- Hardware & Software IT Services

- Artificial Intelligence Platform Market

Artificial Intelligence Platform Market Size, Share, and Growth Forecast, 2025 - 2032

Artificial Intelligence Platform Market By Component (AI Tools, AI Machine Learning Platforms), Deployment (Cloud-based, On-premises), End-user (Retail and E-commerce, IT and Telecom, BFSI), and Regional Analysis for 2025 - 2032

Artificial Intelligence Platform Market Size and Trends Analysis

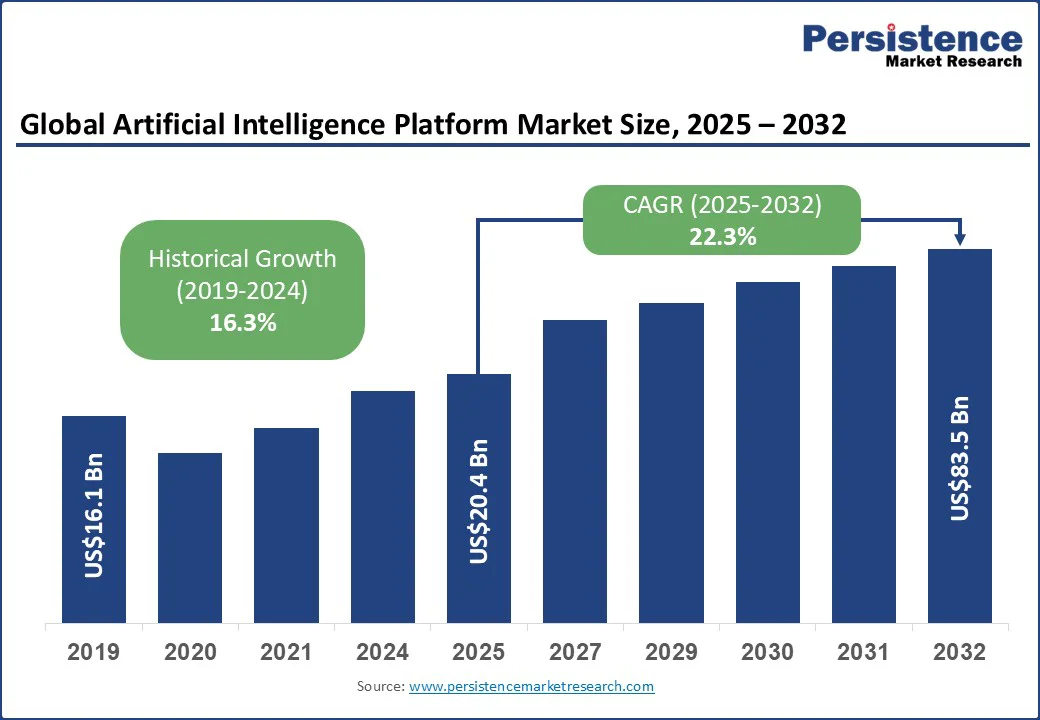

The global artificial intelligence platform market size is likely to be valued at US$20.4 Bn in 2025 and is estimated to reach US$83.5 Bn in 2032, growing at a CAGR of 22.3% during the forecast period 2025 - 2032, driven by extensible enterprise automation, ongoing cloud adoption, and rising demand for customized AI solutions that improve operational intelligence as well as business productivity.

Key Industry Highlights

- BFSI Development: In November 2024, Temenos and NVIDIA deployed an on-premises generative AI platform for banks. It supported real-time insights and regulatory compliance with explainable AI.

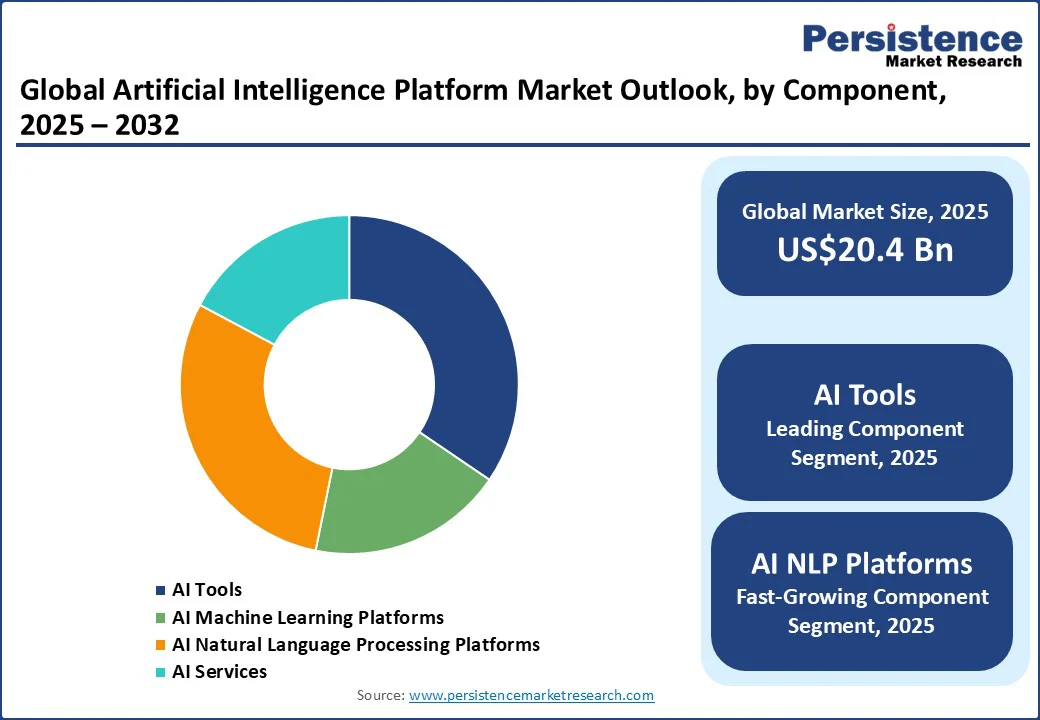

- Leading Component: AI tools hold nearly 34.5% share in 2025, as they simplify complex analytics, automate workflows, and deliver actionable insights quickly.

- Dominant Deployment: Cloud-based, approximately 67.4% of the artificial intelligence platform market share in 2025, owing to low infrastructure costs and easy integration with enterprise systems.

- Key End-user: IT and telecom, around 30.2% share in 2025, as it requires novel data processing, network optimization, and predictive analytics.

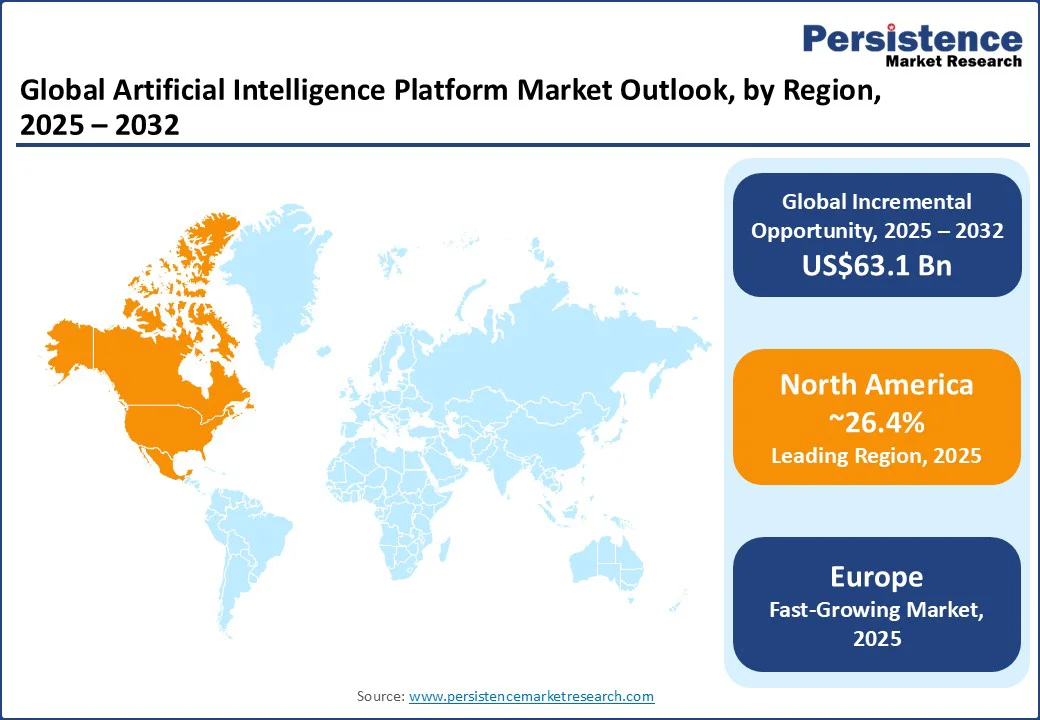

- Leading Region: North America with about 26.4% share in 2025, owing to mature AI ecosystems, high research investments, and early enterprise adoption.

- Fastest-growing Region: Europe, with a projected 22.0% share in 2025, spurred by favorable policies, digital transformation initiatives, and the adoption of AI in healthcare.

| Key Insights | Details |

|---|---|

| Artificial Intelligence Platform Market Size (2025E) | US$20.4 Bn |

| Market Value Forecast (2032F) | US$83.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 22.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 16.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Ongoing Digitization and Automation

Major industries are accelerating the adoption of AI to manage data at scale, automate workflows, and increase efficiency. Global survey data shows that over 40% of enterprises have initiated AI pilots since 2021, with manufacturing reporting productivity gains of up to 15% due to predictive analytics and automated quality control.

Governments and industry bodies such as the Organization for Economic Co-operation and Development (OECD) and the World Economic Forum (WEF) are promoting digital transformation. They are contributing significantly to the market's momentum through policy incentives and regulatory clarity.

Cloud Infrastructure and Accessibility

Cloud-based AI platforms are gaining traction across the globe. The proliferation of hyperscale cloud vendors such as AWS, Microsoft, and Google has enabled streamlined deployment, reduced upfront investments, and facilitated development by providing pre-built model libraries.

Gartner statistics reveal that cloud AI services increase model deployment speed by 40% and reduce operational costs by 30% for large enterprises. Regional governments in North America and Asia Pacific continue to subsidize cloud AI projects, propelling global accessibility.

Regulatory Mandates and Data Governance

Evolving regulations, including the General Data Protection Regulation (GDPR) and the EU AI Act, are mandating robust model compliance, auditability, and risk minimization. This fosters demand for platforms designed for transparency and secure data governance.

Industry associations such as the Institute of Electrical and Electronics Engineers (IEEE) and the International Organization for Standardization (ISO) are actively shaping standards. Regulatory changes have catalyzed increased spending on AI compliance tools, especially in banking, healthcare, and government operations.

Data Privacy and Security Vulnerabilities

Exposure to cyber threats remains a key concern, with enterprises now spending over 25% of their AI budgets solely on compliance and risk management due to the rising cost of securing AI systems. Failure to meet data privacy requirements can result in multi-million-dollar fines and reputational damage, as seen in recent GDPR enforcement actions.

Beyond regulatory fines, data privacy and security vulnerabilities can directly impact business operations and stakeholder trust. Breaches or misuse of sensitive data can lead to intellectual property theft, operational disruptions, and loss of competitive advantage. Customers are increasingly aware of how their data is handled, and any perceived negligence can drive them to competitors.

Skills Gap and Talent Shortage

Few organizations possess the required talent to fully utilize AI platforms. Industry surveys from PwC and KPMG indicate the availability of skilled personnel lags behind demand by 40%, resulting in delayed projects and suboptimal system utilization. This gap increases operational risks and imposes high training costs on businesses.

This shortage extends beyond just data scientists and AI engineers. It also includes AI architects, MLOps specialists, and domain experts capable of translating complex business problems into AI solutions. Hence, several organizations struggle to integrate AI tools effectively into their workflows, leading to underutilized platforms and limited return on investment.

Launch of Industry-specific AI Solutions

Rising demand for verticalized platforms in healthcare, finance, and retail is unlocking significant new opportunities. Healthcare AI is projected to expand at a 22% CAGR through 2032, generating incremental market revenues of US$30 Bn. Customized tools for manufacturing and BFSI are rapidly scaling, driven by regulatory compliance needs and operational efficiency requirements.

In addition to vertical-specific applications, there is a growing opportunity for AI platforms to support small and medium-sized enterprises (SMEs) that previously lacked access to novel AI tools. Cloud-based AI-as-a-Service is lowering entry barriers, allowing SMEs to use predictive analytics, automated workflows, and personalized customer engagement without heavy upfront investments.

Edge AI and Decentralized Analytics

Integration of AI with edge computing systems is enabling real-time decision-making in factories, transportation, and urban infrastructure. The industrial AI market is predicted to reach US$153.9 Bn by 2030. It underscores the actionable potential of local data processing. Investments in edge infrastructure have also quadrupled since 2021.

Alongside edge computing, there is a rising emphasis on federated learning and decentralized AI models. These allow organizations to train algorithms across multiple locations without sharing sensitive raw data. This approach improves privacy while enabling collaborative intelligence across industries such as healthcare, finance, and autonomous transportation.

Ongoing Expansion in Emerging Markets

Asia Pacific, Latin America, and the Middle East are poised to register above-average growth rates. Growth in Asia Pacific is anticipated to be supported by national AI strategies, manufacturing hubs, and digitization programs. Emerging regions deliver untapped customer bases, with governments investing heavily in local AI ecosystems.

Asia Pacific, Latin America, and the Middle East are further experiencing a surge in AI-focused start-ups, incubators, and innovation centers. These are pushing localized solutions and industry-specific applications. The proliferation of cloud infrastructure, increasing mobile internet penetration, and surging adoption of digital payment as well as e-commerce platforms are also accelerating AI deployment in these regions.

Category-wise Analysis

Component Insights

AI tools lead with an estimated 34.5% market share in 2025, propelled by rising demand for integrated development kits that accelerate custom model creation, algorithm selection, and orchestration. Enterprises and developers favor AI tools for rapid prototyping and workflow automation.

Natural Language Processing (NLP) platforms are projected to surge at a 21.9% CAGR through 2032, augmented by chatbot, sentiment analysis, and text analytics proliferation. The adoption in healthcare and BFSI continues to surge as regulatory requirements increase the requirement for explainable and compliant AI models.

Deployment Insights

Cloud-based platforms dominate, constituting approximately 67.4% market share in 2025. Preference for cloud stems from cost efficiency, scalability, and access to distributed AI resources. Enterprises are embracing cloud-native architectures for agile experimentation and deployment.

On-premises or hybrid deployment approaches are gaining traction, providing flexibility for businesses balancing data sovereignty with computational resource scalability. Hybrid adoption is predicted to rise at a 15.2% CAGR as organizations address multi-cloud strategy and compliance requirements.

End-user Insights

The IT and telecom segment retains leadership at nearly 30.2% market share in 2025, reflecting ongoing digital transformation and rising demand for novel analytics in network optimization, customer management, and service delivery. The industry’s rapid tech cycles foster high platform turnover.

The healthcare and life sciences segment is the fastest-growing. It is attributed to stringent regulatory mandates, validated clinical use cases, and increasing demand for precision medicine, predictive diagnostics, and automated coding. The surge in healthcare AI adoption is also fueled by the increasing availability of Electronic Health Records (EHRs), wearable devices, and genomic data.

Regional Insights

North America Artificial Intelligence Platform Market Trends - Public-sector Initiatives Boost AI Deployment

North America accounts for approximately 26.4% of the global market share in 2025, with the U.S. representing 76% of the regional share. Market growth is poised to remain above 19% CAGR through 2032. Key drivers include increasing investments from technology providers, public-sector digital initiatives, and deep penetration of cloud-native infrastructure in healthcare, BFSI, and retail. Venture capital investments and established tech hubs also facilitate rapid development.

North America’s favorable regulatory framework supports widespread adoption. Government agencies advocate for ethical AI standards and fund university-industry partnerships. The market is moderately consolidated, led by giants such as Microsoft, Google, AWS, IBM, and Salesforce. Ongoing merger and acquisition activities raise competition and platform diversity. AI platform start-ups also receive extensive funding for verticalized applications, edge computing integrations, and cross-sector deployment.

Europe Artificial Intelligence Platform Market Trends - Tech Cluster Consolidation Strengthens Development

Europe holds about 22.0% of the global market share in 2025. Germany, the U.K., and France are leading performers, with Germany expected to rise at nearly 18.5% CAGR over the forecast period. Emphasis on ethical frameworks, sustainability, and compliance is prioritized. EU mandates and cross-border partnerships fuel developments, especially in the automotive, energy, and healthcare industries.

Stringent GDPR and impending EU AI Act bolster platform architecture focused on transparency, explainability, and data security. Consolidation of tech clusters in Germany and the U.K., as well as the rise of specialized local start-ups, is augmenting growth. Domestic enterprises employ hybrid cloud adoption strategies to support regulated cross-border operations. EU funding programs and university-industry linkages further underpin growth.

Asia Pacific Artificial Intelligence Platform Market Trends- Collaboration with Cloud Providers Expands Infrastructure Reach

In Asia Pacific, China, India, and Japan spearhead market expansion. Rapid adoption of AI-based manufacturing, fintech, retail, and telecom solutions boosts regional performance. National AI strategies and public investments also accelerate local innovation hubs.

Government incentives, streamlined regulatory environments, and high population density support platform scaling. Various domestic tech leaders from China, Japan, and India are entering global markets. Regional providers collaborate with cloud giants for scalable infrastructure deployment. Significant increases in funding for industrial automation, smart city deployment, and financial sector AI are further expected to drive the market.

Competitive Landscape

The global artificial intelligence platform market is moderately consolidated, with leading global players holding a combined share of over 60%. The structure allows for intense competitive dynamics and frequent strategic moves, including mergers and acquisitions, vertical integration, and global expansion. Specialized start-ups continue to capture niche segments in areas such as healthcare and edge analytics.

Key Industry Developments

- In June 2025, Lenovo expanded its Hybrid AI Advantage platform via collaborations with Cisco, IBM, and NVIDIA. It accelerated the adoption of AI-optimized infrastructure for enterprise applications.

- In May 2024, Siemens partnered with Microsoft to launch Teamcenter X with generative AI tools on Azure. It helped in streamlining product data management and accelerating customer innovation cycles.

Business Strategies

Market leaders pursue innovation-led strategies, focusing on vertical-specific tools, model governance, and responsible AI deployment. Cost leadership through cloud scaling, rapid MLOps implementation, and hybrid expansions remains a key differentiator.

Companies Covered in Artificial Intelligence Platform Market

- Microsoft Corporation

- Amazon Web Services

- Google LLC

- IBM Corporation

- Oracle Corporation

- SAP SE

- Salesforce, Inc.

- H2O.ai

- DataRobot, Inc.

- NVIDIA Corporation

- Infosys Limited

- Infogain Corporation

- Avenga

- Vital AI LLC

Frequently Asked Questions

The artificial intelligence platform market is projected to reach US$20.4 Bn in 2025.

Increasing enterprise adoption of AI and rising demand for natural language processing are the key market drivers.

The artificial intelligence platform market is poised to witness a CAGR of 22.3% from 2025 to 2032.

The growing shift toward low-code AI development platforms and the emergence of ethical AI frameworks represent key market opportunities.

Microsoft Corporation, Amazon Web Services, and Google LLC are a few key market players.