- Medical Devices

- Minimally Invasive Surgical Instruments Market

Minimally Invasive Surgical Instruments Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Minimally Invasive Surgical Instruments Market by Product (Handheld Instruments, Inflation Systems, Cutter Instruments, Guiding Devices, Electrosurgical Devices, Auxiliary Instruments, Others), Application, End-user, and Regional Analysis from 2026 to 2033

Minimally Invasive Surgical Instruments Market Share and Trends Analysis

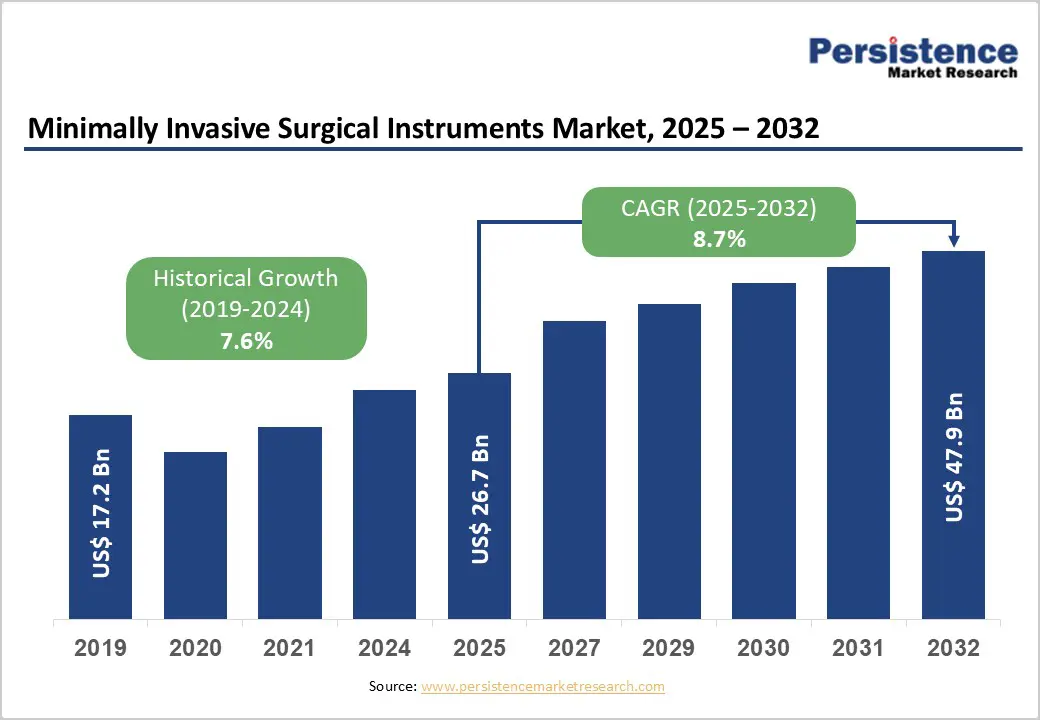

The global minimally invasive surgical instruments market size is estimated to reach US$26.7 billion in 2026 and is projected to reach US$47.9 billion by 2033, growing at a CAGR of 8.7% between 2026 and 2033.

The global market is undergoing rapid expansion as healthcare systems shift toward techniques that reduce patient trauma, shorten recovery time, and improve surgical precision. Advancements in imaging, robotics, and surgeon-assistive technologies continue to elevate the accuracy and safety of MIS procedures across specialties. Growing surgical volumes driven by aging populations, rising chronic disease incidence, and increased preference for cost-effective interventions further strengthen market demand. At the same time, expanding medical tourism and investments in next-generation operating room infrastructure are accelerating global adoption, positioning MIS as a core pillar of modern surgical care.

Key Industry Highlights

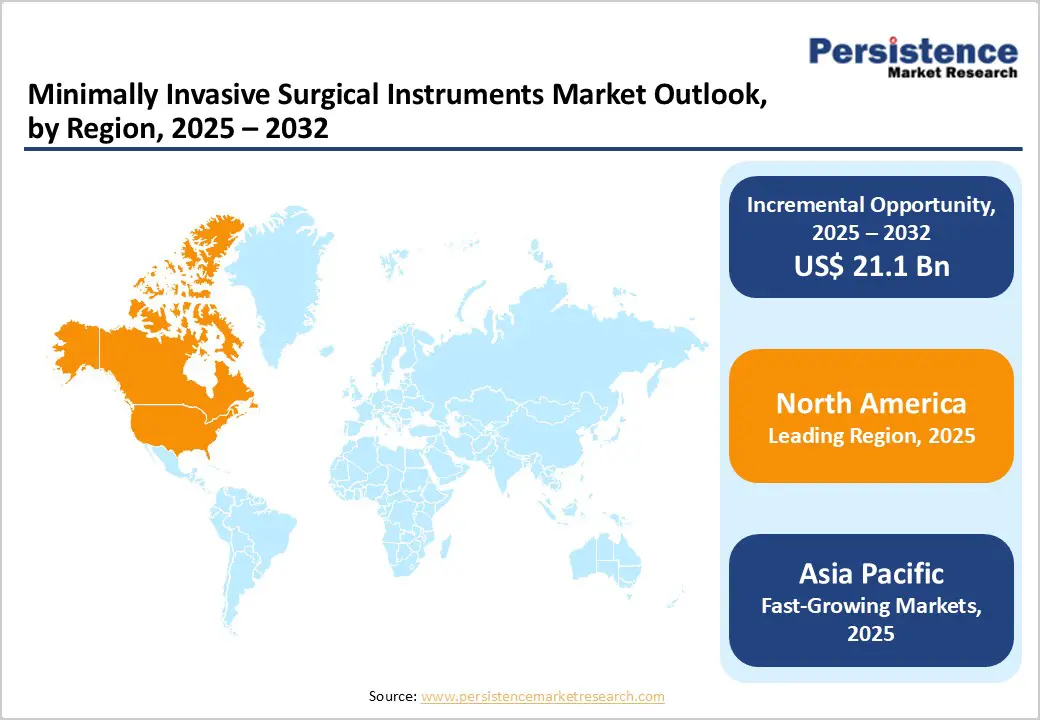

- Leading Region: North America dominates the global market, accounting for 31.9%, driven by strong adoption of advanced robotics, high surgical volumes, and well-established reimbursement systems that support rapid uptake of minimally invasive technologies.

- Fastest-Growing Region: The Asia Pacific market is expected to grow rapidly with a CAGR of 10.6% in the forecast period, fueled by expanding medical tourism, increased hospital investments, and rising demand for cost-effective, technology-enabled minimally invasive procedures.

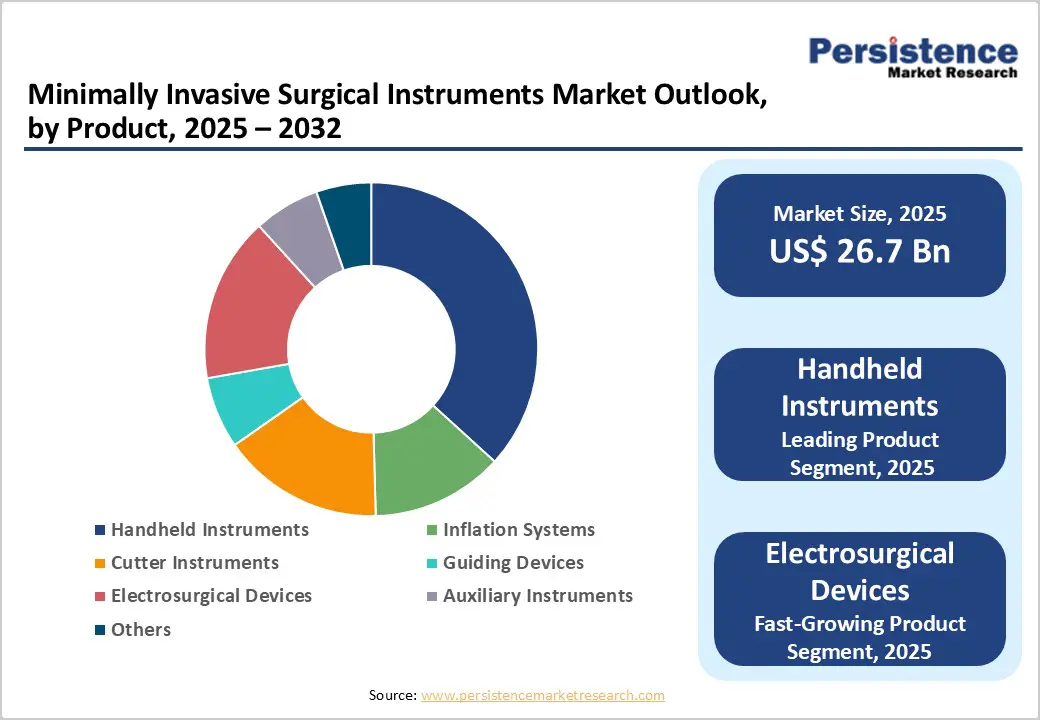

- Leading Product: Handheld instruments lead with 26.5% share, supported by widespread use across specialties, ease of integration into existing workflows, and continuous innovation improving precision and surgeon control.

- Leading Application: Cardiothoracic surgery dominates with 31.4%, driven by the rising prevalence of heart diseases and the accelerated shift toward minimally invasive approaches that reduce surgical trauma and recovery time.

- Leading End-user: Hospitals dominate with a 48.3%, driven by higher procedure volumes, advanced operating room infrastructure, and greater capacity to adopt and maintain complex minimally invasive technologies.

- Robotic-assisted platforms are rapidly expanding across specialties, improving precision, reducing variability, and accelerating hospital investments in next-generation minimally invasive surgical ecosystems.

- Simulation-based MIS training programs are expanding as hospitals prioritize skill development to reduce procedural errors and enhance surgeon proficiency.

- Ambulatory surgical centers are adopting MIS instruments to support same-day procedures, reducing healthcare costs and increasing patient throughput.

| Key Insights | Details |

|---|---|

| Minimally Invasive Surgical Instruments Market Size (2026E) | US$26.7 Billion |

| Market Value Forecast (2033F) | US$47.9 Billion |

| Projected Growth (CAGR 2026 to 2033) | 8.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.6% |

Market Dynamics

Driver - Growing Demand for Precision, Faster Recovery, and Advanced Surgical Technologies

The global minimally invasive surgical instruments market is expanding rapidly, driven by a growing geriatric population and the resulting increase in age-related surgical volumes. MIS techniques offer clear advantages over traditional open procedures, including reduced pain, shorter hospital stays, minimal scarring, and lower tissue damage, making them increasingly preferred worldwide. Their cost-effectiveness further strengthens adoption, especially as healthcare systems focus on efficiency and value-based care.

Advancements in precision technologies, imaging, and AI continue to enhance surgical accuracy and safety, accelerating this transition. In November 2024, technological momentum intensified when Medtronic acquired Fortimedix, a developer of flexible instruments designed for complex endoscopic and single-port procedures.

Innovation advanced further in November 2025, when Royal Philips introduced DeviceGuide, an Artificial Intelligence (AI)-enabled tracking solution built on its EchoNavigator platform to support minimally invasive structural heart interventions.

Collectively, increasing procedural demand, strong clinical benefits, AI-enabled surgical guidance, and expanding medical tourism in developing regions remain key drivers of global MIS instrument market growth.

Restraints - Limited Access, High Costs, and Training Barriers Slow Market Expansion

The global minimally invasive surgical instruments market faces several restraints that slow its full-scale adoption despite strong global demand. High upfront costs associated with advanced imaging systems, robotic platforms, and precision instruments continue to challenge budget-constrained hospitals, particularly in developing regions.

Limited reimbursement for certain MIS procedures in emerging markets further restricts accessibility. In addition, the steep learning curve for surgeons, combined with the need for specialized training, simulation infrastructure, and ongoing skill development, creates operational barriers for healthcare facilities transitioning from open to minimally invasive techniques.

Concerns about sterilization standards, equipment reprocessing, and infection control also persist, particularly regarding reusable MIS instruments. Variability in clinical outcomes due to inconsistent surgeon experience raises additional hesitation among providers. Finally, supply chain disruptions and dependence on high-quality components can delay procurement and increase costs for healthcare systems. Collectively, these financial, operational, and clinical constraints continue to hinder the widespread expansion of MIS technologies across global markets.

Opportunity - Imaging, Robotics, and Ecosystem Integration Unlock High-Growth Potential

Global opportunities in the minimally invasive surgical instruments market are expanding as hospitals worldwide accelerate the shift toward image-guided, robotics-enabled, and AI-supported procedures. A major opportunity lies in the growing demand for real-time visualization and navigation tools that enhance surgeon confidence while reducing variability in complex interventions.

This trend strengthened in April 2023, when GE HealthCare introduced the next-generation bkActiv intraoperative ultrasound system for urology, colorectal, and pelvic floor surgeries. Designed with automatic no-touch autogain and advanced imaging algorithms, the platform delivers high-clarity guidance with minimal user interaction, allowing surgeons to focus fully on precision and outcomes.

The market is also benefiting from the rising adoption of hybrid operating rooms, expanding training programs for MIS techniques, and strong investment in interoperable surgical ecosystems that combine imaging, energy devices, and robotic platforms.

Growing procedural volumes driven by medical tourism, faster recovery expectations, and payer preference for cost-efficient interventions create substantial room for MIS penetration in both developed and emerging markets. Collectively, advancements in intraoperative imaging, surgeon-assistive technologies, and integrated surgical workflows represent the most significant global opportunities for MIS instrument manufacturers.

Category-wise Analysis

By Product: Handheld Instruments Dominate Owing to Versatility, Precision, and Cross-Specialty Utility

Handheld instruments are expected to hold a 26.5% share of the global minimally invasive surgical instruments market by 2026, driven by their versatility, ergonomic design, and widespread use across diverse surgical specialties. Their ease of integration into existing workflows, lower capital requirements compared to advanced robotic systems, and continuous enhancements in precision and control make them the preferred choice for both routine and complex minimally invasive procedures. Ongoing innovation in materials, energy delivery, and single-use formats further strengthens their adoption in hospitals and ambulatory settings worldwide.

By Application: Cardiothoracic Surgery Lead Due to High Disease Burden and Shift Toward Less-Invasive Techniques

Cardiothoracic surgery is expected to hold 31.4% of the global market in 2026, driven by the rising prevalence of cardiac and thoracic disorders and strong clinical preference for less-invasive approaches that reduce trauma, hospital stay, and complications. Advances in imaging, endoscopic tools, and robotic-assisted cardiothoracic procedures are further accelerating adoption. Growing investments in hybrid operating rooms and surgeon training are also enabling broader use of minimally invasive techniques for valve repair, bypass procedures, and thoracic interventions worldwide

By End-user: Hospitals Lead Due to High Procedure Volumes, Advanced Infrastructure, and Multidisciplinary Capabilities

Hospitals are projected to dominate with a 48.3% share in 2026, supported by their ability to manage high surgical volumes, maintain advanced minimally invasive operating suites, and integrate robotics, imaging, and navigation technologies. Their multidisciplinary teams, access to critical care, and broader reimbursement coverage make hospitals the preferred setting for complex minimally invasive procedures. Although ambulatory surgical centers (ASCs) are rapidly expanding, highlighted by nearly 6,500 Medicare-certified ASCs in the United States, hospitals remain the primary hubs for technologically intensive and high-acuity minimally invasive surgeries.

Regional Insights

North America Minimally Invasive Surgical Instruments Market Trends

By 2026, North America is projected to hold 31.9% of the global minimally invasive surgical instruments market, supported by rapid technological adoption, rising procedure volumes, and expanded robotic-assisted surgery capabilities.

Growth momentum strengthened in June 2024, when Zimmer Biomet Holdings, Inc. entered a limited distribution agreement with THINK Surgical, Inc. for the TMINI (Think Miniature Robotic System), a wireless, handheld robotic system for total knee arthroplasty. This integration of Zimmer Biomet technology with a CT-based three-dimensional surgical planning platform enhanced precision and broadened MIS deployment across orthopaedics.

Advancements continued in November 2024, with the U.S. Food and Drug Administration (FDA) granting Investigational Device Exemption (IDE) approval for the OTTAVA Robotic Surgical System, enabling clinical trials in U.S. hospitals. This milestone expanded access to next-generation robotic solutions to reduce variability and improve MIS outcomes.

In June 2025, Johnson & Johnson MedTech launched the ETHICON 4000 Stapler, featuring Three-Dimensional (3D) Staple Technology, improved end-effector engineering, and standardized reload mechanisms for both open and laparoscopic procedures. Together, these developments reflect a consistent regional push toward robotics-enabled accuracy, reduced complication risks, and enhanced MIS efficiency, key drivers shaping North America’s market leadership.

Europe Minimally Invasive Surgical Instruments Market Trends

By 2026, Europe is expected to account for 28.4% of the global minimally invasive surgical instruments market, supported by accelerated innovation in digital surgery, robotics, and artificial intelligence (AI). A major growth catalyst emerged in September 2025, when Medtronic plc announced the expansion of its London operations, doubling its office footprint to 25,000 sq ft and its workforce to more than 200 employees. This site was elevated to Medtronic’s largest global digital centre focused on AI-driven and robotic-assisted surgical technologies.

The multi-million-dollar investment forms part of a five-year commitment to strengthen the United Kingdom’s role in advancing next-generation MIS capabilities. It also builds on ongoing research and design collaborations aimed at refining robotic-assisted surgery tools and enhancing procedural precision. Importantly, the initiative aligns with the National Health Service (NHS) 10-Year Health Plan, which prioritizes digital transformation, reduces surgical invasiveness, and improves patient recovery pathways.

Together, these developments signal Europe’s strong ecosystem for innovation, robust regulatory support, and expanding R&D infrastructure, factors that continue to drive the adoption of high-precision MIS instruments across the region.

Asia Pacific Minimally Invasive Surgical Instruments Market Trends

By 2026, the Asia Pacific minimally invasive surgical instruments market is projected to grow rapidly, with a 10.6% CAGR, driven by rising procedure volumes, expanding healthcare infrastructure, and strong demand from medical tourism. Clinical trial data show increasing adoption of minimally invasive neurosurgical techniques, especially for intracranial haemorrhage (ICH) and brain-tumour interventions, as evidence strengthens and reimbursement frameworks mature.

Simultaneously, Asia Pacific is emerging as a major medical tourism hub, with countries such as India, Thailand, and South Korea attracting international patients for advanced MIS procedures due to high-precision, lower-cost minimally invasive surgery, spurring investments in modern surgical tools and systems.

Infrastructure investment in emerging APAC markets is also accelerating. Regional healthcare systems are building capacity for robotic and navigation-assisted MIS platforms, particularly in neurosurgery, where robotic neurosurgery is forecast to grow strongly. These factors, including stronger clinical evidence, improved reimbursement, inflow from medical tourism, and infrastructure build-out, are collectively driving the robust growth of MIS instruments in the Asia Pacific.

Competitive Landscape

The competitive landscape is shaped by rapid advancements in robotics, energy platforms, imaging ecosystems, and AI-enabled surgical guidance. Players compete through integrated digital surgery solutions, cross-industry collaborations, and ecosystem-based innovation that enhance precision, reduce variability, and support complex procedures across specialties. Growing focus on platform interoperability and smart surgical workflows further intensifies competition.

Key Industry Developments:

- In September 2024, Medtronic launched new software, hardware, and imaging upgrades to strengthen its AiBLE™ ecosystem, enhancing navigation, robotics, data, and AI capabilities for spine and cranial procedures, and partnered with Siemens Healthineers to broaden access to advanced imaging.

- In March 2025, Johnson & Johnson MedTech introduced the DUALTO™ Energy System, an integrated multi-modal surgical energy platform compatible with Polyphonic™ Fleet software, supporting both open and minimally invasive surgery and designed for future integration with the OTTAVA™ Robotic Surgical System.

Companies Covered in Minimally Invasive Surgical Instruments Market

- Medtronic

- B. Braun Melsungen AG

- Stryker

- Smith+Nephew

- Abbott

- Boston Scientific Corporation

- CONMED Corporation

- Microline Surgical

- Zimmer Biomet

- Siemens Healthineers International AG

- Medical Devices Business Services, Inc.

- GE Healthcare

- Intuitive Surgical Operations, Inc.

- NuVasive®, Inc.

Frequently Asked Questions

The global minimally invasive surgical instruments market is projected to be valued at US$26.7 Billion in 2026.

Rising demand for faster recovery, enhanced precision, and robotics-enabled surgical efficiency is propelling global adoption of minimally invasive surgical instruments.

The global minimally invasive surgical instruments market is poised to witness a CAGR of 8.7% between 2026 and 2033.

Expanding robotic surgery ecosystems and growing procedure volumes in emerging markets offer strong opportunities for next-generation minimally invasive surgical instruments.

Major players in the global are Medtronic, B. Braun Melsungen AG, Stryker, Smith+Nephew, Abbott, Boston Scientific Corporation, and others.