- Healthcare Services

- Refurbished Medical Equipment Market

Refurbished Medical Equipment Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Refurbished Medical Equipment Market by Product (Medical Imaging Equipment, Operating Room & Surgical Equipment, Critical Care Devices, Patient Monitoring Devices, Neurology Devices, Cardiovascular Devices, Endoscopy Devices, and Others), by Application (Cardiology, Neurology, Oncology, Orthopedics, Gynecology, and Others), End-user, and Regional Analysis from 2026 - 2033

Refurbished Medical Equipment Market Share and Trend Analysis

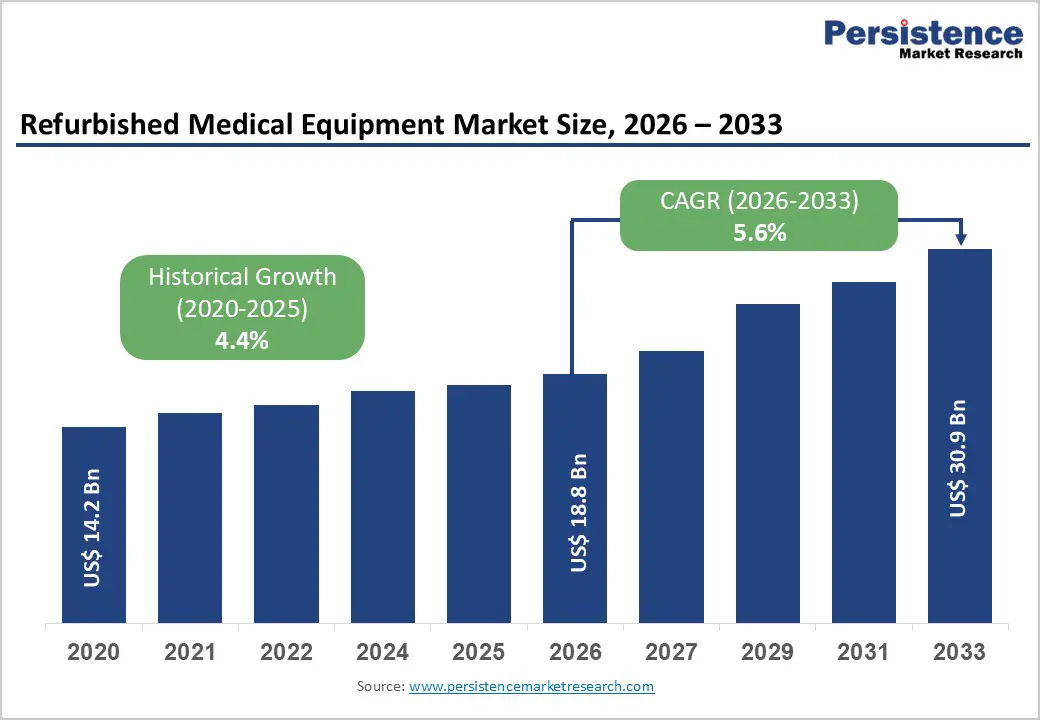

The global refurbished medical equipment market size is estimated to grow from US$ 18.8 billion in 2026 to US$ 30.9 billion by 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033. Healthcare providers worldwide are increasingly prioritizing cost-efficient capital procurement strategies, driving steady expansion in demand for refurbished medical equipment. Budget constraints across public and private hospitals, coupled with the high acquisition cost of new imaging and surgical systems, are accelerating preference for certified pre-owned MRI, CT, ultrasound, cath lab, patient monitoring, and anesthesia systems.

Rising diagnostic volumes linked to cardiovascular disorders, oncology cases, neurological conditions, and trauma incidents are sustaining equipment utilization rates across both mature and developing healthcare markets. Healthcare infrastructure expansion in emerging economies is further amplifying adoption, as refurbished systems enable faster deployment at significantly lower capital intensity. Improvements in refurbishment standards, including OEM-compliant component replacement, recalibration, performance validation, and extended warranty coverage, have strengthened buyer confidence. Sustainability priorities and circular procurement initiatives aimed at reducing medical e-waste are also supporting the lifecycle extension of high-value assets. Additionally, flexible financing structures, equipment leasing models, and service-backed resale programs are improving accessibility, reinforcing long-term global market progression.

Key Industry Highlights:

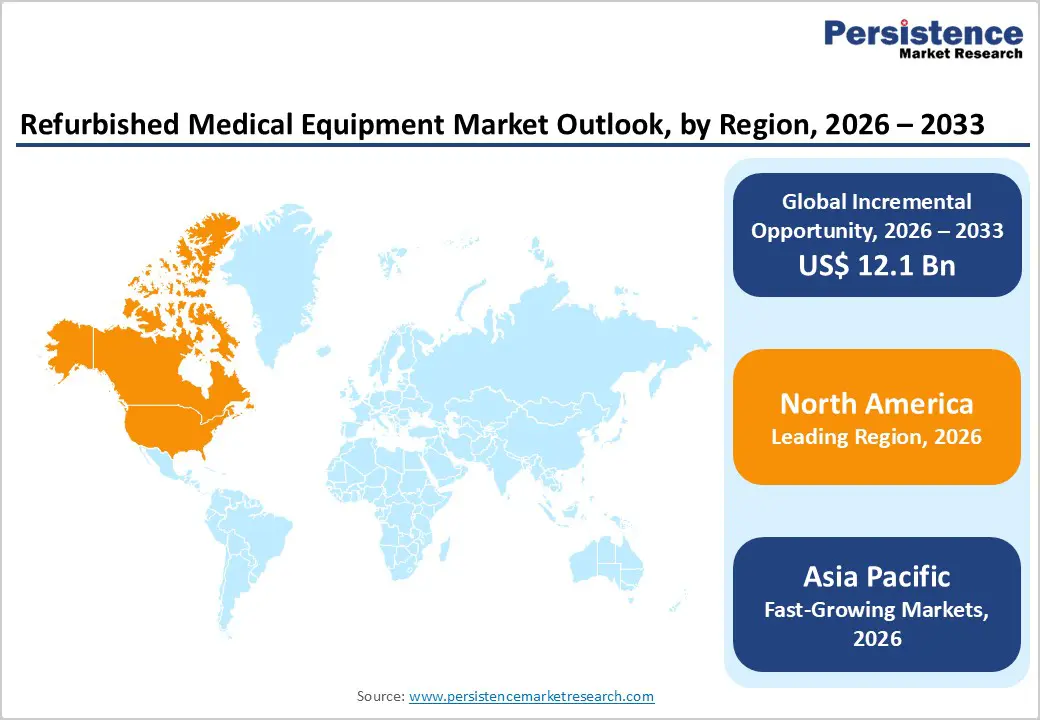

- Leading Region: North America commands 47.3% share, underpinned by structured secondary equipment channels, strong regulatory oversight, advanced hospital networks, and consistent technology upgrade cycles generating resale supply.

- Fastest-Growing Region: Asia Pacific is advancing at the fastest pace, supported by healthcare infrastructure scaling, expanding diagnostic networks, rising chronic disease burden, and increasing affordability-driven procurement strategies.

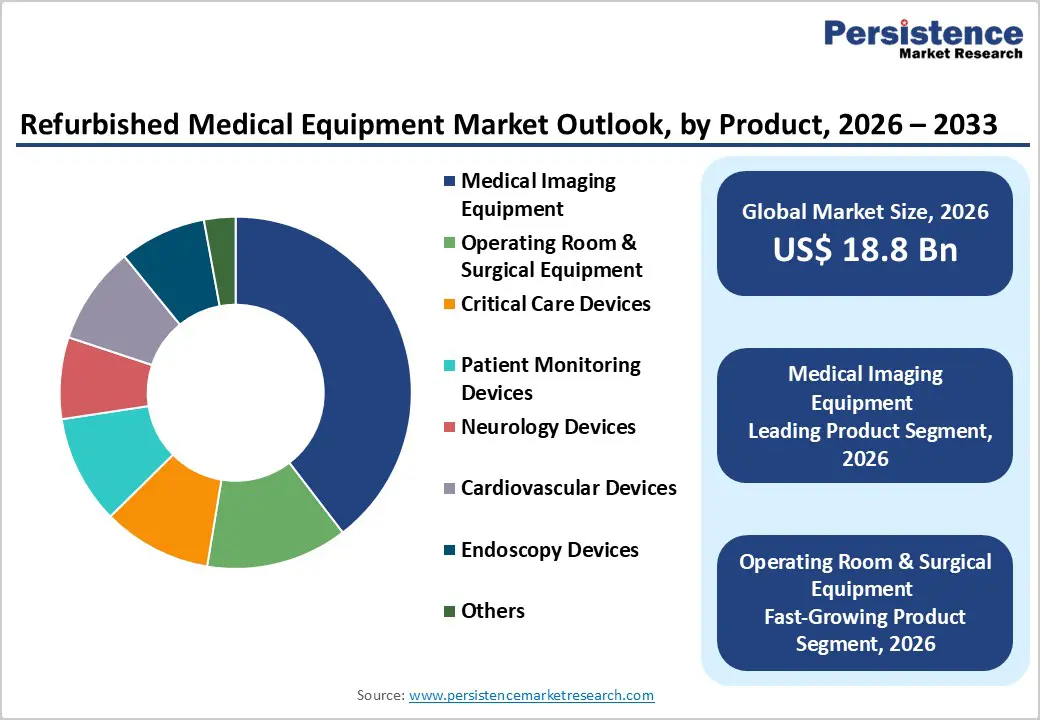

- Leading Product Segment: Medical imaging equipment accounts for 39.6% share, reflecting high replacement value, sustained imaging demand, and strong institutional preference for refurbished MRI and CT platforms.

- Fastest-Growing Product Segment: Operating room & surgical equipment is witnessing accelerated uptake as facilities optimize surgical capacity through cost-effective anesthesia systems, C-arms, and operating tables.

- Leading Application Segment: Cardiology leads with 20.0% share, driven by extensive utilization of refurbished cath labs, cardiac ultrasound, and monitoring systems for cardiovascular diagnostics and interventions.

- Fastest-Growing Application Segment: Oncology is expanding quickly due to increasing imaging-based cancer detection volumes and rising investment in affordable radiology infrastructure.

| Key Insights | Details |

|---|---|

|

Refurbished Medical Equipment Market Size (2026E) |

US$ 18.8 Bn |

|

Market Value Forecast (2033F) |

US$ 30.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Dynamics

Driver - Rising Healthcare Cost Containment and Expanding Demand for Affordable Diagnostic Infrastructure

Escalating healthcare expenditure globally has compelled hospitals, diagnostic centers, and specialty clinics to adopt cost-optimization strategies without compromising clinical efficiency. Capital-intensive medical technologies such as MRI systems, CT scanners, cath lab units, ventilators, and anesthesia machines require substantial upfront investment, creating procurement challenges for mid-sized and public healthcare institutions. Refurbished medical equipment provides a financially viable alternative, often priced 30–60% lower than new systems while maintaining comparable performance standards when certified and quality tested.

Growing demand for diagnostic imaging driven by increasing prevalence of cardiovascular diseases, cancer, neurological disorders, and trauma cases further strengthens equipment utilization rates. In parallel, healthcare infrastructure expansion in emerging economies necessitates rapid capacity building, where refurbished systems enable faster deployment within constrained budgets. Improvements in refurbishment processes including OEM-compliant part replacement, software upgrades, recalibration, and performance validation have significantly enhanced buyer confidence. Additionally, sustainability initiatives promoting circular economy practices and medical waste reduction encourage lifecycle extension of high-value devices. Leasing models, warranty-backed resale programs, and structured asset recovery channels are also accelerating adoption across institutional buyers worldwide.

Restraints - Regulatory Stringency, Perceived Quality Concerns, and Limited Financing Access

Despite strong demand momentum, market expansion faces structural constraints arising from regulatory variability and perception-driven concerns. Medical device compliance frameworks differ significantly across countries, and inconsistent classification of refurbished systems complicates cross-border trade. Obligations related to re-certification, labeling, traceability, and post-market surveillance can prolong transaction cycles and elevate operational costs for refurbishers. In February 2026, India’s Union Health Ministry constituted a committee to frame a dedicated regulatory policy for refurbished medical devices, triggering debate between domestic manufacturers and multinational firms. Local industry stakeholders opposed easing import norms, citing patient safety considerations and potential implications for the “Make in India” initiative illustrating how evolving national policies can materially influence competitive dynamics and market access.

Beyond regulatory factors, perception-related risks continue to shape procurement decisions. Concerns regarding equipment reliability, residual component life, and software compatibility affect adoption, particularly in high-acuity departments such as intensive care and interventional cardiology. Limited access to structured financing restricts smaller hospitals and rural facilities from capitalizing on refurbished alternatives. Additionally, rapid technological innovation shortens resale cycles and complicates inventory valuation, while cybersecurity vulnerabilities in legacy digital systems and interoperability challenges with modern hospital IT infrastructure further temper adoption in technologically advanced healthcare settings.

Opportunity - Emerging Market Penetration, Digital Upgrades, and Sustainable Procurement Models

Significant growth opportunities are emerging from expanding healthcare infrastructure across Asia Pacific, Latin America, Africa, and parts of the Middle East, where demand for affordable diagnostic and surgical equipment is rising rapidly. Governments and private healthcare providers are prioritizing capacity expansion, particularly in radiology, cardiology, and critical care departments. Refurbished systems enable rapid scaling at lower capital intensity, making them highly attractive for secondary cities and rural healthcare programs.

Technological retrofitting presents another transformative avenue, as older imaging platforms can be upgraded with advanced software, AI-enabled image reconstruction tools, dose-reduction technologies, and remote monitoring capabilities. Such digital enhancements extend equipment lifespan while improving clinical output and workflow efficiency. Increasing emphasis on sustainability and environmental governance is also driving procurement shifts toward circular economy models that reduce electronic waste and carbon footprint. Strategic collaborations between OEMs and certified third-party refurbishers enhance credibility, service assurance, and global distribution reach. Additionally, subscription-based maintenance contracts, equipment-as-a-service models, and cross-border resale platforms create recurring revenue streams and strengthen long-term market scalability.

Category-wise Analysis

By Product, Medical Imaging Equipment Leads Due to High Capital Cost Savings and Strong Replacement Demand

Medical imaging equipment is projected to lead the global refurbished medical equipment market in 2026, accounting for a revenue share of 39.6%, primarily driven by the high capital cost of new imaging systems and sustained demand for diagnostic capacity expansion. This segment includes refurbished MRI systems, CT scanners, ultrasound systems, C-arms, and X-ray equipment widely used across hospitals and diagnostic centers. Healthcare providers increasingly prefer refurbished imaging systems to optimize capital expenditure while maintaining diagnostic accuracy and regulatory compliance. Growing imaging volumes linked to chronic diseases, trauma cases, oncology diagnostics, and cardiovascular conditions further support demand. Certified refurbishment processes, software upgrades, detector replacements, and OEM-standard quality testing enhance system reliability and lifecycle extension. Emerging markets particularly favor refurbished imaging solutions to bridge infrastructure gaps affordably. Continuous advancements in digital imaging, AI-enabled workflow optimization, and remote servicing capabilities further reinforce this segment’s revenue leadership globally.

By Application, Cardiology Leads Owing to High Diagnostic Imaging and Interventional Equipment Utilization

The cardiology segment is expected to dominate the global refurbished medical equipment market in 2026, capturing a revenue share of 20.0% due to high utilization of imaging and interventional systems in cardiovascular diagnosis and treatment. Refurbished cath lab systems, cardiac ultrasound devices, patient monitors, and stress testing equipment are widely adopted to manage rising cardiovascular disease prevalence worldwide. Increasing incidence of coronary artery disease, heart failure, and arrhythmias drives procedural volumes in both developed and emerging economies. Hospitals and specialty cardiac centers leverage refurbished systems to expand capacity without incurring the high cost of new installations. Growing demand for minimally invasive cardiac interventions and real-time imaging guidance further strengthens equipment utilization rates. Additionally, expanding screening initiatives and preventive cardiology programs increase diagnostic imaging requirements. Cost-efficient procurement strategies and improved refurbishment standards position cardiology as the leading application contributor within the refurbished equipment landscape.

By End-user, Hospitals Lead Due to High Equipment Turnover and Multi-Department Utilization

Hospitals are projected to dominate the global refurbished medical equipment market in 2026, accounting for a revenue share of 60.0%, supported by their large-scale procurement capacity and multi-specialty service offerings. Hospitals operate across radiology, cardiology, intensive care, operating rooms, and emergency departments, creating consistent demand for refurbished imaging systems, patient monitors, ventilators, anesthesia machines, and surgical equipment. Budget optimization initiatives and value-based healthcare models encourage hospitals to adopt certified refurbished systems without compromising clinical performance. High patient inflow, emergency care requirements, and expanding diagnostic workloads further drive equipment utilization. Many institutions integrate refurbished devices for secondary departments, rural outreach programs, and capacity expansion projects. Additionally, hospital networks frequently upgrade to next-generation systems, creating a steady supply pipeline for refurbishment. While ambulatory surgical centers and specialty clinics are growing, hospitals remain the primary revenue contributors due to their scale and diversified equipment needs.

Region-wise Insights

North America Refurbished Medical Equipment Market Trends

North America is expected to dominate the global refurbished medical equipment market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from advanced healthcare infrastructure, structured regulatory pathways, and well-established secondary equipment markets. High healthcare expenditure and continuous technology upgrades generate a strong supply of pre-owned imaging and surgical systems suitable for certified refurbishment. Hospitals and diagnostic centers increasingly adopt refurbished equipment to control capital budgets while maintaining compliance with FDA and quality standards.

The U.S. reports substantial volumes of imaging procedures annually, including MRI, CT, and cardiac imaging, supporting sustained equipment utilization. Growth in outpatient imaging centers and ambulatory facilities further expands demand. Additionally, sustainability initiatives and circular procurement models are gaining institutional support, reducing medical e-waste and extending device lifecycles. The presence of leading OEMs and refurbishment specialists strengthens service capabilities, warranty assurance, and technical upgrades. Strong financing options and leasing models further reinforce North America’s leadership position in the refurbished medical equipment market.

Europe Refurbished Medical Equipment Market Trends

The Europe refurbished medical equipment market is expected to grow steadily, supported by cost-containment measures within public healthcare systems and increasing demand for diagnostic modernization. Countries such as Germany, the U.K., France, Italy, and Spain are prioritizing efficient capital allocation while maintaining high standards of clinical care. Budget constraints across public hospitals are encouraging adoption of certified refurbished imaging systems, operating room equipment, and patient monitoring devices. Strict regulatory frameworks emphasizing CE certification, device traceability, and quality compliance enhance physician confidence in refurbished solutions.

Rising chronic disease prevalence, including cardiovascular and oncological conditions, sustains imaging demand across regional healthcare networks. Additionally, expansion of outpatient diagnostic centers and private specialty clinics contributes to equipment procurement growth. Sustainability goals aligned with circular economy policies further promote lifecycle extension of medical devices. Collaboration between OEMs and third-party refurbishers ensures standardized testing and warranty support, enabling consistent adoption across Western and Central European healthcare markets.

Asia Pacific Refurbished Medical Equipment Market Trends

The Asia Pacific refurbished medical equipment market is expected to register a relatively higher CAGR of around 7.6% between 2026 and 2033, driven by expanding healthcare infrastructure and growing demand for affordable diagnostic technologies. Rapid urbanization and increasing healthcare investments across China, India, Japan, South Korea, and Australia are strengthening hospital and imaging center capacity. Many public and private healthcare providers prefer refurbished systems to accelerate infrastructure expansion while managing budget limitations. The rising incidence of chronic diseases, trauma cases, and cardiovascular conditions increases demand for imaging and monitoring equipment.

Government initiatives aimed at improving rural healthcare access further stimulate the procurement of cost-effective refurbished devices. Expansion of private hospital chains and diagnostic networks enhances distribution opportunities for refurbishment providers. Strategic collaborations between global OEMs and regional distributors improve technical servicing and warranty support. As healthcare access broadens and cost-efficiency remains critical, the Asia Pacific is positioned as the fastest-growing regional market globally.

Competitive Landscape

The global refurbished medical equipment market is highly competitive, with strong participation from companies such as GE HealthCare, AGITO Medical, Avante Health Solutions, Block Imaging, Inc., and Siemens Healthineers AG. These players leverage strong brand recognition, global service networks, and technical refurbishment expertise to meet rising demand for cost-effective diagnostic and surgical systems.

Their portfolios emphasize certified refurbishment processes, OEM-compliant parts replacement, performance validation, extended warranties, and lifecycle management services. Continuous quality upgrades, strategic partnerships, regulatory compliance, and adherence to international safety standards remain critical to sustaining competitive advantage.

Key Industry Developments:

- In April 2025, Stryker partnered with Project C.U.R.E. to distribute medical equipment to underserved regions globally, supporting healthcare infrastructure in low-resource settings and reinforcing the growing importance of equipment lifecycle extension and secondary market redistribution within the refurbished medical equipment ecosystem.

- In July 2024, the World Health Organization launched MeDevIS (Medical Devices Information System), an online open-access platform serving as the first global clearinghouse for medical device information. The system is intended to assist governments, regulatory authorities, and healthcare providers in making informed decisions regarding the selection, procurement, and utilization of medical devices for disease diagnosis, testing, and treatment.

- In May 2023, Siemens Healthineers AG and CommonSpirit Health agreed to acquire Block Imaging, Inc., a leading provider of refurbished medical imaging equipment, parts, and services. The joint acquisition aimed to strengthen sustainable medical equipment solutions by expanding access to multi-vendor refurbished imaging parts and lowering total cost of ownership for hospitals and health systems. Under the agreement, Block Imaging will continue to supply refurbished equipment and components, enhancing lifecycle management, encouraging reuse, and supporting demand for cost-effective diagnostic infrastructure across healthcare facilities.

- In October 2023, GE HealthCare collaborated with reLink Medical to introduce a structured medical equipment disposition program that enables healthcare providers to resell, recycle, or redeploy surplus devices. The initiative strengthens organized secondary supply channels, improves asset recovery efficiency, and supports circular lifecycle management

Companies Covered in Refurbished Medical Equipment Market

- GE HealthCare

- AGITO Medical

- Avante Health Solutions

- Block Imaging, Inc.

- Siemens Healthineers AG

- EverX Pyt. Ltd.

- Koninklijke Philips N.V.

- Soma Tech Intl.

- Cambridge Scientific

- CANON MEDICAL SYSTEMS CORPORATION

- Hilditch Group Ltd

- Master Medical Systems LLP

- Integrity Medical Systems, Inc.

- KUBTEC®

- Others

Frequently Asked Questions

The global refurbished medical equipment market is projected to be valued at US$ 18.8 Bn in 2026.

Rising healthcare cost pressures and capital budget constraints are accelerating adoption of lower-cost, quality-certified refurbished medical equipment globally.

The global refurbished medical equipment market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Expansion of healthcare infrastructure in emerging markets and growing demand for sustainable, circular procurement models create significant growth opportunities.

GE HealthCare, AGITO Medical, Avante Health Solutions, Block Imaging, Inc., and Siemens Healthineers AG are some of the key players in the refurbished medical equipment market.