- Automation & Robotics

- Industrial Robotics Market

Industrial Robotics Market Size, Share, Trends, Growth, Regional Forecasts 2025 - 2032

Industrial Robotics Market by Robot Type (Articulated Robotcs, Cartesian/Linear Robots, Parallel Robots, Other), Payload Range (upto 20 kg, 21 to 60 kg, 61 to 200 kg, above 200 kg), Industry (Automotive, Electrical & Electronics, Metals & Heavy Machinery), Regional Analysis from 2025 - 2032

Industrial Robotics Market Share and Trends Analysis

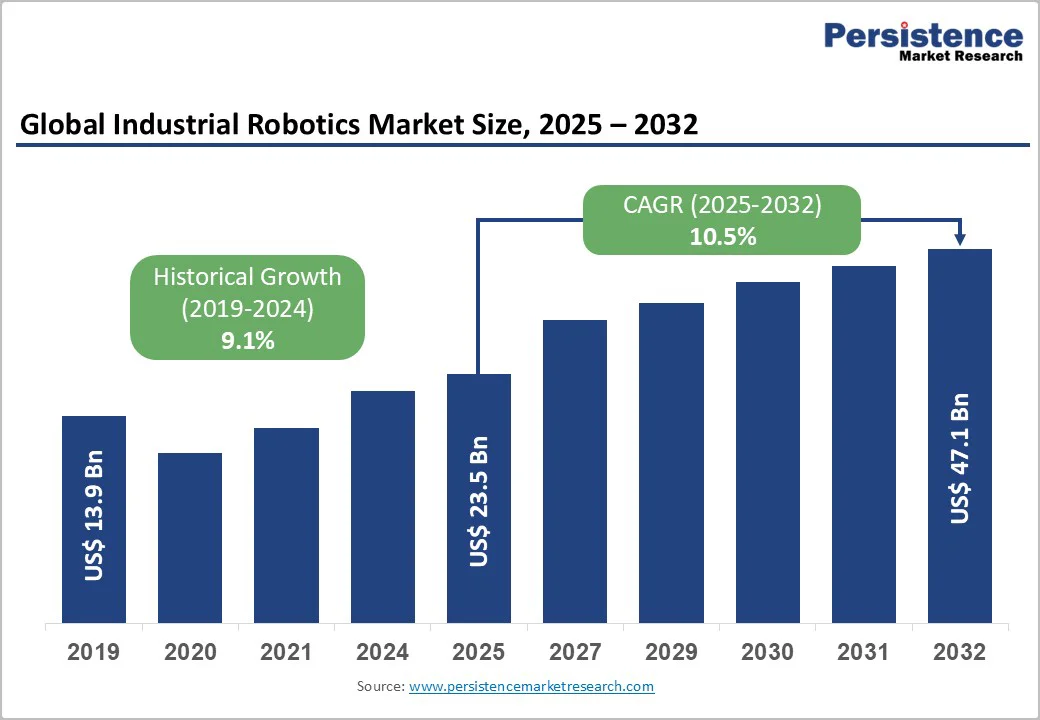

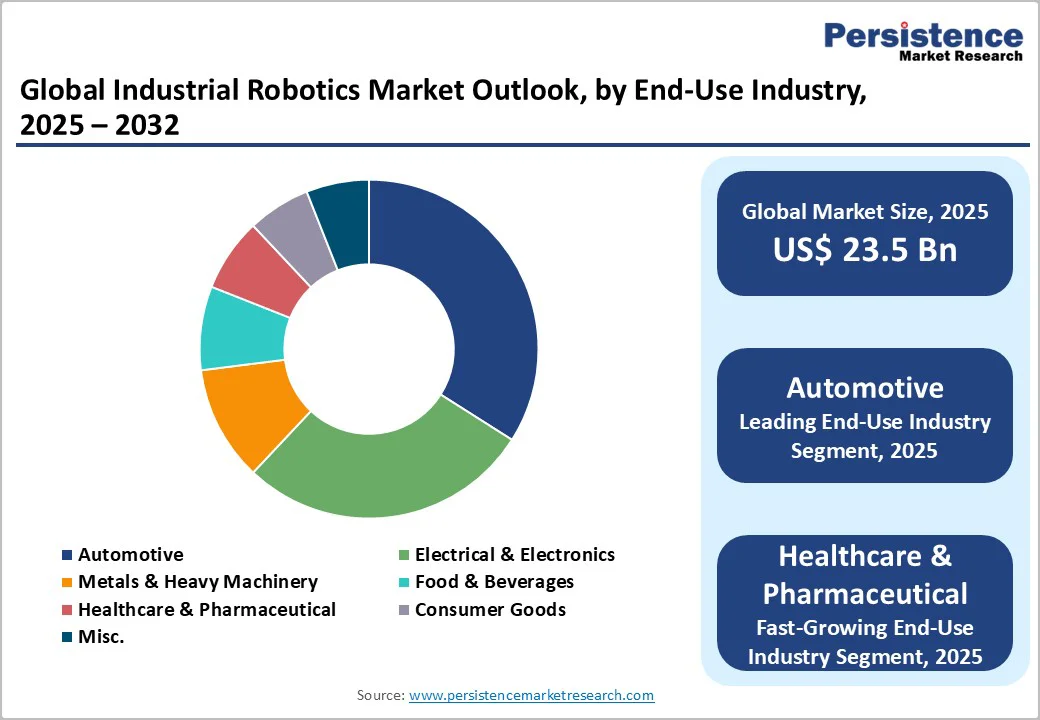

The global industrial robotics market size is valued at US$23.5 billion in 2025 and is projected to reach US$47.1 billion by 2032, growing at a CAGR of 10.5% between 2025 and 2032. The market's robust expansion is primarily driven by accelerating adoption of Industry 4.0 initiatives, persistent labor shortages across developed economies, and the automotive sector's transition toward electric vehicle manufacturing.

According to Rockwell Automation, 95% of manufacturers are currently using or evaluating smart manufacturing solutions as of March 2024, representing a significant increase from 83% the previous year. The International Federation of Robotics reported a 14% rise in operational industrial robots during 2024, marking the steepest annual jump since 2018, underscoring the unprecedented momentum in automation investments across global manufacturing sectors.

Key Highlights Summary

- Dominant Robot Configuration: Articulated robots command 44% market share, while SCARA robots emerge as fastest-growing category at 11.2% CAGR fueled by electronics manufacturing precision requirements

- Payload Segment Leadership: "Up to 20 kg" payload robots hold 35% market share for light-duty applications, with "21 to 60 kg" segment growing fastest at 11.2% CAGR addressing mid-range manufacturing needs

- Industry Dynamics: Automotive sector maintains 34% market share as leading adopter, while healthcare and pharmaceutical represents fastest-growing segment at 12.4% CAGR driven by quality and safety imperatives

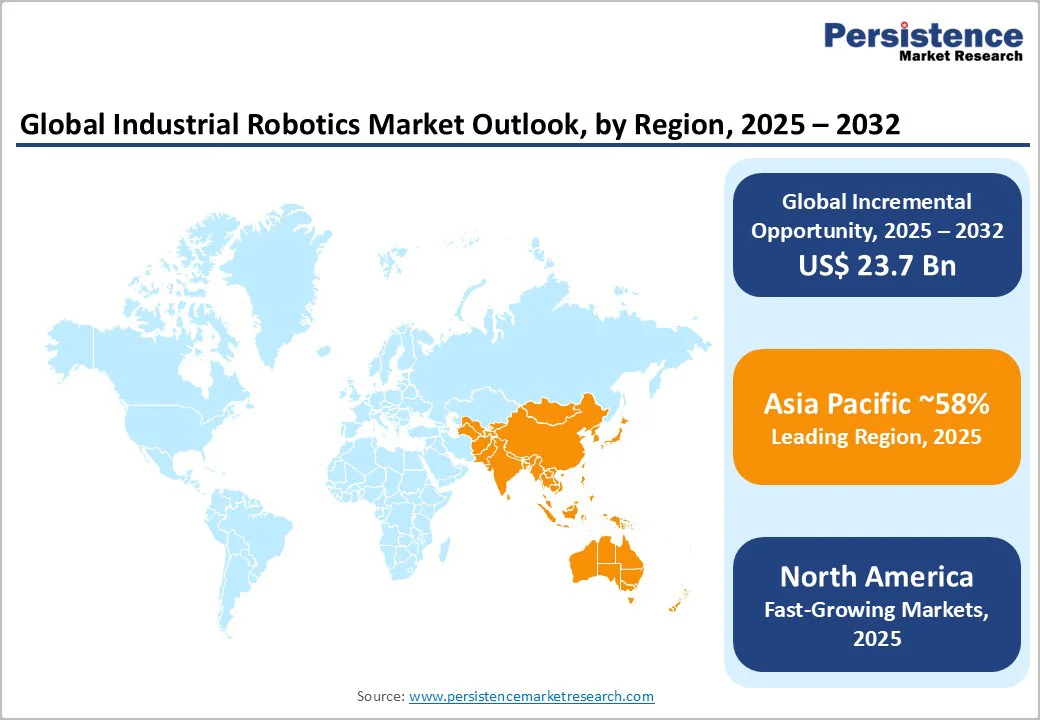

- Regional Market Leadership: Asia Pacific dominates with 58% global market share and 11.1% CAGR, led by China's 51% share of global installations; North America grows at 10.2% CAGR; Europe holds 18% share at 9.5% CAGR

- Competitive Concentration: Top four vendors-FANUC, ABB, Yaskawa, and KUKA-control approximately 75% of global shipments, with 2024 M&A activity exceeding US$1.2 billion reflecting strategic consolidation trends

- Technology Convergence: 95% of manufacturers using or evaluating smart manufacturing as of March 2024; 14% annual increase in operational robots during 2024 marks steepest growth since 2018, underscoring automation momentum

| Key Insights | Details |

|---|---|

|

Industrial Robotics Market Size (2025E) |

US$ 23.5 billion |

|

Market Value Forecast (2032F) |

US$ 47.1 billion |

|

Projected Growth CAGR (2025-2032) |

10.5% |

|

Historical Market Growth (2019-2024) |

9.1% |

Market Dynamics Analysis

Drivers - Escalating Labor Shortages and Rising Wage Costs in Manufacturing

The manufacturing sector faces an acute labor crisis that is fundamentally reshaping automation investment strategies. According to the 9th Annual State of Smart Manufacturing Report, 42% of manufacturers identify increasing automation as their primary strategy for addressing labor shortages and skills gaps. The manufacturing labor shortage persists across North America and Europe, where aging demographics and shifting workforce preferences have created persistent talent gaps. In the United States alone, the manufacturing sector struggles to fill critical positions, with employee turnover rates significantly impacting production continuity. Industrial robots provide a compelling solution by operating continuously without fatigue, eliminating dependency on limited workforce availability. Furthermore, 94% of manufacturers expect to hire more workers or repurpose employees to new roles through automation implementation, demonstrating that robotics complements rather than replaces human capital. The cost-benefit analysis increasingly favors automation, as robots reduce operational expenses through 24/7 productivity, consistent quality output, and elimination of costs associated with training, benefits, and turnover.

Accelerating Industry 4.0 and Smart Manufacturing Adoption

The proliferation of Industry 4.0 technologies represents a transformative driver for industrial robotics demand. According to IoT Analytics, 72% of manufacturers already have or are implementing Industry 4.0 and smart factory initiatives. The 2025 Smart Manufacturing and Operations Survey revealed that respondents achieved average improvements of 10-20% in production output, 7-20% in employee productivity, and 10-15% in unlocked capacity following smart manufacturing implementation. These quantifiable returns are accelerating investment decisions across manufacturing sectors. Industrial robots serve as the physical manifestation of Industry 4.0, integrating with Internet of Things (IoT) sensors, artificial intelligence, machine learning algorithms, and cloud-based analytics platforms to create intelligent, adaptive production systems. KUKA's February 2024 launch of the KR FORTEC industrial robot exemplifies this convergence, featuring extended reach of 368.3 cm, payload capacity of 240 kg, and energy-efficient operation optimized for handling and spot welding applications. The North American industrial automation market alone is forecast to increase at a CAGR of 8.4% between 2024 and 2030, directly benefiting industrial robotics adoption.

Restraints - High Initial Capital Investment and Integration Complexity

The high upfront costs of industrial robotics pose a significant barrier for small and medium-sized enterprises (SMEs). Implementing robotic systems involves substantial capital investments, including hardware, specialized tooling, safety systems, programming, facility modifications, and integration with existing systems. Despite long-term benefits, the initial investment remains a challenge for broader market expansion. The total cost of ownership goes beyond the purchase price and includes installation, employee training, ongoing maintenance, and potential production downtime. For manufacturers with tight margins, these financial burdens create hesitancy toward adoption. Additionally, the complexity of integrating robots with legacy equipment and the need for expertise in programming and safety protocols can further increase costs and timelines for automation projects.

Cybersecurity Vulnerabilities and Technical Standardization Challenges

The rising connectivity of industrial robots in Industry 4.0 presents cybersecurity risks that manufacturers need to address. As robots connect to cloud platforms, IoT networks, and 5G, they can become entry points for cyberattacks, compromising data and disrupting operations. Challenges in adapting to standards and cybersecurity for connected robots are significant barriers. Manufacturers must protect proprietary processes while allowing data sharing for predictive maintenance and supply chain coordination. The lack of universal technical standards among robot manufacturers complicates integration, as different vendors use proprietary languages and protocols, resulting in interoperability issues. Meanwhile, the rapid advancement of robotics technologies outpaces standardization efforts, leaving manufacturers to navigate a fragmented landscape with uncertain compatibility and upgrade options.

Opportunity - Expanding Healthcare and Pharmaceutical Automation

The healthcare and pharmaceutical sectors present substantial growth opportunities for industrial robotics, driven by stringent regulatory requirements and demand for contamination-free production. The Healthcare & Pharmaceutical robots market is expected to grow at a CAGR of 12.4%. In December 2020, the US pharmaceutical sector witnessed a 61% increase in automation applications for packaging and FDA-compliant traceability on production lines, motivated by reshoring practices and supply chain vulnerabilities exposed during the pandemic. Pharmaceutical companies utilize robotic technology to enhance production precision, ensure adherence to Good Manufacturing Practices (GMP), and reduce contamination risks inherent in human-involved processes. The rising demand for biologics, biosimilars, and personalized medicines increases production complexity, requiring the precision and consistency that only robotic automation can reliably deliver. Robots streamline repetitive laboratory testing, accelerate drug discovery timelines, and enable 24/7 production capacity to meet growing medication demand driven by aging populations and chronic disease prevalence.

Collaborative Robotics and Robotics-as-a-Service Business Models

Collaborative robots (cobots) and innovative Robotics-as-a-Service (RaaS) business models are democratizing access to automation for previously underserved market segments. The global collaborative robot market is projected to grow at a CAGR of 18.9%. Cobots offer distinct advantages over traditional industrial robots: they work safely alongside human operators without expensive safety barriers, feature intuitive programming interfaces accessible to non-specialists, and provide faster deployment with lower upfront capital requirements. The RaaS subscription model further reduces adoption barriers by eliminating large capital expenditures in favor of predictable operational expenses, enabling SMEs with limited budgets to access cutting-edge automation. According to Bigwave Robotics CEO Minkyo Kim, while robots were historically deployed primarily by medium and large enterprises, solutions have become increasingly cost-competitive and user-friendly, accelerating adoption among small-to-medium-sized manufacturers. The electronics and electrical sectors particularly benefit from cobot capabilities in delicate component handling, while the e-commerce and logistics industries leverage cobots for order fulfillment and warehouse operations. Asia Pacific is emerging as the fastest-growing collaborative robot market, driven by rapid logistics network expansion, large-scale manufacturing automation, and AI-enabled robotics adoption across key sectors.

Category-wise Analysis

Robot Type Insights

Articulated robots dominate the industrial robotics market with approximately 44% market share, maintaining their position as the most versatile and widely deployed robot configuration. These multi-jointed robots, typically featuring 4-6 axes of movement, excel in applications requiring complex motion patterns, including welding, painting, material handling, and assembly operations. Their anthropomorphic design provides exceptional workspace flexibility and reach capabilities, making them ideal for automotive manufacturing, where they perform spot welding, sealing, and component installation tasks. The International Federation of Robotics data indicates articulated robots account for the majority of the 23,000 units installed in Europe's automotive sector during 2024. Major manufacturers, including FANUC, ABB, KUKA, and Yaskawa, continuously enhance articulated robot capabilities through integration of advanced vision systems, force-sensing technology, and AI-powered path optimization.

While articulated robots lead in market share, SCARA (Selective Compliance Assembly Robot Arm) robots represent the prominent growth with a CAGR of 11.2%. These robots are recognized for high-speed precision in pick-and-place, assembly, and material handling operations, achieving repeatability of up to 0.01 mm in numerous applications. The electronics manufacturing sector, which accounts for approximately 65% of all SCARA robot installations, drives this growth through demand for rapid component placement on circuit boards and precise assembly of miniaturized devices. In 2023, global SCARA robot shipments exceeded 150,000 units, marking a 12% increase from the previous year. The automotive industry deploys approximately 7,000 new SCARA robots annually in the United States alone, primarily for precise component assembly tasks.

Payload Range Insights

The "Up to 20 kg" payload segment commands the largest market share at approximately 35%, reflecting the predominance of light-duty assembly, electronics manufacturing, and packaging applications across global production facilities. Low-payload robots typically feature compact footprints and lighter mass compared to higher-payload counterparts, making them ideal for space-constrained manufacturing environments. These robots automate processes involving small components, delicate parts handling, light-duty palletizing, dispensing operations, and packaging tasks.

The FANUC LR Mate 200ic and ABB IRB 140 exemplify popular low-payload industrial robot arms optimized for these applications. The electronics and electrical equipment sector, which relies heavily on the precise handling of fragile components, drives sustained demand for this payload category. Low-payload robots offer significant advantages in speed and acceleration, compensating for reduced strength with superior cycle time performance, critical in high-volume production environments.

The "21 to 60 kg" payload segment is the fastest-growing category, with a CAGR of 11.2%. This range is ideal for diverse applications such as automotive component handling, machine tending, and moderate-weight material transfer, catering to the need for robots that can manipulate heavier subassemblies with precision. For instance, electric vehicle battery module handling falls within this weight range, requiring robots with both sufficient lifting capacity and accurate positioning. Manufacturing facilities are increasingly using 21-60 kg payload robots for flexible automation across multiple product lines. This segment benefits from advancements in gripper technology, force-torque sensing, and vision-guided systems, enhancing its application possibilities.

Industry Insights

The automotive industry maintains market leadership with approximately 34% market share, representing the most mature and extensively automated manufacturing vertical. Automotive manufacturers pioneered industrial robotics adoption in the 1960s and continue driving innovation through demanding application requirements. In 2024, the sector deployed 23,000 robots in Europe, with six countries in the top ten for automotive robot density. Switzerland leads with 3,876 robots per 10,000 workers, followed by Slovenia (1,762), Germany (1,492), Austria (1,412), Finland (1,288), and the Benelux countries (1,132). Vehicle manufacturers held 61.2% of the automotive robotics market, driven by the shift to electric vehicles, which increases demand for automated battery assembly and production processes. In China, the automotive sector has 429,500 robots, equating to 470 per 10,000 workers, aided by government incentives for domestic manufacturers.

The healthcare and pharmaceutical sector is the fastest-growing industry, with a CAGR of 12.4%, due to strict quality standards and rising demand for advanced therapeutics. The sector utilizes robots in drug manufacturing, laboratory automation, packaging, and supply chain logistics to reduce human intervention and contamination risks. The increasing production of biologics, biosimilars, and personalized medicines adds complexity, requiring precise robotic automation. Additionally, healthcare robotics in surgical assistance, rehabilitation, and hospital logistics is on the rise, with medical robot sales expected to reach about 16,700 units globally by 2024. The aging population and demand for minimally invasive procedures are key factors driving robotics adoption in both pharmaceutical manufacturing and clinical healthcare.

Regional Market Insights

North America Industrial Robotics Market Trends

North America demonstrates robust growth with a CAGR of 10.2%, characterized by advanced manufacturing infrastructure, substantial research and development investments, and supportive policy frameworks promoting industrial automation. The United States leads regional adoption, driven by automotive, aerospace, electronics, and healthcare sectors implementing automation to enhance productivity, reduce operational costs, and maintain quality standards.

The North American industrial automation market is expected to grow at a CAGR of 8.4% from 2024 to 2029, with industrial robotics playing a key role. Federal incentives for onshoring electronics are projected to boost CAGR by 2.1%, driving sustained demand for manufacturing automation. In 2024, the automotive industry held a 29.28% revenue share due to ongoing investments in battery-module assembly and robotics. The U.S. installed around 19,200 robots in automotive, trailing Europe's 23,000 but still showing strong growth.

North America’s robotics landscape features a strong mix of global leaders and fast-growing startups, supported by rising acquisition activity as seen in Symbotic’s purchases of Veo Robotics and OhmniLabs. Industry 4.0 adoption is deeply established with widespread use of cloud computing, industrial IoT, and 5G connectivity. Collaborative robot uptake is accelerating among SMEs, especially in the US Midwest and Southern Ontario, boosting short-term growth. Demand for energy-efficient manufacturing adds medium-term momentum, while Canada and Mexico strengthen regional automation through automotive, electronics, and nearshoring-driven investments.

Europe Industrial Robotics Market Trends

Europe maintains a considerable market share of approximately 18% globally, growing at a steady CAGR of 9.5% supported by strong automotive manufacturing traditions, Industry 4.0 leadership, and harmonized regulatory frameworks promoting automation adoption. Germany dominates the European market, accounting for approximately 30% of total regional robot installations and representing the world's second-leading automation and robotics investment destination.

From 2019 to 2024, Europe's compound annual growth rate (CAGR) for robot installations reached +3%, with Germany hosting over 450 FDI projects in robotics and automation from 2019 to 2024. The German robotics market generated revenues exceeding €15 billion in 2024, with robot density in manufacturing reaching 415 robots per 10,000 employees, far above the European average of 204 units. Germany accounts for almost half of all industrial robots operating in Europe, with major manufacturers KUKA and ABB maintaining substantial production and research facilities serving the continent's automotive giants, including Volkswagen, BMW, and Mercedes-Benz.

Europe remains a global automation leader, with the United Kingdom recording 191 FDI projects and France 144 during 2019 to 2024. Italy contributes about ten percent of installations and Spain about six percent. The automotive sector leads demand with 23,000 robot installations, nearly one-third of the region’s 2024 total. EU27 countries represent around 85% of installations, supported by strong Industry 4.0 policies. Adoption continues to rise across major manufacturers and SMEs driven by EV production, electronics growth, and labor efficiency needs.

Asia Pacific Industrial Robotics Market Trends

Asia Pacific dominates the global industrial robotics market with a commanding 58% market share and leads growth with a CAGR of 11.1%, establishing the region as the epicenter of global manufacturing automation. The region accounted for 73% of global industrial robot installations in 2022, with this concentration intensifying through 2024 as China, Japan, South Korea, and emerging markets accelerate automation investments.

China leads the world in industrial robot installations, comprising 51% of the global market in 2023, driven by the government's "Made in China 2025" initiative. The automotive sector has a robot density of 470 units per 10,000 workers, with 429,500 robots in use, supported by state incentives that keep acquisition costs low for manufacturers. Japan ranks second in the region, functioning as both a leading robotics market and the world's preeminent robot manufacturing hub. Home to industry giants FANUC, Yaskawa, and Kawasaki, Japan accounted for approximately 25% of global robot production in 2023. Japan's "Society 5.0" initiative promotes the use of AI and robotics across various industries, particularly in automotive and electronics, where robotic automation is crucial for precision tasks like welding and assembly.

India is emerging as a high-potential growth market fueled by the "Make in India" initiative, particularly in the automotive industry, where companies like Tata Motors and Mahindra & Mahindra are adopting robotics for assembly and welding. Although adoption rates are behind regional leaders, India's focus on smart manufacturing positions it for future growth. Meanwhile, Southeast Asian nations are attracting OEMs to localize EV production through production-linked incentives, making ASEAN an emerging manufacturing hub. The region's emphasis on smart manufacturing enhances productivity through robotics, with Industry 4.0 initiatives in China, Japan, and South Korea driving significant investments in AI and IoT-connected factories.

Competitive Landscape

The global industrial robotics market remains moderately concentrated, with FANUC, ABB, Yaskawa, and KUKA accounting for a dominant share of global shipments supported by strong IP portfolios, global service networks, and scale advantages. FANUC benefits from deep vertical integration, while ABB strengthens its automotive focus alongside portfolio optimization efforts. Yaskawa’s motion control expertise and KUKA’s leadership in European automotive automation reinforce their positions, with Mitsubishi Electric, Kawasaki, Denso, Nachi Fujikoshi, Epson, and Dürr forming the next competitive tier.

Strategic Developments

- In January 2024, ABB advanced its AI automation strategy by acquiring Sevensense Robotics and Meshmind, adding visual navigation and analytics capabilities to strengthen autonomous mobile robotics and enhance its position in delivering integrated, AI enabled smart factory automation platforms worldwide.

- In September 2024, Nano Dimension advanced this consolidation by acquiring Markforged for US$115 million, creating an integrated additive manufacturing robotics platform addressing rising demand for automated, high precision, rapid production solutions across aerospace, automotive, and medical device industries.

- In February 2024, KUKA launched the KR FORTEC robot featuring 368.3 cm reach and 240 kg payload, delivering compact, energy efficient, high performance capabilities tailored to automotive handling and spot welding applications, particularly supporting evolving electric vehicle manufacturing and battery component handling requirements.

Companies Covered in Industrial Robotics Market

- ABB Ltd.

- FANUC Corporation

- KUKA AG

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Universal Robots

- Stäubli Robotics

- Nachi-Fujikoshi Corporation

- Comau S.p.A.

- Omron Corporation

- Epson Robots

- Kawasaki Heavy Industries

- Denso Robotics

- Honda Robotics

- Siemens AG

Frequently Asked Questions

The global industrial robotics market was valued at US$23.46 billion in 2025 and is projected to reach US$47.14 billion by 2032.

The industrial robotics market is largely driven by the fast adoption of Industry 4.0 and the need for automation due to labor shortages. The shift towards electric vehicle manufacturing in the automotive sector also requires specialized automation. Implementing robotics has shown ROI improvements of 10-20% in production output.

The industrial robotics market is projected to grow at a CAGR of 10.5% between 2025 and 2032.

Key market opportunities include healthcare and pharmaceutical automation, growth in collaborative robotics via Robotics-as-a-Service for SMEs, industrialization in India and Southeast Asia driven by government incentives, and the transformation of electric vehicle manufacturing needing specialized robotics for battery assembly and component handling.

The key players in the global industrial robotics market include FANUC Corporation (Japan), ABB (Switzerland), Yaskawa Electric Corporation (Japan), KUKA AG (Germany), Mitsubishi Electric Corporation (Japan), Kawasaki Heavy Industries (Japan), Denso Corporation (Japan), and other key players hold significant global market share.