the combined North America and Europe table eggs market due to its unmatched production scale, industrialized poultry system, and high domestic consumption base. According to USDA Egg Markets Overview, the U.S. produces over 90–92 billion eggs annually, making it one of the world’s largest producers. This scale is supported by vertically integrated firms, advanced automation in layer farming, and highly efficient feed-to-egg conversion systems. Per capita consumption remains strong at around 280–285 eggs per year, driven by widespread inclusion of eggs in breakfast foods, bakery, and foodservice sectors. The U.S. also benefits from strong cold-chain logistics and biosecurity systems that stabilize supply even during disease outbreaks such as avian influenza.

Compared to Europe, where production is fragmented across multiple countries (Germany, France, Spain, Netherlands), the U.S. has consolidated production hubs that improve cost efficiency and output consistency. Additionally, USDA data indicates strong growth in specialty eggs (cage-free and organic), further expanding market value. These structural advantages allow the U.S. to dominate overall volume, pricing influence, and supply leadership in the combined North America–Europe egg market structure.

Germany Table Eggs Market Trends and Insights

Germany plays a critical role in the Europe table eggs market due to its large consumer base, high regulatory standards, and strong demand for value-added egg products. According to Eurostat agricultural production data, Germany is among the top egg-producing countries in the European Union, contributing a significant share of the EU’s ~6.5 million tonnes annual egg output. Domestic consumption is also high, supported by a population exceeding 83 million and strong dietary integration of eggs in bakery, processed foods, and breakfast consumption patterns.

A key factor driving Germany’s importance is its strict animal welfare legislation. Government regulations have accelerated the transition from conventional cage systems to barn, free-range, and organic production systems. As a result, Germany has one of the highest shares of cage-free and organic eggs in Europe, increasing its influence in the premium segment. Additionally, Germany has a highly developed food processing industry, particularly in baked goods, noodles, and confectionery, all of which are egg-intensive industries.

Despite stable production, Germany often relies on imports during peak demand periods, reflecting its high consumption intensity. This combination of large demand, premium product shift, and regulatory leadership makes Germany a structurally important and influential market within the Europe table eggs industry.

France Table Eggs Market Trends and Insights

France is currently the fastest-growing market in the North America and Europe table eggs segment, driven by rising consumption, affordability pressures, and supply-demand imbalance. According to data from FranceAgriMer and the French egg industry committee (CNPO), national egg consumption reached approximately 237 eggs per capita in 2025, one of the highest levels in Europe and continuing to rise annually. This growth is largely attributed to eggs being a low-cost, high-protein substitute during periods of inflation, when consumers reduce meat and dairy intake.

French production stands at around 14–15 billion eggs annually, but demand growth has increasingly outpaced domestic supply. This has resulted in a measurable rise in imports, which increased by over 20% in recent years, according to French customs and agricultural trade statistics. The hospitality sector, bakery industry, and retail consumption all contribute to sustained demand expansion. Additionally, government and industry initiatives have supported modernization of poultry housing systems, improving production efficiency and encouraging capacity expansion.

France is also experiencing structural dietary shifts toward protein-rich, affordable foods, further strengthening egg consumption. Combined with supply constraints and strong consumer demand, these factors position France as the fastest-growing market in the region.

Competitive Landscape

The North America and Europe table eggs market is moderately consolidated at the production level, with a handful of large integrated producers including Cal-Maine Foods, Rose Acre Farms, and Hillandale Farms in North America, and Noble Foods, DANISH AGRO, and OVOSTAR UNION in Europe commanding significant regional market shares. Key competitive differentiators include animal welfare certification, specialty egg portfolio breadth, supply chain traceability, and retailer partnership depth. Investment in cage-free housing conversion, biosecurity infrastructure against HPAI, and sustainability certification is shaping the competitive landscape. Direct farm-to-retailer supply models and private-label egg production partnerships with major grocery chains are dominant emerging business model trends.

Key Developments

- June, 2024: Cal-Maine Foods, Inc. completed the acquisition of egg production assets of ISE America, Inc., strengthening its position in the U.S. table eggs market. The transaction expanded Cal-Maine’s production capacity and reinforced its integrated supply chain, allowing the company to better meet rising domestic demand for shell eggs and specialty egg products.

- 2024: Saudi Arabia’s table egg production surpassed 8 billion eggs in 2024, marking a significant milestone in the country’s food security and poultry sector expansion. The increase was driven by rising domestic demand, supported by population growth, higher protein consumption, and government efforts to enhance self-sufficiency in essential food commodities. The poultry industry also benefited from improved production efficiency, investment in large-scale layer farming, and adoption of modern biosecurity practices that reduced mortality and boosted output.

Companies Covered in North America and Europe Table Eggs Market

- Cal-Maine Foods

- Rose Acre Farms, Inc.

- HUEVOS GUILLÉN S.L

- Hillandale Farms

- OVOSTAR UNION PUBLIC COMPANY LIMITED

- Noble Foods

- MPS EGG FARMS

- Rujamar GRUPO AVICOLA

- DANISH AGRO

- Others

Frequently Asked Questions

The North America and Europe table eggs market with primary focus on North America and Europe is expected to be valued at US$ 34.7 billion in 2026

High protein demand, affordability, rising population, health awareness, processed food growth, and convenience consumption trends

North America leads the table eggs market with approximately 55% of total market share in 2025. The U.S. market is the primary driver, supported by its position as the world's second-largest egg producer, landmark cage-free legislation, and robust specialty egg retail infrastructure anchored by major grocery chains nationwide.

Growing specialty eggs demand, organic trends, emerging markets expansion, foodservice growth, and packaging innovations.

Cal-Maine Foods, Rose Acre Farms, Inc., HUEVOS GUILLÉN S.L, Hillandale Farms, OVOSTAR UNION PUBLIC COMPANY LIMITED, Noble Foods.