- Smart Packaging

- Medical Devices Packaging Market

Medical Devices Packaging Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Medical Devices Packaging Market By Material (Plastic (PE, PP, PET, PVC), Metal (Aluminum), Paper & Paperboard, Glass, Others), Product Type (Pouches & Bags, Trays, Boxes & Cartons, Clamshells, Laminates/Films, Blisters, Others), Application (Pharmaceutical/Biologics, Surgical & Medical Instruments, Equipment & Monitoring Devices), and Regional Analysis for 2025-2032

Medical Devices Packaging Market Share and Trends Analysis

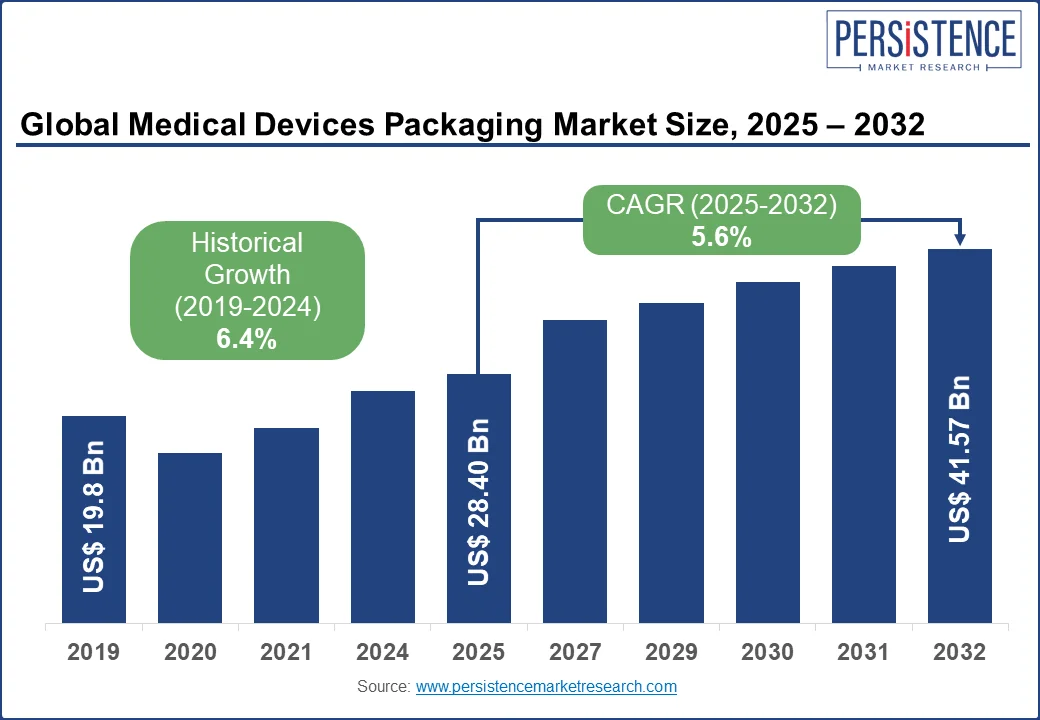

The global medical devices packaging market size is likely to be valued at US$ 28.40 billion in 2025, and is estimated to reach US$ 41.57 billion by 2032, growing at a CAGR of 5.6% during the forecast period 2025 - 2032.

Medical device packaging refers to the specialized materials and formats used to protect, sterilize, and deliver a wide array of medical instruments, implants, diagnostics, and consumables. Having to comply with stringent regulatory standards, these packaging systems play a crucial role in ensuring product integrity, patient safety, and ease of handling across clinical and home-care settings.

The medical devices packaging market is witnessing reasonable growth, driven by the rising volume of surgeries around the globe, the proliferation of single-use devices, and a heightened regulatory emphasis on sterility assurance and traceability. Emerging trends such as smart packaging integration, sustainable material innovation, and the expansion of point-of-care diagnostics are reorienting the competitive landscape in a new direction. At the same time, regional developments in healthcare infrastructure, particularly in Asia Pacific, are unlocking exciting demand and localization opportunities.

Key Industry Highlights:

- Plastic packaging is set to dominate the material segment in 2025 with a projected 64.7% revenue share, driven by the scalability, sterilization compatibility, and regulatory acceptance of plastic across a wide range of disposable medical devices.

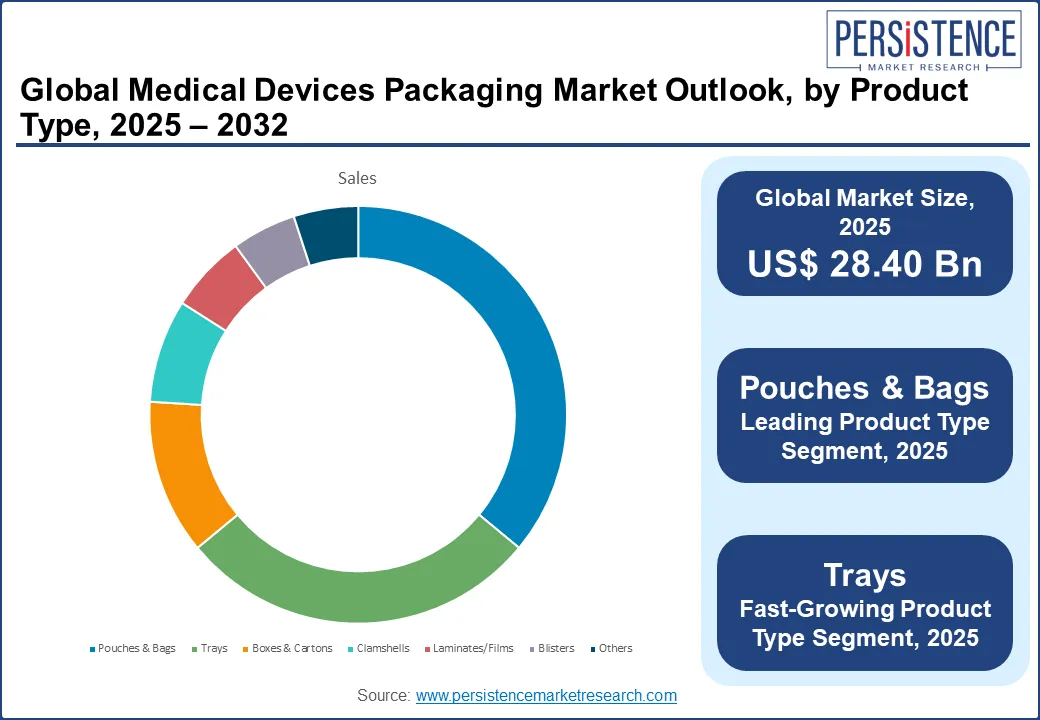

- Pouches & bags will retain the largest share among product type in 2025, with a 36% of the market revenue, owing to their flexibility, cost-efficiency, and widespread use in sterile and high-throughput medical devices packaging lines.

- Pharmaceutical & biologics are poised to maintain a leading position in the application segment due to their stringent sterility and compliance requirements, while in-vitro diagnostics (IVD) is expected to register as the fastest-growing sub-segment, propelled by decentralized testing and sample integrity demands.

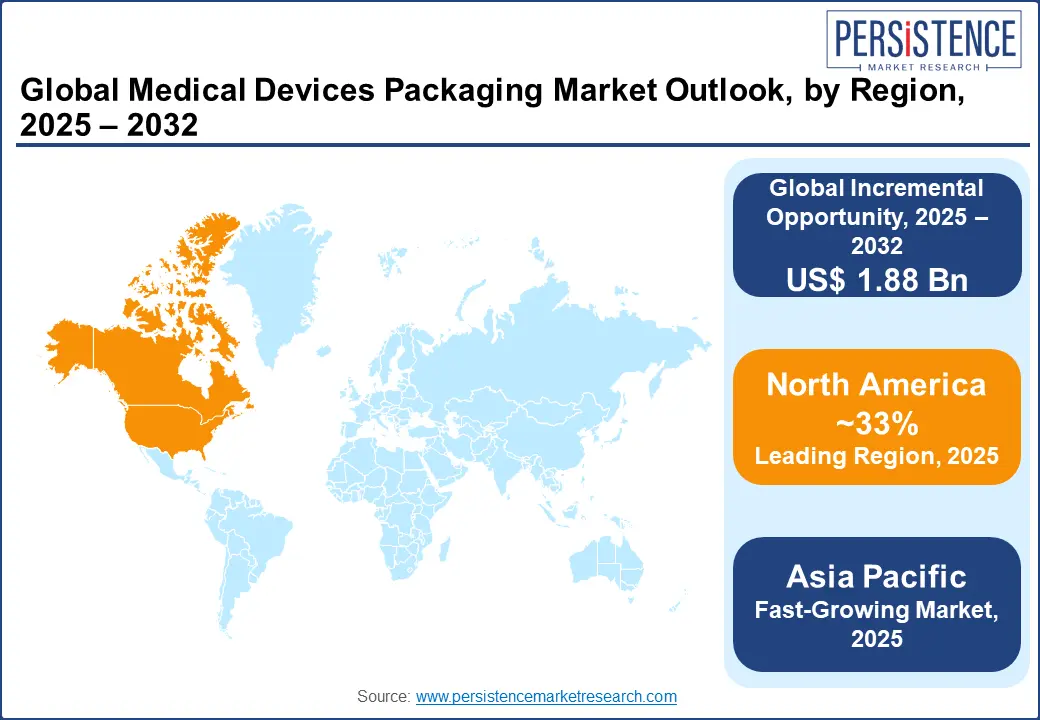

- North America is expected to maintain its lead in 2025 with around 33% of the global market share, aided by a mature regulatory landscape, high device adoption rates, and established packaging infrastructure.

- Asia Pacific will exhibit the fastest CAGR of 8.4% through 2032, boosted by rapid healthcare expansion, local manufacturing incentives, and a growing demand for advanced diagnostics and single-use medical devices.

- Smart and connected packaging in the form of RFID tags, tamper-evident indicators, and embedded UDI compliance is gaining momentum.

- Sustainability mandates across Europe and North America are accelerating the shift toward recyclable, mono-material, and fiber-based medical devices packaging, producing unique growth avenues for eco-compliant product development.

- Leading industry players such as Amcor, Berry Global, Sealed Air, DuPont, Wipak, AptarGroup, and Klöckner Pentaplast are investing strategically in mergers & acquisitions (M&A), vertical integration, and material innovation to bolster their competitiveness quotient and ensure regulatory alignment.

|

Global Market Attribute |

Key Insights |

|

Medical Devices Packaging Market Size (2025E) |

US$ 28.40 Bn |

|

Market Value Forecast (2032F) |

US$ 41.57 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.4% |

Market Dynamics

Driver - Growing Preference for Minimally Invasive and At-Home Healthcare Devices to Broaden Market Horizon

The rapid rise in the popularity of minimally invasive procedures and the growing shift toward at-home medical care are playing a central role in influencing the medical devices packaging design, and volume. Critical devices such as insulin pens, wearable monitors, diagnostic test kits, and portable infusion pumps require compact, single-use, and contamination-proof packaging that supports ease of use and ensures patient safety. The demand for such packaged devices grew in the wake of the COVID-19 pandemic, which accelerated the adoption of remote care and decentralized diagnostics. According to study conducted in 2024, over 40% of U.S. healthcare consumers used home-based diagnostics at least once between 2022 and 2023. This sudden surge in the adoption of at-home diagnostic devices has pushed manufacturers to reconsider packaging for sterility, user-friendliness, and clear instructions.

Moreover, these trends have generated momentum for unit-dose, pre-sterilized blister packaging and tamper-evident formats that align with both patient convenience and regulatory compliance. For example, since 2021, Dentsply Sirona has been offering Vortex Blue endodontic files in pre-sterilized, single-use blister packs to enhance hygiene, and reduce cross-contamination risk, and improve clinical efficiency. These files maintain high performance while supporting infection prevention protocols in dental practices. Mounting side-by-side to these developments are sustainability concerns that encourage the use of recyclable films and bio-based polymers, especially for high-volume at-home devices. The convergence of consumer-centric healthcare and safety assurance is, therefore, driving packaging innovation that balances the integrity, portability, and usability of the products, fueling the medical devices packaging market growth in the process.

Restraint - Sterilization Compatibility and Packaging Material Constraints to Pose Limitations on Market Scalability

One of the most formidable challenges confronting the medical devices packaging market is the requirement of ensuring material compatibility with diverse sterilization methods. This has become a core necessity as devices become increasingly complex to deal with even more complicated medical conditions and regulatory scrutiny intensifies. Packaging must maintain a high sterility post-processing, and also withstand exposure to methods such as gamma irradiation, ethylene oxide (EtO), and steam sterilization. Each of these methods interacts differently with materials such as polyethylene, polypropylene, and Tyvek. For instance, gamma sterilization can degrade certain polymers over time, leading to brittleness or discoloration, while EtO, though material-friendly, it requires extended aeration periods to remove toxic residues, delaying the time to reach the market.

Compounding this hurdle is the fact that not all advanced or sustainable materials are approved or compatible with current sterilization protocols, limiting innovation in eco-friendly packaging. In 2023, for instance, multiple European manufacturers reported delays in CE marking due to failures in sterile barrier validation under ISO 11607 post-irradiation, reiterating the material-sterilization trade-off. Stricter domestic regulations, such as the reduced EtO emissions mandates in the U.S., are further narrowing sterilization options, placing additional pressure on packaging engineers to find multi-compatible materials, often at higher costs or with a limited number of suppliers.

Opportunity - Rising Adoption of Smart and Connected Packaging to Usher in a New Growth Wave in the Market

A highly lucrative and upcoming opportunity in the medical devices packaging market is the growing adoption of smart and connected packaging solutions, particularly for high-value, sensitive, or implantable devices that require real-time traceability, environmental monitoring, and anti-tampering safeguards. With global healthcare logistics becoming more decentralized and complex, especially post-COVID, stakeholders are increasingly seeking packaging systems that can integrate technologies such as RFID tags, NFC chips, QR codes, and temperature sensors to ensure compliance, track chain-of-custody, and prevent sterility breaches during transit. According to published studies, there is a perceptible trend among manufacturers to implement smart labeling or embedded tracking systems within their medical device packaging solutions.

Facilitating this shift further are the mandates enforced by different regulatory authorities, such as the FDA’s Unique Device Identification (UDI) system and the EU’s Medical Device Regulation (MDR) traceability requirements, both of which compel manufacturers to enhance transparency across the supply chain. Leading label companies are already piloting smart blister and pouch solutions that log humidity, temperature excursions, and opening events, that prove highly useful for cold chain-sensitive surgical implants and biologic device kits.

In June 2025, label experts from Avery Dennison, Abbott Label, and Diversified Labeling Solutions (DLS) provided insights on how these companies are integrating RFID inlay converting into their existing processes by adding insertion modules, enabling the production of smart labels with minimal investment.

Key challenges include ensuring precise inlay placement, tension control, quality inspection, and handling defective inlays to maintain high performance and reliability in RFID labels for diverse applications. As evident, smart packaging offers a convergence of compliance, patient safety, and logistical efficiency, making it one of the most commercially promising frontiers in the medical devices packaging sector.

Category-wise Analysis

Material Insights

The plastic packaging segment is expected to hold around 65% of the medical devices packaging market share in the material category in 2025. The unmatched versatility, lightweight profile, and cost-efficiency of plastic packaging, especially in high-throughput formats such as pouches and thermoformed trays, are the primary growth drivers for this sub-segment. Moreover, its adaptability to sterilization techniques such as EtO and gamma irradiation makes it ideal for disposable syringes, surgical kits, and diagnostic tools. With manufacturers facing the dual pressures of meeting stringent regulatory requirements and advancing the employment of sustainable packaging materials use, the adoption of high-performance polymers such as cyclic olefin copolymers (COCs) and bio-based polyethylene has accelerated. For the medical devices packaging industry, a key opportunity lies in engineering recyclable, sterilizable polymers and integrating smart layers, such as RFID-embedded flexible films.

As the fastest growing sub-segment, metal packaging in aluminum formats is gaining firm ground due to its robust barrier properties, tamper resistance, and thermal stability. These qualities make aluminium-based medical devices packaging especially suitable for temperature-sensitive biologics, orthopedic implants, and surgical-grade equipment that demand zero tolerance for compromise during sterilization or shipment. As EtO emission concerns intensify and autoclave use surges, metal containers offer a compelling solution by withstanding high-temperature sterilization without degradation. Furthermore, the recyclability of aluminum aligns with growing environmental, social, and governance (ESG) mandates across the medtech value chain, offering a premium, circular economy opportunity. Forward-thinking manufacturers are also exploring hybrid packaging formats, such as metal-lined cartons or aluminum-foil multilayers, which balance sustainability with performance.

Product Type Insights

Forecast to hold a revenue share of nearly 36% in 2025 in the product segment, pouches and bags are considered the backbone of the sterile medical device packaging ecosystem, primarily on account of their low cost, lightweight nature, and scalability across diverse device categories, ranging from catheters and IV sets to diagnostic swabs and dental equipment. Being well compatible with form-fill-seal automation and EtO/gamma sterilization processes makes them indispensable in high-volume manufacturing environments.

The increasing adoption of single-use and disposable medical devices, especially in infection-prone environments such as ICUs, has emerged as a central growth driver for pouches and bags. Manufacturers are also working on developing peelable sealants, antimicrobial film coatings, and transparent barrier layers that allow visual inspection while maintaining shelf stability. In terms of innovation, the next advancement involves smart pouches integrated with tamper indicators or NFC tags to support traceability in remote healthcare and clinical trials, where device integrity is difficult to monitor.

Trays, particularly thermoformed variants, are increasingly becoming the preferred packaging choice for surgical kits, orthopedic implants, and procedure-specific device assemblies. Their rigid structure ensures dimensional stability and protection against puncture or compression, making them essential for ensuring sterile barrier integrity in transit and handling. A major growth driver for this sub-segment is the rising demand for pre-assembled, procedure-ready kits that streamline workflows in high-pressure surgical environments. Besides this, the rising proclivity for minimally invasive surgery (MIS) is fueling the uptake of trays, as complex multi-part tools must remain sterilized and organized upon delivery.

Regional Insights

North America Medical Devices Packaging Market Trends

North America is anticipated to secure around 33% of the medical devices packaging market share in 2025. The position is attributed to its stringent regulatory environment, such as the FDA’s UDI mandates, capacity to channelize resources into medical R&D and healthcare infrastructure, and being home to some of the most established packaging and medtech manufacturers. In the sterile packaging space, the position of North America is even stronger because of the widespread deployment of high-volume drug delivery systems and device usage in hospitals and outpatient surgical centers across the U.S. and Canada. The maturity of the regional market is further bolstered by an increasing adoption of advanced sterile barrier systems and continuous investments in automation and R&D.

Asia Pacific Medical Devices Packaging Market Trends

Asia Pacific is the fastest growing market for medical devices packaging solutions, driven by a steadily improving healthcare infrastructure, increasing penetration of advanced diagnostics, and rising consumption of injectable biologics. Estimated to display a CAGR of 8.4% through 2032, the region is emerging as a formidable force in the medical flexible packaging space, with China occupying a commanding position in IVD packaging. The lucrative pull of Asia Pacific in these contexts is supported by heavy investments in molecular and point-of-care testing systems. This rapid momentum is underpinned by an expanding budgetary allocation for public healthcare, ambitious domestic manufacturing strategies, and a shifting disease burden that emphasizes diagnostics and outpatient care. As regulatory mandates become more consistent and unambiguous across the region and governments stimulate domestic production, Asia Pacific is set to lead in volume growth and mass-market packaging innovation in the years to come.

Europe Medical Devices Packaging Market Trends

Europe represents a highly strategic, profitable, and influential region in the medical devices packaging market. The growth of the market here is mainly owing to the EU’s rigorous regulatory framework, sustainability mandates, and a strong medtech manufacturing base. While it may not stand out in terms of volume, Europe is instrumental in shaping packaging innovations around the world through its leadership in compliance-driven design and green packaging standards. The implementation of the EU MDR has heightened requirements for traceability, usability validation, and sterile barrier performance, particularly for high-risk Class II and III devices. As a result, medical device packaging manufacturers have been pushed to invest in formats that ensure regulatory alignment, extended shelf-life, and labeling accuracy.

Simultaneously, Europe’s aggressive transition toward a circular economy is stoking the demand for recyclable, biodegradable, and fiber-based packaging solutions. Germany and the Netherlands are at the forefront of this trend, with public health systems increasingly prioritizing low-carbon and closed-loop packaging in procurement policies. Moreover, Europe’s central role in cross-border clinical trials, surgical kit distribution, and biologics handling positions it as a premium market for customized, high-integrity packaging systems.

Competitive Landscape

The competitive landscape of the global medical devices packaging market is characterized by the dynamic presence of scale-driven incumbents and highly specialized innovators. Key players are pursuing a multi-pronged strategy revolving around vertical integration, technological differentiation, and expansion powered by M&A operations. Large, diversified packaging giants, such as Amcor, Berry Global, Sealed Air, DuPont, and Wipak, leverage their global manufacturing footprint to offer end-to-end solutions, from high-barrier film extrusion for sterile pouches to thermoformed trays. These companies are investing massively in R&D and sustainable materials to adhere to regulatory and ESG compliances.

Another aspect of the competition in this market are the increasing M&A and partnership activities by industry leaders. In recent years, major players have acquired or partnered with regional specialists to widen product portfolios and serve local markets more effectively. CCL’s acquisition of Graphic West and Gerresheimer merging with Bormioli Pharma testify to this evolving trend. Furthermore, growing private equity interest in the medical devices packaging space also underpins the perceived profitability of entering this market. Feeding the competitive spirit is the expansion of logistics and kitting specialists such as Owens & Minor and UFP Technologies into engineered packaging for complex device kits, aligning with supply chain resilience and nearshoring trends.

Key Industry Developments:

- In June 2025, DuPont expanded its healthcare manufacturing facility in Heredia, Costa Rica, adding 16,000 square feet to introduce the region’s first sterile healthcare packaging production using Tyvek® technology, alongside increased medical tubing capacity. The ISO-certified facility now operates 24/7 to support healthcare customers across the Caribbean and the Americas, strengthening DuPont’s role as a comprehensive supply chain partner in the global medical device industry.

- In April 2025, Amcor inaugurated a state-of-the-art healthcare packaging coating facility in Selangor, Malaysia, the first in Asia to use advanced air knife coating technology, enhancing supply chain resilience and reducing lead times for medical device packaging. The facility expands Amcor’s existing plant to produce both top and bottom substrates locally, improving product consistency, reducing waste, and meeting growing regional demand for sterile, reliable packaging solutions.

- In March 2025, Avanos Medical, Inc. issued a Class I recall of its Ballard Closed Suction Systems due to a sterilization failure that could cause serious harm including infection, airway injury, sepsis, or death. The recall requires users to immediately stop using affected products, quarantine them, report inventory, and return or destroy the devices; replacements will be provided. The FDA has identified this recall as a concerning type.

Companies Covered in Medical Devices Packaging Market

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- DuPont de Nemours, Inc.

- 3M Company

- Wipak Group

- Klöckner Pentaplast Group

- AptarGroup, Inc.

- SteriPack Group

- Nelipak Corporation

- Oliver Healthcare Packaging

- CCL Industries

- Constantia Flexibles

- Sonoco Products Company

- WestRock Company

- Billerud

- Mitsubishi Chemical Holdings

- Printpack

- Proampac

- Oliver Healthcare Packaging

- Hudson Poly Bag

Frequently Asked Questions

The medical devices packaging market is projected to reach US$ 28.40 billion in 2025.

The rapid rise in the popularity of minimally invasive procedures and the growing shift toward at-home medical care are driving the market.

The medical devices packaging market is poised to witness a CAGR of 5.6% from 2025 to 2032.

The growing adoption of smart and connected packaging solutions and a steady decentralization of global healthcare logistics are key market opportunities.

Amcor, Berry Global, Sealed Air, and DuPont are some of the key players in the global medical devices packaging market.