- Healthcare Services

- Medical Automation Market

Medical Automation Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Medical Automation Market by Product (Automated Laboratory Solutions, Pharmacy Automation Systems, Therapeutic Automation, Medical Imaging Automation, and Healthcare Workflow & Software Automation), by Application (Diagnostics & Monitoring, Surgery & Therapeutic Automation, Medication Management / Pharmacy Automation, Patient Monitoring & Tele-ICU, Administrative & Workflow Automation, and Medical Logistics & Training Automation) End-user, and Regional Analysis from 2026 to 2033

Medical Automation Market Share and Trend Analysis

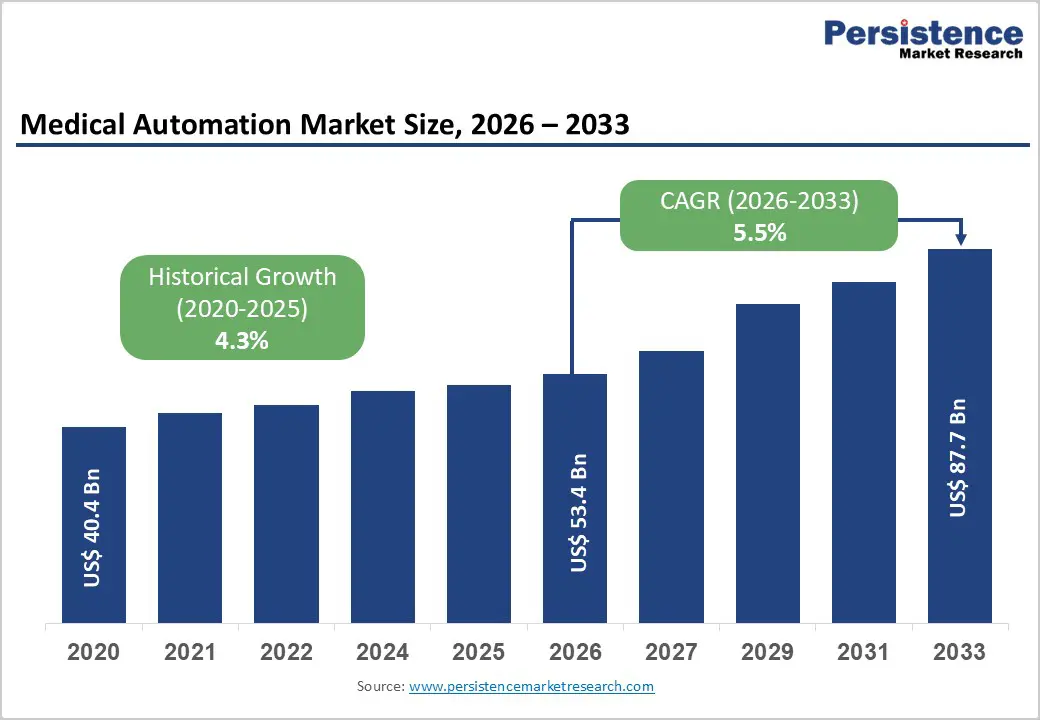

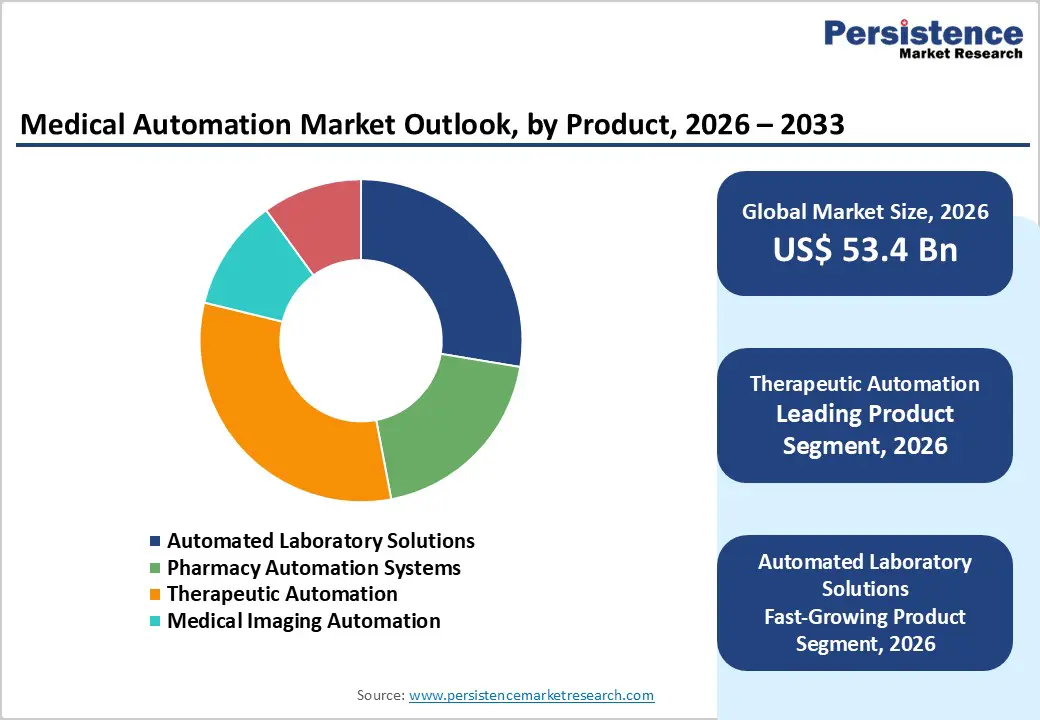

The global medical automation market size is estimated to grow from US$ 53.4 billion in 2026 to US$ 87.7 billion by 2033. The market is projected to record a CAGR of 5.5% during the forecast period from 2026 to 2033.

Rising pressure on global healthcare systems to improve efficiency, accuracy, and patient safety is significantly accelerating the adoption of medical automation technologies. Hospitals, diagnostic laboratories, and clinical facilities are increasingly implementing automated systems to manage growing patient volumes while reducing manual workload and operational errors. Automation platforms such as robotic-assisted surgical systems, automated laboratory analyzers, and intelligent medication dispensing technologies enable healthcare providers to streamline complex clinical workflows and enhance treatment precision. These technologies also support faster diagnostic processes and more reliable patient monitoring, allowing clinicians to make informed decisions in real time.

Continuous innovation in artificial intelligence, robotics, and digital health infrastructure is further transforming healthcare delivery models. Modern healthcare facilities are integrating automated imaging analysis, workflow management platforms, and smart patient monitoring systems to improve clinical productivity and quality of care. In addition, governments and healthcare organizations worldwide are investing in hospital modernization initiatives that emphasize digital connectivity and automated clinical operations. Increasing adoption of data-driven healthcare practices, along with expanding access to advanced medical technologies in emerging economies, is strengthening the global shift toward automated healthcare environments.

Key Industry Highlights:

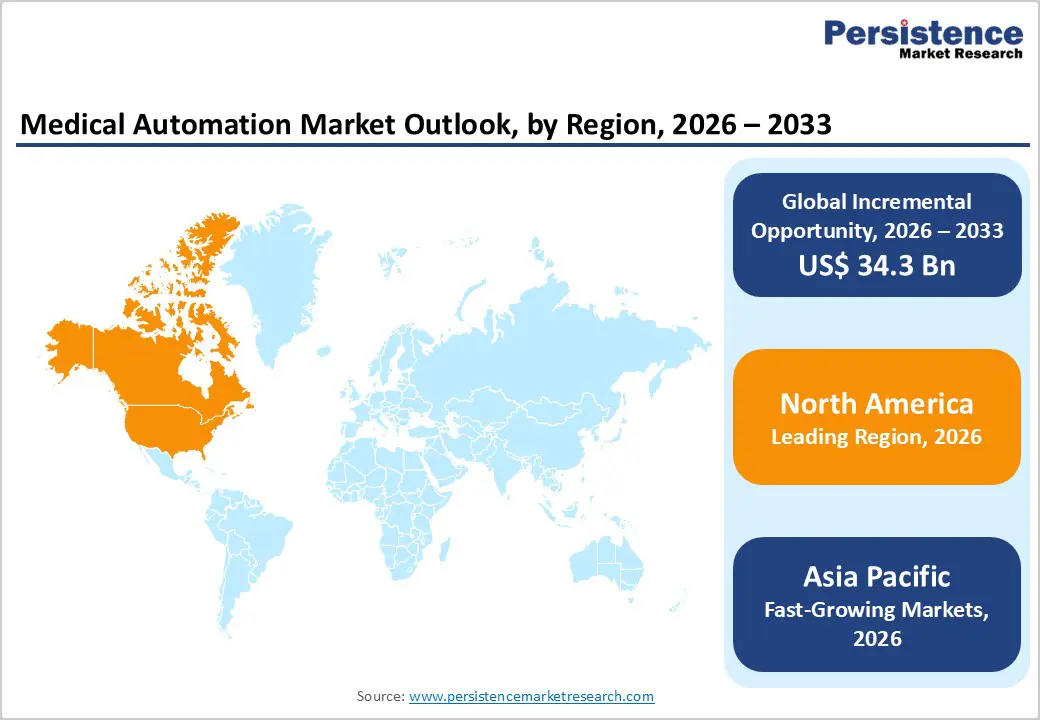

- Leading Region: North America accounts for 46.7% of the global market, supported by strong healthcare infrastructure, early adoption of advanced automation technologies, high healthcare spending, and the presence of major medical technology innovators.

- Fastest-Growing Region: Asia Pacific is witnessing the most rapid expansion due to improving healthcare infrastructure, increasing government investment in hospital modernization, rising patient volumes, and growing adoption of digital healthcare technologies.

- Leading Product Segment: Therapeutic automation holds the largest share as automated surgical systems, precision treatment platforms, and robotic-assisted technologies significantly enhance procedural accuracy and clinical efficiency.

- Fastest-Growing Product Segment: Automated laboratory solutions are gaining strong momentum as healthcare facilities increasingly rely on high-throughput automated diagnostic systems to improve testing efficiency and reduce manual processing errors.

- Leading Application Segment: Diagnostics & monitoring captures the largest share of the market as automation plays a critical role in clinical data analysis, laboratory testing, and continuous patient monitoring across healthcare facilities.

- Fastest-Growing Application Segment: Surgery & therapeutic automation is experiencing rapid growth as hospitals expand the use of robotic-assisted surgical systems and automated treatment platforms to enhance procedural outcomes and reduce surgical variability.

| Key Insights | Details |

|---|---|

| Medical Automation Market Size (2026E) | US$ 53.4 Bn |

| Market Value Forecast (2033F) | US$ 87.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Increasing Demand for Healthcare Efficiency and Rapid Integration of Intelligent Automation Technologies

Growing pressure on healthcare systems to improve operational efficiency and patient safety is a major factor accelerating the adoption of medical automation technologies. Hospitals, diagnostic laboratories, and clinical centers worldwide are handling increasing patient volumes while facing workforce shortages and rising operational costs. Automation platforms help healthcare providers streamline complex clinical workflows, reduce manual intervention, and minimize the risk of human error during critical processes such as laboratory testing, medication dispensing, and surgical procedures.

Additionally, continuous technological progress in artificial intelligence, robotics, and data analytics is transforming how healthcare services are delivered. Automated laboratory analyzers, robotic-assisted surgical systems, and AI-powered diagnostic tools enable clinicians to process large volumes of clinical data quickly and with higher precision. These technologies also support faster decision-making and improved treatment planning. Furthermore, healthcare institutions are increasingly adopting digital workflow platforms that integrate patient records, diagnostic information, and real-time monitoring data. Governments and healthcare organizations are also investing heavily in digital health infrastructure to modernize hospitals and improve clinical productivity. Collectively, these factors are strengthening the global shift toward automation-driven healthcare environments.

Restraints - High Implementation Costs and Integration Challenges in Healthcare Facilities

Despite its advantages, the adoption of medical automation systems can be constrained by significant financial and operational barriers. Advanced automation technologies often require high initial investment, including the cost of sophisticated equipment, software platforms, system integration, and ongoing maintenance. Hospitals must also allocate resources for infrastructure upgrades and staff training to ensure proper utilization of these technologies. For smaller healthcare facilities and institutions in developing regions, these capital requirements can limit the pace of automation adoption.

Another challenge involves integrating automated systems with existing hospital information technology infrastructure. Many healthcare institutions still rely on legacy systems that may not easily connect with modern automation platforms. This can create interoperability issues, data management complexities, and workflow disruptions during the transition phase. Additionally, concerns related to cybersecurity, patient data protection, and regulatory compliance further complicate large-scale technology deployment. The shortage of skilled professionals capable of managing automated systems also remains a limiting factor in certain regions. Together, these financial, technical, and operational challenges can slow the widespread implementation of automation solutions across global healthcare environments.

Opportunity - Expansion of AI-Driven Healthcare Platforms and Smart Hospital Infrastructure

Rapid progress in digital health technologies is creating substantial opportunities for the growth of the medical automation market. Healthcare providers worldwide are increasingly investing in smart hospital infrastructure that integrates artificial intelligence, robotics, connected devices, and advanced data analytics into clinical operations. These systems enable healthcare institutions to automate routine administrative tasks, optimize clinical workflows, and improve the accuracy of diagnostic and treatment processes. AI-powered diagnostic platforms, automated patient monitoring solutions, and robotic surgical technologies are becoming central components of modern healthcare delivery.

Moreover, the growing adoption of remote patient monitoring and telehealth services is opening new avenues for automation in patient management. Intelligent monitoring systems can continuously track patient vitals and transmit real-time health data to healthcare professionals, enabling earlier detection of complications and more proactive care. Emerging economies are also presenting strong growth potential as governments invest in digital healthcare infrastructure and hospital modernization initiatives. As technologies such as machine learning, robotics, and predictive analytics continue to evolve, automation solutions are expected to play a critical role in improving healthcare efficiency, expanding access to quality medical services, and supporting the transformation toward fully digital healthcare ecosystems.

Category-wise Analysis

By Product Insights

Therapeutic automation is expected to remain the largest product segment in 2026, accounting for 31.8% of total medical automation market revenue. The segment’s strong position is primarily supported by the rapid adoption of robotic-assisted surgical systems, automated infusion technologies, and precision-based treatment delivery platforms. These solutions enable clinicians to perform complex procedures with enhanced accuracy, real-time monitoring, and reduced procedural variability. Robotic systems and automated therapeutic devices assist surgeons in executing delicate operations while minimizing human error and improving patient safety.

Additionally, automation platforms used in therapeutic settings often integrate imaging guidance, sensor-based feedback, and AI-assisted analytics that support improved clinical decision-making during treatment. Hospitals are increasingly deploying such technologies to enhance surgical workflow efficiency and reduce procedure time. Continuous innovation in surgical robotics, automated anesthesia delivery, and advanced treatment planning software is further strengthening the segment’s role in modern healthcare facilities. As healthcare providers prioritize precision medicine and outcome-based treatment strategies, therapeutic automation continues to dominate the market by improving surgical consistency, operational efficiency, and overall treatment effectiveness.

By Application Insights

The diagnostics & monitoring segment is projected to represent 26.5% of the global market in 2026, making it the largest application area for medical automation technologies. Automation has become essential in modern diagnostic environments, particularly in clinical laboratories, imaging centers, and hospital monitoring units where rapid and accurate data processing is critical. Automated diagnostic platforms enable high-throughput testing, consistent sample handling, and faster turnaround times, which are vital for early disease detection and timely treatment decisions.

Healthcare providers are increasingly adopting automated systems that integrate laboratory analyzers, imaging interpretation tools, and digital patient monitoring platforms. These technologies help clinicians continuously track vital parameters, detect abnormalities earlier, and streamline clinical workflows. The growing burden of chronic diseases, combined with the rising volume of diagnostic tests worldwide, has significantly increased demand for automation-driven solutions. Furthermore, advancements in AI-enabled diagnostics and connected monitoring systems are enhancing the reliability of clinical data analysis. As healthcare institutions emphasize data-driven decision making and precision diagnostics, the diagnostics and monitoring segment continues to command the largest share of automation deployment across healthcare settings.

By End-user Insights

Hospitals are anticipated to account for 44.7% of the global medical automation market in 2026, maintaining their role as the primary environment for advanced healthcare automation systems. Large healthcare institutions possess the financial resources, clinical infrastructure, and technical expertise required to integrate sophisticated automation technologies across multiple departments. These facilities frequently deploy automated laboratory systems, robotic surgical platforms, pharmacy dispensing technologies, and intelligent patient monitoring solutions to improve operational efficiency and clinical outcomes.

Hospitals also manage high patient volumes, requiring streamlined workflows and reliable clinical decision support systems. Automation solutions help reduce administrative burden, minimize medication errors, and improve coordination between departments such as laboratories, imaging units, and intensive care units. Many tertiary hospitals and academic medical centers are also investing in AI-driven workflow management tools and digital health platforms that enhance patient data integration and treatment planning. Continuous technological upgrades, along with increasing focus on quality care and patient safety, are encouraging hospitals to expand their automation capabilities, reinforcing their dominant position as the largest end-user segment within the global medical automation ecosystem.

Regional Insights

North America Medical Automation Market Trends

North America is projected to account for 46.7% of the global medical automation market in 2026, maintaining its position as the largest regional contributor. The region benefits from a highly advanced healthcare infrastructure, substantial healthcare spending, and early adoption of automation technologies across hospitals, laboratories, and imaging centers. Healthcare providers in the United States and Canada increasingly deploy robotic surgical platforms, automated laboratory systems, and AI-enabled imaging solutions to enhance diagnostic accuracy and operational efficiency. Continuous technological advancements, along with strong demand for improved patient safety and reduced clinical errors, are further encouraging healthcare institutions to integrate automation across multiple clinical workflows.

Another important factor supporting regional leadership is the presence of major medical technology manufacturers and healthcare innovation hubs that continuously develop next-generation automation systems. Hospitals are also implementing digital workflow management tools, automated pharmacy dispensing systems, and intelligent patient monitoring platforms to streamline care delivery. Strong reimbursement frameworks for advanced medical procedures and ongoing investments in healthcare digitization further strengthen market growth. In addition, extensive clinical research activities, physician training initiatives, and hospital modernization programs continue to support the widespread deployment of medical automation technologies across North America.

Europe Medical Automation Market Trends

Europe represents a well-established and steadily expanding market for medical automation technologies, supported by strong public healthcare systems and well-developed clinical infrastructure. Countries including Germany, France, the United Kingdom, and Italy serve as key centers for healthcare innovation and technology adoption. Hospitals and diagnostic laboratories across the region are increasingly implementing automated laboratory analyzers, robotic-assisted surgical systems, and AI-driven imaging platforms to enhance diagnostic efficiency and improve patient outcomes. The presence of structured healthcare policies and strong regulatory frameworks also encourages the adoption of reliable and standardized automation solutions across medical facilities.

Furthermore, Europe’s aging population is significantly increasing healthcare demand, encouraging hospitals to adopt automation tools that can manage higher patient volumes and improve clinical workflow efficiency. Many healthcare providers are investing in smart hospital technologies, including integrated patient monitoring systems and digital healthcare platforms that enable better data management and coordinated care. Furthermore, academic hospitals and research institutions actively collaborate with medical device manufacturers to develop advanced healthcare technologies. Continuous investment in digital health infrastructure and medical innovation ensures that Europe remains a technologically progressive and stable market within the global medical automation landscape.

Asia Pacific Medical Automation Market Trends

Asia Pacific is expected to emerge as the fastest-growing regional market, registering a CAGR of approximately 7.4% between 2026 and 2033. Rapid healthcare infrastructure expansion across countries such as China, India, Japan, and South Korea is significantly improving access to advanced medical technologies. Governments across the region are investing heavily in modernizing hospitals, expanding diagnostic facilities, and integrating digital healthcare systems to meet the increasing demand for quality medical services. The rising prevalence of chronic diseases, coupled with population growth and urbanization, is encouraging healthcare providers to adopt automation solutions that enhance clinical efficiency and diagnostic accuracy.

The region is also witnessing a growing number of private hospitals and specialized healthcare centers that prioritize advanced technology integration. These institutions are actively deploying automated laboratory platforms, AI-enabled diagnostic systems, and intelligent patient monitoring technologies to improve healthcare delivery. Increasing availability of trained medical professionals and expanding digital health initiatives are further supporting automation adoption across the region. Additionally, the affordability of healthcare services in several Asian countries has contributed to the growth of medical tourism, encouraging healthcare providers to invest in advanced automation systems that enhance service quality and operational efficiency.

Competitive Landscape

The global medical automation market is highly competitive, with strong participation from Stryker Corporation, Siemens Healthineers AG, Koninklijke Philips N.V., Danaher Corporation, Zimmer Biomet Holdings, Inc., and Abbott Laboratories. These companies leverage extensive hospital networks, clinical training programs, and continuous innovation in robotic-assisted systems, laboratory automation platforms, smart imaging technologies, and AI-driven workflow solutions to improve healthcare delivery. Increasing demand for operational efficiency, rising patient volumes, and the need to reduce clinical errors are accelerating automation adoption, encouraging manufacturers to develop integrated digital platforms, advanced analytics tools, and scalable automation technologies that enhance diagnostic accuracy, streamline clinical workflows, and support improved patient outcomes across global healthcare systems.

Key Industry Developments:

- In March 2026, Ethermed partnered with VisiQuate to integrate authorization automation with predictive analytics and workflow intelligence, aiming to speed approvals and reduce administrative workload in healthcare revenue cycle operations.

- In March 2026, Nitra raised US$187 million to expand its AI-powered operating system designed for healthcare practices. The funding will support the company’s efforts to enhance automation in administrative workflows, financial management, and operational efficiency for medical providers.

- In February 2026, IXICO reported new findings showing that the automated brain volume measurement capabilities within its IXI™ platform can match and, in some cases, outperform traditional semi-manual MRI analysis methods performed by human experts.

- In July 2025, Indegene introduced NEXT Medical Writing Automation, a platform that integrates generative AI with medical writing expertise to accelerate the development of high-quality regulatory, clinical, and scientific documentation across drug development processes.

Companies Covered in Medical Automation Market

- Stryker Corporation

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- Danaher Corporation

- Zimmer Biomet Holdings, Inc.

- Abbott Laboratories

- Becton, Dickinson and Company

- Thermo Fisher Scientific Inc.

- Boston Scientific Corporation

- GE HealthCare Technologies Inc.

- Accuray Incorporated

- Tecan Group Ltd.

- Medtronic plc

- Swisslog Holding AG

- Intuitive Surgical, Inc.

- Others

Frequently Asked Questions

The global medical automation market is projected to be valued at US$ 53.4 Bn in 2026.

Rising demand for operational efficiency, patient safety, and adoption of AI- and robotics-based healthcare technologies are major drivers of the global medical automation market.

The global medical automation market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Growing adoption of telemedicine, remote patient monitoring, and AI-enabled diagnostic systems is creating significant opportunities for medical automation solutions worldwide.

Stryker Corporation, Siemens Healthineers AG, Koninklijke Philips N.V., Danaher Corporation, Zimmer Biomet Holdings, Inc., and Abbott Laboratories are some of the key players in the medical automation market.