- Non-food Packaging

- Industrial Packaging Market

Industrial Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Packaging Market by Product Type (Drums, I.B.C., Boxes, Sacks, Crates, Pallets, Folding Cartons), Material (Plastic, Paper, Glass, Wood, Metal), Industry (Food & Beverage, Healthcare, Personal Care & Cosmetics, Automotive, Agriculture, Building & Construction, Electrical & Electronics, Misc), Regional Analysis, 2026 - 2033

Industrial Packaging Market Size and Trend Analysis

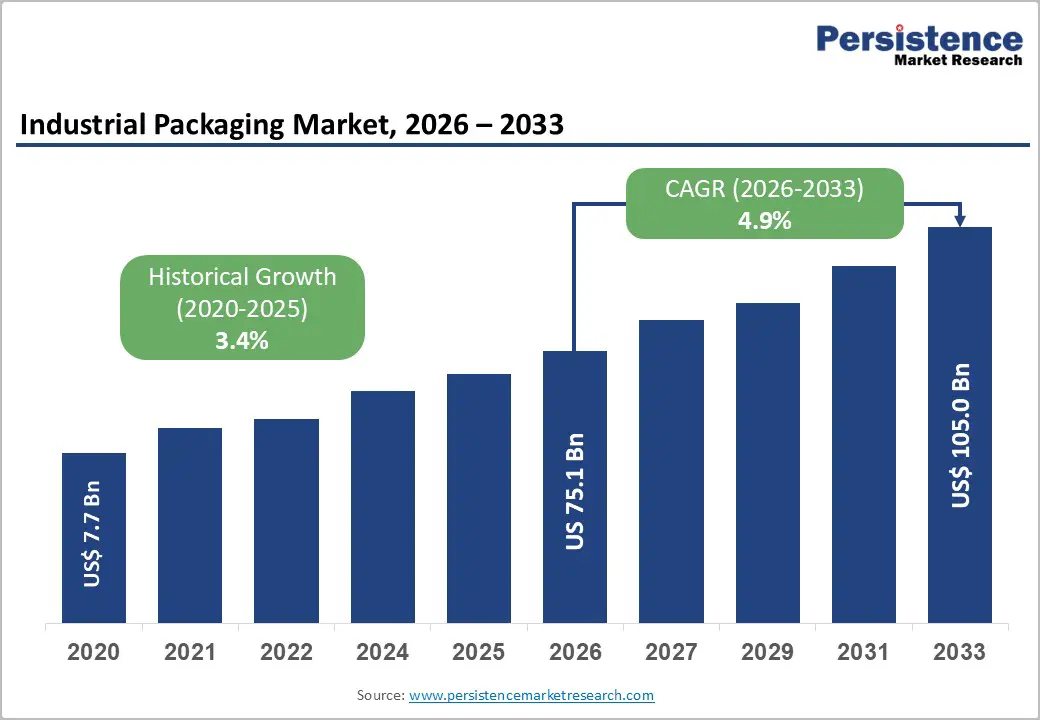

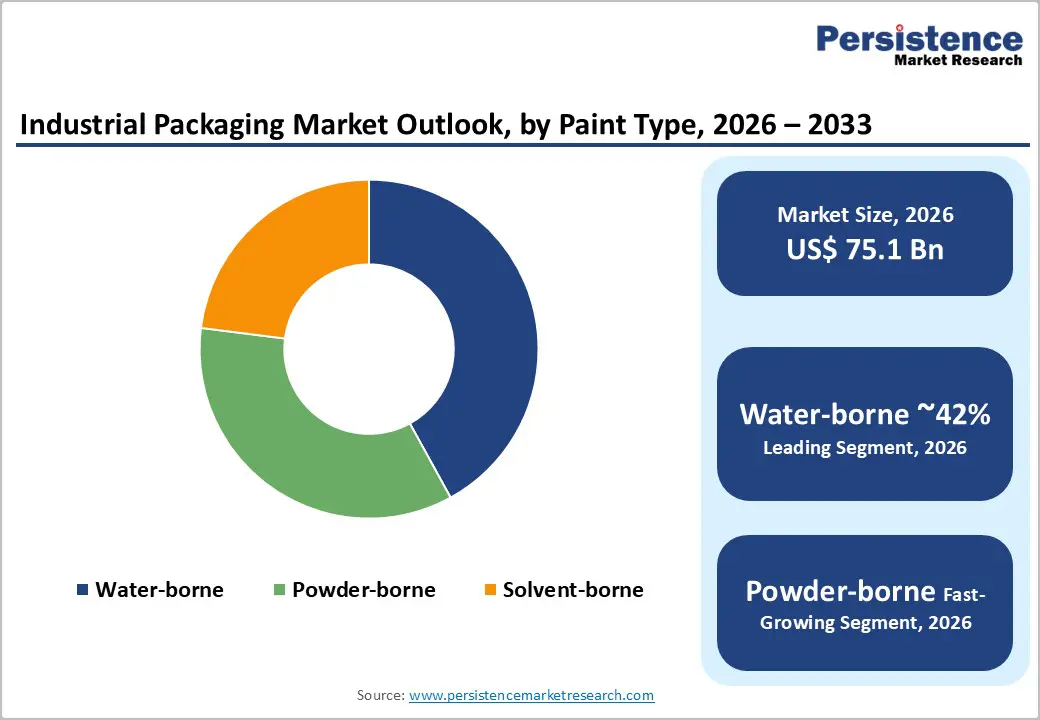

The global industrial packaging market size is likely to be valued at US$ 75.1 billion in 2026 and is expected to reach US$ 105.0 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 and 2033.

Rapid expansion of global manufacturing and cross-border trade is boosting demand for robust packaging that protects goods in long and complex supply chains. Strong growth in sectors such as chemicals, food and beverage, pharmaceuticals, and e-commerce logistics is accelerating the adoption of industrial drums, I.B.C.s, pallets, and crates, especially in emerging economies.

Key Industry Highlights:

| Key Insights | Details |

|---|---|

| Industrial Packaging Market Size (2026E) | US$ 75.1 billion |

| Market Value Forecast (2033F) | US$ 105.0 billion |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 3.4% |

Market Dynamics

Drivers - Global Expansion of Trade, E-Commerce, and Industrial Output Driving Strong Demand for High-Performance Industrial Packaging Solutions

Global trade expansion, growing e-commerce activity, and rising industrial production are steadily increasing demand for reliable industrial packaging solutions, including drums, IBCs, pallets, and corrugated bulk boxes. As international trade recovers from past disruptions, companies are shipping larger volumes of chemicals, food ingredients, and consumer products across complex supply chains, creating sustained demand for durable transit packaging.

E-commerce fulfilment centers and 3PL warehouses are expanding their networks and storage capacity, which further boosts the consumption of high-performance packaging per shipped tonne. At the same time, industrial output in fast-growing regions, especially in chemicals, pharmaceuticals, and automotive manufacturing, is structurally higher, particularly in emerging Asian markets. This shift requires standardized and cost-efficient packaging that ensures cargo protection, supports automated handling, improves cubic space utilization, and meets strict transportation regulations. Together, these factors reinforce the critical role of industrial packaging in enabling safer, faster, and more efficient global movement of goods.

Tightening Sustainability Regulations Accelerating Industry Shift toward Recyclable Materials, Reusable Containers, and Closed-Loop Packaging Models

Environmental regulations and corporate sustainability goals are rapidly reshaping industrial packaging choices by encouraging the use of recyclable, reusable, and lower-impact materials. Governments across major global economies are tightening rules related to extended producer responsibility, plastic waste reduction, and carbon reporting. As a result, companies are increasingly adopting returnable IBCs, steel drums, reusable containers, and corrugated packaging made with high recycled content.

These regulations also support the growth of closed-loop service models, in which providers manage the collection, cleaning, reconditioning, and return of industrial packaging assets. Such models help reduce waste, cut lifecycle emissions, and lower overall ownership costs for customers. Additionally, large manufacturers are integrating sustainability criteria into procurement decisions, favoring packaging options that improve material recovery and reduce reliance on single-use. This regulatory and corporate shift is accelerating industry transformation and creating long-term demand for innovative, greener industrial packaging solutions.

Restraints - Volatile Raw Material Prices and Ongoing Supply Disruptions Creating Cost Pressures and Planning Challenges for Packaging Manufacturers

The industrial packaging sector faces ongoing challenges from fluctuating prices of key raw materials, including resins, containerboard, and steel. These materials are influenced by global petrochemical supply trends, energy market instability, and logistics disruptions, all of which can significantly raise production costs. When supply constraints or sudden price spikes occur, such as during geopolitical events, energy shortages, or shipping delays, manufacturers are forced to adjust prices frequently, pressuring downstream buyers and reducing margin stability.

High input volatility also affects packaging companies' ability to plan capital investments, undertake large-scale product redesign projects, or commit to long-term procurement contracts. Additionally, shortages of polyethylene, polypropylene, and fiber-based materials can delay production timelines and disrupt customer supply chains. Together, these issues limit operational predictability for industrial packaging producers and create financial strain, particularly for smaller suppliers with less bargaining power and inventory flexibility.

Increasingly Complex Regulatory Requirements Raising Compliance Costs and Slowing Innovation for Global Industrial Packaging Producers

Industrial packaging companies must navigate increasingly complex regulatory requirements across hazardous goods transport, food-contact safety, environmental compliance, and waste management. These rules vary widely by country and transport mode, road, rail, sea, and air, and often require specific labeling, tracking, testing, and documentation procedures. Managing this regulatory landscape increases operational costs and demands specialized compliance expertise.

Smaller converters and regional players face particular challenges due to limited resources for certification, audits, and continuous monitoring of regulatory updates. Moreover, overlapping national and international standards can slow product development and extend approval timelines for new packaging designs. Compliance with recycling mandates and extended producer responsibility schemes adds further responsibilities, requiring investments in material traceability and reporting systems. Collectively, these factors increase the cost of doing business and slow the pace at which innovative industrial packaging solutions can be scaled globally.

Opportunity - Rising Demand for Sustainable Materials and Smart Technologies Creating High-Value Innovation Opportunities in Industrial Packaging Solutions

Growing demand for sustainable, high-performance packaging is creating major opportunities for suppliers that can offer recyclable, reusable, and technologically advanced solutions. The shift away from traditional single-use plastics is increasing the adoption of mono-material films, recyclable barrier coatings, and fiber-based alternatives that reduce environmental impact while maintaining required performance. Companies integrating smart features, such as RFID tags, sensors, QR codes, and condition-monitoring devices, are helping industrial customers track shipments, ensure product integrity, and meet stricter traceability standards across sectors such as pharmaceuticals, specialty chemicals, and food ingredients.

As sustainability and digitalization reshape global supply chains, industrial buyers are seeking packaging that delivers durability, efficiency, and environmental benefits simultaneously. These evolving expectations support premium pricing and long-term contracts for suppliers capable of delivering innovative materials, connected packaging, and integrated lifecycle management services.

Rapid Industrialization in Emerging Markets Driving Major Growth Opportunities for Standardized, Durable, and Reusable Industrial Packaging Systems

Rapid industrialization in the Asia-Pacific, the Middle East, and parts of Latin America is driving strong demand for reliable industrial packaging solutions across manufacturing, logistics, and export sectors. Countries such as China, India, Indonesia, Vietnam, and those in the GCC region are investing heavily in petrochemical plants, construction materials, pharmaceuticals, and electronics production. These industries rely on standardized drums, IBCs, pallets, and crates to safely transport bulk liquids, powders, and components.

Growth in export terminals, logistics hubs, and warehouse automation further drives the need for high-quality industrial packaging to support efficient handling and global regulatory compliance. International packaging companies and regional players have significant opportunities to establish localized production facilities, leasing networks, reconditioning services, and value-added consulting. As these economies scale up manufacturing capacity, the demand for modern, durable, and circular industrial packaging systems continues to rise.

Category-wise Analysis

By Product Type Insights

Drums remain the leading product-type segment in industrial packaging, holding nearly 50% share in the industrial bulk packaging market due to their versatility and cost-effectiveness. Steel and plastic drums are widely preferred for chemicals, lubricants, solvents, and food ingredients because they provide standardized capacities and are supported by established handling systems across ports and warehouses. Their cylindrical shape makes stacking and container loading efficient, while compliance with hazardous-materials regulations enables safe transport of dangerous goods. As chemical and pharmaceutical manufacturers increasingly shift to certified packaging under UN and national transport codes, drum usage is expected to remain structurally strong, even as IBCs gain traction in specific bulk-liquid applications.

By Material Insights

Plastic continues to dominate the industrial packaging market, with plastic-based containers and films accounting for the majority of bulk packaging demand. Materials such as high-density polyethylene and polypropylene offer an effective mix of strength-to-weight ratio, chemical resistance, design flexibility, and affordability, making them ideal for drums, IBC bottles, crates, and pallets. At the same time, regulations encouraging recyclability and higher recycled-content usage are pushing suppliers to innovate with improved recycled resins and mono-material designs that simplify recovery. As sustainability targets intensify globally, packaging manufacturers that can provide certified recycled content and reliable closed-loop programs are positioned for long-term growth despite stricter environmental requirements.

By Industry Insights

The food and beverage sector remains one of the largest end-use industries for industrial packaging, as demand for processed foods, beverages, and edible oils directly drives bulk container usage. Flexitanks, drums, IBCs, and corrugated bulk boxes are commonly used to transport liquid sweeteners, fruit juices, dairy ingredients, and alcoholic beverages across global supply chains under strict hygiene and temperature-control guidelines. Oversight from agencies such as the U.S. FDA, EFSA, and regulatory bodies in China and India ensures packaging materials meet food-contact standards, encouraging the use of certified containers and liners. With rising urbanization and increased consumption of packaged foods in emerging markets, this segment is expected to maintain more than 30% of industrial packaging demand in the medium term.

Regional Insights

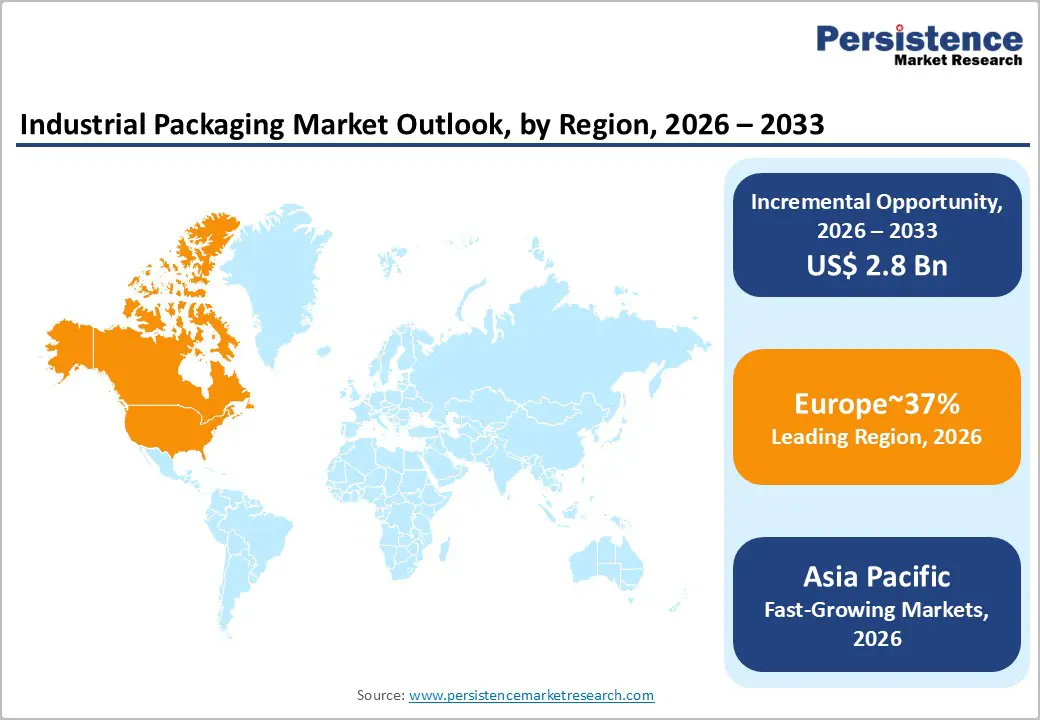

North America Industrial Packaging Market Trends

North America holds a major share of global industrial packaging revenues due to its diverse manufacturing base, advanced logistics ecosystem, and strong presence of multinational companies in chemicals, automotive, and food processing. The United States remains the largest contributor, supported by expanding e-commerce fulfilment infrastructure and renewed interest in regional manufacturing and near-shoring. These shifts are increasing the flow of packaged goods through distribution networks that rely heavily on IBCs, drums, pallets, and heavy-duty corrugated boxes.

Regulatory frameworks related to hazardous materials, recycling, and traceability are encouraging manufacturers to adopt compliant, trackable, and reusable packaging formats. Companies across the region are also accelerating sustainability initiatives by integrating high-recycled-content materials and closed-loop systems. Innovation hubs in the U.S. and Canada are actively exploring IoT-enabled smart packaging, temperature and condition monitoring, and digital product passports, reinforcing North America’s position as a leader in technologically advanced industrial packaging systems.

Europe Industrial Packaging Market Trends

Europe represents a mature but highly innovative industrial packaging market, driven by strong demand from industries such as automotive, chemicals, engineering, and food manufacturing. Countries including Germany, the U.K., France, and Spain rely heavily on standardized pallets, high-performance corrugated packaging, and returnable IBC pools to support efficient cross-border transport across integrated European supply chains.

Regulations under the EU Green Deal, packaging waste directives, and extended producer responsibility schemes are pushing companies toward higher recycling rates, reusable container systems, and carbon-efficient materials. As a result, Europe is at the forefront of circular industrial packaging models, investing in collection, cleaning, and reconditioning networks for drums, IBCs, and pallets. European companies also lead in material lightweighting, digital tracking technologies, and closed-loop programs that reduce waste and improve sustainability. These practices set a global benchmark and are increasingly being adopted by industrial packaging stakeholders in other regions.

Asia Pacific Industrial Packaging Market Trends

Asia Pacific is the fastest-growing region in the industrial packaging market, driven by rapid expansion in manufacturing, exports, and domestic consumption across China, India, Japan, and ASEAN countries. Major investments in chemicals, electronics, automotive components, and food processing have increased demand for reliable packaging solutions, including FIBCs, drums, pallets, and heavy-duty corrugated formats. The region is also emerging as a manufacturing hub for industrial packaging production, supported by competitive costs, growing automation, and large-scale capacity additions.

Government initiatives focused on sustainability, plastic reduction, and improved waste management are accelerating the adoption of recyclable and reusable packaging materials. Markets like China and India are implementing circular economy policies that encourage the use of returnable containers and higher recycled-content products. As manufacturing output and export volumes rise, Asia Pacific continues to strengthen its position as a key driver of global industrial packaging demand and innovation.

Competitive Landscape

The global industrial packaging market is moderately consolidated at the global level, with large integrated groups such as Amcor plc, Mondi Group, Greif, Inc., Mauser Packaging Solutions, WestRock Company, and Berry Global Group, Inc. operating alongside numerous regional and niche specialists. These leaders compete on global supply capability, breadth of rigid and flexible product portfolios, sustainability credentials, and value-added services such as design, testing, leasing, and reconditioning. Strategic priorities include expanding presence in high-growth emerging markets, investing in recyclable and lightweight materials, developing smart and connected packaging solutions, and pursuing mergers, acquisitions, and partnerships to enhance scale and technology depth.

Key Market Developments:

- In January, 2024: Mondi Group announced new investments in paper-based industrial bags and sustainable sack kraft capacity in Europe to meet rising demand for recyclable packaging in construction and industrial markets.

- In June, 2024: Greif, Inc. expanded its intermediate bulk container reconditioning network in North America, adding service centers that support circular economy models for chemical and lubricant customers.

- In September, 2023: Berry Global Group, Inc. introduced high-recycled-content heavy-duty industrial films targeting pallet unitization and bulk transport, aligning with brand owners’ packaging sustainability targets.

Companies Covered in Industrial Packaging Market

- Amcor plc

- International Paper Company

- Sealed Air Corporation

- Smurfit Kappa Group plc

- Sonoco Products Company

- WestRock Company

- Mondi Group, Greif, Inc.

- Berry Global Group, Inc.

- Bemis Company, Inc.

- Schoeller Allibert

- Time Technoplast Ltd.

- Mauser Packaging Solutions

- Schutz GmbH & Co. KGaA

- Global-Pak, Inc.

- Werit Kunststoffwerke

- W. Schneider GmbH & Co. KG

- Schaefer Systems International, Inc.

- DS Smith plc

- Nefab Group

Frequently Asked Questions

The global industrial packaging market is expected to reach around US$ 105.0 billion by 2033, up from about US$ 75.1 billion in 2026, reflecting a forecast CAGR of 4.9% during 2026-2033.

Demand is driven by expansion of global trade and e-commerce, growth in manufacturing sectors such as chemicals, food, and pharmaceuticals, and strengthening regulatory and sustainability requirements that favor high-performance, compliant packaging.

Drums constitute the leading product-type segment, accounting for close to 50% share in industrial bulk packaging because of their versatility, standardized sizes, and strong suitability for hazardous and non-hazardous materials.

North America and Europe together hold a significant share of global revenues, supported by mature industrial bases, while Asia Pacific is expected to be the fastest-growing region because of rapid industrialization and export-oriented manufacturing.

A major opportunity lies in sustainable and smart industrial packaging that combines recyclable or reusable materials with digital traceability and condition monitoring, helping customers meet regulatory, cost, and environmental objectives simultaneously.

Key players profiled in the industrial packaging market report include Amcor plc, International Paper Company, Sealed Air Corporation, Smurfit Kappa Group plc, Sonoco Products Company, WestRock Company, Mondi Group, Greif, Inc., Berry Global Group, Inc., Mauser Packaging Solutions, and others that provide a broad range of rigid, flexible, and service-based industrial packaging solutions.