- Healthcare Services

- Medical Equipment Calibration Services Market

Medical Equipment Calibration Services Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Medical Equipment Calibration Services Market by Service (In-house, Third-party Services, and Original Equipment Manufacturer (OEM)), by End User (Hospitals, Clinical Laboratories, and Others), and Regional Analysis from 2026 to 2033

Medical Equipment Calibration Services Market Size and Trends Analysis

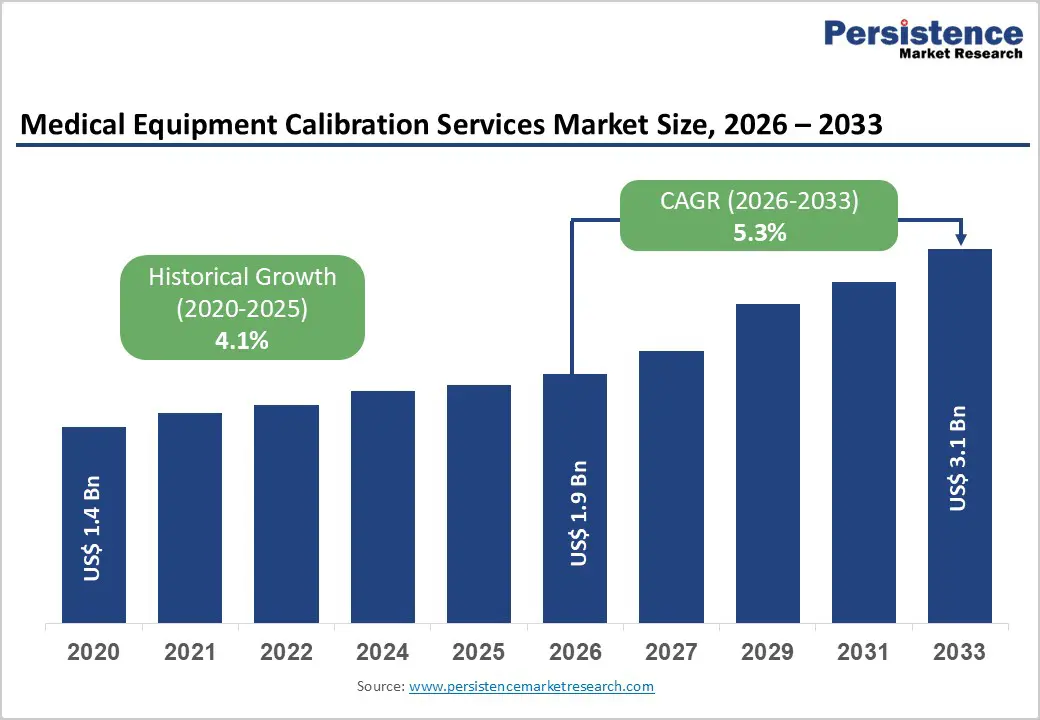

The global medical equipment calibration services market size is estimated to grow from US$ 1.9 Bn in 2026 to US$ 3.1 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for medical equipment calibration services is rising steadily, driven by the expanding deployment of advanced medical devices across hospitals, diagnostic laboratories, and outpatient care settings. Increasing emphasis on patient safety, diagnostic accuracy, and regulatory compliance is compelling healthcare providers to adopt routine and certified calibration practices. Growing procedure volumes, higher utilization rates of imaging systems, patient monitors, infusion devices, and laboratory analyzers, and stricter accreditation requirements are reinforcing sustained demand. Rising healthcare expenditure, modernization of healthcare infrastructure, and broader adoption of digital and automated medical technologies are further accelerating service uptake.

Continuous advancements in device complexity, software-driven diagnostics, and connected medical equipment are increasing calibration frequency and technical requirements. In parallel, growing awareness among healthcare administrators regarding risk mitigation, audit readiness, and lifecycle management is supporting long-term investment in professional calibration services. Increasing adoption of digital calibration management systems, remote diagnostics, and predictive maintenance tools is also improving service efficiency and compliance outcomes, strengthening overall market growth.

Key Industry Highlights

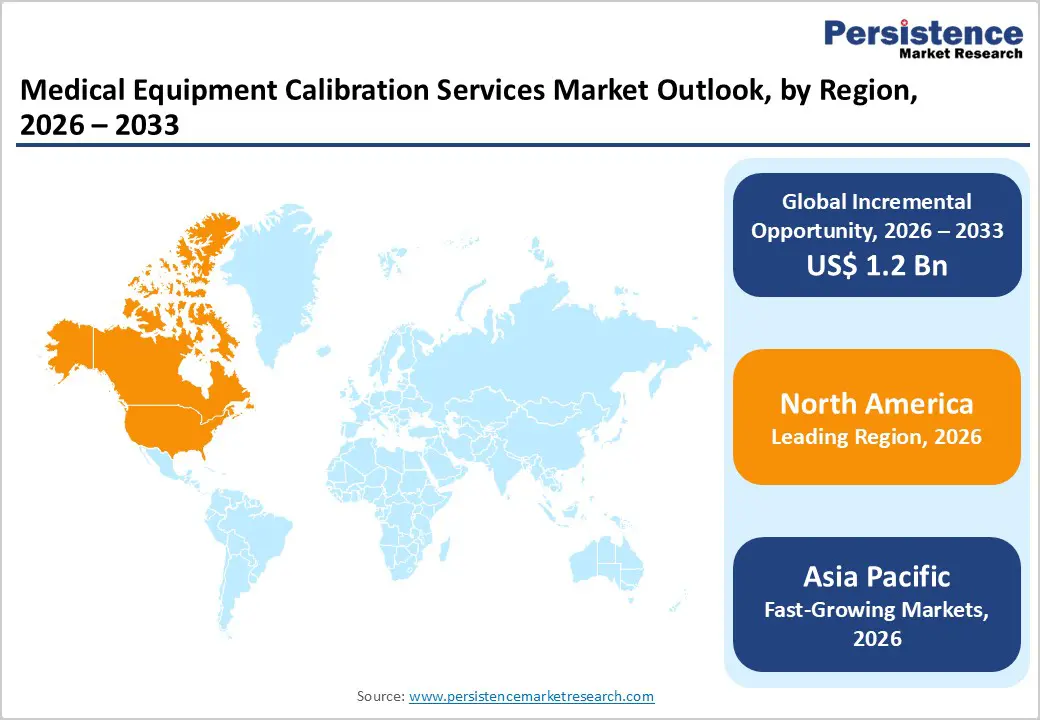

- Leading Region: North America holds the largest share at 47.9%, supported by stringent regulatory standards, advanced healthcare infrastructure, high medical device penetration, strong accreditation requirements, and the presence of major calibration service providers and OEMs.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid healthcare infrastructure development, increasing adoption of advanced medical devices, strengthening regulatory frameworks, and rising investments in quality assurance and patient safety.

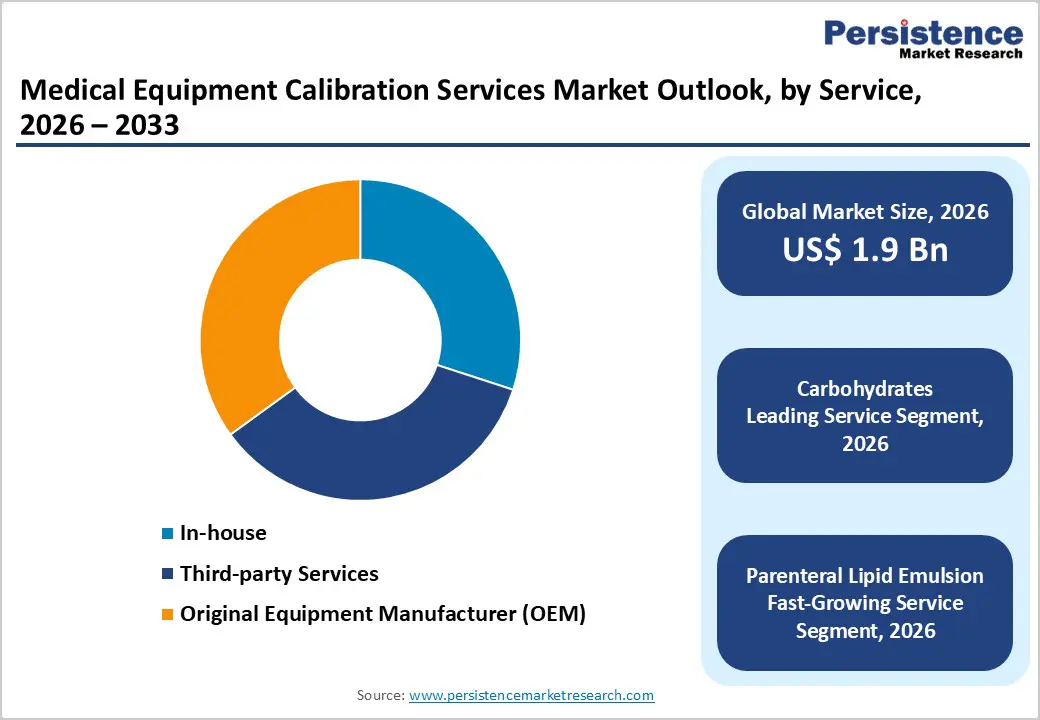

- Leading Service Segment: Original Equipment Manufacturer (OEM) services dominate the market due to device-specific expertise, certified calibration protocols, and strong preference for manufacturer-backed compliance assurance.

- Fastest-Growing Service Segment: In-house calibration is expanding rapidly as large hospitals invest in internal biomedical engineering capabilities to reduce long-term service costs and improve operational control.

- Leading End User Segment: Hospitals remain the top end user, driven by high equipment density, strict compliance requirements, and continuous utilization of mission-critical medical devices.

- Fastest-Growing End User Segment: Clinical laboratories are scaling quickly due to increased diagnostic testing volumes, automation of lab workflows, and heightened accuracy and traceability requirements.

| Global Market Attributes; | Key Insights; |

|---|---|

| Medical Equipment Calibration Services Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Increasing Regulatory Scrutiny and Growing Dependence on Precision Medical Devices

Growth is strongly supported by the rising emphasis on patient safety, clinical accuracy, and regulatory compliance across healthcare systems globally. Hospitals, diagnostic laboratories, and outpatient facilities are operating under increasingly stringent standards imposed by regulatory authorities, accreditation bodies, and insurance providers, all of which mandate routine calibration of medical equipment. The expanding use of high-precision devices—such as imaging systems, patient monitoring equipment, infusion pumps, and automated diagnostic analyzers—has heightened the importance of maintaining measurement accuracy and functional reliability. Even minor deviations in device performance can lead to diagnostic errors, treatment inaccuracies, and legal liabilities, reinforcing the need for professional calibration services.

Additionally, the global expansion of healthcare infrastructure and rising procedural volumes are increasing equipment utilization rates, accelerating wear and drift, and shortening calibration cycles. Adoption of advanced technologies, including digital imaging, AI-enabled diagnostics, and connected medical devices, further intensifies calibration requirements due to their technical complexity. Healthcare providers are also prioritizing risk mitigation and audit readiness, driving demand for documented, traceable, and standards-compliant calibration. Together, these factors are sustaining long-term demand for reliable calibration services across clinical environments.

Restraints – Cost Pressures, Skilled Workforce Gaps, and Operational Disruptions

Market expansion is constrained by cost-related and operational challenges. Calibration services, particularly for high-end or mission-critical equipment, can represent a significant recurring expense for healthcare providers operating under budgetary pressure. Smaller hospitals, standalone diagnostic centers, and clinics often struggle to balance compliance requirements with limited capital and operating budgets, leading to delayed or infrequent calibration cycles. In cost-sensitive regions, calibration is sometimes deprioritized in favor of immediate clinical needs, increasing reliance on in-house capabilities that may lack advanced expertise.

Moreover, the shortage of skilled and certified calibration professionals, especially in emerging markets. Maintaining a trained workforce capable of servicing complex, multi-vendor equipment requires continuous investment in training and certification. Additionally, calibration activities can disrupt clinical workflows, as equipment downtime affects patient throughput and operational efficiency. Scheduling challenges, particularly in high-utilization settings, further complicate service delivery. Variability in regulatory enforcement across regions also leads to inconsistent adoption, while evolving standards require ongoing process updates. Collectively, these factors moderate market penetration and slow adoption among resource-constrained healthcare facilities.

Opportunity – Outsourcing Trends, Digital Calibration Platforms, and Emerging Market Expansion

Significant growth opportunities are emerging as healthcare providers increasingly outsource non-core technical functions to specialized service providers. Outsourcing calibration allows hospitals and laboratories to reduce internal staffing burdens, improve compliance consistency, and access multi-vendor expertise through long-term service contracts. Demand for third-party and hybrid service models is rising, particularly among mid-sized facilities seeking cost efficiency without compromising quality.

Technological advancement presents another major opportunity. Digital calibration management systems, cloud-based documentation, predictive maintenance, and remote diagnostics are transforming service delivery by improving traceability, reducing downtime, and enabling proactive equipment management. These solutions align well with broader healthcare digitization and value-based care models. Additionally, rapid healthcare infrastructure development in emerging economies is expanding the installed base of medical devices, creating sustained demand for calibration services. Governments are strengthening regulatory frameworks and quality standards, accelerating formal adoption of calibration practices. Strategic partnerships with OEMs, hospital networks, and diagnostic chains, combined with localized service models, are expected to unlock new revenue streams and support long-term market growth.

Category-wise Analysis

By Service, Original Equipment Manufacturer (OEM) Lead Due to Device-Specific Accuracy and Regulatory Assurance

The Original Equipment Manufacturer (OEM) segment is projected to dominate the global medical equipment calibration services market in 2026, accounting for a revenue share of 35.0 %. This leadership is primarily attributed to OEMs’ deep technical expertise, proprietary calibration protocols, and direct access to original device specifications. Healthcare providers increasingly rely on OEM calibration services to ensure optimal device performance, maintain warranty validity, and comply with stringent regulatory and accreditation standards. OEMs offer standardized, traceable, and manufacturer-certified calibration, which is critical for high-value and complex equipment such as imaging systems, patient monitors, and diagnostic analyzers. Additionally, bundled service contracts, preventive maintenance agreements, and lifecycle management offerings strengthen long-term relationships with hospitals and laboratories. Growing adoption of advanced and digitally enabled medical devices further reinforces demand for OEM-led calibration, as end users prioritize accuracy, safety, and regulatory compliance over cost considerations. Continuous innovation, remote diagnostics, and software-enabled calibration capabilities further support the dominant position of the OEM segment globally.

By End Users, Hospitals Lead Through High Equipment Density and Strict Compliance Requirements

The hospitals segment is projected to dominate the global medical equipment calibration services market in 2026, accounting for a revenue share of 45.0 %. This dominance is driven by the extensive use of diverse medical equipment across departments such as radiology, intensive care, surgery, and diagnostics, all of which require routine and precise calibration. Hospitals operate under strict regulatory frameworks and accreditation requirements, necessitating regular calibration to ensure patient safety, clinical accuracy, and operational reliability. The presence of high-cost and mission-critical equipment increases dependence on professional calibration services, including OEM and certified third-party providers. Centralized biomedical engineering departments, structured maintenance schedules, and long-term service contracts further contribute to higher spending levels. Additionally, large patient volumes, complex clinical workflows, and the need for uninterrupted equipment availability reinforce the importance of timely calibration. Hospitals also prioritize documentation, traceability, and audit readiness, supporting sustained demand for high-quality calibration services and reinforcing their leading position within the end-user landscape.

Region-wise Insights

North America Medical Equipment Calibration Services Market Trends

North America is expected to dominate the global medical equipment calibration services market with a value share of 47.9 % in 2026, led primarily by the United States. The region benefits from a highly developed healthcare infrastructure, widespread deployment of advanced medical technologies, and strict regulatory oversight by bodies such as the FDA, CMS, and accreditation organizations. Hospitals and laboratories in North America maintain rigorous equipment maintenance and calibration protocols to meet patient safety, quality assurance, and compliance standards. High adoption of sophisticated diagnostic imaging systems, life-support equipment, and automated laboratory instruments significantly increases calibration frequency and service demand.

The strong presence of leading OEMs, specialized third-party service providers, and well-established biomedical engineering capabilities further strengthens market growth. Additionally, favorable reimbursement structures, high healthcare spending, and increasing focus on risk management and liability reduction support sustained investment in calibration services. Integration of digital calibration records, remote monitoring, and predictive maintenance solutions is further enhancing service efficiency and reinforcing North America’s leadership position.

Europe Medical Equipment Calibration Services Market Trends

The Europe medical equipment calibration services market is expected to grow steadily, supported by a mature healthcare system, stringent regulatory frameworks, and increasing emphasis on patient safety and quality assurance. Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate consistent demand due to widespread adoption of advanced medical devices across public and private healthcare facilities. Compliance with EU Medical Device Regulation (MDR), ISO standards, and national accreditation requirements necessitates regular and certified calibration services. Public healthcare systems and centralized procurement models promote standardized maintenance and calibration practices, driving stable service demand.

The region also benefits from a strong presence of OEM service networks and certified third-party providers offering multi-vendor calibration solutions. Growing investments in diagnostic modernization, laboratory automation, and digital health infrastructure further support market expansion. Additionally, increasing focus on cost optimization is encouraging selective outsourcing of calibration services, while outcome-based healthcare models reinforce the importance of equipment accuracy and reliability across Europe.

Asia Pacific Medical Equipment Calibration Services Market Trends

The Asia Pacific medical equipment calibration services market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by rapid healthcare infrastructure expansion and increasing adoption of modern medical technologies. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are witnessing significant growth in hospitals, diagnostic laboratories, and specialty clinics, increasing demand for calibration services. Rising healthcare investments, growing private sector participation, and expanding medical device penetration are key contributors.

Governments across the region are strengthening regulatory frameworks and quality standards, prompting healthcare providers to adopt routine calibration practices. Cost-sensitive markets are increasingly leveraging third-party service providers and localized calibration solutions to balance affordability and compliance. The availability of skilled biomedical engineers, growth of domestic device manufacturing, and increasing awareness of equipment accuracy are further supporting market growth. Gradual adoption of digital maintenance systems, remote calibration tools, and service automation is expected to enhance efficiency and sustain long-term expansion across the Asia Pacific region.

Market Competitive Landscape

The global medical equipment calibration services market is highly competitive, with key players such as Novo TEKTRONIX, INC., Fluke Biomedical, Biomedical Technologies S.L., NS Medical Systems, Transcat, Inc., and JM Test Systems, along with Nordisk, GSK Plc, VIVUS LLC, and Currax Pharmaceuticals, competing through strong brand recognition, extensive service portfolios, wide geographic reach, and technical expertise in equipment accuracy and compliance management.

Companies emphasize expanding multi-vendor calibration capabilities, enhancing service turnaround times, and ensuring compliance with international regulatory and accreditation standards. Strategic priorities include adoption of digital calibration management platforms, remote and predictive maintenance solutions, workforce training and certification, and expansion into emerging healthcare markets. Strengthening long-term service contracts, OEM collaborations, and partnerships with hospitals, clinical laboratories, and diagnostic centers remains central to sustaining competitive advantage and long-term market growth.

Key Industry Developments:

- In January 2026, India advanced its national quality infrastructure with the launch of two apex-level calibration facilities at the CSIR–National Physical Laboratory, reinforcing the institute’s long-standing role as the country’s National Metrology Institute. With over eight decades of service, CSIR-NPL has been instrumental in supporting accurate and traceable measurements across research institutions, industrial operations, municipal services, and strategic sectors, underpinning product quality, fair trade practices, environmental monitoring, and consumer safety.

- In April 2024, IIT Madras introduced India’s first mobile medical devices calibration facility under its “Anaivarukkum IITM” initiative, aimed at improving access to certified calibration and maintenance of critical medical equipment across the country, especially in underserved areas.

Companies Covered in Medical Equipment Calibration Services Market

- TEKTRONIX, INC.

- Fluke Biomedical

- Biomedical Technologies S.L.

- NS Medical Systems

- Transcat, Inc.

- JM Test Systems

- JPen Medical Ltd

- Tag Medical

- NES GROUP MEDICAL

- Helix Pvt

- Angelus Medical and Optical

- Universal calibration services (P) Ltd.

- KTPL Technologies (P) Ltd.

- Trescal

- Others

Frequently Asked Questions

The global medical equipment calibration services market is projected to be valued at US$ 1.9 Bn in 2026.

The global medical equipment calibration services market is driven by stringent regulatory compliance, rising use of high-precision medical devices, and growing focus on patient safety and diagnostic accuracy drive demand for medical equipment calibration services.

The global medical equipment calibration services market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Rapid healthcare infrastructure expansion in emerging markets and increasing outsourcing to third-party, digital, and remote calibration services create strong growth opportunities.

TEKTRONIX, INC., Fluke Biomedical, Biomedical Technologies S.L., NS Medical Systems, Transcat, Inc., and JM Test Systems are some of the key players in the medical equipment calibration services market.