- Medical Devices

- Primary Care POC Diagnostics Market

Primary Care POC Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

Primary Care POC Diagnostics Market by Product (Glucose tests, Heart & cholesterol tests, Infectious disease tests, Pregnancy & fertility tests, Cancer marker tests, Coagulation tests, Others), by End-user (Hospitals, Clinics/Diagnostic centers, Home care, Pharmacy/Retail clinics, Research labs) and Regionala Analysis, 2026 - 2033

Primary Care POC Diagnostics Market Share and Trends Analysis

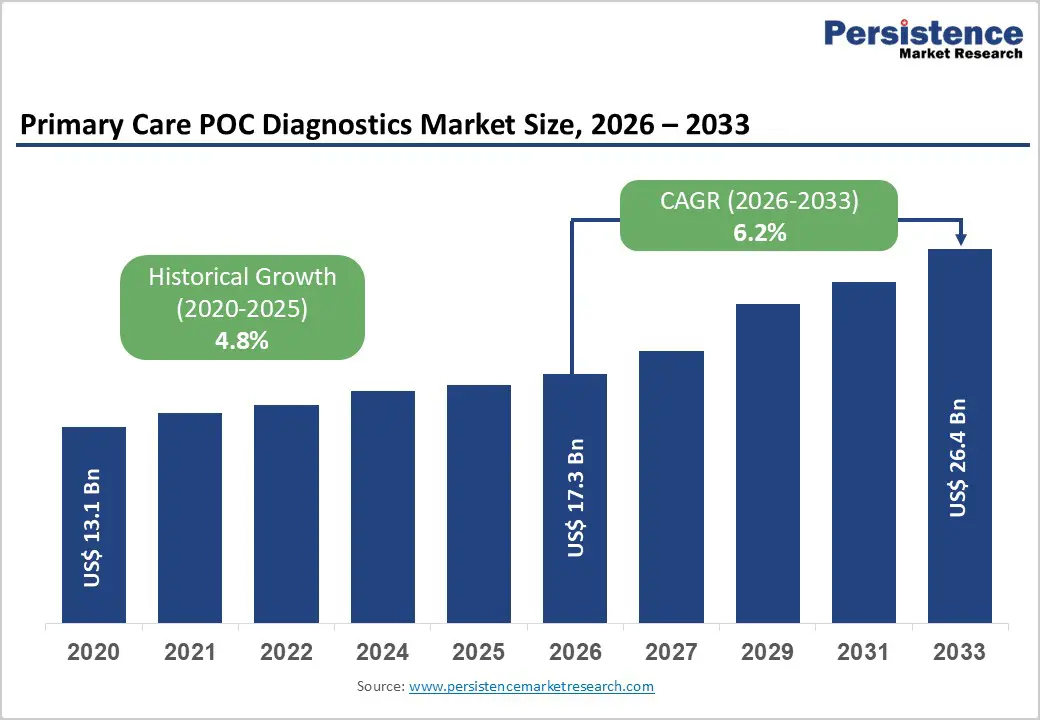

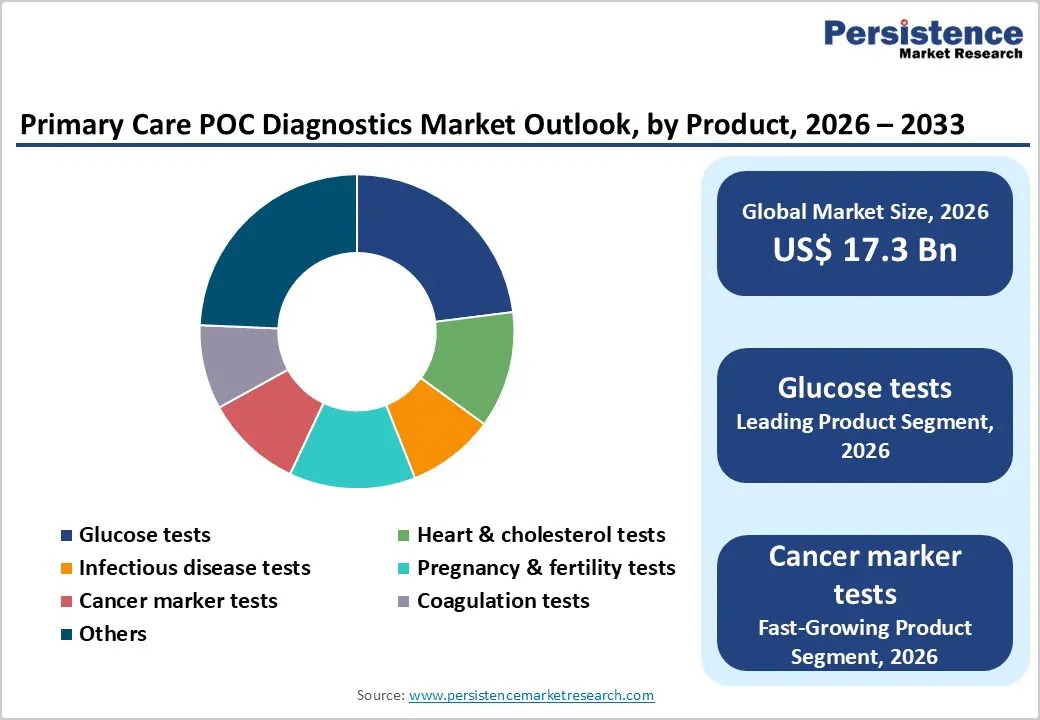

The global primary care POC diagnostics market is expected to be valued at US$ 17.3 billion in 2026 and projected to reach US$ 26.4 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Market expansion is fundamentally driven by three distinct structural mechanisms rather than incremental demand shifts. First, technological inflection points in high-sensitivity cardiac troponin assays achieving near-perfect correlation with laboratory-based platforms (r = 0.999) enable 1-hour ACS rule-out decision pathways, establishing POC testing as a clinical prerequisite rather than a convenience alternative in emergency medicine. Second, regulatory expansion of CLIA-waived testing, combined with 2025 regulatory updates strengthening Proficiency Testing and personnel qualifications, enables pharmacy and clinic deployment of molecular diagnostics multiplexing (enabling simultaneous influenza/RSV/COVID differentiation and targeted antiviral selection), creating structural demand independent of individual disease prevalence. Third, geographic market asymmetries position Asia Pacific as the fastest-growing region through manufacturing cost convergence, enabling affordable POC deployment across rural primary health centers in China, India, and ASEAN, addressing diagnostic infrastructure gaps affecting over 20 countries facing 20%+ chronic disease premature death risk.

Key Market Highlights

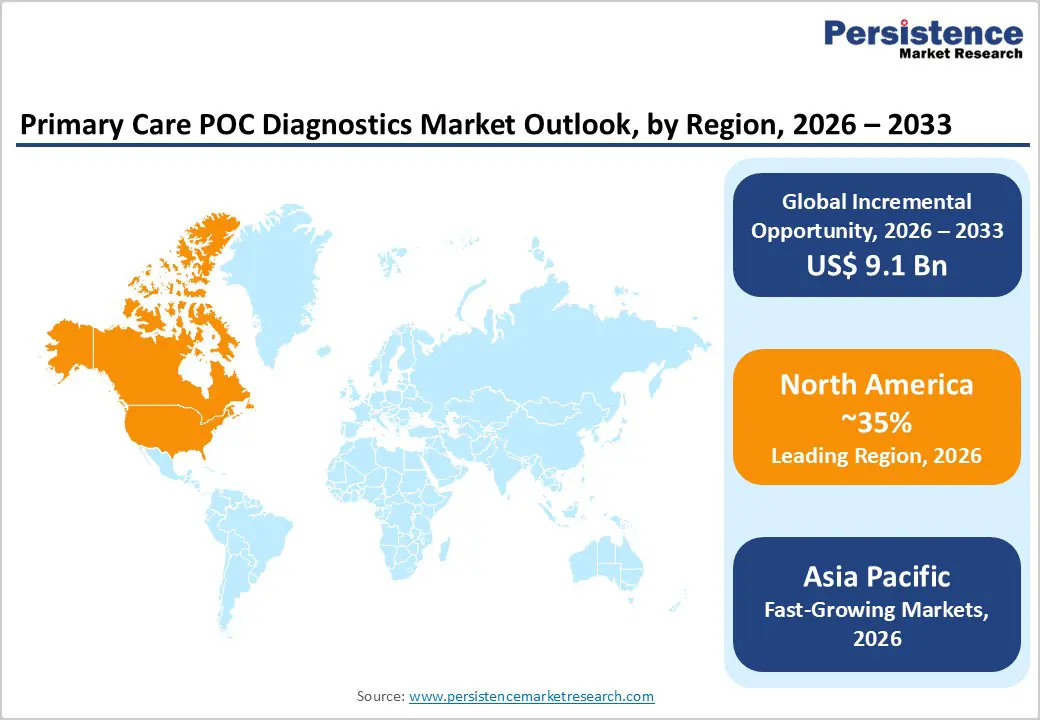

- Leading Region: North America led the market with 35% share in 2025, supported by advanced healthcare infrastructure, strong regulations, robust reimbursement policies, and high disease prevalence across cardiology, endocrinology, and infectious diseases.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by affordable local manufacturing, rising healthcare spending, gaps in diagnostic infrastructure, and government initiatives to expand rural testing.

- Dominant Product: Glucose testing held 23% share in 2025, fueled by widespread diabetes prevalence and recurring test strip demand.

- Fastest-Growing Product: Cancer marker testing is growing fastest, supported by biomarker panel expansion, molecular POC innovations, and rising oncology diagnostic needs.

- Key Opportunity: Molecular POC diagnostics and multiplex pathogen testing offer high growth potential, enabling rapid influenza/RSV/COVID differentiation and pandemic-ready triage, with the market expected to grow from USD 4.48B in 2025 to USD 11.03B by 2034.

| Key Insights | Details |

|---|---|

| Primary Care POC Diagnostics Market Size (2026E) | US$ 17.3 billion |

| Market Value Forecast (2033F) | US$ 26.6 billion |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Clinical Validation Convergence Enabling High-Sensitivity POC Assays as Diagnostic Standard of Care in Emergency and Primary Settings

The increasing convergence of clinical validation with high-sensitivity point-of-care (POC) assays is driving the adoption of advanced diagnostics in primary care settings. By ensuring that POC tests deliver accuracy and reliability comparable to centralized laboratories, healthcare providers can confidently use these tools as part of the standard of care. High-sensitivity assays enable rapid detection of critical conditions, such as infectious diseases, cardiovascular events, and metabolic disorders, allowing timely clinical decisions and immediate intervention at the patient’s first point of contact. This is particularly crucial in emergency and primary care settings where delays in diagnosis can significantly impact patient outcomes. As regulatory frameworks increasingly recognize clinically validated POC tests, their integration into routine workflows is accelerating, supporting broader adoption, improving patient management, and reducing healthcare system burdens. Consequently, demand for reliable, high-performance POC diagnostics is expected to grow rapidly.

Geographic Market Asymmetries: Establishing Asia Pacific as a Structural Growth Vector Through Manufacturing Decentralization and Rural Healthcare Infrastructure Deployment

Geographic market asymmetries are positioning the Asia Pacific region as a critical growth engine for the primary care point-of-care (POC) diagnostics market. Rising healthcare demand in emerging economies, coupled with disparities in access between urban and rural areas, is prompting the strategic decentralization of diagnostic manufacturing and distribution. Establishing local production hubs not only reduces costs and supply chain dependencies but also accelerates the availability of POC tests in remote and underserved regions. Concurrently, governments and private stakeholders are investing heavily in rural healthcare infrastructure, including primary health centers and mobile diagnostic units, to bridge gaps in timely disease detection. This combination of localized manufacturing and enhanced healthcare reach enables rapid deployment of high-quality POC diagnostics, improving patient outcomes and clinical decision-making. As a result, the Asia Pacific is emerging as both a manufacturing powerhouse and a high-demand market, driving sustained expansion in primary care diagnostics.

Restraint- Analytical Sensitivity-Specificity Trade-offs and Clinical Implementation Gaps Constraining Universal POC Adoption in High-Risk Decision Pathways

Despite the rapid advancements in point-of-care (POC) diagnostics, the trade-offs between analytical sensitivity and specificity remain a significant barrier to universal adoption, particularly in high-risk clinical decision pathways. Many POC assays, while offering rapid results, may compromise either sensitivity, leading to false negatives, or specificity, resulting in false positives, creating challenges for clinicians in making critical treatment decisions. These limitations are further compounded by gaps in clinical implementation, including insufficient integration with electronic health records, lack of standardized protocols, and variable staff training in primary and emergency care settings. Consequently, healthcare providers often rely on centralized laboratory testing for confirmation, limiting the use of POC assays as standalone diagnostic tools. These factors collectively constrain market growth, delaying the widespread adoption of POC diagnostics in high-stakes, time-sensitive clinical settings.

Opportunity - Molecular POC Diagnostics and Multiplexed Pathogen Detection Enabling Precision Antiviral Stewardship and Early Outbreak Containment Through Rapid Triage

Molecular POC diagnostics represent the highest-growth opportunity within the Primary Care POC Diagnostics Market, with market expansion from USD 4.48 billion in 2025 to USD 11.03 billion by 2034 at a CAGR exceeding 10%, substantially exceeding the aggregate market growth rate. The clinical mechanism driving this expansion centers on multiplexed respiratory pathogen detection, enabling simultaneous influenza/RSV/COVID differentiation within a single patient encounter, establishing rapid triage capability, eliminating multi-day turnaround delays inherent in laboratory-based molecular testing. The pandemic preparedness imperative, amplified by the COVID-19 experience, drives government and healthcare system investment in decentralized diagnostic capabilities that support early outbreak detection and containment, creating structural demand independent of endemic disease prevalence.

Targeted antiviral selection optimization through pathogen-specific diagnosis enables antimicrobial stewardship protocols, reducing inappropriate antibiotic prescriptions (estimated 30% unnecessary prescribing eliminated through rapid viral diagnosis) while reducing virus transmission through early isolation protocols and enabling treatment initiation with oral antivirals (oseltamivir, baloxavir) within narrow therapeutic windows requiring early diagnosis for efficacy optimization. Pharmacy-led POC model enabling same-visit pathogen diagnosis and antivirals dispensing creates a convenience value proposition supporting consumer willingness-to-pay premium pricing for comprehensive diagnostic-therapeutic packages.

Category-wise Analysis

Product Insights

Glucose testing remains the leading product segment in primary care point-of-care (POC) diagnostics due to the global prevalence of diabetes and rising awareness of metabolic health. Rapid, accurate, and easy-to-use glucose monitors enable timely monitoring of blood sugar levels, empowering both healthcare providers and patients to make immediate treatment decisions. The convenience of POC glucose testing reduces the need for laboratory visits, making it particularly suitable for outpatient clinics, rural health centers, and home care settings. Additionally, ongoing technological advances, including high-sensitivity test strips and connected digital devices, enhance patient adherence and enable real-time data tracking. The segment’s strong clinical utility, combined with widespread adoption across diverse healthcare settings, ensures consistent demand. These factors collectively establish glucose testing as the dominant and most trusted product segment in primary care POC diagnostics.

End-user Insights

Clinics and diagnostic centers are the leading end-use segment in the primary care point-of-care (POC) diagnostics market due to their role as the first point of contact for patients seeking rapid and reliable healthcare services. These settings cater to high patient volumes and require timely diagnostic results to support immediate clinical decision-making, making POC tests an ideal solution. Unlike hospitals, clinics and diagnostic centers focus on outpatient care, preventive health screenings, and chronic disease monitoring, driving frequent use of tests such as glucose, cholesterol, and infectious disease assays. Additionally, their streamlined workflows and shorter turnaround times amplify the value of POC diagnostics in improving operational efficiency and patient satisfaction. The combination of accessibility, high patient throughput, and the need for quick, actionable results ensures that clinics and diagnostic centers remain the dominant end-users in the primary care POC diagnostics market.

Regional Insights

North America Primary Care POC Diagnostics Market Trends and Insights

North America maintains consolidated market dominance with 35% global market share in 2025, driven by advanced healthcare infrastructure, elevated healthcare spending, and strong regulatory framework enabling rapid innovation deployment. The United States leads regional growth through sophisticated reimbursement policies supporting POC testing adoption including CMS coverage for home INR testing in mechanical heart valve and chronic atrial fibrillation populations, private insurance coverage for home glucose monitoring, and accelerating OTC diagnostics adoption post-COVID enabling consumer direct access to pregnancy testing, COVID antigen, and influenza diagnostics.

Healthcare system efficiency drivers, including 1-hour ACS rule-out protocols mandating rapid troponin testing, establish structural demand for high-sensitivity cardiac POC assays in emergency departments, with approximately 8 million suspected ACS presentations annually in U.S. emergency departments creating substantial consumables revenue. Digital health integration through EHR connectivity and telehealth platform bundling accelerates home-based testing adoption, with remote patient monitoring expanding for chronic disease management in cardiology, pulmonology, and primary care settings. Regulatory harmonization through FDA streamlining of CLIA waiver applications for emerging POC technologies establishes rapid approval pathways, enabling manufacturers to deploy novel diagnostics within 12-24 months of laboratory validation, supporting continuous innovation velocity.

Asia Pacific Primary Care POC Diagnostics Market Trends

Asia-Pacific is emerging as a key growth region in the primary care point-of-care (POC) diagnostics market, driven by rising healthcare demand, expanding patient awareness, and improved access in both urban and rural areas. Rapid population growth, increasing prevalence of chronic diseases such as diabetes and cardiovascular disorders, and rising infectious disease incidence are fueling the need for timely and reliable diagnostics. Technological advancements in compact, high-sensitivity POC devices, along with the adoption of digital health solutions, are enhancing clinical efficiency and patient outcomes. Government initiatives to strengthen primary healthcare infrastructure, coupled with localized manufacturing and cost-effective distribution strategies, are further accelerating market adoption. As a result, Asia Pacific is not only witnessing increasing POC deployment in clinics and diagnostic centers but is also poised to become a long-term structural growth driver in the global market.

Competitive Landscape

The primary care POC diagnostics market is highly competitive, characterized by rapid technological innovation and continuous product development. Key players focus on enhancing assay sensitivity, reducing turnaround times, and integrating digital connectivity to improve clinical decision-making. Strategic initiatives such as partnerships, collaborations, and regional expansions are common to strengthen market presence and distribution networks. Companies are also investing in cost-effective, user-friendly devices tailored for both urban and rural healthcare settings.

Key Market Developments

- In April 2024, Roche Diagnostics India launched a point-of-care (PoC) NT-proBNP test specifically aimed at screening diabetes patients who are at risk of cardiovascular diseases (CVD) such as heart failure (HF).

Companies Covered in Primary Care POC Diagnostics Market

- Roche Diagnostics

- BD Biosciences

- Danaher Corporation

- Abbott Laboratories

- Instrumentation Laboratory

- bioMerieux

- Siemens Healthcare

- Quidel Corporation

Frequently Asked Questions

The global primary care POC diagnostics market is projected to achieve a valuation of US$ 17.3 billion in 2026.

Increasing prevalence of diabetes, cardiovascular disorders, respiratory infections, and emerging pathogens is driving continuous demand for rapid diagnostic testing at the primary care level.

North America maintains global market leadership with 35% regional share in 2025, driven by advanced healthcare infrastructure, sophisticated reimbursement policies supporting POC adoption, strong regulatory framework enabling rapid innovation deployment, and substantial disease prevalence establishing structural testing demand across cardiology, endocrinology, and infectious disease applications.

Molecular POC diagnostics and multiplexed pathogen detection constitute the highest-potential growth opportunity, with market projected expansion from USD 4.48 billion in 2025 to USD 11.03 billion by 2034, enabling simultaneous influenza/RSV/COVID differentiation, rapid triage capability, targeted antiviral selection, and pandemic preparedness infrastructure supporting healthcare system resilience.

The Primary Care POC Diagnostics Market is dominated by Roche Diagnostics, BD Biosciences, Danaher Corporation, Abbott Laboratories, and Siemens Healthcare.