- Healthcare Services

- Non-Emergency Medical Transportation Market

Non-Emergency Medical Transportation Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Non-Emergency Medical Transportation Market by Service (Private Pay Patient Transportation, Insurance Backed Patient Transportation, Courier Services, and Others), by Application (Dialysis, Routine Doctor Visits, Mental Health Related Appointments, Rehabilitation, and Others), by End User (Hospitals, Nursing Care Centers, Assisted Living Facilities, Home Healthcare Settings, and Individual Patients), and Regional Analysis from 2026 to 2033.

Non-Emergency Medical Transportation Market Share and Trend Analysis

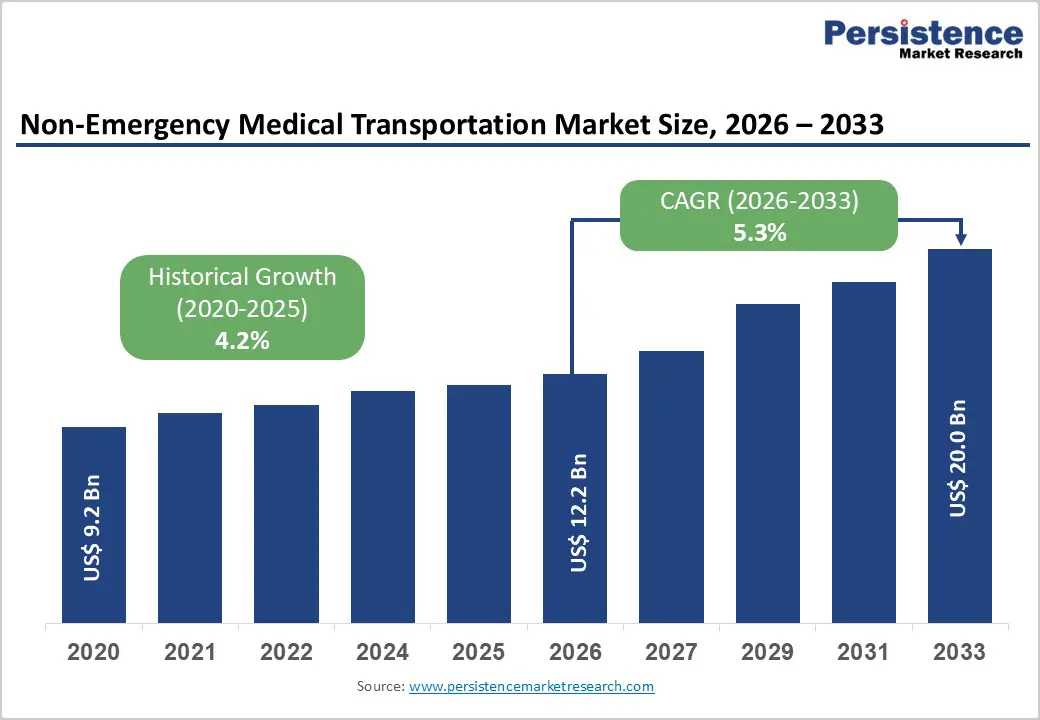

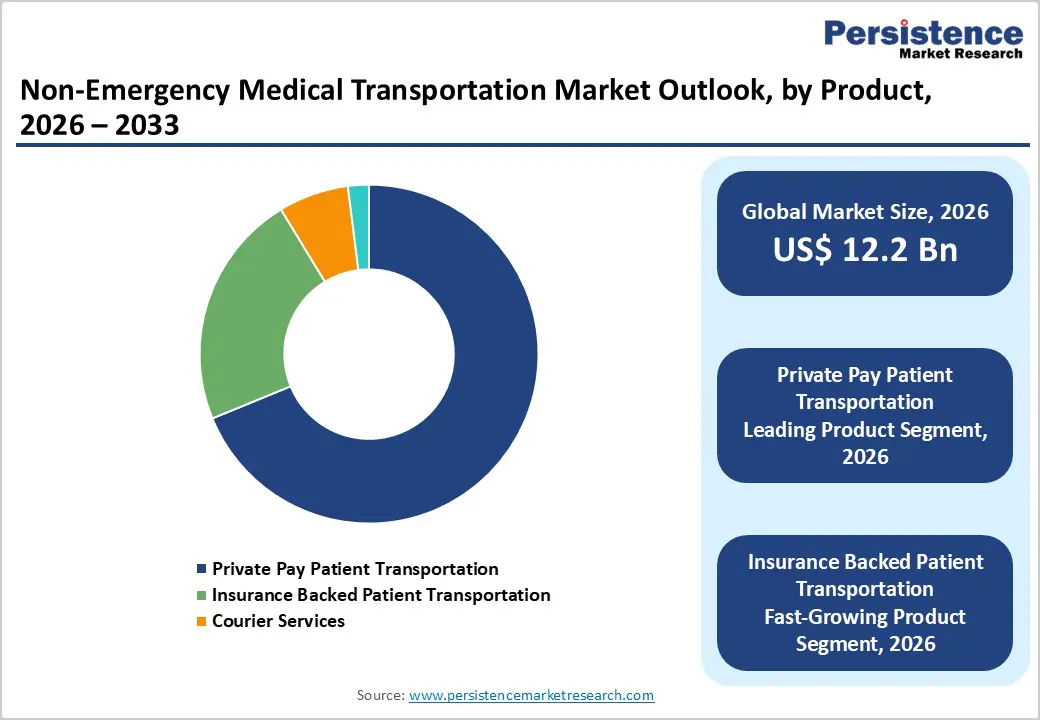

The global Non-emergency medical transportation market size is estimated to grow from US$ 12.2 Bn in 2026 to US$ 20.0 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for non-emergency medical transportation services is increasing steadily, driven by the rising prevalence of chronic diseases, aging populations, and growing emphasis on consistent access to outpatient healthcare. Conditions such as renal failure, cardiovascular disorders, diabetes, and mobility-related impairments require frequent, scheduled visits to dialysis centers, hospitals, rehabilitation facilities, and physician offices, directly supporting sustained demand for non-emergency transport solutions. Increasing healthcare utilization, expansion of outpatient and home-based care models, and greater awareness of transportation as a critical enabler of care continuity are reinforcing market growth.

Non-emergency medical transportation services are widely used across hospitals, nursing care centers, assisted living facilities, and home healthcare settings to ensure timely patient access to medical appointments. Growing focus on reducing missed appointments, improving treatment adherence, and enhancing patient outcomes is accelerating adoption. Expansion of managed care programs, improved reimbursement coverage, and increasing integration of digital scheduling, dispatch, and route-optimization platforms are further strengthening operational efficiency. Additionally, expanding healthcare infrastructure in emerging economies and rising investments in patient access solutions are reinforcing long-term demand for non-emergency medical transportation globally.

Key Industry Highlights

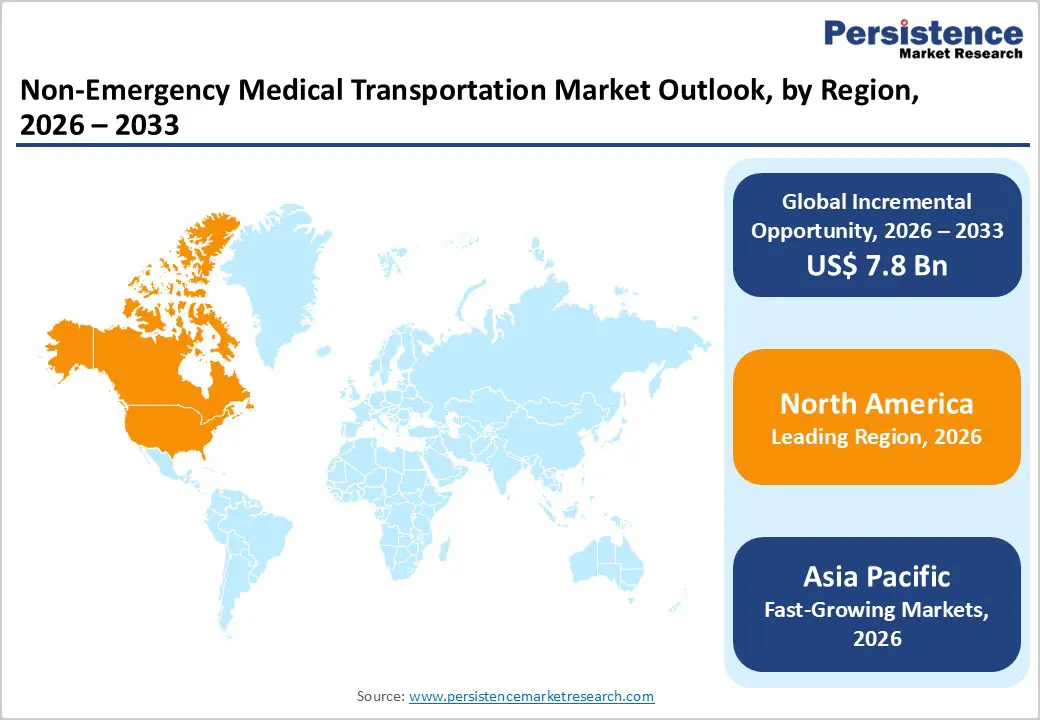

- Leading Region: North America holds the largest share at 47.3%, supported by strong healthcare infrastructure, widespread insurance coverage for transportation services, high chronic disease burden, advanced care coordination models, and high adoption of organized non-emergency transportation across hospitals and outpatient facilities.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising elderly populations, increasing chronic disease prevalence, rapid urbanization, expanding healthcare infrastructure, government-led access initiatives, and improving availability of organized patient transport services.

- Leading Service Segment: Private pay patient transportation dominates the market due to operational simplicity, cost flexibility, quick service availability, and widespread use for routine medical visits and outpatient care.

- Fastest-Growing Service Segment: Insurance-backed patient transportation is growing rapidly as healthcare systems emphasize care coordination, reduced no-show rates, reimbursement-backed access, and integration with payer-managed programs.

- Leading Application Segment: Routine doctor visits remain the top segment, driven by high volumes of scheduled outpatient appointments and ongoing management of chronic conditions.

- Fastest-Growing Application Segment: Dialysis is scaling quickly due to the high frequency of recurring treatments and the critical need for reliable, timely transportation services.

| Key Insights | Details |

|---|---|

| Non-Emergency Medical Transportation Market Size (2026E) | US$ 12.2 Bn |

| Market Value Forecast (2033F) | US$ 20.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver – Growing Chronic Disease Burden, Aging Populations, and Shift Toward Outpatient Care

Market growth is strongly supported by the rising global burden of chronic diseases and the rapid expansion of aging populations that require frequent, scheduled access to healthcare facilities. Conditions such as renal failure, cardiovascular disease, diabetes, and mobility-related disorders necessitate recurring visits to dialysis centers, outpatient clinics, and rehabilitation facilities, significantly increasing reliance on non-emergency transportation services. As healthcare systems continue to transition away from inpatient treatment toward outpatient and community-based care models, the need for dependable patient mobility solutions has intensified. Older adults, particularly those with physical or cognitive limitations, increasingly depend on assisted transportation to maintain continuity of care. In parallel, healthcare providers and payers are emphasizing reduced missed appointments, improved treatment adherence, and better patient outcomes—factors that directly support NEMT utilization.

Expansion of insurance-backed transportation benefits, especially under public healthcare programs, further strengthens demand. Additionally, advancements in digital dispatching, route optimization, and scheduling platforms are improving service efficiency and scalability, making NEMT services more accessible and cost-effective. Increased awareness of patient access as a social determinant of health, coupled with rising healthcare expenditure in both developed and developing economies, continues to create a strong and sustained demand environment for non-emergency medical transportation services.

Restraints – Operational Cost Pressures, Workforce Challenges, and Regulatory Complexity

The market expansion is constrained by a range of operational and structural challenges. One of the primary restraints is the high cost associated with fleet acquisition, vehicle maintenance, fuel price volatility, and insurance coverage, which places financial pressure on small and mid-sized transportation providers. These cost burdens are further amplified in regions with strict vehicle compliance standards and safety regulations. Workforce-related issues also present significant limitations. Recruiting and retaining trained drivers, particularly those qualified to handle elderly, disabled, or medically fragile patients, remains difficult. High employee turnover, rising wage expectations, and mandatory training requirements increase operating expenses and can disrupt service continuity.

Regulatory complexity across regions adds another layer of challenge. Compliance with healthcare transportation standards, reimbursement documentation requirements, and payer-specific policies can be administratively intensive, particularly for insurance-backed services. Delayed reimbursements and claim denials negatively impact cash flow for providers. In rural and underserved regions, limited infrastructure, long travel distances, and low trip density reduce economic viability. Collectively, these factors slow service expansion, limit scalability, and create barriers to entry, particularly for new or smaller operators.

Opportunity – Digital Platforms, Emerging Market Expansion, and Value-Based Care Alignment

Significant growth opportunities are emerging through the digital transformation of patient transportation services and expanding healthcare access in emerging markets. Adoption of technology-enabled platforms such as real-time booking systems, GPS-based fleet tracking, automated scheduling, and predictive analytics is enhancing service efficiency while reducing operational costs. These solutions improve coordination between providers, payers, and healthcare facilities, creating opportunities for scalable and integrated transportation networks. Emerging economies across Asia Pacific, Latin America, and parts of the Middle East offer substantial untapped potential due to expanding healthcare infrastructure, increasing elderly populations, and rising prevalence of chronic diseases.

Government initiatives focused on improving healthcare accessibility, along with growth in private hospitals and dialysis centers, are expected to drive structured demand for NEMT services. Additionally, the global shift toward value-based care models presents a long-term opportunity. Healthcare systems are increasingly recognizing transportation as a critical enabler of patient adherence and outcome improvement. Partnerships between NEMT providers, hospitals, insurers, and digital health platforms are enabling bundled service offerings and long-term contracts. As patient-centric care models gain traction, non-emergency medical transportation is positioned to evolve from a logistical service into an essential component of coordinated healthcare delivery.

Category-wise Analysis

By Service, Private Pay Patient Transportation Leads Due to Operational Simplicity, Cost Flexibility, and High Adoption for Routine Care

Private pay patient transportation is projected to dominate the global non-emergency medical transportation market in 2026, accounting for a revenue share of 68.8%. This dominance is primarily driven by simplified operational models, direct payment structures, and flexibility in scheduling compared to insurance-backed services. Private pay services are widely utilized for routine medical visits, follow-up consultations, and outpatient care, particularly among elderly individuals and patients without comprehensive insurance coverage.

Lower administrative burden, faster booking turnaround, and minimal reimbursement complexities further support adoption. These services are especially prevalent among small transport providers and independent operators catering to urban and semi-urban populations. Additionally, private pay transportation is less dependent on payer approvals, making it more accessible in emerging markets and rural areas. Continued demand from aging populations and steady utilization for recurring medical appointments are expected to sustain the leadership of private pay patient transportation globally.

By Application, Routine Doctor Visits Lead Due to High Volume of Recurring Medical Appointments

The routine doctor visits segment is expected to dominate the global non-emergency medical transportation market in 2026, capturing a revenue share of 34.7%. This leadership is driven by the high frequency of scheduled outpatient visits, follow-up consultations, and chronic disease management appointments that require dependable transportation support. NEMT services play a critical role in ensuring patient adherence to care plans by enabling timely access to primary care physicians and specialists.

Rising prevalence of chronic conditions such as diabetes, cardiovascular disorders, and mobility-limiting illnesses particularly among elderly populations continues to increase transport demand. Expansion of outpatient care models and growing emphasis on preventive healthcare further support sustained utilization. As healthcare systems increasingly focus on reducing missed appointments and improving patient outcomes, routine doctor visits remain the largest application area for non-emergency medical transportation services.

By End User, Hospitals Lead Due to High Patient Volume and Structured Discharge and Referral Networks

Hospitals are projected to dominate the global non-emergency medical transportation market in 2026, accounting for a revenue share of 28.0%. This dominance is attributed to high patient throughput, frequent referrals to outpatient services, and structured discharge planning that often requires coordinated transportation support. Hospitals rely heavily on NEMT services to ensure continuity of care for patients transitioning to rehabilitation centers, dialysis units, or home healthcare settings.

Established partnerships with transportation providers, standardized patient transport protocols, and higher institutional budgets support consistent service utilization. Additionally, hospitals prioritize reliable and compliant transportation solutions to reduce readmission risks and improve care coordination. While home healthcare and assisted living facilities are expanding rapidly, hospitals continue to lead due to centralized decision-making, scale of operations, and consistent demand for organized non-emergency transport services.

Region-wise Insights

North America Non-Emergency Medical Transportation Market Trends

North America is expected to dominate the global non-emergency medical transportation market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a well-established healthcare ecosystem, strong insurance coverage for NEMT services, and a high prevalence of chronic diseases requiring recurring medical visits.

Robust Medicaid reimbursement frameworks, widespread use of managed care models, and strong presence of organized NEMT providers support market growth. Additionally, high awareness of patient access programs, integration of digital scheduling platforms, and emphasis on reducing missed appointments contribute to sustained demand. Frequent service utilization, high healthcare spending, and regulatory support are expected to maintain North America’s leadership position throughout the forecast period.

Europe Non-Emergency Medical Transportation Market Trends

The Europe non-emergency medical transportation market is expected to grow steadily, supported by strong public healthcare systems and increasing demand for accessible patient transportation across countries such as Germany, the U.K., France, Italy, and Spain. Aging populations and rising incidence of mobility-limiting conditions are driving consistent demand for scheduled medical transport services.

Hospitals and regional health authorities continue to rely on structured transport networks to support outpatient care and post-acute services. Expansion of private healthcare providers and growing focus on patient-centric care models further strengthen demand. Preference for compliant, standardized, and high-quality transportation services supports market stability, positioning Europe for steady long-term growth.

Asia Pacific Non-Emergency Medical Transportation Market Trends

The Asia Pacific non-emergency medical transportation market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare infrastructure, rising awareness of patient accessibility, and growing elderly populations. Countries such as China, India, Japan, South Korea, and Australia are witnessing increasing demand for organized medical transportation due to urbanization and improved access to healthcare services.

Rapid expansion of private hospitals, dialysis centers, and outpatient clinics is significantly increasing transport needs. Improving affordability, availability of cost-effective transport services, and growing penetration of digital booking platforms are enhancing market accessibility. Government initiatives focused on healthcare access and chronic disease management further contribute to growth. With rising disposable income and healthcare utilization, Asia Pacific is expected to emerge as the fastest-growing regional market.

Market Competitive Landscape

The global non-emergency medical transportation market is highly competitive, with strong participation from companies such as MTM, Inc., AMR, Xpress Transportation, CJ Medical Transportation, and Southeastrans. These players leverage extensive service networks, long-standing payer and provider relationships, and strong operational capabilities to address the rising demand for reliable, timely, and patient-centric non-emergency transportation services.

Their offerings emphasize on-time performance, route optimization, digital scheduling and dispatch systems, patient safety, regulatory compliance, and cost efficiency across recurring transport needs such as dialysis, routine medical visits, and post-acute care. Continuous investments in fleet modernization, technology-enabled coordination platforms, adherence to healthcare transportation regulations, and service quality standards remain critical for sustaining competitive positioning in the global non-emergency medical transportation market.

Key Industry Developments:

- In November 2025, Mobisoft Infotech launched a cloud-based Non-Emergency Medical Transportation (NEMT) platform in India aimed at assisting hospitals and clinics in coordinating transportation for patients requiring chronic and recurring medical care. The company indicated that the platform is designed to streamline healthcare logistics by facilitating safe, timely, and dependable patient transport, while enhancing care continuity and improving operational efficiency across healthcare facilities.

- In August 2024, MTM, the largest privately held non-emergency medical transportation broker in the U.S., announced an agreement with Global Medical Response to acquire Access2Care, LLC. The acquisition, anticipated to close in the fall, is expected to substantially strengthen MTM’s market footprint and boost its annual revenue.

- In January 2024, MediDrive®, a CTG Partner Company, announced its formal entry into the non-emergency medical transportation market, marking a strategic expansion of its healthcare services portfolio. This move underscores the company’s focus on enhancing patient access solutions and strengthening coordinated care delivery through reliable transportation services.

Companies Covered in Non-Emergency Medical Transportation Market

- MTM, Inc.

- AMR

- Xpress Transportation

- CJ Medical Transportation

- Southeastrans

- Modivcare

- Crothall Healthcare

- Elite Medical Transport

- Acadian Ambulance Service

- ERS Transition Ltd.

- Global Rescue LLC.

- London Medical Transportation Systems

- FirstGroup PLC

- Others

Frequently Asked Questions

The global non-emergency medical transportation market is projected to be valued at US$ 12.2 Bn in 2026.

Rising elderly population and chronic disease prevalence are increasing demand for recurring, non-emergency access to healthcare services.

The global non-emergency medical transportation market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Integration of digital booking platforms and partnerships with ride-hailing services to improve efficiency, scalability, and patient access.

MTM, Inc., AMR, Xpress Transportation, CJ Medical Transportation, and Southeastrans are some of the key players in the non-emergency medical transportation market.